Doug Kass: A Market Bacchanal Rages On, While I Remain Celibate

Despite the market’s amazing advance, there are many justifiable reasons for our doubt and skepticism.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* Investors are ignoring a number of clearly defined and intensifying fundamental and valuation headwinds

* Investor sentiment and expectations are inflated — market risks are being underappreciated

* Equities remain overvalued — perhaps materially so

* The stock market is a church with a casino attached to it — the casino has grown much more active in recent months

* It feels like deja vu all over again

The magnitude and strength of the recovery in the major indexes during the past month have been anathema to me (and to others who have a taste for value and don’t have a momentum-based orientation). The size and the rapidity of the market’s rally (especially since March) have likely been momentum-driven (due in part to market structure changes over the last decade in which passive products and strategies have dominated the investment landscape).

This backdrop of momentum based machine-driven dominance — in which buyers buy strength (and, ultimately, sellers sell weakness) — has, in turn, led to a great deal of fear of missing out (FOMO). These factors and others (including a strong belief in an AI productivity miracle) have contributed to a record pace of recovery, producing another “V”- type rally from the March 2026 lows.

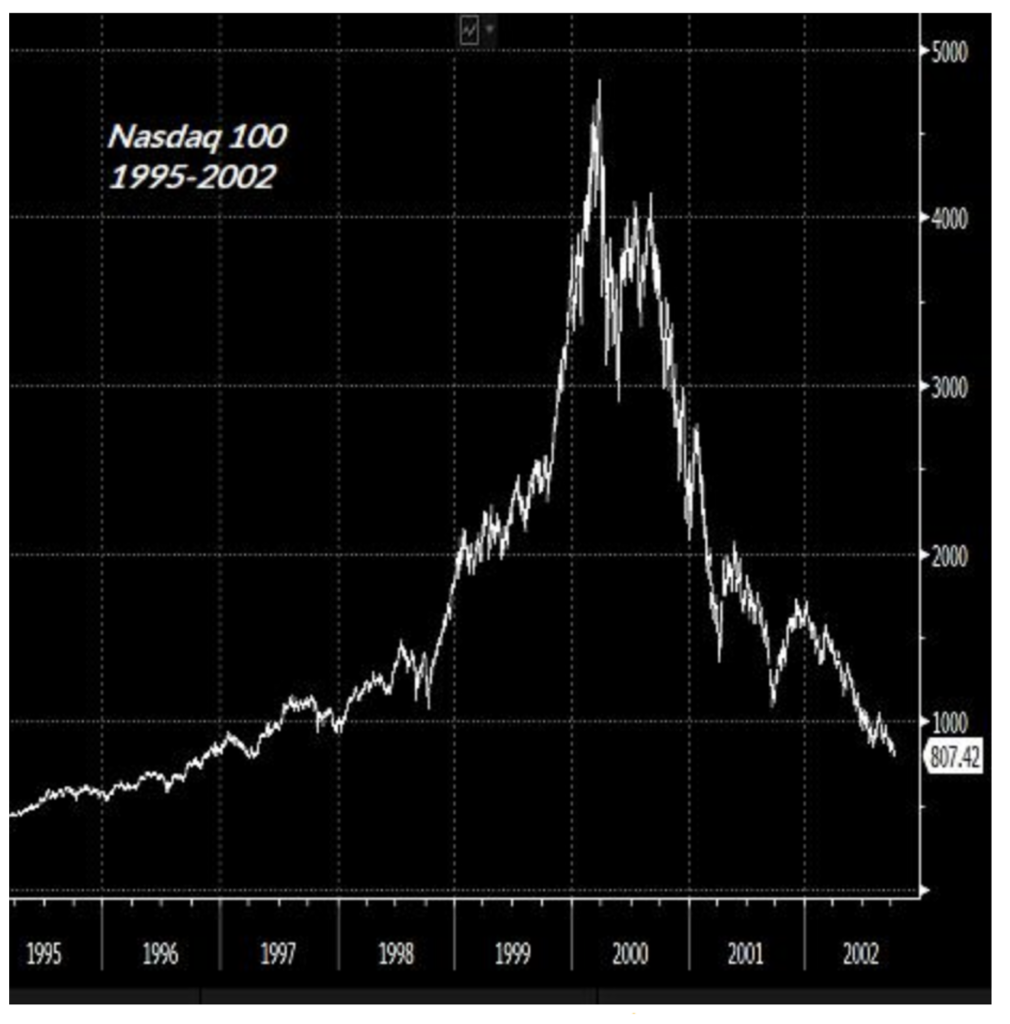

I did not see the extent of this rally coming and remain skeptical of it continuing. Indeed, despite the growing optimism of the consensus, I now see stunning similarities between today’s equity market and previous market tops. Most noticeable is the comparison to the dot-com top in 2000 (a similar period of narrowing/concentrated market leadership and the belief in technology’s new big thing (the internet) to deliver robust revenue/profit expectations (which failed to pan out)):

At times like this I am reminded that incredulity robs us of many pleasures and gives us very little in return! Or as Samuel Johnson wrote:

“To revenge reasonable incredulity by refusing evidence, is a degree of insolence with which the world is not yet acquainted; and stubborn audacity is the last refuge of guilt.”

In today’s missive I have several points to make:

* Though it may appear — to Samuel Johnson (in his above quote) and others — that I am in stubborn denial of the facts (and the market’s amazing advance), I feel I have many justifiable reasons to maintain our doubt and skepticism. I have discussed my reasoning and evidence in my past Diary commentaries and I will expand on those reasons again today.

* Though bullish market participants seem to disagree, it is an unusual and potentially threatening period for the global economy, our markets, our society and for innovation (in which AI is distorting stock prices and profits). I have had a lot to say about this in the past and I will continue in this missive and in the future.

* Main Street and Wall Street have diverged dramatically.

* I will further explain why — despite growing ever more bearish — I have maintained a relatively small net exposure on the short side (and have no current plans to meaningfully expand my short portfolio further).

With the fear of missing out reverberating, there is growing pressure to speculate today. Nonetheless, I will not abandon my disciplines nor forget the lessons of history.

Before expanding on our market view, I wanted to recite a relevant quote from Georg Hegel and cite two examples of differing behavior towards the end of the dot-com boom in 2000:

”What we have learned from history is that too many have not learned from history.”

Below are examples of Berkshire Hathaway’s (BRK.A, BRK.B) avoidance of the dot-com bust and Stanley Druckenmiller’s emotional purchase of tech stocks at the height of the dot-com boom.

1. The stock market, to paraphrase Warren Buffett, is a church with a casino attached to it. In the last several months the casino has become very active!

At the top of the dot-com bubble (and before a -81% drawdown in the Nasdaq), a Berkshire Hathaway shareholder asked Warren Buffett and Charlie Munger “to just speculate” in technology:

2. An example of the consequences of succumbing to speculation (and emotion) occurred around the same time when Stanley Druckenmiller (arguably the greatest modern-day investor) acquiesced to the markets and, within hours of the dot-com top purchased billions of dollars of technology stocks.

Here Stan recounts his investment boner in March 2000, when he purchased $6 billion in tech stocks at the peak of the dot-com bubble, which resulted in losses of about $3 billion in only six weeks:

Another Technology Victim; Top Soros Fund Manager Says He ‘Overplayed’ Hand – The New York Times

Druckenmiller on his $3B loss.

