Weekly Roundup

After a tough several weeks for stocks, we have a few names on our shopping list, including Qualcomm, McDonald's, and Lockheed Martin.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Stocks regained some ground on Friday, but they finished the week lower, adding to the August decline. The S&P 500 shed 1.3% this week, bringing its total decline to 2.9% over the last several weeks. The Nasdaq Composite lost 1.9% over the last four days and almost 4.1% since the start of August. Small caps continued to take a larger beating evidenced by the 7.6% drop since early August. Weighing on stocks this week was renewed uncertainty about what's next for monetary policy and China's smartphone ban, including iPhones, which led Apple to weigh on the S&P 500 and Nasdaq Composite.

The renewed questions over the path ahead for monetary policy following the stronger than expected August ISM Non-Manufacturing Index that showed further acceleration in its Prices sub-index. That was followed by the upward revision in second-quarter Unit Labor Cost to +2.2% from the initial +1.6% figure. More hawkishness from Fed heads followed with Dallas Fed President Lorie Logan pinpointing the concern: "If stronger economic activity continues, it could lead to a resurgence in inflation."

After this week's data, the Atlanta Fed's GDPNow model was unchanged at 5.6%, a figure that will continue to be updated as more data is published. So far, it speaks to the concern called out by Logan. So too does Goldman Sachs cutting its 12-month recession probability to 15% from its prior estimate of 20%. For context, a Bloomberg survey finds the consensus probability at 60%. Goldman's economists also see GDP growth averaging 2% through the end of 2024.

Our thinking is while the market will be overly focused on next week's core consumer price index reading for August, which is expected to fall to 4.3% from 4.7% in July, and the Fed will be looking at additional data to capture a clearer picture on inflation. Should the August CPI print come in warmer than expected, we should expect to see that reflected in Treasury yields as well as shifting probabilities collected by the CME FedWatch Tool.

With the CNN Business Fear & Greed Index registering "Neutral" as we close the week, it tells us a warmer than expected core CPI print would catch the market off guard, likely extended the recent pressure on stocks. However, if the core CPI print is better than expected (that is lower than 4.3%), the market will be in a more ebullient mood at least until the August Retail Sales later in the week.

As that data is released, we'll continue to fine tune our expectations and take action with our shopping list shared below as warranted.

Catching Up on the AAP Portfolio This Week

During the shortened trading week we took advantage of the continued climb in oil prices and the positive impact had on our shares of the Energy Select Sector SPDR Fund since early June. Oil prices finished the week on a positive note, and our view is if we see that translate into further gains for XLE shares, we are inclined to book additional profits as the shares move closer to our $98 target. The move lower in the S&P 500 and Nasdaq Composite during the week lifted our inverse ETF positions again this week, making them a positive contributor to the portfolio over the last five weeks. Other notable performers this week included Costco, Chipotle, Elevance Health, Microsoft, and PepsiCo shares.

Following disappointing quarterly results, we downgraded the shares of ChargePoint to a Three rating and cut our price target to $9 from $15 even though many Wall Street voices reiterated their Buy ratings.

Wednesday was the September members only call, and here we heard from Helene Meisler along with Chris Versace in talking about the various positions in the AAP portfolio.

Getting ready for next week, shares on our shopping list include Qualcomm, McDonald's, Lockheed Martin and potentially Marvell and Universal Display as we revisit our current price targets. As we share that list, we will also mention we aren't likely to make any sizable moves until we have the August core CPI data in hand. Should the print for that data come in hotter than expected, it most likely means we will see stocks trade off, giving us potentially better prices with which to nibble.

This Week's AAP Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns and the AAP Podcast. If you happened to miss one or more of them, here are some helpful links:

Tuesday, September 5: Here's What's Shaping the Portfolio's Trading Game Plan

Wednesday, September 6: Action Alerts PLUS Members Call - September 2023

Thursday, September 7: Missed Wednesday's Live Call? No Problem, Here's the Full Rewind

Friday, September 8: Carley Garner on What's Next for Oil Prices, Gold, and Other Commodities

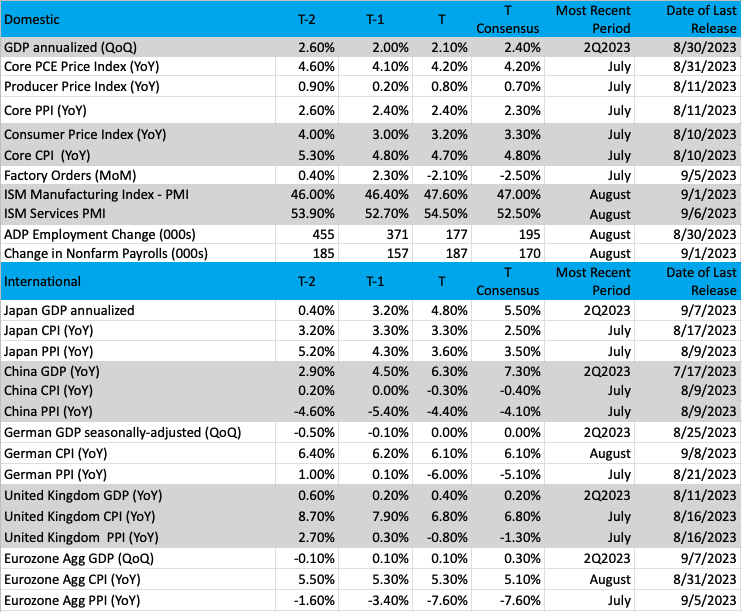

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

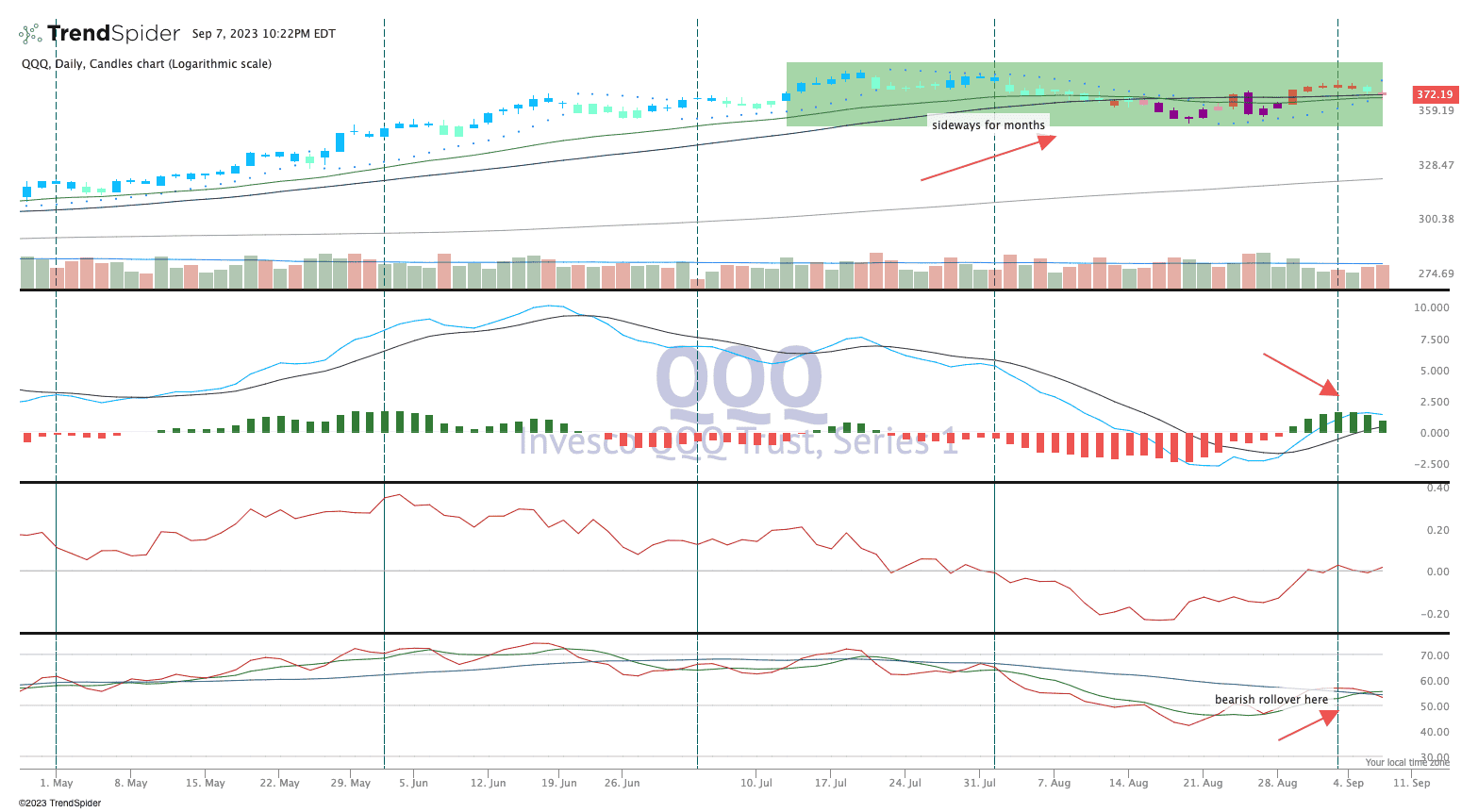

Chart of the Week: The Nasdaq 100 is Showing Some Cracks

There is no doubt the undisputed winner so far has been Nasdaq 100, or the QQQ ETF. Following a forgettable 2022 which saw the index lose a third of its value, the QQQ has stormed back strong on the heels of good earnings, strong prospects, and the eventual end to the Federal Reserve's massive rate hike cycle. It is the names in the QQQ that have drawn the attention of investors, but only a few, the "magnificent seven" were responsible for the bulk of gains in the first half of 2023. But while other stocks in the index caught up to the "seven," this big cap-weighted index has really gone nowhere for the past three months. Since a nice breakout occurred in early June the QQQ has been stuck in a tight range between $355 and $390. With just under four months remaining in 2023 the pressure is on to push the Nasdaq 100 higher towards the all-time high just above $400. That elusive level is only 10% away, and with a furious run to the finish the QQQ might just get there before the year is over.

