What Comes Next? Charting the Trend, Buffett's Annual, Strong Earnings, Week Ahead

Here's why market participants may get a chance to catch their collective breath this week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Rock! Rock! (Till You Drop)

I said, rock, rock 'til you drop

Rock, rock, never stop

Rock, rock, 'til you drop

I say, rock, rock, 'til you drop

Ridin' into danger, laughin' all the way

Fast, free and easy, living for today...

- Lange, Clark, Allen, Savage, Elliott, Willis (Def Leppard), 1983

The Unknowable

Hear it? Feel it? Taste it. Prepare thyself for what comes next. For what comes next is surely the unknowable. It's all going to be okay. They say. Hope so. Market participants may get a chance to catch their collective breath this week.

The macroeconomic calendar is rather quiet, by macroeconomic standards. The earnings calendar is not really that thin when measured in sheer numbers, but the headline level corporations reporting their numbers will be few and far between. My guess? I only see a handful of speakers on this week's docket, but I would expect the days ahead to fill in with Fed officials making public appearances that either haven't yet committed to or that I have not yet picked up on.

We do know that over the past couple of weeks, the economic data that has been released, has appeared to weaken relative to where these data-points hover through the second half of 2023. Over the past two weeks, we have seen weakness or renewed weaknesses across a number of regional and national manufacturing and service sector surveys, across data for non-farm productivity, and employment, and data covering construction spending.

On top of that, consumer confidence has become a lot less confident as the costs associated with retaining labor have absolutely soared for employers.

Growth? or Growth!

Two weeks ago, Q1 GDP hit the tape at growth of 1.6% q/q, SAAR. Well below expectations, but still not crisis-like. The data since the end of the first quarter, to the somewhat astute (I hope) observer, seems to have weakened. Somehow, the Atlanta Fed's GDPNow model for the second quarter is running at growth of 3.3%. Hmm. Interesting.

What do the other regional Fed districts that run real-time GDP models have to say about this? The New York Fed's model currently stands at a far more believable 2.23%, as St. Louis has not generated a first Q2 estimate just yet.

It should be noted that St. Louis, at 1.71% easily modeled Q1 the most accurately among this group as both New York and St. Louis overestimated activity for that period as well. Cleveland, which has been low all along, has Q2 modeled at growth of 0.71%.

The Week That Was

The market focus for the past week was split in three directions. First, markets were focused on earnings releases by many firms in what was perhaps the most active stretch of earnings season, but really centered that attention on both Amazon AMZN and Apple AAPL.

Those two headliners turned out to be crowd pleasers. Amazon showed growth in all the right places, especially AWS and advertising, while Apple turned in a quarter that was far better than feared, while showing investors their "big bazooka" of a US record $110B share repurchase authorization that dragged a dividend increase along with it for good measure.

Earnings might have held the attention early, but the real show-stoppers last week were the FOMC policy decision on Wednesday and the results of the April employment surveys posted by the BLS on Friday. What was not to like for investors who perhaps cannot always see past their nose?

The Fed was more dovish than expected, and probably more dovish than they should have been as the current "quantitative tightening" program was curbed more aggressively than anyone expected, and Fed Chair Jerome Powell all but promised that the next adjustment made by the Fed on rates would not likely be an upward move.

Then it was on to the April employment numbers. I know, after what BLS quietly released back on April 24th (The Q3 BED report), it becomes very difficult for any self-respecting economist, trader, investor or even student for that matter, to take the monthly Non-Farm Payrolls numbers seriously. Alas, we must though, as all involved understand that keyword reading algorithms control price discovery across financial markets, and those algorithms do not understand that the NFP number has become a running joke on Wall Street.

Therefore, we must play the game with numbers we know will likely be revised significantly down the road. Those numbers still managed to disappoint. Just a week after the BLS told us that these monthly surveys were basically blowing smoke for much of 2023. Who would have thought it? Bottom line... the pace of job creation slowed in April. Wage growth slowed in April. Unemployment increased in April. Underemployment increased in April. That's if the numbers hold, which is no sure thing.

