All Hail Microsoft CEO Satya Nadella as Earnings Explode: Here's the Trade

Cash flows are beastly. The balance sheet is in outstanding condition.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday afternoon, two charter members of the "Magnificent Seven" went to the tape with their quarterly financial results. From Redmond, Washington... Microsoft MSFT released the firm's fiscal first quarter data. The crowd cheered. Almost simultaneously, from Mountain View, California... Alphabet GOOGL released its third quarter results. This time, the crowd booed and hissed. This is that story, obviously from the view of a Microsoft shareholder.

For the three month period ended September 30th, Microsoft posted a GAAP EPS of $2.99 on revenue of $56.517B. The top line beat Wall Street by almost $2B, as the bottom line did so by a rough $0.34. In short, Microsoft crushed the consensus view. While that revenue print was good for year over year growth of 12.8%, the cost of that revenue increased 5.5% to $16.302B. This put gross profit at $40.215B (+16%) on a gross margin of 71.16%. That was up from the year ago comparison of 69.17%.

Slicing and dicing a little deeper, services driven revenue increased 19.2% to $40.982B, producing a gross profit margin of 68.8%. Product driven revenue actually decreased 1.3% to $15.535B, but produced a gross profit margin of 77.3%.

Operating expenses increased just 1.3% to $13.32B, which allowed operating income to grow an impressive 25% to $26.895B. This left operating margin at 47.6%, up dramatically from 42.9% for the year ago comp. After accounting for interest and taxes, net income was left at $22.291B (+27%) as net margin improved from 35% to 39.4%.

Segment Performance

- Productivity and Business Processes drove sales of $18.592B (+12.9%), producing an operating income of $9.97B (+19.8%). Microsoft 365 experienced a q/q increase in paid subscriptions from 74.9M to 76.7M. Microsoft Office saw a 17% (constant currency) revenue increase.

- Intelligent Cloud drove sales of $24.259B (+19.4%), producing an operating income of $11.751B (+30.9%). This segment beat consensus decisively. Within the group, Azure and cloud services produced 29% y/y growth crushing estimates that were down around 26%. Microsoft told us last night that AI infrastructure for Azure is (in the firm's opinion), the best for both training and inference. Microsoft also told us that Azure took share for cloud services during the quarter. We now know or think that at least some of that share came from Alphabet's Google Cloud after seeing that firm's report last night. We'll hear from Amazon AMZN on AWS on Thursday afternoon.

- More Personal Computing drove sales of $13.666B (+2.5%), producing an operating income of $5.174B (+22.7%). Noted here is the segment's return to revenue growth. Leading the growth was a 12% pop for Xbox content and services as well as a 4% increase for Windows OEM. The real impressive part of this segment's performance however was the dramatic increase in profitability.

Guidance

There was no guidance provided in the press release. Those interested either had to listen to the call or read through the transcript. For the current quarter, broken out by segment, the firm sees revenue growth of 11% to 12% for Productivity and Business Processes to $18.8B-$19.1B driven by Office 365 and Microsoft Copilot 365, which has AI capabilities built into the software. Early trials show significant gravitational pull toward this product from those who have tried it.

For Intelligent Cloud, revenue is expected to grow 17% to 18% landing at $25.1B-$25.4B. Expected growth for Azure is seen at 26% to 27%. This is well above the growth rate expected by Wall Street.

For More Personal Computing, revenue is seen at $16.5B to $16.9B, with Windows OEM growing in the mid to high single digits as PC volumes look to be similar to Q1. A decline is seen in device sales as the firm's focus there turns to margin.

Put together, the firm as a whole is likely looking for revenue growth of 14.5% to 16.4%, as operating margins are expected to print flat year over year.

Fundamentals

For the quarter reported, Microsoft generated operating cash flow of $30.583B (+31.8%). Out of this came CapEx of $9.917B, which was a little more than expected. This left free cash flow of $20.666B (+22.2%). Out of that number, the firm paid out $5.051B in cash dividends to shareholders, repurchased $4.831B worth of common stock for the firm's treasury and repaid $1.5B worth of debt. The rest as well as the proceeds for newly issued debt moved onto the balance sheet.