The chart is quite a bit challenged here, with weakness in the money flow and the Moving Average Convergence Divergence (MACD) oscillator just floundering and looking to press lower for a sell signal. Since mid-August the goNOgo indicator has mostly been purple or amber color, not inspiring the buyers to step up. And now we have a bearish crossover on the Traders Dynamic Index (TDI) indicator, where relative strength is breaking down versus the Bollinger bands. If the Nasdaq can show bullish leadership as it did in the first half of 2023, there should be optimism all around.

Other charts we shared with you this week were:

Tuesday, September 5: S&P 500 - The Index Confirms a Bull Market Is Here

Tuesday, September 5: SPDR Gold Trust ETF (GLD) - Gold Starts to Shine

Wednesday, September 6: Applied Materials (AMAT) - Applied Materials May Need to Take a Breather

Thursday, September 7: Chipotle (CMG) - Chipotle Quietly Grinds to Higher Ground

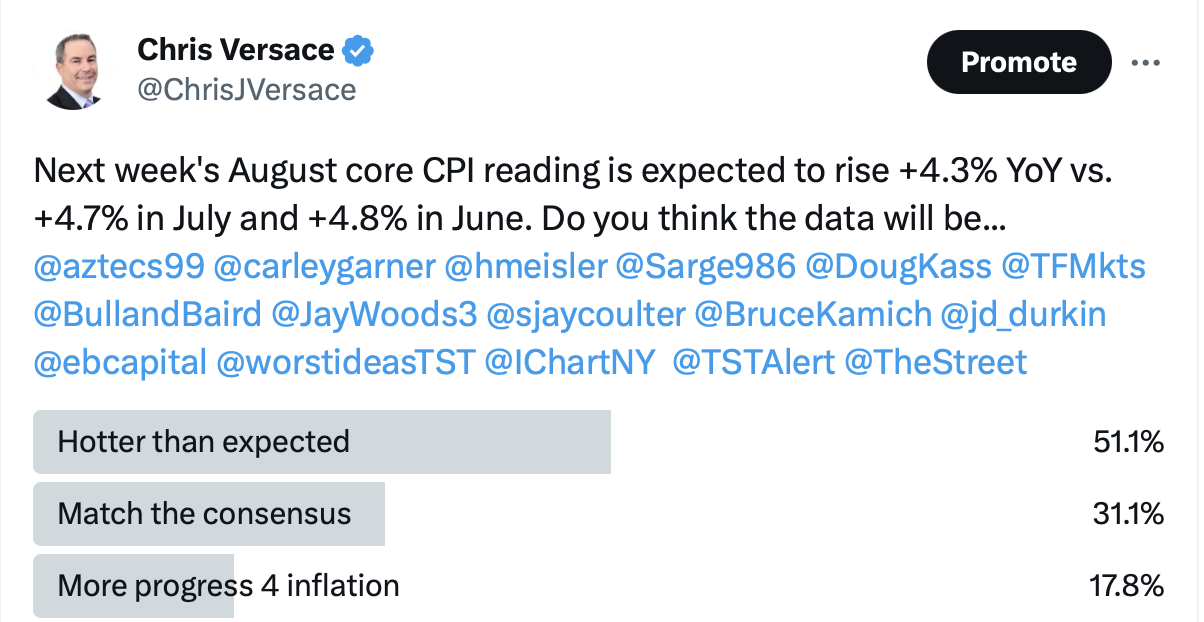

Poll of the Week

We know the August CPI report next week is one the Fed will be closely watching for further progress on inflation via the core CPI data. That means we and the larger will be watching it as well. As we head into the weekend, the consensus forecast is for August core CPI to come in at +4.3% on a year over year basis, down from +4.7% in July and +4.8% in June.

This brings us to our AAP Poll of the week - Do you expect the August core CPI reading to come in hotter than expected, match the consensus forecast or point to further progress on inflation?

Be sure to

The Coming Week

Next week we are back to five trading days, and while the pace of earnings slows to a mere trickle, we will have another helping of investor conferences. We will also be getting a few key pieces of economic data the market will be vetting given renewed concerns for monetary policy after the Hawkins Fed head comments late this week. We discussed those above in our opening remarks for this edition of the Roundup, but Federal Reserve Bank of New York President John Williams comment that more data needs to be analyzed to determine how to proceed with rates sums it up pretty nicely.

The data next week includes the August CPI and PPI reports, and we expect both will be put under the microscope rather closely. We noted the expected core CPI print for August above in our AAP Poll of the Week, but a hotter print is likely to spook the market. Given what we saw in the August ISM Non-Manufacturing Index's price component, we're keeping our inverse ETFs in play leading into that data. August Import/Export prices will add another dimension for inflation as well.

We also have the August Retail Sales report, which we will be assessing for several portfolio holdings, including Costco (COST), Amazon (AMZN), McDonald's (MCD), Chipotle (CMG), Mastercard (MA), and some others. Heading into that report, let's remember sequential comparisons are likely to be impacted by the July data benefitting from Amazon's 2023 Prime Day as well as competing efforts by others, including Walmart (WMT), Target (TGT), and Best Buy (BBY).

Another item that will be in the spotlight next week will be the potential UAW-Detroit Three strike. The current UAW contract expires on September 14 and following the pronounced win by the Teamsters in its recent negotiations with UPS (UPS), we see the UAW standing tough, aiming to maximize what it can deliver for its membership. We see the odds of a strike as better than 50/50 at this point. While we have no direct exposure, a strike would have an impact on the economy.

We are also keeping an eye on Congress given the potential government shutdown on September 30. We do expect political theatrics to be had but if history holds at least a short-term funding bill will pass, most likely at the eleventh hour.

In addition to the US Open finals, we will also be tracking Hurricane Lee which became a Category 4 storm on Friday. The latest reports suggest it's too soon to know whether this system will directly impact the US mainland.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, September 11

- Consumer Inflation Expectations - August (11:00 AM ET)

Tuesday, September 12

- NFIB Small Business Optimism Index - August (6:00 AM ET)

- USDA WASDE Report - August (12 PM ET)

Wednesday, September 13

- Weekly MBA Mortgage Applications (7:00 AM ET)

- Consumer Price Index - August (8:30 AM ET)

- Weekly EIA Crude Oil Inventories (10:30 AM ET)

- Treasury Budget - August (2 PM ET)

Thursday, September 14

- Weekly Initial & Continuing Jobless Claims (8:30 AM ET)

- Producer Price Index - August (8:30 AM ET)

- Retail Sales - August (8:30 AM ET)

- Business Inventories - July (10:00 AM ET)

- Weekly EIA Natural Gas Inventories (10:30 AM ET)

Friday, September 15

- Import/Export Prices - August (8:30 AM ET)

- Empire Manufacturing Index - September (8:30 AM ET)

- Industrial Production & Capacity Utilization - August (9:15 AM ET)

- University of Michigan Consumer Sentiment Index (Preliminary) - September (10:00 AM ET)

International

Tuesday, September 12

- China: Vehicle Sales, New Yuan Loans and Loan Growth - August

- Japan: Machine Tool Orders - August

- Eurozone: ZEW Economic Sentiment Index - September

Wednesday, September 13

- Japan: Producer Price Index - August

- UK: GDP, Industrial and Manufacturing Production - July

- Eurozone: Industrial Production - July

Thursday, September 14

- Japan: Machinery Orders, Industrial Production - July

- European Central Bank Interest Rate Decision

Friday, September 15

- China: Industrial Production, Unemployment Rate, Retail Sales - August

- Eurozone: Labor Cost Index, Wage Growth - 2Q 2023

As you can see below, quarterly earnings will slow to a mere trickle next week but make no mistake the market will be hanging on what Oracle (ORCL) and Adobe (ADBE) have to say about enterprise spending, cloud and, of course, AI.

Taking up the earnings slack will be another week of investor conferences including:

- the Piper Sandler Growth Frontiers Conference

- the Morgan Stanley 21st Annual Global Healthcare Conference,

- Barclay's 21st Global Financial Services Conference

- Goldman Sachs 30th Annual Global Retail Conference

Much as we did this week, we will be listening to company presentations updating our thoughts for what lies ahead for the market, economy, stocks in the portfolio and ones we are closely watching.