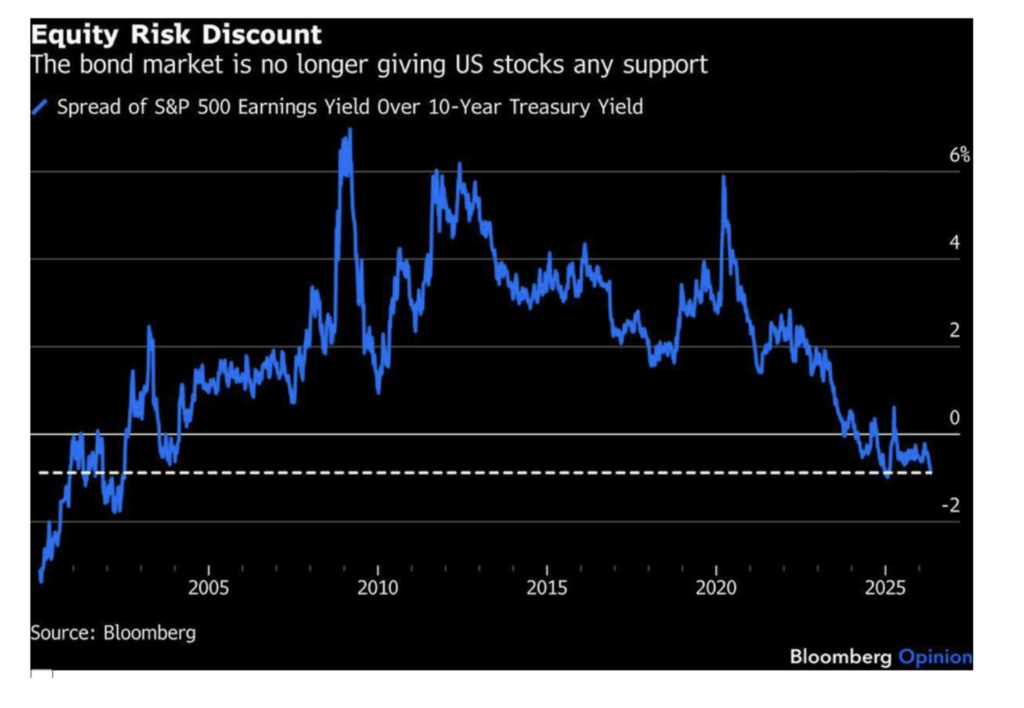

The Equity Risk Premium Is Now at a Discount and the Shiller CAPE Ratio Is Near an All Time High

The chart below, of the equity risk premium, is probably the most important reason for my ursine market view.

The equity risk premium is the difference between the S&P earnings yield (the inverse of the P/E ratio) and the risk-free rate of return.

Surprisingly, the equity risk premium has morphed into an equity risk discount — standing at the deepest discount since 2003. As of Tuesday, the S&P Index’s earnings yield was 90 basis points lower than the risk-free rate of return (using the 10-year yield) — meaning that market participants believe there is more risk in holding bonds than in holding equities!

