Weekly Roundup: How We Benefited From the Market Divergence

Nvidia, Qualcomm, and Marvell powered the portfolio higher, while pushback on rate cuts weighed on other sectors.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

When we compare the performance of the S&P 500 against the Nasdaq Composite this week, it’s evident there were diverging forces pulling on the stock market. The picture becomes even clearer when we account for the declines registered by the Dow Jones Industrial Average and the small-cap-laden Russell 2000.

What pulled the market higher was Nvidia NVDA following its beat-and-raise quarter that also included a dividend hike and a 10-for-1 stock split announcement. Those results lifted the larger basket of AI-related stocks, propelling the Nasdaq higher as well as several of our holdings.

Weighing on the rest, however, was the market digesting sobering comments found in the latest Fed meeting minutes and comments from Fed officials. In our Alerts to you, we shared how we were not surprised by either given the string of recent data but also what was found in Thursday’s Flash May PMI report. Cutting to the chase, the factors pushed back on Fed rate cut expectations for September, taking some wind out of the market. While we saw some bounce back on Friday, which helped propel the portfolio higher, by and large, the S&P 500 was little changed on the week, leaving it up modestly so far this quarter.

Below we share our updated shopping list for the portfolio and our near-term game plan. When we return from the Memorial Day holiday weekend, we’ll start the compressed week off with an updated table of earnings expectations for our holdings as well as the S&P 500. We’ll look for you in next week’s Office Hours in the portfolio Forum on Tuesday, May 28, from 4 PM – 5 PM ET and again on Thursday, May 30, from 12 PM – 1 PM ET. We hope to see you there!

Catching Up on the Portfolio This Week

With one week to go in May, the S&P 500 is up roughly 1.0% quarter to date and the good news is the bulk of our holdings have cleared that hurdle. Leading the pack so far this quarter are Qualcomm (QCOM) and Nvidia (NVDA), which both notched double-digit gains this week, as well as Alphabet (GOOGL), Costco (COST) and Apple (AAPL). Other big contributors include Marvell (MRVL) as well as Applied Materials (AMAT), both of which are up more than twice the Nasdaq’s quarter-to-date return. We see this speaking to moves we made in February through March paying off.

We do have some laggards, including Axon (AXON), Coty (COTY), and United Rentals (URI). We used that underperformance this week to add to our AXON and COTY holdings. The next-known catalyst for both URI as well as Vulcan Materials (VMC) shares will be the April Construction Spending report due out June 3.

During the week, we used the more than 90% move in QCOM shares to lock in a slice of gains, using those proceeds to fund our pick-ups for incremental AXON and COTY shares. We also boosted our price targets on Morgan Stanley (MS), Bank of America (BAC), Qualcomm and Nvidia.

We’ve shared some of the companies on our current shopping list, including The Trade Desk (TTD) and Waste Management (WM), but the late-in-the-week selloff in Labcorp (LH) earns them a spot as well. We’ll revisit pick-up points for positions on our shopping list, and scout for new potential Bullpen candidates putting this week’s pullback to good use.

We’ll also continue to revisit price targets as needed, including the one for our SPDR Gold (GLD) shares. And as we’ve discussed we plan on giving TreeHouse Foods (THS) the same treatment we recently gave Eaton (ETN) and Meta Platforms (META), which should end with some potential entry points for those shares.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns and the Portfolio Podcast. If you happened to miss one or more of them, here are some helpful links:

Monday, May 20: What We're Watching This Week and Price Targets We're Revisiting

Tuesday, May 21: These Portfolio Stocks Helped Power the Nasdaq to All-Time Highs

Wednesday, May 22: Breaking Down Today's Trades and Learnings From Target's Earnings