Here's a closer look at the earnings reports coming at us next week:

Monday, September 11

- Close: Casey's General Store (CASY), Mission Produce (AVO), Oracle (ORCL)

Wednesday, September 13

- Open: Cracker Barrel (CBRL)

- Close: Lovesac (LOVE)

Thursday, September 14

- Open: Korn/Ferry (KFY)

- Close: Adobe (ADBE), Lennar (LEN)

ONEs

Applied Materials Inc. AMAT; $147.53; 275 shares; 1.09%; Sector: Semiconductor Manufacturing

WEEKLY UPDATE: At the Goldman Sachs Communacopia + Technology Conference this week, Applied CEO Gary Dickerson shared its IoT, communications, auto, power and sensors end markets are "doing extremely well." Dickerson also touched on the growing demand for chips related to EVs, AI and AI servers, and other markets, which in total should continue to drive a mid-to-high-single compound annual growth rate for chips, in turn driving demand for semiconductor capital equipment. He also shared that pandemic inspired efforts to re-shape the company's supply chain combined with price increases and other cost reduction efforts should drive favorable margins in the coming quarters. Also, this week, Applied declared its next quarterly dividend of $0.32 per share, which will be paid on December 14 to shareholders of record on November 24. We would like to add more AMAT shares to the portfolio, and we are inclined to do so closer to $140. If the shares breach the 50-day moving average near $144, the next stop may be the 100-day moving average near $134. While such a move may be somewhat painful, it would offer an opportunity for us to potentially back up the truck for AMAT shares.

1-Wk. Price Change: -4.2% Yield: 0.9%

INVESTMENT THESIS: Applied provides manufacturing equipment, services and software to the semiconductor, display, and related industries. With its diverse technology capabilities, Applied delivers products and services that improve device performance, power, yield and cost. Applied's customers include manufacturers of semiconductor chips, liquid crystal, and organic light-emitting diode (OLED) displays, and other electronic devices. Applied operates in three reportable segments: Semiconductor Systems (73% of 2022 revenue, 78% of 2022 operating income), Applied Global Services (22%, 19%), and Display and Adjacent Markets (5%, 2%). Key customers include Samsung (12% of 2022 sales), Taiwan Semiconductor (20%), and Intel (10%). The company has a rising dividend bias with the current annualized dividend reaching $1.28 per share vs. the 2017 dividend of $0.43 per share and 2018's $0.64 per share.

Target Price: Reiterate $165; Rating: One

RISKS: Manufacturing and Supply Chain, Competitive Factors, Government Regulation, Technology Change.

ACTIONS, ANALYSIS & MORE: We're Pulling This Name Up From the Bullpen, Investor Relations.

Amazon AMZN; $138.23; 835 shares; 3.11%; Sector: Consumer Discretionary

WEEKLY UPDATE: With disposable income poised to come under pressure in the coming months, we continue to see consumers leaning into digital shopping and Amazon in particular to stretch those dollars. We'll look for confirmation with next week's August Retail Sales report. Let's remember, the current quarter benefits from Amazon's 2023 Prime Day event and the company is planning a similar event - Prime Big Deal Days - for early in the December quarter. In our view, those events are tapping into the customer mindset and should allow Amazon's to grab share gains. As we know, Amazon has a few differentiators compared to most retailers, including Amazon Web Services (AWS), its growing and high margin advertising business, and its healthcare efforts. Data collected by Bloomberg Intelligence sees Amazon's advertising business growing to $100 billion by 2028 and calls it one of Amazon's most profitable business with operating margins of 40%-50%. Those two businesses along with improving digital shopping volumes and cost reduction efforts should drive further margin expansion at the company in the coming quarters. This week Needham names Amazon (AMZN) one of three long-term beneficiaries from generative AI. Also, this week, Shopify (SHOP) and Amazon struck a deal to allow Shopify merchants to offer a Buy with Prime option for payment processing and fulfillment, something we see as a win for Amazon. And as we move through September, the Federal Trade Commission is expected to file an antitrust lawsuit against Amazon focusing on some of Amazon's business practices, such as its Fulfillment by Amazon logistics program and pricing on Amazon.com by third-party sellers.

1-Wk. Price Change: 0.1%; Yield: 0.0%

INVESTMENT THESIS: We believe upside will result from Amazon's continued eCommerce dominance, AWS' continued leadership in the public cloud space, and ongoing growth of the company's advertising revenue stream, which feeds off Amazon's eCommerce business. Additionally, we believe profitability will continue to improve as AWS and advertising account for a larger portion of total sales as both these segments sport higher margins than the eCommerce operation. And while we believe the increasing share of revenue from these higher margin businesses will be key to driving profitability longer-term, we believe margins on eCommerce stand to improve as the company's infrastructure is further built out and economies of scale further kick in. The embedded call option is that management is always looking to enter a new space and generate new revenue streams.

Target Price: Reiterate $170; Rating: One

RISKS: High valuation exposes the stock to volatile swings, eCommerce has exposure to slower consumer spending, and competition, management is not afraid to invest heavily, potential headwinds resulting from new eCommerce regulation in India, and management is not scared to invest aggressively for growth, which can at times cause volatile reactions as near-term concerns arise relating to the impact on margins.

ACTIONS, ANALYSIS & MORE: FY2Q21 Earnings Analysis (7/29/21), 2020 Letter to Shareholders (4/15/21), Initiation (2/2/18), Investor Relations

Axon Enterprise Inc. AXON; $214.71; 765 shares; 4.43%; Sector: Aerospace & Defense

WEEKLY UPDATE: At the Goldman Sachs Communacopia and Technology conference, Axon held a fireside chat with COO and CFO Brittany Bagley. Bagley recapped the company's history and development from tasers to body cameras and software tools, but also touched on its efforts to utilize AI and other technologies. She also called out the opportunity to cross-bundle all of the company's offerings as more productivity and software tools become available as part of its Officer Safety Program (OSP). For context, during the chat it was shared that exiting its last quarter Axon had $5.3 billion of future contracted revenue on the balance sheet, which is more than 3x consensus revenue for next year. As the new Taser 10 product matures, the expectation is it will carry higher margins compared to recent quarter, putting them on par with past margins by mid-2024. While the company continues to see a large opportunity at the federal level, it is also targeting opportunities in the justice department, private security, hospital security and other adjacent opportunities. With prospects for further margin expansion and the ramp of next-generation products as public safety stimulus spending continues to flow, we remain bullish on AXON shares.

1-Wk. Price Change: -0.3% Yield: 0.00%

INVESTMENT THESIS: Axon Enterprise Inc develops, manufactures, and sells conducted energy devices and cloud-based digital evidence management software designed for use by law enforcement, corrections, military forces, private security personnel, and private individuals for personal defense. The company operates in two segments: Taser and Software & Sensors. Taser develops and sells CEDs used for protecting users and virtual reality training. Software & Sensors manufactures fully integrated hardware and cloud-based software solutions such as body cameras, automated license plate reading, and digital evidence management systems. Axon delivers its products worldwide and gets most of its revenue from the United States. President Biden's fiscal year 2023 budget requests a fully paid-for new investment of approximately $35 billion to support law enforcement and crime prevention -- in addition to the President's $2 billion discretionary request for these same programs. According to Mordor Intelligence, the wearable, and body-worn cameras market on its own was valued at $1.62 billion in 2020 and is expected to reach $424.63 billion by 2026.

Target Price: Reiterate $255; Rating: One

RISKS: Manufacturing and supply chain, competitive factors, government regulation, technology change.

ACTIONS, ANALYSIS & MORE: Strong Demand Bodes Well for This Conducted Energy Devices Firm, Initiating a New Position in a Public Safety Technology Name, Investor Relations.

Bank of America Corp. BAC; $28.36; 3,615 shares; 2.77%; Sector: Financial Services

WEEKLY UPDATE: There wasn't much to drive banking stocks higher this week. Interest rates were steady on the long end of the curve and the economic data portrays continued strength in some sectors of the economy. BAC shares caught a Buy rating late in the week from HSBC with a target of $35. AAP team member Helene Meisler shared her view that should the $27-$28 level on the chart hold, the shares may look to move higher. From a fundamental perspective, prospects for net interest income remain favorable, and we'll continue to watch loan activity as well as the potential rebound in investment banking activity.

1-Wk. Price Change: -2.1% Yield: 3.4%

INVESTMENT THESIS: Bank of America is one of the world's leading financial institutions, serving individual consumers, small and middle-market businesses, and large corporations with a full range of banking, investing, asset management and other financial and risk management products and services. The company provides unmatched convenience in the United States, serving approximately 67 million consumer and small business clients with approximately 3,900 retail financial centers, approximately 16,000 ATMs and award-winning digital banking with approximately 56 million verified digital users. Bank of America is a global leader in wealth management, corporate and investment banking, and trading across a broad range of asset classes, serving corporations, governments, institutions, and individuals around the world. Bank of America offers industry-leading support to approximately 3 million small business households through a suite of innovative, easy-to-use online products and services. The company serves clients through operations across the United States, its territories and approximately 35 countries. From a reporting basis, the company's business breaks down as follows: Net Interest Income breakdown: Consumer Banking 57%, Global Banking 23%, Global Wealth & Investment Management 14%, and Global Markets 6%; Income Before Tax breakdown: Consumer Banking 42%, Global Banking 27%, Global Wealth & Investment Management 16%, and Global Markets 15%. Bank of America pays a quarterly dividend of $0.22 per share.

Target Price: $37; Rating: One

RISKS: Financial markets, fiscal, monetary, and regulatory policies, economic conditions, and credit ratings.

