Weekly Roundup

The short trading week was a good one for our portfolio, but with notable gains in our shares, especially for Elevance Health, Chipotle, Mastercard, Alphabet, and McDonald's.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

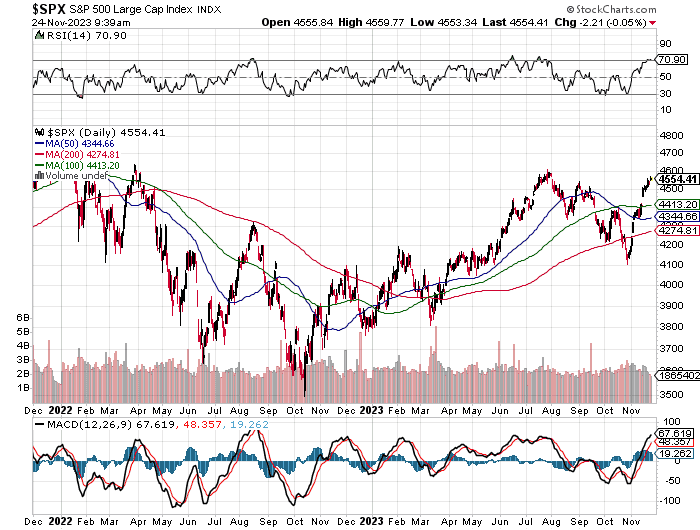

The stock market continued to melt up during the abbreviated trading week, led higher by the fall in oil prices and the 10-year Treasury yield, despite the latter clawing its way back modestly on Friday's shortened trading session.

Also supporting the continued lift in equities were strong inflows into global stock funds over the last two weeks as latecomers try to catch the current rally, even though the S&P 500 is once again flirting with being overbought following its around 10.5% move since bottoming on Oct. 27. The same goes for the Nasdaq Composite. While those late buyers add to the melt-up, typically it's more of a signal the market is likely to give some of those gains back, especially as short-term traders look to lock in some of those quick profits.

We've shed some shares last week and again this week, which has us flush with cash to put to work at better prices. We recently added Cisco CSCO and Walmart WMT to the Bullpen, where they join Morgan Stanley MS and Builders FirstSource BLDR . We're working on a few more candidates as well as we look to steer the portfolio for the last month of 2023 and the start of 2024.

Catching Up on the AAP Portfolio This Week

The shortened trading week was a fairly positive one for the portfolio's positions, with notable gains in our shares of Elevance Health ELV , Chipotle CMG , Mastercard MA , Alphabet GOOGL , and McDonald's MCD . With ELV shares, they are not only back at levels last seen in July and mid-October, but they are entering overbought territory as well. If you missed ELV shares up in late October or early November, our message is to hold off for now.

Early gains in the week added to the significant outperformance in Chipotle CMG shares and we responded with some profit-taking as we lifted our panic point to $1,850 from $1,800. The rationale behind that action was the same with our taking some United Rentals URI , Costco COST , and Qualcomm QCOM shares off the table the week before. The continued rebound in MCD shares prompted us to lift that pain point to $240 from $235.

Even though the shares of Deere DE recovered much of their post-earnings slump, the shares were a drag on the portfolio this week. Ahead of the earnings conference call, we downgraded DE shares to a "Two" rating from "One" and trimmed our price target to $435 from $450 after that presentation. While much of the earnings call rehashed the earnings press release, several items confirmed Deere will remain a disciplined company in the coming year focused on maintaining structural profit improvements instead of using price to boost market share. That will take some time to win over investors, making Deere shares a show-me story for the next one to two quarters.