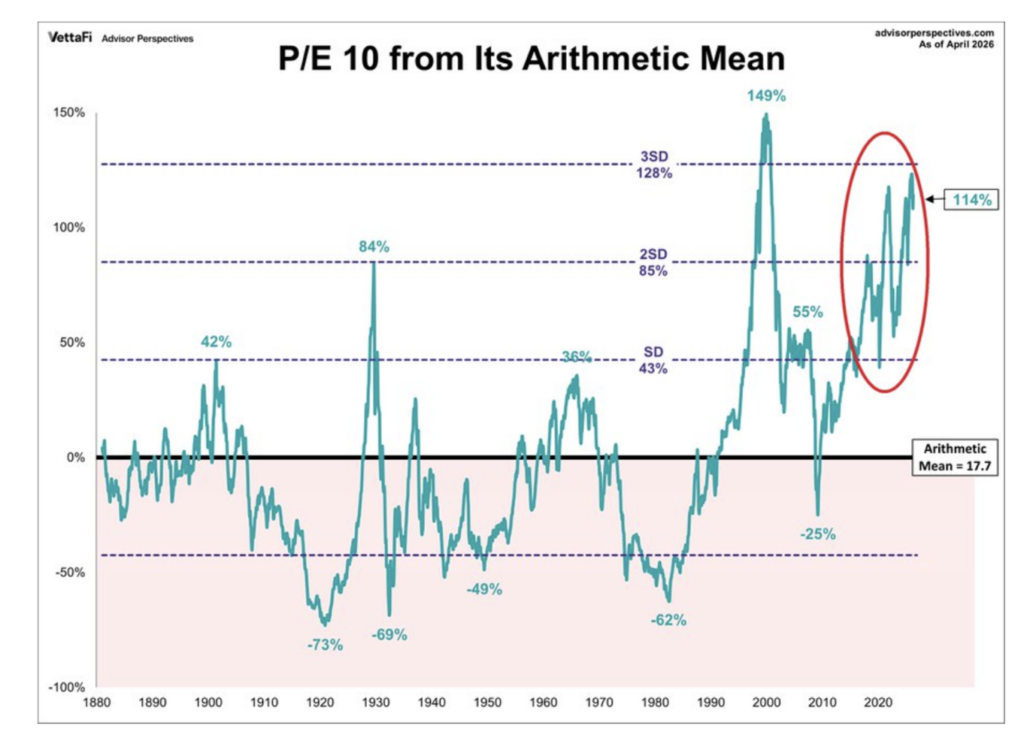

Here is another chart that has concerned us — the P/E 10 ratio. This ratio measures stock prices against the average of 10 years of inflation-adjusted earnings to smooth out short-term business cycle distortions. Thursday’s reading of 37.9 is +114% above its long-run arithmetic mean, placing into a zone only visited once before in the last 150 years — during the dot-com bubble (when it stood at 44.2). Today’s P/E 10 reading is above the level hit in 1929:

The P/E 10 chart above is a derivative of the Shiller CAPE Ratio shown below (which I have presented to you often over the last 24 months). Shiller CAPE now stands at 42.05, a whisker away from the dot-com bubble high of 44.0.

It would take a 60% fall in stocks to reach the historical mean of 17:

Over the last century, every time the equity risk premium narrows considerably (as it currently has (in the extreme) transitioned into an equity risk discount) and the P/E 10 ratio moves as far as it is today from its arithmetic mean — a large decline and mean reversion in investment returns occur.

My Market Concerns Summarized

In my view, the markets have ignored the same conditions that set off the January-February selloff. None of the non-war issues that drove stocks lower have been resolved:

* Oil prices are off their highs but are likely to remain elevated because of the magnitude of the supply shock and continued uncertainties related to the Iran conflict.

* Inflation is now rising on a sequential monthly basis — and is higher than before the conflict in Iran.

* Interest rates will be higher for longer.

* The 2026 annual deficit will approach $2 trillion, and neither political party show any signs of being fiscally responsible.

* The U.S. debt will hit $40 trillion this year — the cost of servicing the debt is over $1 trillion/year.

* With a burgeoning deficit, stiff debt load and persistent inflation, the Fed’s hands are tied.

* While private equity’s problems are not systemic, the leverage they brought us remains in place. KKR Private-Credit Fund Takes $560 Million Loss – WSJ

* The enormous amount of money spent on AI will probably never see an adequate return on investment. As noted by Stan Druckenmiller (again!), AI’s societal and transformative impact could rival the internet’s life-changing influence — and so may the stock market consequences (rhyme) be similar:

“If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to fruition. That’s not going to happen with AI. But it could rhyme – AI could rhyme with the Internet as we go through all this capital spending we need to do. The big payoff might be four to five years from now. So AI might be a little overhyped now but under-hyped long term.”

* Valuations are a terrible clock but a good weather forecast. That valuations are stretched is an understatement. See CAPE Shiller in Part 2. The Buffett ratio (the total market capitalization divided by GDP) hit an all-time high this week). Most other traditional metrics indicate that equity valuations are in the 97 percentile.