ACTIONS, ANALYSIS & MORE: We're Upgrading and Building Upon a Position, We're Initiating a Bank Position, Investor Relations

Clear Secure Inc. YOU; $21.23 ; 5,935 shares; 3.4%; Sector: Technology

WEEKLY UPDATE: While there was no Clear specific news this week, airline partner United Airlines (UAL) presented at the TD Cowen 16th Annual Global Transportation Conference. During that presentation, the company reiterated its prior guidance for the quarter calling for momentum in the June quarter continuing in the back half of 2023. This week YOU shares hit a 52-week low, and we would remind you exiting the June quarter Clear had ~$50 million remaining under its current share repurchase authorization after buying back 1.8 million shares alone in 1H 2023. We would not be surprised to learn the company is scooping up shares at current levels when it reports its September quarter. Catalyst we are watching for include additional airport wins as part of its goal for the top 75 US airports and the pending launch of its TSA PreCheck Enrollment product, one that should be accretive to margins.

1-Wk. Price Change: -2.4%; Yield: 1.3%

INVESTMENT THESIS: Clear Secure is involved in the creation of a frictionless travel experience while enhancing security. Its secure identity platform uses biometrics to automate the identity verification process through lanes in airports, which helps to make the travel experience safe and easy.

Target Price: Reiterate $37; Rating: One

RISKS: Membership growth, partnership retention, and growth, competitive dynamics, new product offerings.

ACTIONS, ANALYSIS & MORE: We're Initiating a Position in This Identity Platform Company,We're Securing This Company a Spot in the Bullpen, Investor Relations.

Coty Inc. COTY; $11.31; 12,030 shares; 3.67%; Sector: Consumer Discretionary

WEEKLY UPDATE: We continue to see Coty's management team pulling the right levers to expand its business in a tactical fashion, driving costs out of the business, while also improving its balance sheet leverage. In short, the team is executing on the turnaround plan it laid out when CEO Sue Nabi took charge in the 2020. Efforts to drive top line growth have been successful, but the larger improvement has been on the company's cost structure with gross margins reaching 63.9% over this last year compared to 58.10% in 2020. With another round of pricing taking hold as we head into the seasonally strongest time of year for the company, we remain bullish on COTY shares.

1-Wk. Price Change: -2.2%; Yield: 0%

INVESTMENT THESIS: Founded in Paris in 1904, Coty is one of the world's largest beauty companies with a portfolio of iconic brands across fragrance, color cosmetics, and skin and body care. Coty serves consumers around the world, selling luxury and mass market products in more than 130 countries and territories. The company derives almost 45% of its revenue from the Americas, 44% from Europe, Middle East and Africa, and the balance from Asia Pacific. By revenue category, Prestige drives 62% of Coty's revenue but more than 80% of its operating income with the balance derived from its Consumer Beauty segment. Management intends to further grow the Prestige business, expanding its prestige fragrance brands, through the ongoing expansion into prestige cosmetics, and the building of a comprehensive skincare portfolio leveraging existing brands. Management is also targeting margin improvement at its Consumer Beauty brands as well as expanding its presence in China across both of its reporting segments. China's beauty and personal care market is expected to grow at a quicker pace of 5.4% per annum through 2027, putting it at $70 billion-$75 billion by 2027.

Target Price: $15; Rating: One

RISKS: Industry competition and consolidation, product efficacy and safety, currency, brand licensing.

ACTIONS, ANALYSIS & MORE: We're Making Our Portfolio a Little More Beautiful Today, We're Adding a Name to the Bullpen, Investor Relations.

Deere & Co. DE; $399.66 ; 357 shares; 3.85%; Sector: Farm Machinery & Equipment

WEEKLY UPDATE: Purdue University's Center for Commercial Agriculture published its monthly producer sentiment findings for August that showed the Financial Performance Index little changed compared to July (85 vs. 86). Barclays shared its findings from Farm Progress 2023 that while farmers do not expect 2023 and 2024 to be as good as 2021 and 2022, farmer income is expected to remain healthy. At the event, Deere shared its 2024 tractors center on taking precision ag and making it easier for customers to use and operate, which starts with Deere's G5+ Display. The G5+ Display features include the largest screen head offered today, AutoTrac, section control, data sync, and over the air updates - while providing another source of recurring revenue for the company. Deere also showcased its Exactshot technology, which was first shown at CES earlier this year, and allows farmers to reduce the amount of starter fertilizer needed during planting by up to 66%. Exactshot is available today as a precision upgrade and is expected to be released in June '24 for model year 2025 planters. Low dealer inventories, better volumes along with favorable pricing and continued cost improvements and the far better supply chains than second-half 2023 bode well for Deere's EPS generation in the coming quarters. With DE shares closing this week closer to $400, the next level of support comes in at $395.50. A successful test would make for a nice pick-up point for newer members.

1-Wk. Price Change: -4.6% Yield: 1.4%

INVESTMENT THESIS: The global agriculture equipment market size is expected to reach $166.5 billion in 2027, growing at a 6% CAGR over the 2020-2027 period. The favorable outlook for equipment purchases in the coming quarters reflects rising farmer income that historically drives new equipment purchases. At the same time, Deere continues to lean into the sustainability movement with its precision ag offering. That technology is helping farmers drive crop yields higher while also realizing cost savings, which makes the new technology a productivity upgrade compared to older equipment. In February, Deere announced a 4.2% in its quarterly dividend per share to $1.25 from $1.20.

Price Target: Reiterate $500; Rating: One.

RISKS: Geopolitical uncertainty, economic conditions, raw material, and other input prices, prices for key agricultural commodities.

ACTIONS, ANALYSIS & MORE: Initiation (10/25/21), Investor Relations

Elevance Health Inc. ELV; $448.75; 275 shares; 3.3%; Sector: Health Care

WEEKLY UPDATE: None. Elevance will pay its third-quarter dividend of $1.48 per share on Sept. 22 to shareholders of record as of Sept. 8.

1-Wk. Price Change: 1.4%; Yield: 1.3%

INVESTMENT THESIS: Elevance, formerly Anthem/Blue Cross Health, is a premier health care brand that appears to be in the sweet spot for HMO companies. Mostly domestic, this company has a wide reach and coverage across the U.S., serving more than 118 million people via medical, pharmacy, clinical, and care solutions. Founded in 1944, Elevance offers a terrific business model that works in boom or bust economic times. The opportunity to find a company with reliable and dependable revenue and cash flows is right here with Elevance. Revenue growth for this company has surged in recent years, with better than double-digit growth since 2018 as the company thrived during the pandemic.

Target Price: Reiterate $550; Rating: One

RISKS: With any insurance business the risk is high for changes in regulation and government programs. Since the onset of Obamacare more than 10 years ago, companies like Elevance have changed their model to be more in line with a better cost/benefit analysis, reducing waste and squeezing out excesses (as was outlined and suggested in Obamacare). Separately, as the population increases and ages, there is more opportunity for Elevance to grow, but with those changes, there is a risk. Lastly, competition is brisk with some very strong opponents who keep their costs low (Humana, Cigna, UNH, CVS/Healthnet).

ACTIONS, ANALYSIS & MORE: We're Trimming One Stock to Add to Another,2021 Annual Report, 2Q 2022 Earnings Report, Investor Relations.

PepsiCo Inc.PEP; $176.27 ; 730 shares; 3.47%; Sector: Consumer Defensive

WEEKLY UPDATE: Amid renewed concerns over consumer spending, we continue to see the company's beverage and higher margin snacking portfolio performing during the coming quarters. Typically, September-January period is a seasonally strong one for the company's product portfolio. During the week AAP team member Helene Meisler shared she is closely watching the $175 level for technical support for PEP shares. Assuming that support holds, it would be a good place for newer members or those underweight PEP shares relative to the portfolio to pick them up.

1-Wk. Price Change: 0.5%; Yield: 2.9%

INVESTMENT THESIS: PepsiCo is one of the largest food-and-beverage companies globally. It makes, markets, and sells a slew of brands across the beverage and snack categories, including Pepsi, Mountain Dew, Gatorade, Doritos, Lays, and Ruffles. The firm uses a largely integrated go-to-market model, though it does leverage third-party bottlers, contract manufacturers, and distributors in certain markets. In addition to company-owned trademarks, Pepsi manufactures and distributes other brands through partnerships and joint ventures with companies such as Starbucks. The combination of the consumable nature of those products along with PepsiCo's ability to realize price increases has led to consistent revenue, EPS, and dividend growth during both the Great Recession and the Covid pandemic.

Target Price: Reiterate $210; Rating: One

RISKS: Economic conditions, supply chain constraints, raw material costs.

ACTIONS, ANALYSIS & MORE: Adding to 2 Positions on Market Weakness, We're Initiating 1 Name While Adding to Another, This Stock Should Have 'Pep,' Even in a Recession, Investor Relations

TWOs

Alphabet GOOGL; $136.38; 850 shares; 3.13%; Sector: Communication Services

WEEKLY UPDATE: Data from Statcounter put Google's global search engine market share across all devices at 91.85% in August, down from 92.07% in June and 92% in the year ago quarter. Despite the modest dip, the next closest competitor is Microsoft's Bing at 3.03% of the market. This strong position should continue to benefit Alphabet's core advertising revenue stream as should increasing views at YouTube. Data from Nielsen found streaming accounting for 38.7% of total TV usage in July with YouTube in the lead with 9.2% share. This too should benefit the company's advertising revenue stream. Those gains along with improving margins at Google Cloud and other cost reductions should drive favorable margin and EPS comparisons in the coming quarters.