Treasuries rallied. Equities rallied. Party-time. Yay.

We're Talkin' Stocks

Equities for the most part, put in a second winning week in a row, on increased trading volume. rather impressive. The S&P 500 gained 1.26% on Friday to swing the week into the win column, up 0.55%. The Nasdaq Composite gained 1.99% on Friday to close the week up 1.43%. The Russell 2000, Dow Transports, and KBW Bank Index all posted winning sessions on Friday and winning weeks.

Among the major and mid-major indexes, only the Philadelphia Semiconductor Index closed in the red, at -0.4% even after gaining 2.41% on Friday.

For the week, nine of the eleven S&P sector SPDR ETFs closed in the green, led by the more defensive funds. The Utilities XLU ran 3.35%, while the REITs XLRE gained 1.54%. Technology XLK finished in third for the week despite the weakness in both the semis and in software.

Apple was up 8.32% for the week to lead the Dow Jones US Computer Hardware Index that was up 7.34%. Within that index, Roku ROKU was also up 4.9%. Energy XLE was slapped around pretty hard (-3.31%)

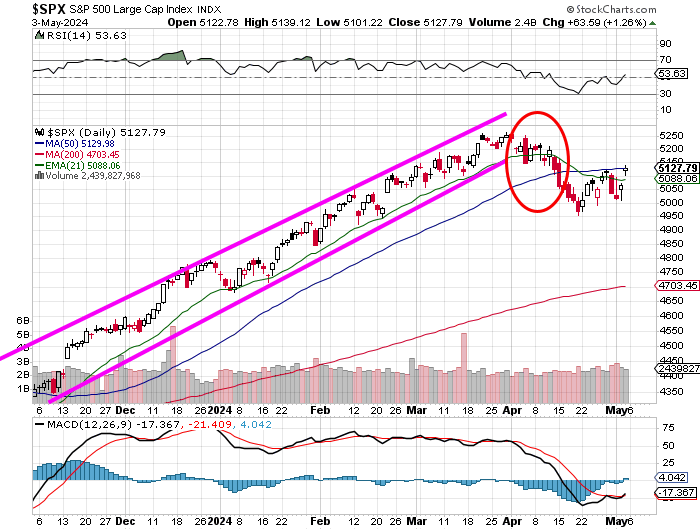

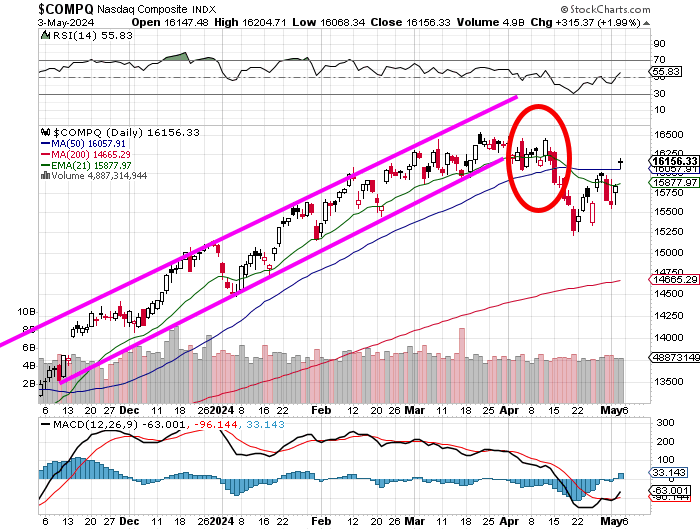

The Charts

Last week, we discussed the possibility that we had tripped across yet another (this time upward) change in trend. Yes, we did nail the change in trend on the downside. I am still not convinced the upward movement of late is for keeps. Let's take a look.

Still, the red candle days stick out for the S&P 500. The Index itself, readers will see, failed to take and hold the important 50-day SMA (simple moving average). Relative strength remains neutral. The daily MACD (moving average convergence divergence), is still struggling to turn more bullish.