* Many bulls highlight the improving strength in projected 2026 S&P EPS. They argue that this year’s robust growth in profits (at about +17%) justify current valuations. However, if one takes out Nvidia (NVDA) and Micron (MU), 2026 S&P EPS growth falls to under +10%:

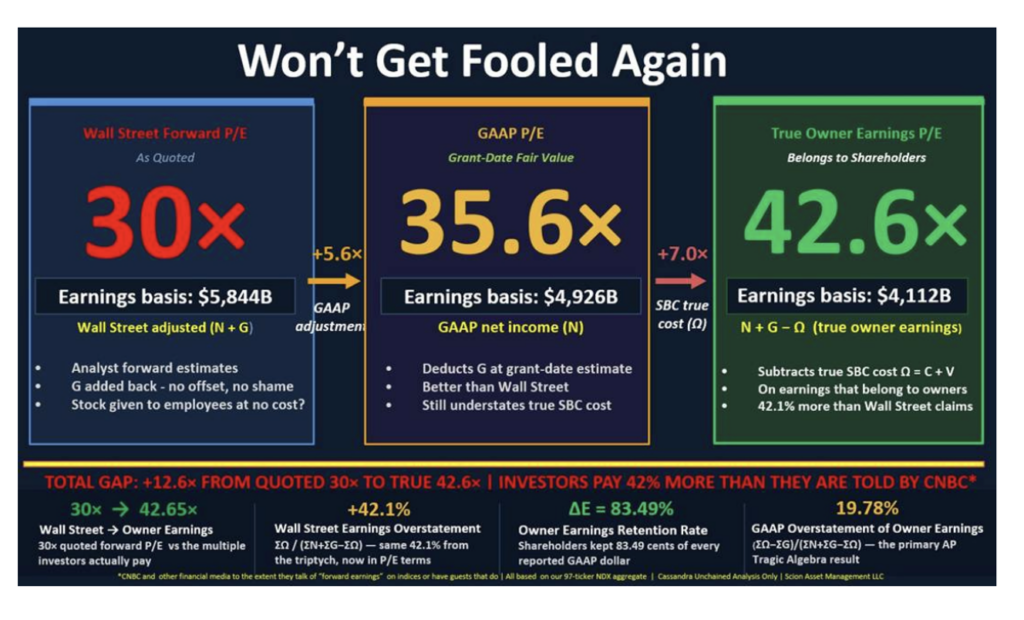

Almost no tech stock, not even the bombed-out software stocks, are inexpensive when held to strict accounting standards, more strict and more forensic in nature than GAAP.

Michael Burry hits the target in his recent commentary:

The NASDAQ 100’s true PE is closer to 43x than the 30x Wall Street tells us.

In addition to the effects of stock-based compensation, previously discussed problems with depreciation policies, construction-in-progress, M&A costs, capital leases, and other necessary adjustments to GAAP net income to find true owners’ earnings.

Including all these adjustments, Wall Street may be overstating by more than 50% the earnings at our fastest growing, most highly valued companies.

In addition, there is the likelihood of future write-downs, in large measure stemming from the numerous circular financings. (Cisco in 2021 and 2002 wrote down years of its best earnings when it had to write off the same types of contracts with its suppliers).

Most investors are now convinced we are in a continued bull market led by AI-related equities.

However, the anatomy of a bear market (we will not know until after the fact!) is that there are violent rallies.