1-Wk. Price Change: 0.5%; Yield: 0.00%

INVESTMENT THESIS: We believe that while search and digital ad dominance are what will carry shares in the near- to- mid-term, longer-term it is the company's artificial intelligence "moat" that will provide for new avenues of growth. AI is what has made the company's search, video and targeted ad capabilities best-in-class and is the driving force behind the company's success in voice (Google Home) and autonomous driving (Waymo). Furthermore, we believe it is this AI expertise that will also make the company more prevalent in other industries, including healthcare via subsidiary Verily, as AI and machine learning continue to disrupt operations across industries. Lastly, compounding out positive view of the company's future opportunities, we believe that Alphabet's free cash flow generation and solid balance sheet set it apart and are what will allow the company to continue taking chances on far-out ground-breaking and potentially world-changing projects. Following the recent rebound in the shares, we would recommend members not commit fresh capital to GOOGL shares at current levels.

Target Price: Reiterate $145; Rating: Two

RISKS: Regulatory risk (data privacy), competition, macroeconomic slowdown impacting consumers and therefore ad buyer activity.

ACTIONS, ANALYSIS & MORE: FY2Q21 Earnings Analysis (7/27/21), Why GOOGL Has Shrugged Off Antitrust Headlines in Early Trading Tuesday (10/20/20)

American Water Works AWK; $137.73; 920 shares; 3.42%; Sector: Utilities

WEEKLY UPDATE: It was another quiet week for American Water. The company continues to benefit from its expanding footprint, and petitions for higher water rates keeping American Water on path through 2027 with its EPS and dividend growth targets. Upside to the company's 2023 guidance could be had depending on acquisition timing, and management indicated it has over $550 million of acquisitions under agreement, including those two sizable deals. Also, in 2H 2023, the company has several general rate increases pending, including ones in California, Indiana, general rate cases in California and Indiana, Kentucky, and Missouri. The company has a solid and expanding base, which paired with additional rate adjustments should help it grow its EPS by 40%-50% between 2022 and 2027, with the same likely for its annual dividend. That gives us a long-term path for AWK shares and argues for the shares steadily moving higher over that time frame. That said, we also understand how the shares trade, which means if the historical seasonal move in AWK shares plays out, we would look to book at least some gains later in the quarter, buying back the shares during the seasonally week December and March quarters.

1-Wk. Price Change: -0.1%; Yield: 2.1%

INVESTMENT THESIS: American Water is the largest and most geographically diverse, publicly traded water and wastewater utility company in the United States, as measured by both operating revenues and population served. The company's primary business involves the ownership of utilities that provide water and wastewater services to residential, commercial, industrial, public authority, fire service, and sale for resale customers. The company's utilities operate in approximately 1,700 communities in 14 states in the United States, with 3.4 million active customers in its water and wastewater networks. Services provided by the company's utilities are subject to regulation by multiple state utility commissions or other entities engaged in utility regulation, collectively referred to as public utility commissions (PUCs). Residential customers make up a substantial portion of the company's customer base in all of the states in which it operates. The company also serves (i) commercial customers, such as food and beverage providers, commercial property developers and proprietors, and energy suppliers, (ii) fire service customers, where the company supplies water through its distribution systems to public fire hydrants for firefighting purposes and to private fire customers for use in fire suppression systems in office buildings and other facilities, (iii) industrial customers, such as large-scale manufacturers, mining and production operations, (iv) public authorities, such as government buildings and other public sector facilities. Because there is usually only one water utility available, the business has a rather wide moat, and the company has used its scale and balance sheet to acquire smaller, regional water utilities thereby further expanding its scale.

Target Price: Reiterate $165; Rating: Two

RISKS: Regulatory oversight risks, environmental safety laws, and regulations, weather-related service disruptions.

ACTIONS, ANALYSIS & MORE: We're Initiating 1 Name While Adding to AnotherInitiating a Position in This Public Water Utility Company, Investor Relations presentation.

Apple AAPL; $178.18; 700 shares; 3.36%; Sector: Technology

WEEKLY UPDATE: Ahead of its September 12 event during which Apple is expected to reveal updated iPhone models with potentially higher price points, China widened a ban on the use of iPhones and other foreign branded devices from government agencies to local governments and state-owned companies. We shared our view China is looking to strong arm Apple as it seeks to diversify its supply chain to India and other markets. We also question the degree to which government officials in China are using iPhones over those from Huawei or other Chinese smartphone companies. Shortly thereafter, Morgan Stanley reiterated its Overweight rating on the AAPL shares commenting it is unlikely China's efforts "turn into something larger" and called the move in AAPL shares overdone. Late in the week, Taiwan Semiconductor (TSM), which supplies chips to Apple and others, reported its August revenue rose 6.2% month over month, the latest sign supporting the seasonal smartphone ramp. Should we see further pressure on the stock, we would look to revisit our "Two" rating closer to $170. Signs of a stronger-than-expected smartphone ramp for 2H 2023 may also lead us to revisit our current rating as well as our price target.

1-Wk. Price Change: -6% Yield: 0.5%

INVESTMENT THESIS: While we acknowledge that near-to-midterm performance remains heavily influenced by iPhone sales, the dynamic is shifting as investors finally place greater emphasis on Services growth. We are bullish on the 5G upgrade cycle and believe longer-term upside will continue to come as Services revenue grows its share of overall sales. Services provide for a recurring revenue stream at higher margins, a factor that serves to reduce earnings volatility while allowing for a higher percentage of sales to fall to the bottom line; as a result, we believe that Services growth and the installed base, are much more important than how many devices the company can sell in each 90-day period. In addition to improved profitability, we also believe the transparent nature of this revenue stream will demand an expanded price-to-earnings multiple as segment sales grow. Furthermore, we believe that Apple's desire to push deeper into the healthcare arena will help make its devices invaluable as more life-changing features are added and the company works to democratize health records. Lastly, also see upside resulting from increased adoption of wearables (think the Apple Watch) and potential new product announcements such as an AR/VR headset or an update on project Titan, the company's secretive autonomous driving program.

Target Price: Reiterate $200; Rating: Two

RISKS: Slowdown in consumer spending, competition, lack of new product innovation, elongated replacement cycles, failure to execute on Services growth initiative.

ACTIONS, ANALYSIS & MORE:FY3Q21 Earnings Analysis (7/27/21), Apple Product Launch Event Takeaways (4/20/21), Takeaways from WWDC (6/22/20), Initiation (1/4/10), Investor Relations

Chipotle Mexican Grill CMG; $1,945.10; 46 shares; 2.41%; Sector: Restaurants

WEEKLY UPDATE: Avocado company Calavo Growers (CVGW) reports its average selling price of avocados fell 38% in its grown segment, which supplies whole avocados like the ones used by Chipotle. That paired with lower chicken prices reported by Pilgrim's Pride (PPC) point to improving input costs at Chipotle. Combined with the lapping of 2022 price increases, we should continue to see nice margin improvement in the coming quarters. Add in Mastercard's comments this week that travel, and entertainment spending remains a bright spot, we can see why Wedbush reiterated its $2,200 price target on CMG shares. Next week brings the August Retail Sales report, and we will be reviewing what it says about restaurant sales during the month. As consumers tighten their belts further in the coming months, we continue to see Chipotle benefiting as they shun higher priced casual dining restaurants. Chipotle will report its September quarter results on October 26.

1-Wk. Price Change: 0.3% Yield: 0.00%

INVESTMENT THESIS: Our investment thesis on shares centers on its offering consumers better-for-you fare while also expanding its geographic density, embracing digital ordering, and bringing to market limited-time menu offerings that should spur traffic and boost average revenue per ticket. With the upside to our price target shrinking, we are once again reviewing the incremental upside and revisiting protein input costs.

Target Price: Reiterate $2,100; Rating: Two

RISKS: Input costs, particularly for the protein complex, labor costs, consumer spending, food safety, industry dynamics, and competition.

ACTIONS, ANALYSIS & MORE: Initiating a New Position in Chipotle, We're Adding Chipotle to the (Bullpen) Menu

Costco Wholesale COST; $551.19 ; 262 shares; 3.89%; Sector: Consumer Staples

WEEKLY UPDATE: Concerns for disposable consumer spending prospects in the coming months keeps us bullish on Costco's business model, its prospects and our position in the shares. We recently downgraded the shares to a Two rating, and we would look to revisit that decision the closer the shares approached $500 (something that is a low probability) or we have reasons to boost our price target to over $600. Next week brings the August Retail Sales report and we will be sizing it up against Costco's recent August sales report.

1-Wk. Price Change: 1.3% Yield: 0.7%

INVESTMENT THESIS: We like Costco's long-term prospects, driven by a club-based operating model that focuses on volumes, not margins, and therefore offers its customers a value proposition of everyday low prices. The strength of this model has created an incredibly loyal customer base with low churn and continued share gains in both bricks-and-mortar and e-commerce. And this is a global concept, evidenced by the strength of sales both in the U.S. and abroad, which includes an emerging China opportunity. We see the company's membership model as a key differentiator vs. other retailers and its plans to open additional warehouse locations in the coming quarters should drive retail volumes and the higher-margin membership fee income as well. We also appreciate management's approach to capital returns and their willingness to return cash when it is in excess on the balance sheet.