This Week's AAP Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns and the AAP Podcast. If you happened to miss one or more of them, here are some helpful links:

Monday, November 20: Don't Miss This Big Data Point That Lands This Week

Tuesday, November 21: How the Portfolio Is Positioned for a More Selective Consumer

Wednesday, November 22: Everyone Needs a 'Wakeup Call' for Stocks

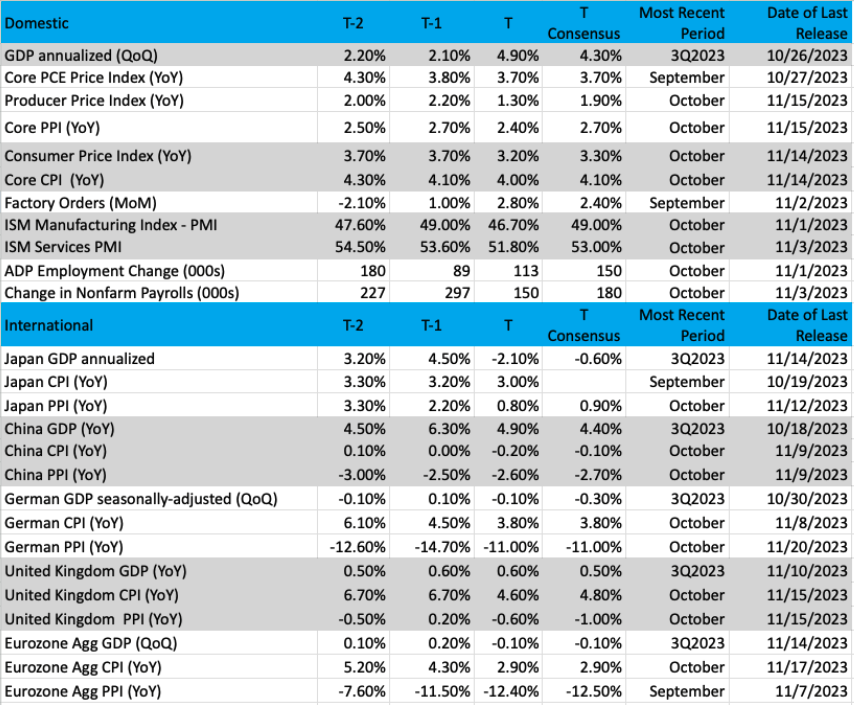

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

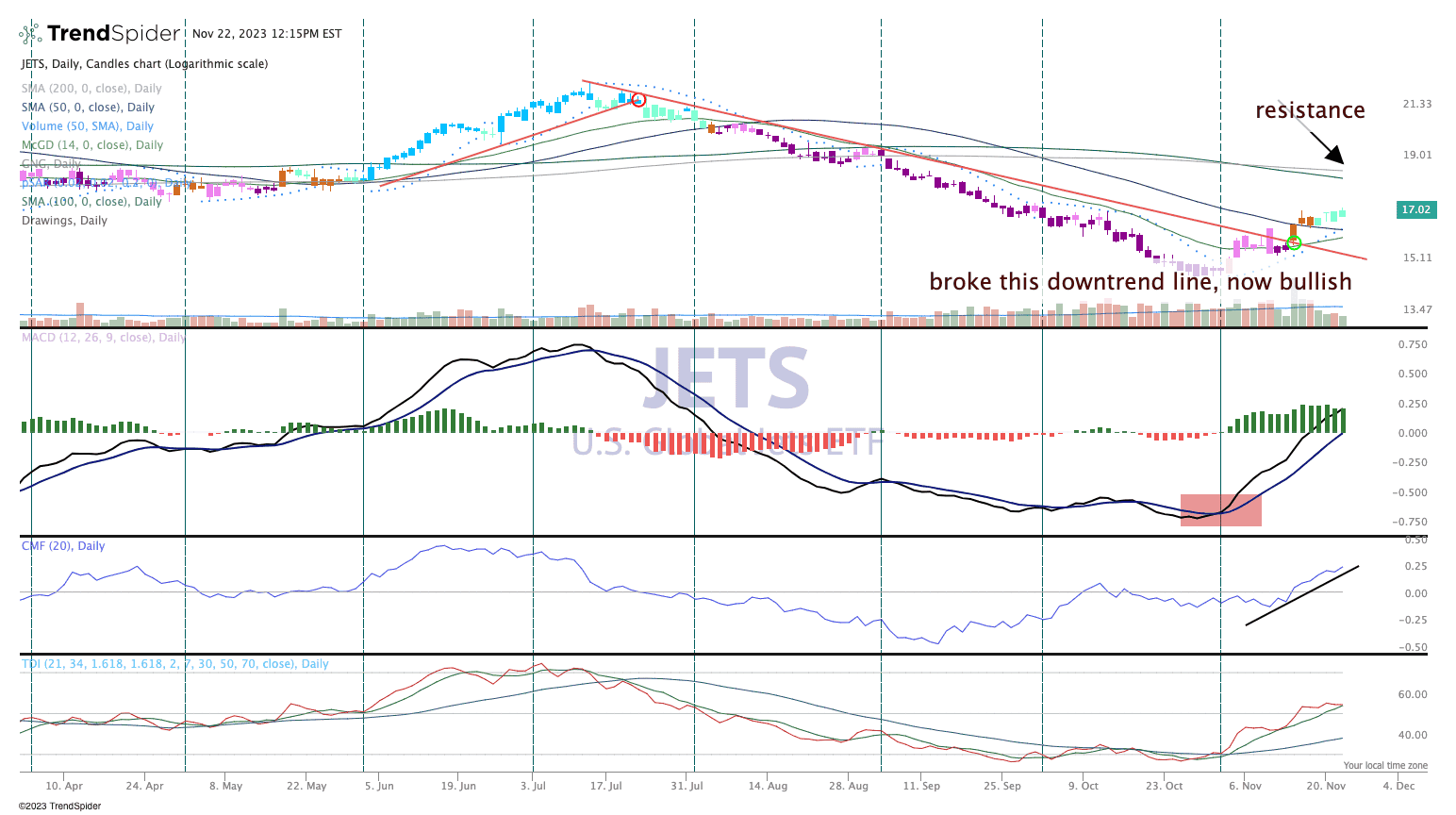

Chart of the Week: JETS!

With oil and therefore jet fuel prices moving lower, we find the chart of the U.S. Global Jets ETF JETS interesting, potentially getting more bullish as the days go on. We highlight the top pane here and the GoNoGo chart of composite indicators (colored candles). It is here we see the transition taking place from bearish to bullish. The colors have moved this month from bearish pink, to amber (neutral), to teal (cautiously bullish). The next color would be blue, and that would indicate a full-out bullish signal.

Other indicators on the chart are bullish, too, including the important Moving Average Convergence Divergence (MACD) oscillator, which has been on a buy signal since the start of November (that crossover is bullish). This indicator tells a change in the trajectory of moving averages before they occur. Chaikin money flow in pane 3 is quite strong and tells us big money is flowing into the airlines.

For a closer look at the chart, click here.

Other charts we shared with you this week were:

Monday, November 20: S&P 500 - Indicators Are Lining Up for the Bulls

Monday, November 20: Deere & Co. - Here's How Deere Looks Heading Into Earnings

Tuesday, November 21: Amazon - Amazon Passes the Test

Wednesday, November 22: SPDR Gold Trust - As the Dollar Tarnishes, Gold Shines

The Coming Week

When we return from the weekend, it will be Cyber Monday and we'll also have initial tallies for the holiday shopping weekend as we begin the last four trading days of November. The economic calendar is back-end loaded next week with the October PCE Price Index and final November Manufacturing PMI reports from S&P Global and ISM. Helping set expectations for that data after Friday's November Flash PMI data from S&P Global showed further inflation improvement is the Fed's latest Beige Book due out Wednesday afternoon. In those pieces of data, we'll be looking for support for the Goldilocks narrative and indications for further declines in the November CPI and PPI reports.