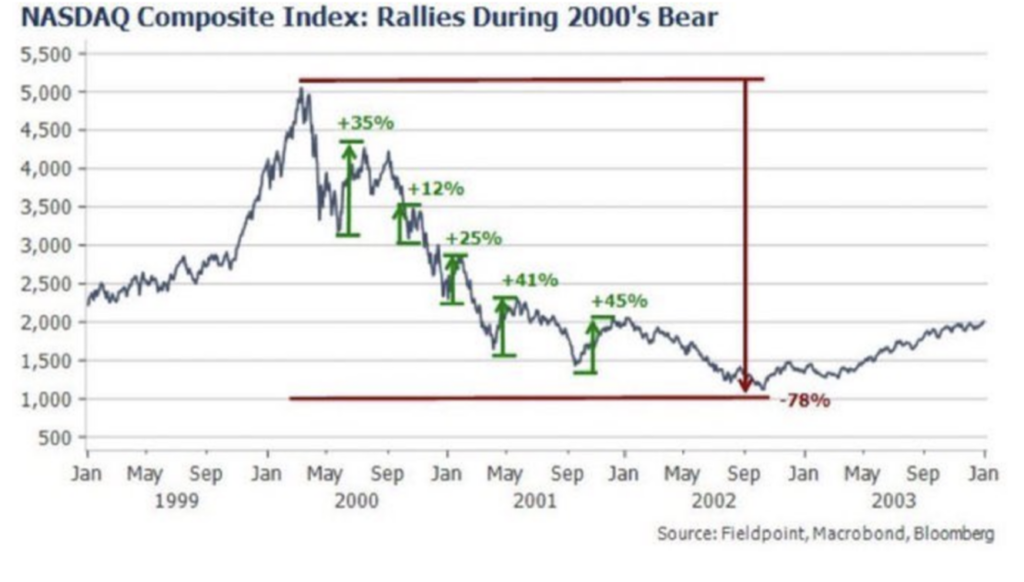

As noted earlier, a classic and extreme example was when the Nasdaq declined by -81% (2000-2002) following the dot-com boom in which the revolutionary impact of the internet was heralded and applauded in the indexes.

Along the way to the nearly 80% drop, there were five robust rallies of between +12% and +45%. The average gain in the rallies was +33%.

Every rally felt like a bottom, but every rally was a trap:

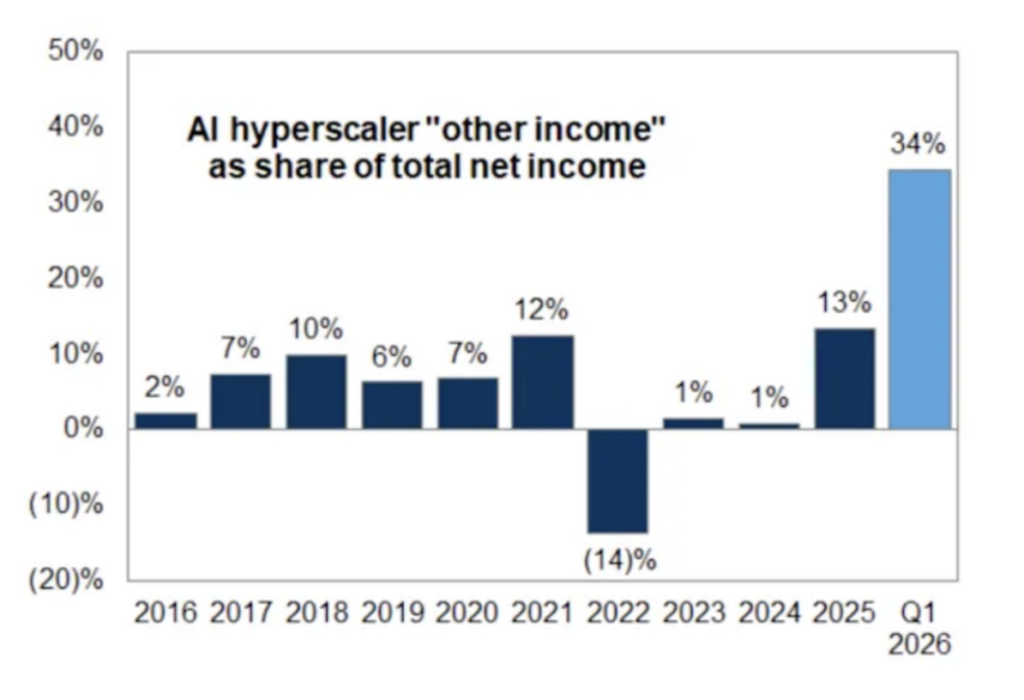

I see multiple traps ahead, including financing circularity and quality of earnings (the other income line has been aided by sizeable increases in private investment valuation marks – below), among other issues (like the large erosion in hyperscaler free cash flow):