Target Price: Reiterate $575. Rating: Two

RISKS: Inability to pass through higher costs, fuel prices, weaker consumer, and membership churn.

ACTIONS, ANALYSIS & MORE: FY4Q21 Earnings Analysis (9/23/21), FY2Q21 Earnings Analysis (3/4/21), Upgrading Costco to a One (2/25/21), $10 Per Share Special Dividend (11/16/20), Recent Buy Alert (2/28/20), Initiation (1/27/20), Investor Relations

Energy Select Sector SPDR Fund XLE; $92.05; 865 shares; 2.15%; Sector: Energy

WEEKLY UPDATE: Continued strength in oil prices fueled further gains in our XLE shares. This led us to prudently ring the register on this position, locking in gains on roughly a quarter of our overall position size. With the remaining XLE shares, we'll be closely watching the prospects for the Fed to be done raising interest rates, China's stimulus efforts to stoke its economy and of course the speed of the US economy with an eye toward oil prices. We will also be watching developments on the supply side following the extension of voluntary supply cuts by Saudi Arabia this week. Should XLE shares continue to move toward our $98 target, we may be inclined to do some additional profit taking.

1-Wk. Price Change: 1.4%; Yield: 3.6%

INVESTMENT THESIS: Energy Select Sector SPDR Fund is an exchange-traded fund (ETF) that tracks the performance of the Energy Select Sector Index. The ETF holds large-cap U.S. energy stocks. It invests in companies that develop & produce crude oil & natural gas and provide drilling and other energy-related services. The holdings are weighted by market capitalization.

Target Price: Reiterate $98; Rating: Two

RISKS: Interest rates, weakness in the broad economy, energy prices.

ACTIONS, ANALYSIS & MORE: Adding to 2 Positions on Market Weakness, We're Initiating a Position in the Energy Sector, State Street Global Advisors SPDR Fact Sheet for XLE.

First Trust Nasdaq Cybersecurity ETF CIBR; $47.02; 2,900 shares; 3.68%; Sector: Cybersecurity

WEEKLY UPDATE: Once again we learned of several data breaches this week, including Iranian hacking groups breaching a US aeronautical organization as reported the FBI and the United States Cyber Command. That keeps us bullish on CIBR shares given the expanding need for companies and other institutions to protect their crown jewels. We continue to favor picking up CIBR shares in the low $40s, but if we see the ETF sprint toward the $50 level, we may be inclined lock in some gains following the move from around $38 in early May.

1-Wk. Price Change: -0.4% Yield: 0%

INVESTMENT THESIS: The First Trust Nasdaq Cybersecurity ETF seeks investment results that correspond generally to the price and yield (before the fund's fees and expenses) of an equity index called the Nasdaq CTA Cybersecurity Index. The Nasdaq CTA Cybersecurity Index is designed to track the performance of companies engaged in the cybersecurity segment of the technology and industrial sectors. It includes companies primarily involved in the building, implementation, and management of security protocols applied to private and public networks, computers, and mobile devices to protect the integrity of data and network operations. To be included in the index, a security must be listed on an index-eligible global stock exchange and classified as a cybersecurity company as determined by the Consumer Technology Association. Each security must have a worldwide market capitalization of $250 million, have a minimum three-month average daily dollar trading volume of $1 million, and have a minimum free float of 20%.

Target Price: Reiterate $62; Rating: Two

RISKS: Cybersecurity spending, technology, and product development, timing of product sales cycle, new products, and services in response to rapid technological changes and market developments as well as evolving security threats.

ACTIONS, ANALYSIS & MORE: We're Swapping One Cybersecurity Stock for Another, ETF Product Summary

Lockheed Martin Corp. LMT; $423.09 ; 265 shares; 3.02%; Sector: Aerospace & Defense

WEEKLY UPDATE: In an financial filing this week, Lockheed updated expectations for F-35 deliveries this year to 97 down from its prior forecast of 100-120 jets. Part of this revision stems from a pushout in the expected start for Lockheed delivering its F-35 Technology Refresh 3 (TR-3) to sometime between April-June 2024 instead of later this year. While Lockheed doesn't think this will have a material impact on its 2023 guidance, our thinking is the number of F-35s delivered in 2024 will hinge on when Lockheed begins shipping TR-3, suggesting we are likely to see downside guidance relative to current consensus expectations. Measured against the U.S. government's current inventory target of 2,456 F-35 aircraft and Lockheed's manufacturing capacity of around 156 per year, this really boils down to a timing issue. Adding to that perspective is the ongoing geopolitical tension that adds another layer of demand for the F-35. LMT shares have come back to levels where we first started the position. Since then, geopolitical tensions have continued to escalate, and the company's backlog has increased as a result. We have room to take advantage of this, something we may consider after digesting comments from Jim Taiclet, Lockheed's Chairman and CEO, next week at Morgan Stanley's 11th Annual Laguna Conference.

1-Wk. Price Change: -5.6% Yield: 2.8%

INVESTMENT THESIS: Lockheed Martin is the largest defense contractor globally and has dominated the Western market for high-end fighter aircraft since the F-35 program was awarded in 2001. Lockheed's largest segment is aeronautics, which is dominated by the massive F-35 program. Lockheed's remaining segments are rotary and mission systems, which is mainly the Sikorsky helicopter business; missiles and fire control, which creates missiles and missile defense systems; and space systems, which produces satellites and receives equity income from the United Launch Alliance joint venture. Historically, the stability of defense spending has been a haven during periods of economic uncertainty, and we see that repeating once again even as geopolitical conflicts are likely to lead to incremental demand for Lockheed's products. The company has increased its dividend consistently over the last 19 years and is widely expected to boost it again in the coming days. In October 2022, Lockheed announced its board authorized the purchase of up to an additional $14.0 billion of LMT stock under its share-repurchase program.

Target Price: $520; Rating: Two

RISKS: Contracts and budget risk with the U.S. government and the Department of Defense, F-35 program funding and renewal, competition, subcontractor issues.

Mastercard MA; $414.84; 275 shares; 3.08%; Sector: Info. Tech

WEEKLY UPDATE: This week we learned July retail sales in the eurozone fell 0.2% month over month, while the UK's retail sales jumped 4.3% vs. year ago levels in August, accelerating from 1.8% in July. Next week brings August Retail Sales for the US as well as for China. We'll be chewing into the figures with an eye toward consumer spending activity, matching it against disposable income prospects and consumer borrowing. With MA shares, the 20-day moving average remains above $400, which tells us the for the last month Mastercard has traded at that level or higher. That is important support and above the long-term resistance of $400. Given our $430 target as well as the $450 consensus price target, members should not be adding to their MA holdings at current level. At the Goldman Sachs Communacopia and Technology conference this week, Mastercard shared travel and entertainment spending remains a bright spot, a positive for our shares of Clear Secure (YOU). Also at the conference, Mastercard reaffirmed it has no plans to boost the rates it charges to business in the US this fall.

1-Wk. Price Change: -0.2% Yield: 0.5%

INVESTMENT THESIS: Mastercard is a card network company that benefits from the secular shift away from cash transactions and toward card-based and electronic payments. On Covid-19 dynamics, we view MA as a "reopening" play and an economic recovery play within technology because its cross-border volumes fell sharply during the pandemic but will rebound as mobility increases and travel restrictions ease. Mastercard has more international exposure relative to Visa, making its growth outlook more susceptible to new travel restrictions. However, we view MA as the better long-term play as we are betting on that inevitable recovery.

Target Price: Reiterate $430 Rating: Two

RISKS: The recovery in cross-border transactions, regulation in payments market, competition from other fintechs, pricing pressures.

McDonald's Corp. MCD; $279.22 ; 300 shares; 2.26%

WEEKLY UPDATE: Shares of McDonald's were upgraded at Wells Fargo to Overweight from Equal Weight with an unchanged price target of $310 vs. our $325 target. Loop Capital also issued positive comments for the company sharing franchise channel checks indicate same-store growth is tracking ahead of expectations. Data from Bloomberg Second Measure found McDonald's US business rose more than 13% in July and nearly 12% in in August. All the above speaks to our view that increasingly cash strapped consumers would trade down from casual and fast casual dining to quick service and fast food. MCD shares remain on our shopping list, but renewed concern over interest rates could lead us to pick the shares up at a better price in the coming days. Next week brings the August Retail Sales report and we will be eyeing what it says about restaurant sales during the month. MCD shares remain on our shopping list.

1-Wk. Price Change: -0.6%; Yield: 2.2%

INVESTMENT THESIS: The company franchises and operates McDonald's restaurants, which serve a locally relevant menu of quality food and beverages in communities across more than 100 countries. Of the 40,275 McDonald's restaurants at year-end 2022, approximately 95% were franchised. The US market accounts for ~40% of total revenue, International 50% and International Developmental Licenses Markets & Corporate ~10%. With consumers facing continued inflation pressures, we see McDonald's winning consumer wallet share as it benefits from pricing action put in place in recent quarters and improving input costs. McDonald's has been paying dividends since, and its next quarterly dividend of $1.52 per share will be paid on September 18 to shareholders of record on September 1.

Target Price: $325; Rating Two

RISKS: Consumer spending, competition, supply chain interruption, franchise business model, employment challenges.

ACTIONS, ANALYSIS & MORE: We're Moving This Bullpen Name Up to the Portfolio, Here's Why We're Adding This Name to the Bullpen, McDonald's Investor Relations.