Thursday, May 23: Why This Bullpen Name Is Up Next for a Closer Look

Friday, May 24: 4 Key Things to Watch Next Week — Including Costco

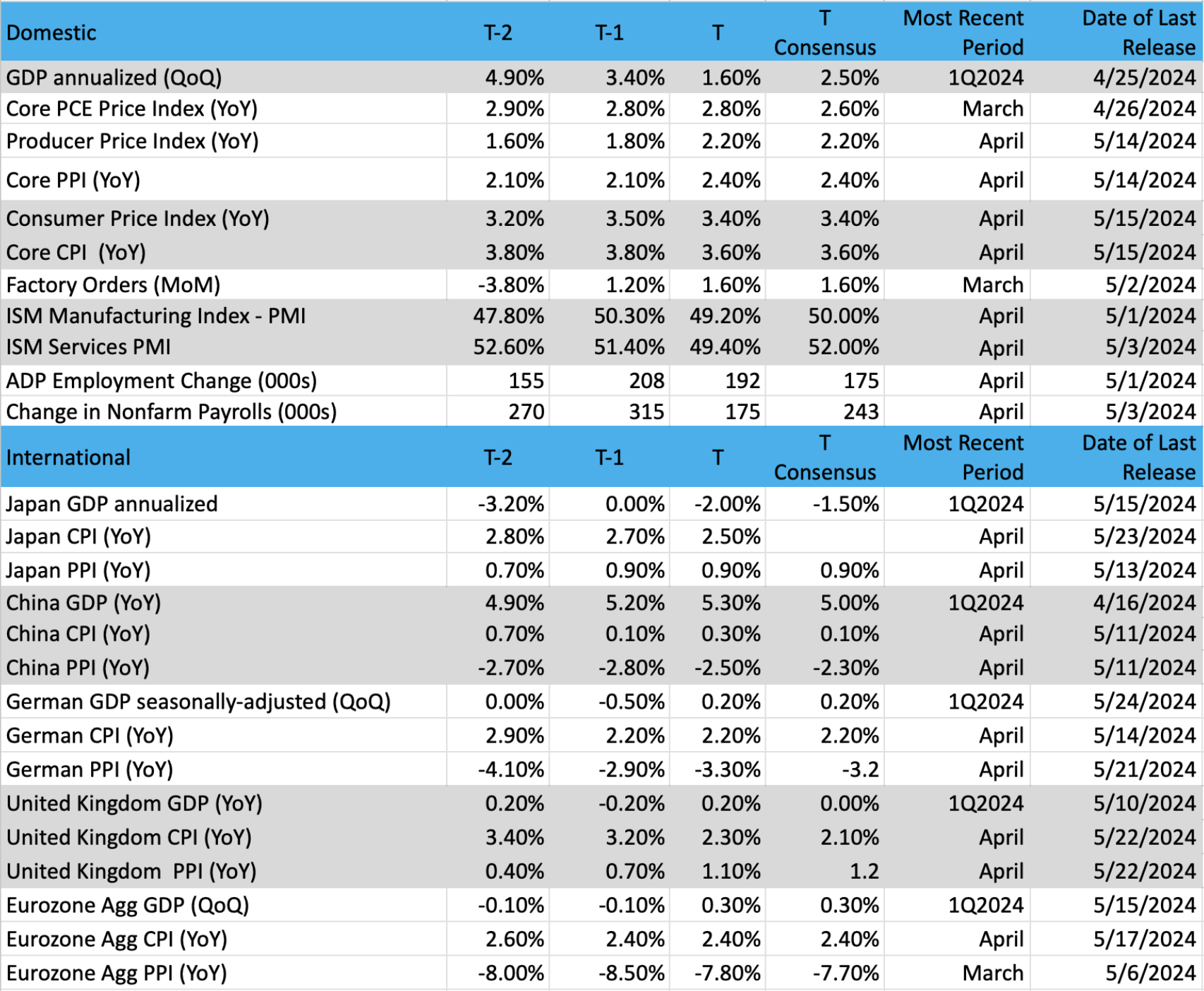

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: Invesco QQQ Trust (QQQ)

The Nasdaq 100 has been carrying the rest of the market this past month, and it shows up with good technical and chart action. But as we know, the markets are better off when there is broad leadership, like we often see when the Russell 2000 is leading the way.

Now, there is nothing wrong with Nasdaq leadership, after all this is the index with the biggest market capitalization stocks and the most widely held names (most owned). But a bull market is better defined as one where many/all groups participate in the upside. Recall in 2023 when the Nasdaq was hands down the best-performing index all year long, most of the market was trailing or even negative in the fourth quarter (Russell 2K, Dow Industrials).

The Nasdaq, for its part, has widespread influence and could certainly pull up other sectors if the conditions are right. Those conditions include strong breadth, volume, price action, lower interest rates, strong earnings, and better economic data (especially on inflation). Having all these characteristics line up positively is probably asking too much, but the more these stack up, the better chance for a bullish run. The QQQ is leading the way right now with good performance so far this spring.

The chart below shows a nice turn from bearish to bullish over the last six weeks. The QQQ had been struggling to move higher in April as the Industrials were the leader. In fact, the QQQ tested the 100-day moving average successfully and bounced firmly off that level. Notice the change in candle colors from purple to blue — that is a bearish to bullish changeover.

