After Bullish Run, Things Could Be Changing for Apple

Apple reported a solid quarter but there are some bearish price trends developing.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The greatest consumer electronics company of all-time, the $3.35 trillion giant, Apple AAPL released the firm's fiscal third quarter financial results on Thursday evening. For the three-month period ended June 29, 2024, Apple posted a GAAP EPS of $1.40 on revenue of $85.777 billion. These top- and bottom-line results both handily beat Wall Street's expectations. The sales number reflected year-over-year growth of 4.9%, which was Apple's best quarter in terms of year over year sales growth since the September (fiscal fourth) quarter of 2022.

CEO Tim Cook, during the accompanying conference call, addressed the elephant in the room, which is the integration of generative AI into Apple software running on Apple hardware. Cook allows that the firm is investing heavily in this technology that will iPhone users using an iPhone 15 Pro or higher will be required to make use of. The iPhone 16's will likely not be introduced until September 2024.

CEO Tim Cook Comments

"At our Worldwide Developers Conference, we were thrilled to unveil game-changing updates across our platforms, including Apple Intelligence. Apple Intelligence builds on years of innovation and investment in AI and Machine Learning," Cook said.

"Siri also becomes more natural, more useful, and more personal than ever," he added. "Apple Intelligence is built on a foundation of privacy, both through on-device processing that does not collect users' data and through private cloud compute, a groundbreaking new approach to using the cloud, while protecting users' information powered by Apple silicon. We are also integrating ChatGPT into experiences within iPhone, Mac, and iPad, enabling users to draw on a broad base of world knowledge."

Operations

As revenue grew 4.9% to $85.777 billion, sales of products grew 1.6% to $61.564 billion, and services driven revenue increased 14.1% to $24.213 billion. The cost of sales increased 2% to $46.099 billion, leaving a gross profit of $39.678 billion (+9%) on a gross margin of 46.3%. That was up from 44.5% and better than expected. segregated, products gross margin came to 35.3%, down from 35.4%, while services gross margin printed at 74%, up from 70.5%, and well above consensus view.

Operating expenses printed at $14.326 billion (+6.8%), which left an operating income of $25.352 billion, good for growth of 10.2%. After accounting for other income, interest and taxes, net income landed at $21.448 billion (+7.9%). This works out to $1.40 a diluted share, up from $1.26 for the year ago comparison and about five cents above consensus view.

Geographic Sales Performance

- Americas generated revenue of $37.678 billion (+6.5%), beating expectations

- Europe generated revenue of $21.884 billion (+8.3%), beating expectations

- Greater China generated revenue of $14.728 billion (-6.5%), short of expectations

- Japan generated revenue of $5.097 billion (+5.7%), beating expectations

- Rest of Asia Pacific generated revenue of $6.39B (+13.5%), beating expectations

Category Sales Performance

- iPhone generated revenue of $39.296 billion (-0.9%), beating expectations

- Wearables, Home & Acc. generated revenue of $8.097 billion (-2.3%), beating expectations

- iPad generated revenue of $7.162 billion (+23.7%), beating expectations

- Mac generated revenue of $7.009 billion (+2.5%), slightly short of expectations

- Services generated revenue of $24.213 billion (+14.1%), beating expectations

Guidance

As always, what guidance Apple offers the public is limited and vague at best. The firm is projecting a 1.5% full-year negative impact on revenue due to currency exchange rates. Comments in parentheses are my own:

During the call, CFO Luca Maestri said, "We expect our September quarter total company revenue to grow year-over-year at a rate similar to the June quarter (which was 4.9%). We expect services revenue to grow double digits at a rate similar to what we reported in the first three quarters of this fiscal year (14.1% form this past quarter). We expect gross margin to be between 45.5% and 46.5%. (Wall Street was looking for 45.7%, so that's a positive). We expect OpEx to be between $14.2 billion and $14.4 billion (that's below the $14.5 billion consensus, another positive)."

Fundamentals

For the period reported, Apple generated operating cash flow of $28.858 billion. Out of that number came $2.151 billion in capex spending leaving free cash flow of $26.707 billion. Through the first nine months of the fiscal year, Apple has generated operating cash flow of $91.443 billion. Out of that number has come capex spending of $6.539 billion, leaving free cash flow of $84.904 billion. From that number has come repurchases of common stock worth $69.866 billion and cash dividend payments to shareholders of $11.267 billion.

Turning to the balance sheet. Apple's cash position is a little tricky. The firm has $61.801 billion in cash, cash equivalents and marketable securities labeled as current. It has another $91.24 billion in marketable securities not listed as current. So, the cash balance is $153.041 billion, though most of it is not meant to be touched this year. Inventories come to $6.165 billion as current assets stand at $125.435 billion. Current liabilities add up to $131.624 billion, including $2.994 billion in short-term debt and $8.053 billion in deferred revenue.