Marvell Technology Inc. MRVL ; $55.74; 2,000 shares; 3.01%; Sector: Technology

WEEKLY UPDATE: We recently upgraded MRVL shares to a Two rating and that decision was supported by Taiwan Semiconductor's 6.2% month over month increase in August revenue. That largest end market for that company is High Performance Computing, which captures data center and AI, making it a positive for Marvell. In addition to other positive comments about AI adoption made during the week's investor conferences, at the Evercore ISI semiconductor conference this week Marvell shared that in addition to AI it is seeing growth in cloud infrastructure as well. Management also confirmed strength in data center as well as a recovery in its networking business. As we digest those comments and ones coming from other investor conferences next week, we will look to revisit our current MRVL price target with an upward bias.

1-Wk. Price Change: -3.8%; Yield: 0.4%

INVESTMENT THESIS: Marvell is a fabless supplier of high-performance standard and semi-custom infrastructure semiconductor solutions. These solutions power the data economy, enabling the data center, carrier infrastructure, enterprise networking, consumer, and automotive/industrial end markets. With roughly 75%-80% of Marvell's revenue stream tied to digital infrastructure, we see it continuing to benefit from rising content consumption and creation. Pointing to that rising demand that necessitate network densification and the build of digital infrastructure, Ericsson sees global monthly average usage per smartphone reach 46 gigabytes (GB) by the end of 2028 vs. 19 GB in 2023 and 15 GB in 2022.

Target Price: Reiterate $62; Rating: Two

RISKS: Technology risk, customer risk, competition risk, reliance on manufacturing partners and supply chain constraints.

ACTIONS, ANALYSIS & MORE: We're Watching These Three Names Set to Report Thursday, Why We Added This Chip Stock to the Bullpen, Investor Relations.

ProShares Short QQQ ETF PSQ; $10.60 ; 4,070 shares; 1.16%

WEEKLY UPDATE: Shares of this inverse ETF were a positive contributor during August and again this week as the renewed concerns over the course of Fed policy weighed on stocks and Apple shares moved lower. Ahead of next week's August CPI, PPI and Retail Sales reports, we'll continue to hold SH shares. We will also be watching developments on the potential UAW strike next week as well. AAP team member Helene Meisler shared her view that "sometime in mid-September we'll see an intermediate-term oversold condition." That will have us stay in close contact with Helene and Bob Lang regarding the market indicators in the next few weeks. Should we see signs the Fed shifts from a hawkish to more neutral tone, we would be open to exiting our position in PSQ shares subject to the market's technical set up at that time.

1-Wk. Price Change: -1.5%; Yield: 0.0%

INVESTMENT THESIS: ProShares Short QQQ seeks daily investment results, before fees and expenses, that correspond to the inverse (-1x) of the daily performance of the Nasdaq 100 Index. The Nasdaq 100 Index includes 100 of the largest domestic and international non-financial companies listed on The Nasdaq Stock Market based on market capitalization.

Target Price: N/A; Rating Two

RISKS: Because PSQ shares track the inverse of the Nasdaq 100 Index, PSQ shares will move lower when the Nasdaq 100 Index moves higher.

ACTIONS, ANALYSIS & MORE: Selling Shares in 1 Position, Closing Another, Adding to 1, and Initiating 1

ProShares Short S&P 500 ETF SH; $14.03; 3,310 shares; 1.25%

WEEKLY UPDATE: Shares of this inverse ETF were a positive contributor during August and again this week as the renewed concerns over the course of Fed policy weighed on stocks. Ahead of next week's August CPI, PPI and Retail Sales reports, we'll continue to hold SH shares. We will also be watching developments on the potential UAW strike next week as well. AAP team member Helene Meisler shared her view that "sometime in mid-September we'll see an intermediate-term oversold condition." That will have us stay in close contact with Helene and Bob Lang regarding the market indicators in the next few weeks. Should we see signs the Fed shifts from a hawkish to more neutral tone, we would be open to exiting our position in SH subject to the market's technical set up at that time.

1-Wk. Price Change: 1.4%; Yield: 0.0%

INVESTMENT THESIS: The ProShares Short S&P 500 ETF seeks daily investment results, before fees and expenses, that correspond to the inverse (-1x) of the daily performance of the S&P 500. We are using SH shares to blunt market volatility and hedge the portfolio's performance against its benchmark, the S&P 500. Given the tactical nature of this position, we do not expect to hold SH shares for the same length of time as we do the portfolio's long positions.

Target Price: N/A; Rating Two

RISKS: Because SH shares track the inverse of the S&P 500, SH shares will move lower when the S&P 500 moves higher.

ACTIONS, ANALYSIS & MORE: Selling Shares in 1 Position, Closing Another, Adding to 1 and Initiating 1.

Qualcomm Inc. QCOM; $ 106.14 ; 815 shares; 2.33%

WEEKLY UPDATE: Qualcomm shares were under pressure this week following reports China banned iPhones and other foreign smartphones for use in government builds. Later in the week that ban was extended to local government and state-owned companies. Our thinking remains this is a move by China to strong arm Apple as it looks to diversify its supply chain out of China. Also, late this week, Taiwan Semiconductor (TSM) reported its August revenue rose 6.2% month over month, another data point supporting the seasonal ramp in smartphone production is unfolding. We've shared we would look to become more aggressive in QCOM shares near the $105 level. The week over week drop in QCOM share should have us revisiting them next week alongside Apple's Tuesday iPhone event.

1-Wk. Price Change: -8%; Yield: 3%

INVESTMENT THESIS: Qualcomm focuses on foundational technologies for the wireless industry, including 3G (third generation), 4G (fourth generation) and 5G (fifth generation) wireless technologies and processor technologies including high-performance, low-power computing and on-device artificial intelligence (AI) technologies. As a connected processor company, its technology roadmap aims to enable the connected intelligent edge (the next generation of smart devices) across industries and applications beyond handsets, including automotive and the internet of things (IoT). Qualcomm has three reportable segments: QCT (Qualcomm CDMA Technologies) semiconductor business, which develops and supplies integrated circuits and system software based on 3G/4G/5G and other technologies for use in mobile devices; automotive systems for connectivity, digital cockpit and ADAS/AD; and IoT including consumer electronic devices; industrial devices; and edge networking products. QCT accounts for 80%-85% of revenue. QTL (Qualcomm Technology Licensing) licensing business grants licenses or otherwise provides rights to use portions of the company intellectual property portfolio, which includes certain patent rights essential to and/or useful in the manufacture and sale of certain wireless products. QTL accounts for ~15% of Qualcomm's revenue but contributes a greater portion of the company's operating income. The company has been paying a quarterly dividend since 2003, and its next quarterly dividend of $0.80 per share will be paid on September 21 to shareholders of record on August 31.

Target Price: $135; Rating Two

RISKS: Customer risk, technology advancement, competition risk, third party supplier and manufacturing partner risk.

ACTIONS, ANALYSIS & MORE: We're Making Another Call to the Portfolio's Bullpen, Here's When We'd Consider Taking a Position in Qualcomm, Qualcomm Investor Relations

SPDR Gold Shares ETF GLD; $178.08 ; 312 shares; 1.5%; Sector: Commodities

WEEKLY UPDATE: Gold has been on a ride these past couple weeks as the metal's volatility has kicked into gear. A rise above that 200-day moving average was a hopeful sign but a pullback towards that moving average squandered whatever bullishness was present at the end of the month. No harm though, the GLD remains up for 2023 and has found good support at the 200 MA, but the ETF is sitting in a no man's land. This means GLD could go any which way, the chart does not weigh either direction with an advantage. We look for gold to make a bigger move at some point, a breakout over the $180 level would be ideal. We continue to hold gold as a hedge against inflation, uncertain times, and weaker currency.

1-Wk. Price Change: -1.1% Yield: 0.0%

INVESTMENT THESIS: The GLD ETF is a proxy for gold. This "trust" buys and sells gold futures each day to mimic the daily moves in the underlying asset, in this case, gold. We see gold as an ideal hedge against a weaker dollar, strong inflation (which tends to weaken the dollar) alternative, and in uncertain times (worry over war and battles). For the past 15 years, gold has been a strong asset class held by fund managers, countries, and banks. The metal is not correlated with markets and will move based on the demand/supply dynamic in the marketplace. Other precious metals such as silver and platinum are good proxies for the criteria stated earlier, however, gold is far more liquid and offers better upside opportunities.

Target Price: Reiterate $200; Rating: Two

RISKS: Weak inflation data, interest rate risk, dollar strength relative to other currencies, geographic risk.

Trinity Capital Inc. TRIN; $14.26; 4,610 shares; 1.77%

WEEKLY UPDATE: Trinity Capital shared current president and chief investment officer Kyle Brown will become CEO effective January 1, 2024. Current Chairman and CEO Steve Brown will become executive chairman of the board. Ahead of this transition, we would suggest members listen or perhaps listen again to our AAP Podcast conversation with Kyle Brown, which you can find here. We remain interested in expanding the portfolio's exposure to this business development company and are inclined to do so closer to the $14 share price.