As that data is collected and digested, we'll continue to evaluate our positions in the SH and PSQ inverse ETFs. Leading up to that data, which will be published on Dec. 12 and 13, AAP team member Helene Meisler is thinking we could see a market pullback in December following November's strong move before another rally ensues.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, November 27

- New Home Sales - October (10:00 AM ET)

Tuesday, November 28

- FHFA Housing Price Index -September (9:00 AM ET)

- S&P Case-Shiller Home Price Index - September (9:00 AM ET)

- Consumer Confidence - November (10:00 AM ET)

Wednesday, November 29

- Weekly MBA Mortgage Applications (7:00 AM ET)

- GDP (Second Estimate) - 3Q 2023 (8:30 AM ET)

- Weekly EIA Crude Oil Inventories (10:30 AM ET)

- Fed Beige Book (2 PM ET)

Thursday, November 30

- Weekly Initial & Continuing Jobless Claims (8:30 AM ET)

- Chicago PMI - November (8:30 AM ET)

- Personal Income & Spending - October (8:30 AM ET)

- PCE Price Index - October (8:30 AM ET)

- Pending Home Sales - October (10:00 AM ET)

- Weekly EIA Natural Gas Inventories (10:30 AM ET)

Friday, December 1

- S&P Global Manufacturing PMI (Final) - November (9:45 AM ET)

- ISM Manufacturing Index - November (10:00 AM ET)

- Construction Spending - October (10:00 AM ET)

International

Monday, November 27

- China: Industrial Profits (YTD) - October

Tuesday, November 28

- Germany: GfK Consumer Confidence - December

- Eurozone: Loans to Companies, Consumers and Households - October

Wednesday, November 29

- UK: Bank of England Consumer Credit - October

- Eurozone: Economic Sentiment, Consumer Confidence, Consumer Inflation Expectations - November

Thursday, November 30

- China: NBS Manufacturing & Non-Manufacturing PMI - November

- Germany: Retail Sales - October

- Eurozone: Inflation Rate (Flash) - November

Friday, December 1

- Japan: Jibun Bank Manufacturing PMI (Final) - November

- China: Caixin Manufacturing PMI - November

- Eurozone: HCOB Manufacturing PMI (Final) - November

- UK: S&P/CIPS Manufacturing PMI (Final) - November

As we take pencil to paper and revisit the expectations for our holdings, quarterly results from Construction Partners ROAD will be something we consider for our shares of United Rentals URI , Vulcan Materials VMC , and Deere DE . Comments from Kroger KR will be an input for PepsiCo PEP and Salesforce CRM guidance will be another one for cloud demand. Dell's DELL results and guidance will be another data point for the rebounding PC market. We'll also be checking in on quarterly results from several cybersecurity companies, including Zscaler ZS , CrowdStrike CRWD , and Splunk SPLK , which should support rising cybersecurity spending and our First Trust Nasdaq Cybersecurity ETF CIBR .

We also have earnings from Marvell MRVL , and as we shared in our post-Nvidia NVDA earnings alert, we are standing on the sidelines with MRVL shares ahead of earnings given export curbs and the size of its China exposure could yield softer than expected guidance.

Here's a closer look at the earnings reports coming at us next week:

Monday, November 27

- Close: Zscaler ZS

Tuesday, November 28

- Close: CrowdStrike CRWD , Hewlett Packard Enterprise HPE , Intuit INTU , NetApp NTAP , Splunk SPLK

Wednesday, November 29

- Open: Construction Partners, Dollar Tree DLTR , Farfetch FTCH , Foot Locker FL , Petco Health & Wellness WOOF

- Close: Credo Technology CRDO , Five Below FIVE , Okta OKTA , PVH PBH , Snowflake SNOW , Victoria's Secret VSCO .

Thursday, November 30

- Open: Big Lots BIG , Cracker Barrell CBRL , Kroger K

- Close: Ambarella AMBA , Dell DELL , Marvell MRVL, Salesforce CRM , Ulta Beauty ULTA .

Action Alerts PLUS is long BAC, AXON, COTY, LMT, ELV, GLD, SH, PSQ, XLE, PEP, MA, CIBR, AMZN, AMAT, URI, MSFT, MRVL, GOOGL, DE, COST, CMG, AAPL, VMC, TRIN, MCD, QCOM.