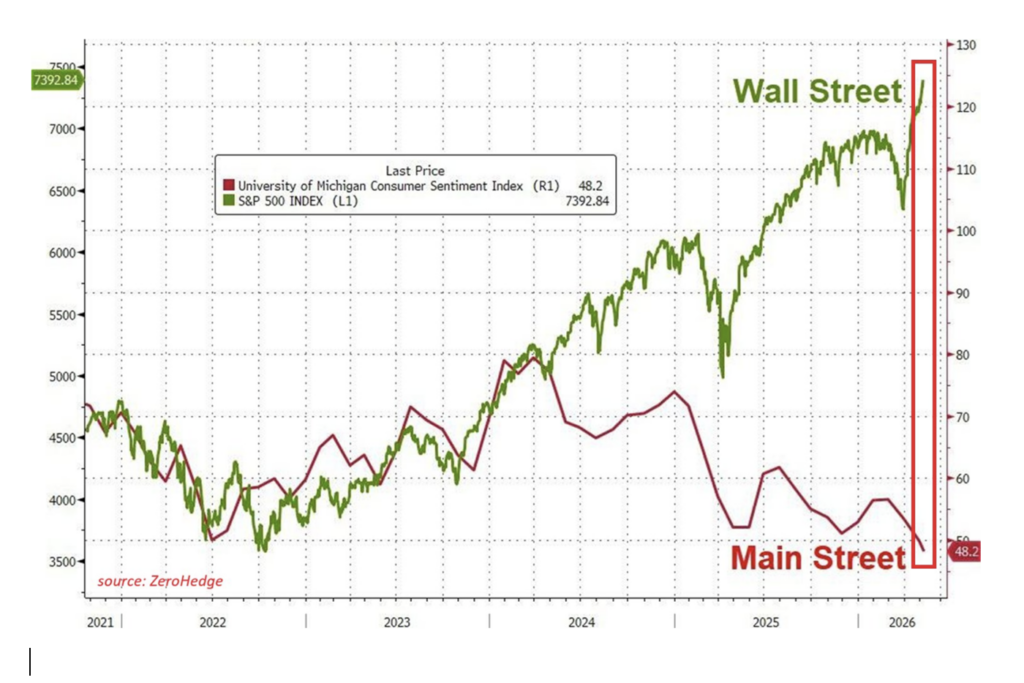

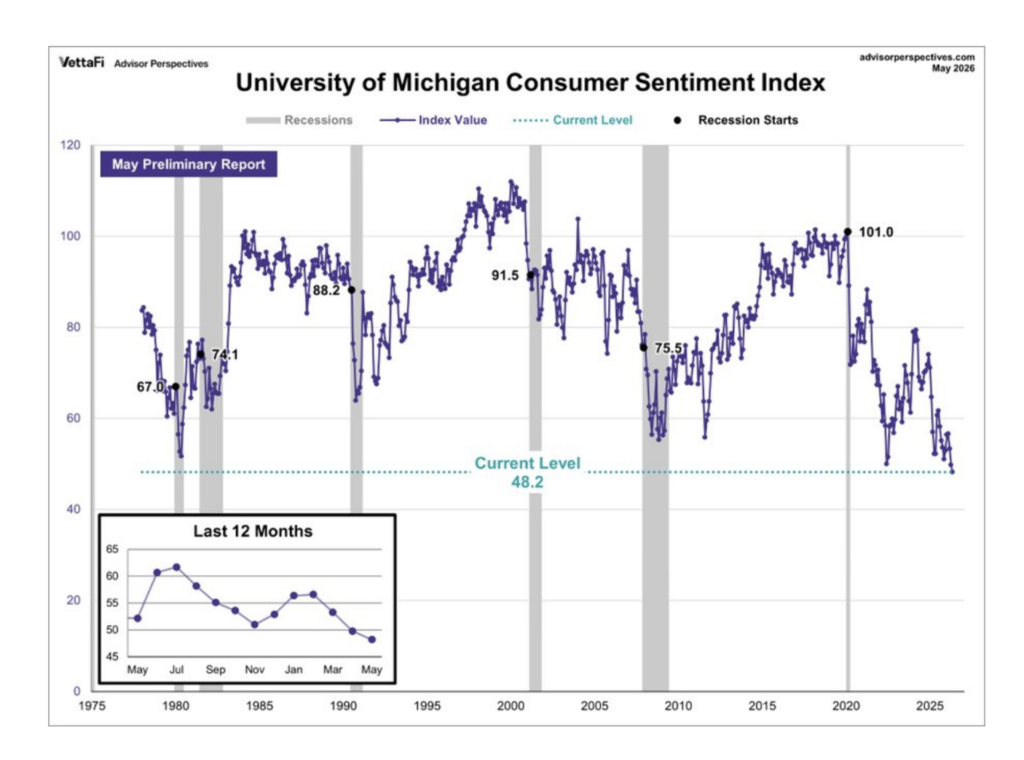

A K-Shaped Economy Has Produced Distortions in Consumer Sentiment and Stock Prices

We are mindful of the gap between Wall Street and Main Street:

As an illustration of the Main Street/Wall Street comparison, here is the stock price chart of Home Depot (HD):

