Buffett Is Sharp as a Tack, So There's No Reason to Sell Berkshire Now

The co-chairs, or leaders in waiting have done nothing to unearn our trust. That said, the two have not yet earned our trust either.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It wasn't meant to feel like a hollowed out annual meeting. Maybe it did not feel that way for those in attendance. For those of us who merely spectated from hundreds or thousands of miles away, there was something clearly missing.

That something was Berkshire Hathaway BRK.A, BRK.B CEO Warren Buffett's former right-hand man, and nearly life-long pal, Charlie Munger. Munger passed away last November just short of his 100th birthday, and with his death, the global mean IQ inched just a bit lower.

As a matter of fact, Buffett brought his audience to both tears and cheers when answering a question posed by a child named Andrew. The boy asked Buffett what he would do if he had one more day with Charlie. Buffett answered the question by talking about his long list of adventures and misadventures with his friend and then challenged Andrew to find his "pal" going forward.

At the end of the day though, this was a corporate annual meeting and the annual meeting type agenda did take over.

News!!

That headline making news that came out of the meeting was the fact that Berkshire had reduced the firm's long position in Apple AAPL more aggressively during the first quarter of 2024 than it had during Q4 2023. Berkshire cut its stake in AAPL by 13% from 905M shares down to a still whopping 790M shares. This is still easily Berkshire's largest long position.

Despite the reduction in shares held. Buffett had this to say about a few of his favorite stocks... "American Express AXP and Coca-Cola KO are wonderful businesses. Apple is an even better business. We will own Apple when Greg is running this place."

That brings us to the elephant in the room. The plan of succession. With Munger gone, and Buffett no longer a teenager, the plan seems to already be in its early implementation stages. Munger was joined on stage by vice chairmen Greg Abel and Ajit Jain. It does seem to this amateur viewer that the plan appears to be to set Abel up as sort of a Buffett, with Jain as something of a Munger.

That of course, is not official. That is more the musings of a small investor trying to decide whether or not to stick with his long position in BRK.B, which has done quite well over the past year and a half or so. Since late September 2022, BRK.B is up 49%. That's to my less than stellar execution and trading around the core position, my position is up just 34%.

Other than the reduction of AAPL and the ascension of Abel and Jain, or should I say... Jain and Abel, we learned that Berkshire had completely exited Paramount Global PARA at a loss and that the firm's cash position was up to a nearly staggering $189B.

Q1 Operations

There was good news. Operating earnings were up 39% to $11.222B from the year ago comparison. However, investment gains were down huge from $27.439B a year ago to $1.48B for the quarter reported. After accounting for interest and taxes, GAAP net earnings attributable to shareholders dropped to $12.702B from $35.504B. That works out to $8,825 per A share (down from $24,377) or $5.88 per B share (down from $16.25).

Among the three largest businesses, Insurance underwriting contributed operating earnings of $2.598B (+185%), while Insurance investment income contributed operating earnings of $2.598B (+32%), which is not a misprint. BNSF (the railroad) contributed $1.143B in operating income, which was down 8.3%.

Fundamentals

For the period covered, Berkshire generated operating cash flow of $10.566B, while spending $4.393B on capital expenditures. This left free cash flow of $6.173B, up from $4.98B for the year ago quarter. The firm did not return capital to shareholders.

Glancing at the balance sheet, the firm's cash position comes to just under $189B, not including another $335.864B in equity investments. Total assets amount to $1.07T, which includes $113.594B in goodwill and other intangibles. Total liabilities less equity comes to $492.25B including $82.031B in debt. All in all, this balance sheet, though not organized in the way that most public corporations lay things out, is in very, very good health.

My Thoughts

Do I think about taking my leave of this stock? Of course. One thing we learned over the weekend, is that Warren Buffett, a man whom I accidentally spoke to on the phone not once, but twice, is still as sharp as a tack. Even without Charlie Munger. He is 93 years old. Hopefully not for a long time, but that day may come. He even made a half joke as the meeting closed that he hoped to be there next year.

The co-chairs, or leaders in waiting have done nothing to unearn our trust. That said, the two have not yet earned our trust either. I imagine on that day that hopefully is well off into the future, the shares will sell off sharply. I am not going to sell the stock today because the healthy chair, who is clearly still with it, is playing in his late innings. I'll worry about that future selloff when it happens, not before.

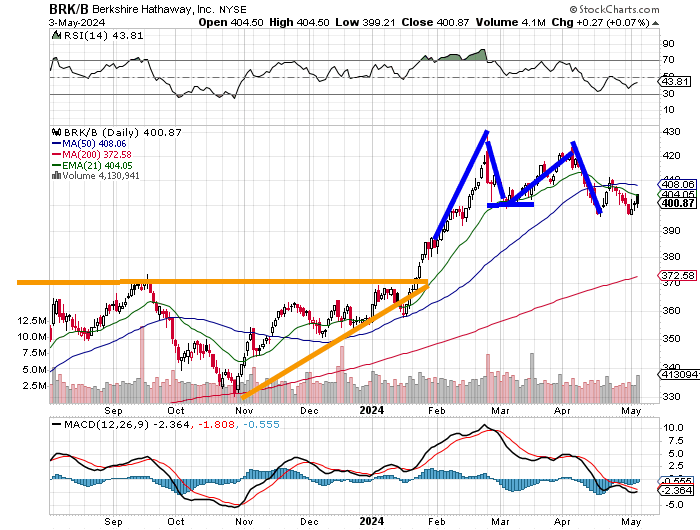

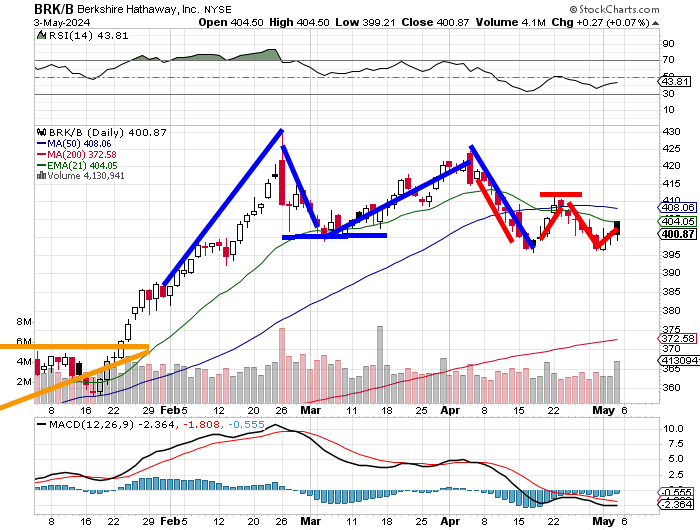

Readers will see that in late 2023, BRK.B developed an ascending triangle that in turn produced a breakout. That breakout culminated with a double top reversal that took course from February into April. The downside $400 pivot should have provided enough fuel to take the stock down into the $340/$350 range. Something changed though. Let's zoom in...

The breakdown from pivot failed almost immediately. A small, but definitely there double bottom reversal formed with $395 support and a $411 pivot. Relative strength is non-committal, while the daily MACD (moving average convergence divergence) remains bearish looking.

Perhaps this morning's pop will improve that MACD. Not that the 50-day SMA (simple moving average) now stands in between the stock and that pivot I mentioned. The pivot is either one or the other. I would think the recent high would outrank the moving average, but that's really splitting hairs at this point.

My target price is currently $472. On a sell-off, I'll add just above the $200-day SMA, but this is a big but. I will turn seller upon the break of that thin red line.

At the time of publication, Stephen Guilfoyle was long BRK.B, AAPL equity.