But recent moves down may signal a bit of trouble ahead. The massive reversal day on Thursday from a new high to closing on the lows of the session was a red flag. Further, notice that stochastics have rolled over following the very high volume selling. If there is a follow-through next week there is a good chance of more correction happening.

Does this mean the uptrend is over? Of course not, we still have strong upside potential, but following a very overbought condition, at some point, the sellers will take control, which is not always a bad thing during a market rally.

Other charts we shared with you this week were:

Monday, May 20: S&P 500 - A Strong Push Means Higher Prices Ahead

Monday, May 20: Nvidia (NVDA) - Don't Expect Nvidia to Disappoint

Tuesday, May 21: AMD (AMD) - AMD Hits Resistance

Wednesday, May 22: Axon (AXON) - Has Axon Fallen to a Buy Point?

Thursday, May 23: Bank of America (BAC) - Bank of America's Strong Uptrend Continues

The Coming Week

Next week brings less than a handful of fresh economic numbers that will give us another perspective on real wage growth, consumer spending, and inflation. Before we get to those reports, though, we’ll get the revised GDP print for Q1 2024. The original figure came in at 1.6%, which was weaker than the market forecast, but the wide expectation is we will get an upward revision.

While an upward revision would be constructive, given where we are in the current quarter, we’re more focused on GDP prospects for the current quarter. Exiting this week, the Atlanta Fed GDPNow model now has a 3.5% figure for the current quarter, down from its recent forecast of 3.6%, but up from its 3.3% figure at the start of May. The Flash May PMI report showed an uptick in the economy during May, but we’ll want to confirm that based on the final report as well as ISM’s May PMI reports that we’ll receive in early June.

The Flash May Flash PMI report also showed input and output cost pressure, signaling inflation didn’t make much progress compared to April. The market will focus on the April PCE Price Index, especially its core reading, but our thinking is it would take a meaningful decline to alter the Fed’s view that it needs to see three to five months of continued progress to get on board with rate cuts.

The current market forecast is for April core PCE to dip to 2.7%, year over year, from March’s 2.8%. On its own, some may try to argue that may be enough but when we look at other indicators, including the April core CPI at 3.6% and the Flash May inflation comments, our view is the Fed will want more. We’ll keep an open mind and update our thinking as new data become available but as we head into the holiday weekend, our call continues to be for one rate cut late this year.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, May 28

· FHFA Housing Price Index – March (9:00 AM ET)

· S&P Case-Shiller Home Price Index – March (9:00 AM ET)

· Consumer Confidence – May (10:00 AM ET)

Wednesday, May 29

· MBA Mortgage Applications – Weekly (7:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, May 30

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· GDP (2nd Estimate) – Q1 2024 (8:30 AM ET)

· Advance Retail Inventories – April (8:30 AM ET)

· Pending Home Sales – April (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, May 31

· Personal Income & Spending, PCE Price Index – April (8:30 AM ET)

International

Thursday, May 30

· Eurozone: Economic Sentiment – May

· Eurozone: Consumer Confidence, Inflation Expectations

Friday, May 31

· China: NBS Manufacturing & Services PMI – May

· Eurozone: Flash Inflation Rate - May

Next week we have two portfolio companies reporting. Both Costco (COST) and Marvell (MRVL) report after the market close on Thursday, May 30. While we wait for those results, we’ll continue to parse the continued wave of retail reports, especially the one for Ulta Beauty (ULTA). In that one, we’ll be listening to what the company says about the North American beauty market, noting comments for the prestige fragrance market.

Inside results and guidance from HP (HPQ) and Dell (DELL), we’ll be focused on what they say about the rebounding PC market and the expected size of the AI-on-PC market this year and next. Those insights should help us frame expectations for Qualcomm (QCOM) and Nvidia (NVDA) as well as Microsoft (MSFT).

Here's a closer look at the earnings reports coming at us next week:

Tuesday, May 28

· Close: Box (BOX), Cava Group (CAVA).

Wednesday, May 29

· Open: Abercrombie & Fitch (ANF), American Eagle (AEO), Chewy (CHWY), Dick’s Sporting Goods (DKS).

· Close: Agilent (A), HP (HPQ), Salesforce (CRM).

Thursday, May 30

· Open: Best Buy (BBY), Dollar General (DG), Foot Locker (FL), Kohl’s (KSS).

· Close: Ambarella (AMBA), Cooper (COO), Costco (COST), Dell (DELL), Gap (GAP), Marvell (MRVL), Nordstrom (JWN), Ulta Beauty (ULTA), Zscaler (ZS).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.