The 12-day EMA (exponential moving average) still has not overtaken the 26-day EMA like the bulls need it to. The histogram of the 9-day EMA has finally broken above zero, but that's real tentative. The MACD needs this index to take that thin blue line.

Now, that's much more like it. See how the Nasdaq Composite tells a different story this week? The index has indeed taken the 50-day SMA (simple moving average) and indeed held that line going into the weekend. Still, the red candle days do appear to have occurred on higher trading volume than do the "up" days. That's a little bit cautionary.

I cannot yet confirm an upward change in trend. I'd love to, so I could be more aggressive. Perhaps this week. Then again, maybe not. If self-discipline were easy, we wouldn't be special.

Berkshire Hathaway Annual Meeting

- The Berkshire Hathaway BRK.A BRK.B meeting put the spotlight on Greg Abel as Warren Buffett's eventual successor both in running the firm and in selecting investments. This is a priority now with last November's passing of Charlie Munger.

- Berkshire pared back the firm's long position in Apple, easily its largest holding, by 13% to 790M shares (from 905M) during the first quarter.

- Berkshire is out of the firm's long position in Paramount Global PARA at a loss. In Buffet's words, Berkshire lost "quite a bit of money" on Paramount.

- Berkshire, at the end of Q1, was sitting on a $189B cash position.

Earnings

This earnings season just keeps getting stronger. According to FactSet, which readers well know, is my earnings-related "go-to", with 80% (up from 46%) of the S&P 500 having reported for this season, 77% of S&P 500 companies have beaten earnings expectations, while 61% have beaten sales projections.

First quarter earnings are running at a blended (results & expectations) year over year growth rate of 5.0%, up from 3.5% a week ago and just 0.5% two weeks ago. Revenue growth is now running at 4.1%, up from last week's 4.0%. For the full calendar year, still according to FactSet, earnings are now seen growing 11%, up from 10.8% last week on revenue growth of 4.9%, down from 5%.

To this point, Communication Services are running the hottest, at growth of 34.9%, with the Utilities in second place at +26.7%. Three sectors, Materials, Energy, and Health Care are all suffering year over year earnings contractions of greater than 20%.

After all of that, the S&P 500 ended last week trading at 19.9 times forward looking earnings, down from 20 times a week ago. This is still above the five-year average of 19.1 times and ten-year average of 17.8 times for the index.

The Week Ahead

As mentioned above, there's not a lot of wood to cut this week. On the macro side, we'll have to get through a few Fed speakers led by Fed Vice Chair Philip Jefferson around midday on Wednesday. The Fed will release its quarterly Loan Officer Survey this (on Monday) afternoon, and the University of Michigan will release the preliminary version of its consumer sentiment survey for may on Friday morning. That survey will include closely watched results for inflation expectations.

Away from that, the US Treasury will go to auction with $42B worth of brand-new Ten-Year Notes and $25B worth of new Thirty-Year Bonds this week on Wednesday and Thursday, respectively.

On the corporate side, this will be another heavy week of earnings releases. Just not a heavy week of high-profile earnings releases. Six of the seven "Mag 7" stocks have reported, Nvidia NVDA is still out there, but will not report still for a couple of weeks.

Among those names that would be considered "headliners" that are reporting this week will be Palantir Technologies PLTR, the Walt Disney Company DIS, Uber Technologies UBER, Arm Holdings ARM, and Robinhood Markets HOOD.

Economics (All Times Eastern)

14:00 - Fed's Quarterly Loan Officer Survey.

The Fed (All Times Eastern)

12:50 - Speaker: Richmond Fed Pres. Tom Barkin.

13:00 - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BNTX(-1.35), SAVE (-1.45), TSN (.40)

After the Close: GT (-.01), IFF (.87), PLTR (.08), RKLB (-.08)

At the time of publication, Stephen Guilfoyle was long PLTR, RKLB, AMZN, AAPL, BRK.B, DIS equity.