Taking a look at that balance sheet, Microsoft ended the period with a cash position of $143.951B and inventories of $3B. This puts current assets at $207.586B. Current liabilities add up to $124.792B including short-term debt of $29.556B, but also $46.429B in unearned revenue. That would place the firm's current ratio at 1.66 and the firm's quick ratio at 1.70. Both are better than good. Once adjusting these ratios for the unearned revenue which is not a financial obligation, these ratios rise to 2.65 and 2.75, respectively. Outstanding.

Total assets amount to $445.785B including goodwill and other intangibles of $76.685B. At 17% of total assets, this is not a problem. Total liabilities less equity comes to $225.071B. This includes $41.946B in longer-term debt and another $2.759B in unearned revenue. The firm could pay off its entire debt-load out of cash more than twice over if it so chose. In fact, if the firm so chose, it could take care of its "current" debt-load of $29.556B out of just the increase ($32.689B) in its cash position during the past quarter. Fortress like.

Wall Street

Since these earnings were released late Tuesday, I have come across 18 sell-side analysts rated at a minimum of four stars by TipRanks that have also opined on MSFT. Among those 18 analysts, there are 17 "buy" or buy-equivalent ratings and one "neutral", which is a hold-equivalent rating. The one "neutral" also failed to set a target price.

Across the other 17 analysts, the average target price is $411.59 with a high of $450 (Kash Rangan of Goldman Sachs) and a low of $385 (Mark Murphy of JP Morgan). Omitting those two as potential outliers, the average target price across the other 15 drops slightly to $410.80.

My Thoughts

Satya Nadella has done it again. The firm performed well across all segments and across nearly all products and services. Cash flows are beastly. The balance sheet is in outstanding condition. The only knock if there is a knock might be valuation. The stock was trading higher this morning at a forward looking PE ratio of just under 30 times. Does a firm growing revenue less than 13% really deserve a well above S&P 500 forward looking valuation? Even if guidance is for 15%-ish growth?

Maybe. That maybe has more to do with the AI-infused Azure cloud and the AI-infused Microsoft Copilot 365 than anything else. If these products are becoming indispensable as quickly as Microsoft thinks they are, then 30 times projected earnings is inexpensive for this product and investors will be paying 35 times or more down the road.

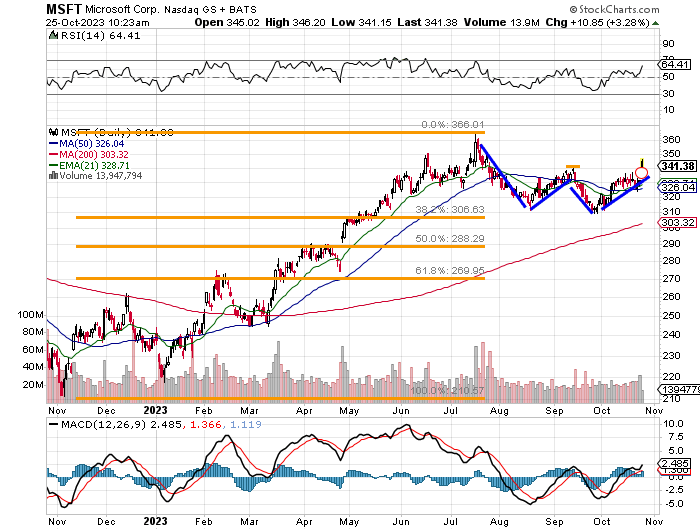

Readers will see that Microsoft has formed a double bottom while consolidating a base in the wake of its November 2022 through late July 2023 rally. Support for this base showed up precisely where our favorite twelfth century mathematician said it might.

The pivot created by the double bottom stands at $340. The stock has taken and is trying to hold that level this morning. If MSFT fails, there is this morning's gap that needs $332 to fill and the stock's own 50 day SMA (simple moving average) ($326) not too far below to provide some traffic. What that means is that in my opinion, the stock is a solid long here (I am long), and entry below $340 would be preferable if possible.

Microsoft (MSFT)

Target Price: $391

Pivot: $340

Add: Down to $326, not above pivot.

Panic: On a break of that 50 day SMA.

(MSFT, GOOGL and AMZN are holdings in the Action Alerts PLUS member club. Want to be alerted before AAP buys or sells these stocks? Learn more now.)

At the time of publication, Stephen Guilfoyle was Long MSFT, AMZN equity.