I Am a Buyer of This Low-Priced Tech Stock After a Big Government Contract

Palantir tried to break out following a Department of Defense announcement and I'm a buyer based on some key fundamentals.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Our, or should I say my, former "Stocks Under $10" portfolio holding and current personal holding tried to break out on Thursday. Of course, I speak of Palantir Technologies PLTR.

There was news. On Wednesday evening, the U.S. Department of Defense (DoD) announced that Palantir had been awarded a $480 million fixed-price contract for a prototype for the Maven Smart System (artificial intelligence) prototype. The internal DoD client is the U.S. Army Contracting Command at the Aberdeen Proving Ground in Maryland.

Palantir had already been a participant in the DoD's surveillance and targeting system known as "Project Maven." The idea is to process imagery and full-motion video from unmanned aircraft and vehicles and automatically detect potential or probable targets. The Pentagon, last year, had let on that Maven had been developed and demonstrated using Palantir's cloud platform that had been customized so as to be mission capable. The platform has also demonstrated an ability to be scaled, which would be key on future battlefields against peer or near-peer adversaries.

The same day, Palantir and Eaton ETN announced a deepening of their already existing collaboration to bring Palantir's AIP (artificial intelligence platform) to Eaton's power management operations. Eaton currently operates in roughly 160 countries and this deepening relationship would accelerate Eaton's impact on powering the clean energy revolution.

Remember The Fundamentals

For the quarter that ended on March 31, 2024, Palantir generated operating cash flow of $129.579 million. Add that flow to the $21.719 million in employer payroll taxes related to the firm's stock-based compensation expense, and then we subtracted the firm's quarterly capex spending of a mere $2.664 million. That left free cash flow of $148.634 million.

On to the balance sheet, Palantir ended that period with a cash position of $3.868 billion and current assets of $4.436 billion. Current liabilities added up to just $750.553 million, including $237.634 million in deferred revenue, which we remember is not a financial obligation, but one of goods or services owed. There is no short-term or current debt on the books. This left the firm's current ratio at a very muscular 5.91. Once we adjusted for deferred revenues, the current ratio rises to an absolutely-herculean 8.65.

Total assets amounted to $4.807 billion. The firm claims no value for intangible assets. It does not need to, and we appreciate that. Total liabilities less equity came to $945.907 million. There is not only no short-term debt on this balance sheet, but no long-term debt either. No debt of any kind.

Ever see a balance sheet this magnificent? You may search, but a quality find like this is rare. This balance sheet, as I have mentioned in the past, is a reason on its own merits to invest in this name.

I Know... The Guidance

The guidance provided three weeks ago did not knock folds over. I get it. For the current quarter, Palantir saw revenue of $649 million to $653 million. This was seen as mildly disappointing with Wall Street looking for $653 million. For the full year, the firm projected revenue of $2.677 billion to $2.689 billion. Again, Wall Street was looking for something around $2.69B.

That said, the firm now expects U.S. commercial clients to drive revenue of $661 million, which would be growth of at least 45%. Keep that in mind. Government contracts like the one dished out by the army above are the lifeblood of the firm, but the growth will have to come from the commercial side as revenue will have to keep pace with customer count, which is growing like a weed. As an investor, I think it likely that AI, like cybersecurity, is one space that managers cannot afford to go cheap on.

Full year adjusted operating income is seen at $868 million to $880 million and free cash flow is seen for the full year at $800 million to $1 billion as well. Palantir still expects both GAAP operating and GAAP net income to remain profitable for each quarter of the year.

Plan of Action

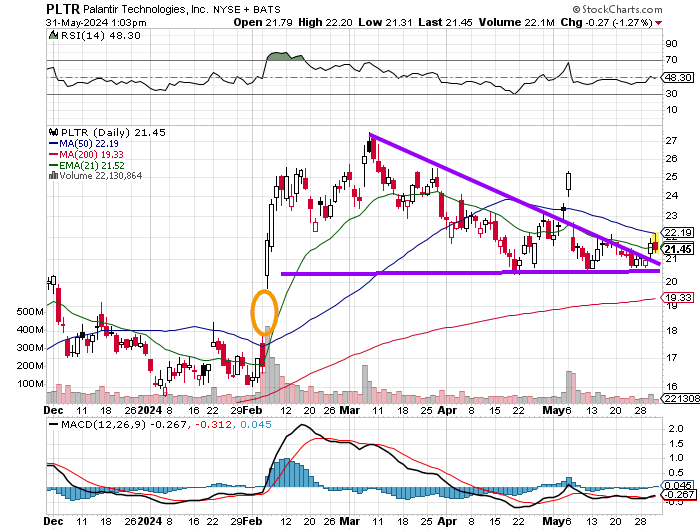

Readers will now see that our descending triangle has closed. This often brings volatility and can be seen as bearish. The stock tried to break out on the U.S. Army news, but has gotten caught up in Friday's broad, market-wide sell off. The stock did touch its 50-day SMA but has not retaken the level. The unfilled gap that would need a tick at $19.76 or lower to fill runs close to the 200-day SMA. I am a buyer down to the 200-day line — more aggressively should the gap actually fill. To the upside, the 50-day SMA remains the pivot, while I reiterate my $29 target price.

At the time of publication, Guilfoyle was long PLTR equity.