Risk Happens Quickly, Blowing a Big Lead, Carry Trade Unwind, Trading Lockheed

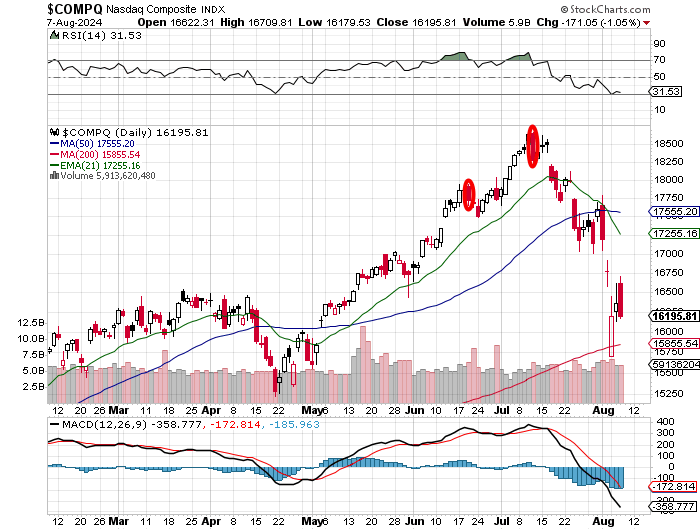

The S&P and Nasdaq gave it all back and more Wednesday, which sets the Nasdaq up for a very interesting day, to say the least, Thursday. Plus, more bad news for Boeing and Intel.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Remember that year, I think it was the 2016 NFL season, when the New England Patriots were down big at halftime of the Super Bowl, or should I say that the Atlanta Falcons were up big at halftime and then blew it? February of 2017 (just Googled it), Super Bowl LI. The Falcons had a 21-3 lead at halftime and a 28-3 lead in the third quarter before surrendering the final 31 points of the game and losing the championship. That's how the Wednesday trading session felt to those of us who lived it.

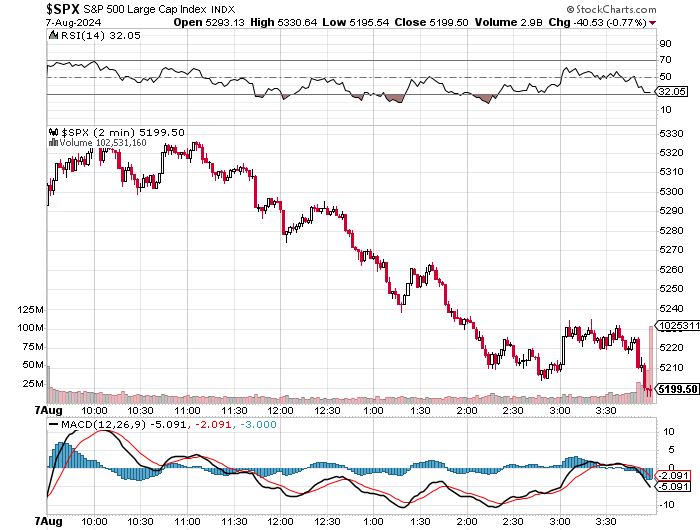

The S&P 500 closed down 0.77% on Wednesday, after having been up 1.7%. The Nasdaq Composite closed down 1.05% for the session after having also been up 1.7%. For both of these major indexes, this was their largest blown lead since March of 2022. Equities came roaring out of the gate on Wednesday. Bank of Japan Deputy Governor Shinichi Uchida had indicated that the BOJ would not tighten monetary policy further while financial markets were unstable. Equities rallied from Asia through Europe and into North America in response.

Was this a verbal sort of put that the BOJ had placed under global equities? Of course not, but that's how markets took it. Can the Deputy Governor speak for the Japanese central bank? Probably not. Was he only speaking of Japanese markets? Possibly.

Risk Happens Quickly

From its early perch, U.S. equity markets started showing signs of weakness after around 11 a.m. Monday It wasn't until after the results of the auction of $42 billion worth of new U.S. 10-Year Notes was announced that the real selling, at lower prices, and in greater volume took place. It wasn't the worst of auctions. I've heard it described as "ugly." I would not go that far. I would say that below-average demand from domestic accounts probably was the catalyst for the deepest sales of U.S. equities on Wednesday as investors lost confidence.

Some of the headline data was less than flattering. The high yield awarded of 3.96% tailed the "when issued" by three basis points as the bid to cover landed at just 2.32, which was the weakest bid to cover for this series in almost two years. Indirect Bidders of foreign accounts did take down 66.2% of the issuance, which is within their aggregate normal range. Apparently, the volatility that we have seen in FX markets has not dissuaded these types of accounts from getting long longer-term U.S. Treasuries.

It was the Direct Bidders, or domestic accounts, that took down just 16% of the auction. That's a sub-par allocation for the home team and left dealers with an above-average slice of the pie. Dealers were stuck with 17.9% of this issuance. We'll possibly do this dance again later today (Thursday) as the Treasury Department unloads $26 billion worth of new 30-Year Bonds.

Marketplace

They say that Wednesday's child is full of woe. Wednesday's child was probably a domestic equity investor.