At the headline, that comes to current and quick ratios of 0.95 and 0.91. Not so hot, but if the entire cash position was labeled as current, which is what every single other public company does (I think), and we adjust for that using the entire cash position as well as the deferred revenue, which is not a true financial liability, Apple's adjusted current and quick ratios improve to a far more palatable 1.75 and 1.70, respectively.

Total assets amount to $331.612 billion. This includes no goodwill nor anything else intangible in nature. I am sure Apple's brand name and product copyrights are worth plenty. Total liabilities less equity comes to $264.904 billion including $88.196 billion in longer-term debt. The debt-load sounds huge, but the firm could if it had to, pay it all off out of pocket and leave a cash position of more than $60 billion.

Wall Street

Since these earnings were released last night, I have come across 17 highly-rated (four-plus stars at TipRanks) sell-side analysts that have opined on AAPL. After allowing for changes, we have 13 "buy" or buy-equivalent ratings, three "hold" or hold-equivalent ratings and one outright "sell" rating. One of the "holds" did not set a target price, so we are working with 16 of those.

The average target price across these 16 analysts is $246.63 with a high of $300 (Ananda Baruch of Loop Capital Markets) and a low of $186 (Tim Long of Barclays). Once omitting those two as potential outliers, the average target across the other 14 rises to $247.14.

My Thoughts

A very solid quarter across the board for Cook and his firm. No runaway growth anywhere, and there will be none as far as the eyes can see. Is that OK? The firm is a cash-producing beast. Maybe it just has to keep on keeping on. Rely on the installed base, which seems to set a record every quarter, to keep the customers who subscribe to the high-margin services product line from going elsewhere. The plan has been working for quite some time. The firm has not launched a successful new product (key word: successful) since the cows came home. Right now, that's still fine. Should something come along and disrupt the status quo, Apple might have no answer, but that is probably not today's problem.

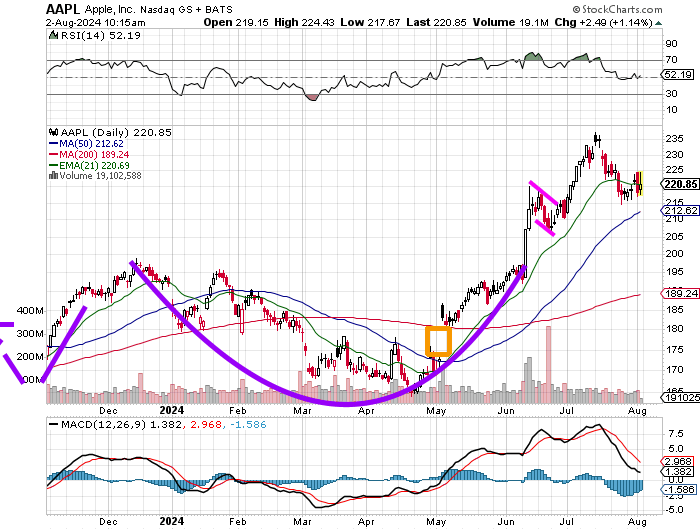

Readers have seen this cup pattern and the bull flag already. These bullish patterns have run their course and are no longer of consequence. Something else is brewing though, and it ain't that sweet to look at.

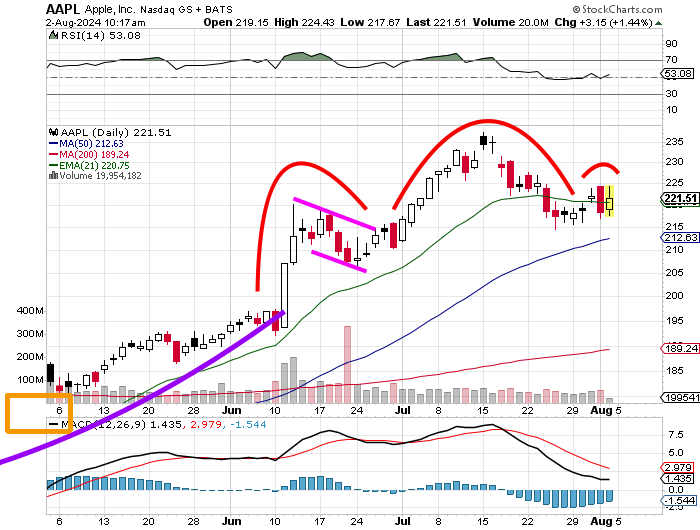

Readers will now see a head-and-shoulders pattern forming that's not complete just yet. This is bearish and is currently coupled with a bearishly postured daily MACD. How bearish? I don't know because we do not yet have a neckline. This morning's pop amid a weak tape might seem encouraging, but it also may just be the right shoulder filling out. I would look for a major test at the 50-day SMA ($213) and if that fails the breakout area from early June which may coincide at that time with the 200-day SMA could present as a truly interesting opportunity to get long or get longer these shares. Of course, I am talking about a 14% discount on a day that the shares are up, but that is what the chart is telling me.

At the time of publication, Guilfoyle was long AAPL calls and AAPL puts.