Surprisingly Good Jobs News Is Bad News for Fed Rate Cuts

Let's break down the March jobs numbers as Trump ups the tariff rhetoric and the market resizes rate-cut expectations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We’ve talked often here about how good news for the economy is bad news for the market’s expectations for Fed rate cuts. While we expected a miss in private sector job creation could result in a weaker-than-consensus March Employment Report, that is not what we got.

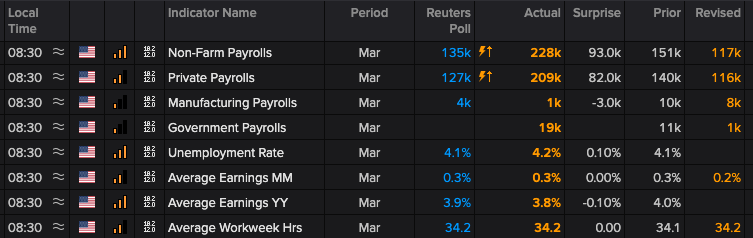

March job creation surprised meaningfully to the upside with 228,000 jobs added during the month, a far quicker pace than the downwardly revised 117,000 for February and the market forecast for 135,000 jobs. Private sector job creation led the upside surprise with 209,000 jobs, which we can see in the table below was far faster than expected and the revised figure for February.

While modest, what stands out is the month-over-month increase in government payrolls to 19,000 jobs when compared against the February and March headlines and findings in the Challenger Job Cuts reports for both of those months. This could be due to the planned nature of government job cuts, something we called out to you Thursday. It does mean at some point, however, we will start to see those planned government job cuts impact the monthly Employment Report. So far, however, that’s not the case.

The Unemployment Rate did edge up to 4.2%, but remains below the Fed’s 4.4% projection for this year shared just a few weeks ago. Given our comment above about government job prospects, we are likely to see the Unemployment Rate tick higher in the coming month. Should we see a pick-up in private sector layoffs, something not indicated in the March Challenger Job Cuts report, that would be another reason to expect the Unemployment Rate to trend higher.

On the inflation front, we see a nice tick lower in year-over-year average hourly earnings to 3.8% from 4.0% the prior month. In all likelihood, this reflects the more subdued hiring we’ve discussed as part of our conversation about March ISM PMI data. However, it does suggest larger job creation in lower-paying jobs, like retail, social assistance, and other areas.

Two Other Items to Note

First, the number of those not in the labor force reached 102.4 million in March, up ~2.5 million year over year. Some of this is likely due to age, but we will want to keep our eyes on this metric in the coming months as it could signal more folks simply giving up on looking for work. As we watch this, we will also examine the payroll to population metric, which while flat at 59.9 in February and March, is lower by a few basis points year over year.

Second, we have to consider the likelihood the March jobs figure will get revised lower just like we saw with the January and February numbers. The change in total nonfarm payroll employment for January was revised down by 14,000 to 111,000 jobs, and for February the revised figure of 117,000 is lower than the original 151,000 figure. On the one hand, 262,000 jobs were still added during the first two months of the year, but that’s 48,000 lower than initially thought.

How Will This Impact Powell's Comments Friday?

Because the March Employment Report was far stronger than anyone had expected, the odds of Fed Chair Powell backing the market’s increased expectations for 4-5 rate cuts this year are extremely low. Rather, this morning’s data mixed with recent inflation data is more likely to result in Powell skewing more cautiously about rate-cut prospects for this year and the Fed remaining data dependent.

Some are expecting the Fed to bake tariffs into its forward view, but the landscape is evolving almost day to day. It could also change based on a presidential tweet, and our thinking is that will keep the Fed in a monetary policy holding pattern at least until upcoming economic data bring more clarity on the economy. In other words, the market will, at least for now, need to reconsider rate-cut prospects and that’s going to remove a potential near-term buoy for the stock market.

Trump Ups the Tariff Rhetoric With China

To all of this we can add President Trump commenting that his policies will "never change" after China retaliates with tariffs. In our opening comments this morning, we discussed why market uncertainty and anxiety are poised to remain, and this only adds to our thinking. While we wait to see how the European Union responds to Trump’s reciprocal tariffs, we will also be watching for a potential next tariff move by Trump with China as well as the expected wave of earnings pre-announcements that now looks even more likely.

While allof this is nerve-wracking, what is unfolding reminds us of some wise words from legendary investor Charlie Munger: “The big money is not in the buying or selling, but the waiting.” In this case, that means waiting for the right opportunities, and for that, we have our eyes wide open.