You already know that the S&P 500 and Nasdaq Composite gave up big leads. The action across the S&P 500 for the regular trading session looked like this:

Interesting that the S&P 500 closed at the lows of the session. So did the Nasdaq Composite. As a matter of fact, the Nasdaq Composite closed not below Monday's low, but below Monday's close, by a hair. Take a look at this:

Is that a huge negative? Not necessarily. It is if this index goes on to test its 200-day simple moving average (SMA) this morning, which is where support had been found on Monday. At least on Monday, the index closed near the top of the range and that was followed by the Tuesday morning rally that faded late. That makes this day very interesting in the least, with Relative Strength weak but not technically oversold, but with the daily Moving Average Convergence Divergence (MACD) postured extremely bearishly.

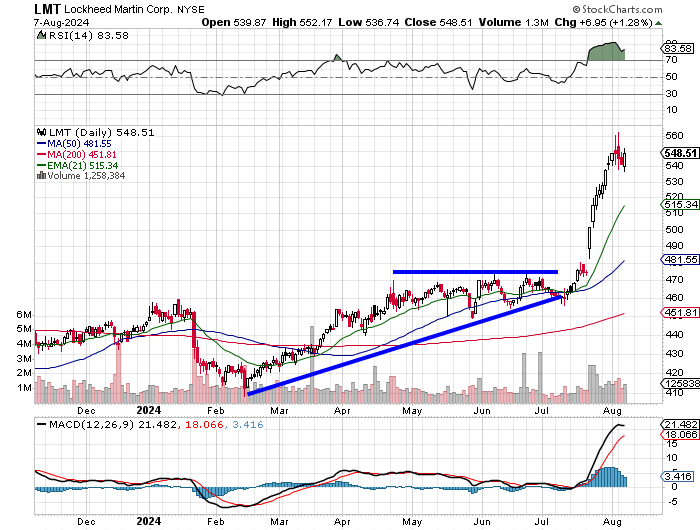

There was no large-scale, joyous rotation into anything else on Wednesday, except for defensive and Defense-related stocks. The Semiconductors took a beating, as did the small-caps. Just four of the 11 S&P sector-select SPDR ETFs closed in the green, with Utilities XLU leading the way.

On an industry level, the Dow Jones U.S. Defense Index gained 1.87%, led by Axon Enterprise AXON, a name that is a position in TheStreet Pro Portfolio. On a personal level, Lockheed Martin LMT, General Dynamics GD, and Northrop Grumman NOC all posted gains as well.

Remember the breakout from the ascending triangle that I set up for you in LMT back in early July? Yeah, the shares have started to form a base of consolidation. I'm not saying get out because I am not getting out, but selling something up here would not be wrong:

Just look at that Realtive Strength Index (RSI) and that daily MACD. Gee willikers, that was a good one, Batman.

Breadth was on the soft side on Wednesday as one might have expected. Losers beat winners at the NYSE by a roughly 4 to 3 margin, and by 2 to 1 at the Nasdaq. Advancing volume took a 39.1% share of composite NYSE-listed trade and 30.9% of composite Nasdaq-listed action. However, trading volume in the aggregate, which had dropped off on Tuesday, remained flat or steady from Tuesday's levels. This suggests that professional money was far more active on Thursday, Friday and Monday with markets in beat-down mode than it has been since.

Humiliating

Boeing BA did not participate in the Defense stock rally, as the shares closed down 1.09%. In what must be another humiliating experience for the aerospace giant, the Financial Times is reporting that NASA is considering asking SpaceX to retrieve two astronauts from the International Space Station who have been stranded there for about two months due to technical difficulties with the Boeing CST-100 Starliner spacecraft that got them there.

SpaceX has a mission to the space station scheduled for September to deliver crew and supplies. The mission may now only transport two new astronauts instead of four to the ISS leaving room for Sunita Williams and Barry Wilmore, the two who have been stranded. A decision will be made by mid-August.

Embarrassing

Intel INTC shareholders filed suit against the chipmaker on Wednesday, making the claim that the firm had falsely concealed issues regarding the foundry business, resulting in poor second-quarter earnings that ultimately led to a suspension of the dividend and plans to reduce the firm's headcount by 15%.

The lawsuit was filed in San Francisco accusing the firm, CEO Pat Gelsinger and CFO David Zinser of hiding problems that led to poor financial performance. The lead plaintiff is Construction Laborers Pension Trust of Greater St. Louis.

Almost There?

Bloomberg News is reporting that JP Morgan quantitative strategists Antonin Delair. Meera Chandan, and Kunj Padh have written a note that global carry trade baskets tracked by the bank have fallen by roughly 10% since May. This has wiped out year-to-date gains, but according to the team... "The spot component of the global carry basket would suggest that 75% of carry trades have been removed."

The group acknowledges that "The yield on the basket has plummeted since the highs of 2023 and is not a sufficient compensation for holding EM high betas through US elections and the risk of further repricing of low yielders if US yields fall."

Recommended Reading

Read the Meta Platforms META/Alphabet GOOGL piece published at the Financial Times this morning. Eye-opening if true. Neither stock seems to be reacting.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 248K, Last 250K.

08:30 - Continuing Claims (Weekly): Last 1.877M.

10:00 - Wholesale Inventories (June): Expecting 0.4% m/m, Last 0.6% m/m.

10:30 - Natural Gas Inventories (Weekly): Last +18B cf.

13:00 - Thirty-Year Bond Auction: $25B.

The Fed (All Times Eastern)

15:00 - Speaker: Richmond Fed Pres. Tom Barkin.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DDOG (0.36), LLY (2.77)

After the Close: GILD (1.60), PARA (0.13), RKLB (-0.07), TTD (0.36), YELP (0.71)

At the time of publication, Guilfoyle was long RKLB, XLU, LMT, GD and NOC.