1-Wk. Price Change: -2%; Yield: 14.4%

INVESTMENT THESIS: Trinity Capital is a Business Development Company (BDC) that provides debt, including loans and equipment financings to growth-stage companies, including venture-backed companies and companies with institutional equity investors. Trinity aims to generate current income and, to a lesser extent, capital appreciation through its investments. It does this by making investments consisting primarily of term loans and equipment financings and, to a lesser extent, working capital loans, equity, and equity-related investments. Because Trinity is a BDC, it must pay out at least 90% of its net income to shareholders in the form of dividends. Trinity is positioned to fill the gap left by recent bank failures and shareholders should benefit as that lifts the company's investment portfolio and income stream, and its dividend payout to shareholders.

Target Price: $16; Rating Two

RISKS: Global economic, political and market conditions; regulations governing our operations as a BDC; credit facility provisions

ACTIONS, ANALYSIS & MORE: Let's Dig Into the Thesis Behind Our Newest Position, As Banks Start Tightening Up on Loans, Let's Check This Bullpen Stock, Listen as We Make a Bullpen Pick -- and Talk Business Development Cos.; Investor Relations.

United Rentals URI; $463.77 ; 335 shares; 4.19%; Sector: Industrials

WEEKLY UPDATE: Bloomberg Intelligence shared this week that it sees United Rentals' benefitting as federal spending ramps up, nonresidential construction expands, and tight equipment supply supports rental rates. As the firm sees it, unprecedented US funding, as well as private-sector activity, should fuel growth even as the economy slows. It also called out United being the largest equipment rental company in what remains a rather fragmented industry, offering it incremental nip and tuck M&A opportunities. With the full effects of the Biden Infrastructure Law, the Chips Act and the Inflation Reduction Act yet to be felt, we will continue to hold the shares. As fresh construction data is had, we will look to further refine our price target. At current levels, our recommendation is to not commit fresh capital. With URI shares above a 4% position size for the portfolio, we may opt to convert some of those hefty double-digit gains into booked profits for the portfolio and members.

1-Wk. Price Change: -5.6% Yield: 1.3%

INVESTMENT THESIS: United Rentals, the largest equipment rental company in the world, operates throughout the United States and Canada, and has a limited presence in Europe, Australia, and New Zealand. It serves industrial and other non-construction; commercial (or private non-residential) construction; and residential construction. Industrial and other non-construction rentals represented approximately 50% of rental revenue, primarily reflecting rentals to manufacturers, energy companies, chemical companies, paper mills, railroads, shipbuilders, utilities, retailers, and infrastructure entities; commercial construction rentals represented approximately 46% of rental revenue, primarily reflecting rentals related to the construction and remodeling of facilities for office space, lodging, healthcare, entertainment, and other commercial purposes; and residential rentals around 4% of revenue. We see the company benefiting on three fronts -- the seasonal uptick in construction spending; the release of funds and projects associated with the five-year Biden Infrastructure Bill; and the company's nip-and-tuck acquisition strategy that should further enhance its geographic footprint. In January, the company announced a fresh $1 billion buyback authorization following the completion of $4 billion in share repurchases over the 2012-2021 period.

Target Price: Reiterate $500; Rating: Two

RISKS: Industry and economic risk, competition and competitive pressures, and acquisition risk.

ACTIONS, ANALYSIS & MORE: Initiating a Position in This Equipment Rental Company, We're Adding This Equipment Rental Company to the Bullpen, Investor Relations

Universal Display OLED; $158.67; 475 shares; 2.03%; Sector: Semiconductors

WEEKLY UPDATE: During the week, management presented at Citi's 2023 Global Technology Conference on September 7.

Management shared the smartphone market is approaching 50% penetration in terms of organic light emitting diode display adoption, primarily in the premium segment with exposure now coming to mid-tier models. Universal sees further adoption for organic light emitting diode technology in the tablet market, which we take as a nod to Apple's upcoming iPad refresh. Management also called out the longer-term potential in the TV market, as that display technology only accounts for 2%-3% of the market. In terms of the automotive market, Universal discussed the adoption of organic light emitting diode in taillight applications, especially in EVs given their power benefits. We see that savings vs. other display technologies helping drive in-car display wins over the coming quarters. Following the August sales report from Taiwan Semiconductor and recent guidance from Broadcom (AVGO) we are reviewing our $165 price target for OLED shares with an upward bias.

1-Wk. Price Change: -3.3% Yield: 0.9%

INVESTMENT THESIS: Universal Display focuses on the development and commercialization of organic light emitting diode (OLED) technologies and materials for use in display and solid-state lighting applications. OLED displays are capturing a growing share of the display market, especially in the mobile phone, television, monitor, wearable, tablet, notebook and personal computer, augmented reality (AR), virtual reality (VR) and automotive markets. This adoption reflects advantages over competing display technologies with respect to power efficiency, contrast ratio, viewing angle, video response time, form factor and manufacturing cost. Universal's business strategy is to develop new OLED materials and sell existing and new materials to product manufacturers for display applications, such as mobile phones, televisions, monitors, wearables, tablets, portable media devices, notebook computers, personal computers and automotive applications, and specialty and general lighting products. The company also looks to license its OLED material, device design and manufacturing technologies to those manufacturers. As such, Universal has a significant portfolio of proprietary OLED technologies and materials with more than 5,500 patents issued and pending worldwide.

Target Price: Reiterate $165 Rating: Two

RISKS: Patent and Intellectual property protection; maintaining OLED manufacturing and customer relationships; technology risk; market risk.

ACTIONS, ANALYSIS & MORE: We're Initiating a New Position Out of the Bullpen; Let's Visit Two Bullpen Stocks; Universal Display Investor Relations.

Vulcan Materials Company VMC; $216.25; 613 shares; 3.58%; Sector: Building Materials

WEEKLY UPDATE: This week Bloomberg Intelligence shared its view that prospects for long-term aggregates demand should be bolstered by the Infrastructure Investment and Jobs Act, which will expand federal highway spending almost 60% by 2026. As that drives demand, aggregates price gains of more than 15% can fuel margin expansion and Vulcan's balance-sheet strength could foster growth through acquisitions. We concur with that assessment, Vulcan's next quarterly dividend of $0.43 per share will be paid on September 6 to shareholders of record on August 17. The next area of support for VMC shares is the 100-day moving average at $207. At that level, we would look to revisit our Two rating with an upward bias.

1-Wk. Price Change: -3% Yield: 0.8%

INVESTMENT THESIS: Vulcan Materials operates primarily in the U.S. and is the nation's largest supplier of construction aggregates (primarily crushed stone, sand, and gravel), a major producer of asphalt mix and ready-mixed concrete, and a supplier of construction paving services. Its products are the indispensable materials used in building homes, offices, places of worship, schools, hospitals, and factories, as well as vital infrastructure including highways, bridges, roads, ports and harbors, water systems, campuses, dams, airports, and rail networks. Ramping spending associated with the Biden Infrastructure Law should drive demand for Vulcan's products over the coming years. Vulcan has historically complemented its organic growth prospects by acquiring businesses to expand its geographic reach and product scope. Since 2014, the company has acquired more than two-dozen companies, including the 2021 acquisition of U.S. Concrete. That combination has allowed the company to deliver steady top and bottom-line growth over the last decade, with only a modest decline when the pandemic hit in 2020.

Target Price: Reiterate $260; Rating: Two

RISKS: General economic and business conditions; dependence on the construction industry; timing of federal, state, and local funding for infrastructure; changes in the level of spending for private residential and private nonresidential construction.

ACTIONS, ANALYSIS & MORE: Initiation Post, Investor Relations

THREEs

ChargePoint Holdings Inc. CHPT; $5.72; 16,135 shares; 2.49%; Sector: Electrical Components & Equipment

WEEKLY UPDATE: Following another bout of disappointing quarterly results and guidance, we downgraded CHPT shares to a Three rating from One. We also cut our price target to $9 from $15. Despite our more critical eye on ChargePoint and its management team, JPMorgan reiterated its Buy rating while cutting its target to $10 from $13 while Oppenheimer kept its Outperform rating after dropping its target to $14 from $27. Late in the week, after assessing the impact of macro headwinds slowing discretionary spending for the company's residential and commercial channels, Evercore ISI cut its target price to $17 from $20.

1-Wk. Price Change: -23.1% Yield: 0.00%

INVESTMENT THESIS: ChargePoint Holdings designs, develops, and markets networked electric vehicle (EV) charging system infrastructure and cloud-based services which enable consumers the ability to locate, reserve, and authenticate Networked Charging Systems, and to transact EV charging sessions on those systems. As part of ChargePoint's Networked Charging Systems, subscriptions, and other offerings, it provides an open platform that integrates with system hardware from ChargePoint and other manufacturers. According to the U.S. Department of Energy, the U.S. reached a milestone this past year with its 100,000th EV charger installed in 2021. Industry analysts at Guidehouse Insights forecast that a total of 120 million chargers will be needed globally by 2030, providing a meaningful opportunity for ChargePoint to expand its charging footprint. To that end, the U.S. Departments of Transportation and Energy announced nearly $5 billion over the next five years that will be made available under the new National Electric Vehicle Infrastructure (NEVI) Formula Program established by President Biden's Bipartisan Infrastructure Law. NEVI aims to build out a national electric vehicle charging network of high voltage chargers along designated Alternative Fuel Corridors, particularly along the Interstate Highway System.

Target Price: Reiterate $9; Rating: Three

RISKS: EV adoption of passenger and fleet applications, changing technology, subscription renewals.

ACTIONS, ANALYSIS & MORE: We're Calling Up a Name From the Bullpen, The Needle Could Begin to Move on This Bullpen Name, Investor Relations.