With inflation high and the economy weakening, should equities decline, the weakness in the K-shaped economy could begin to impact the middle and upper-middle classes —adversely impacting aggregate economic growth.

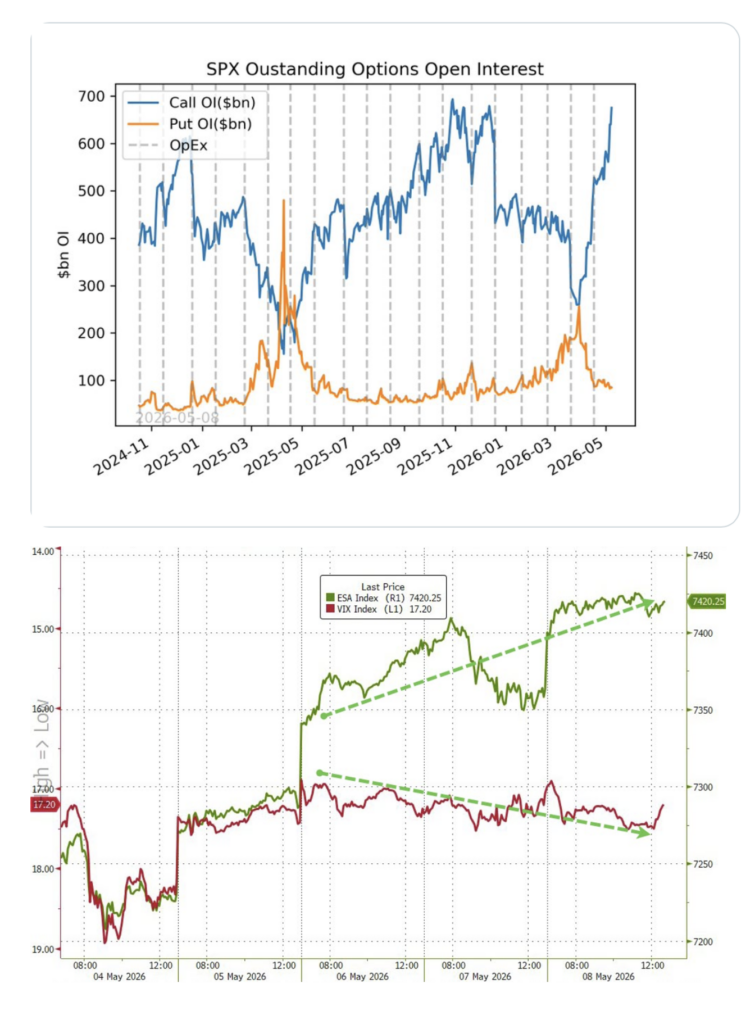

The Casino Is in Overdrive… And We Refuse to Gamble

As mentioned, the stock market is now acting less like a church (which respects valuations) and more like a casino.

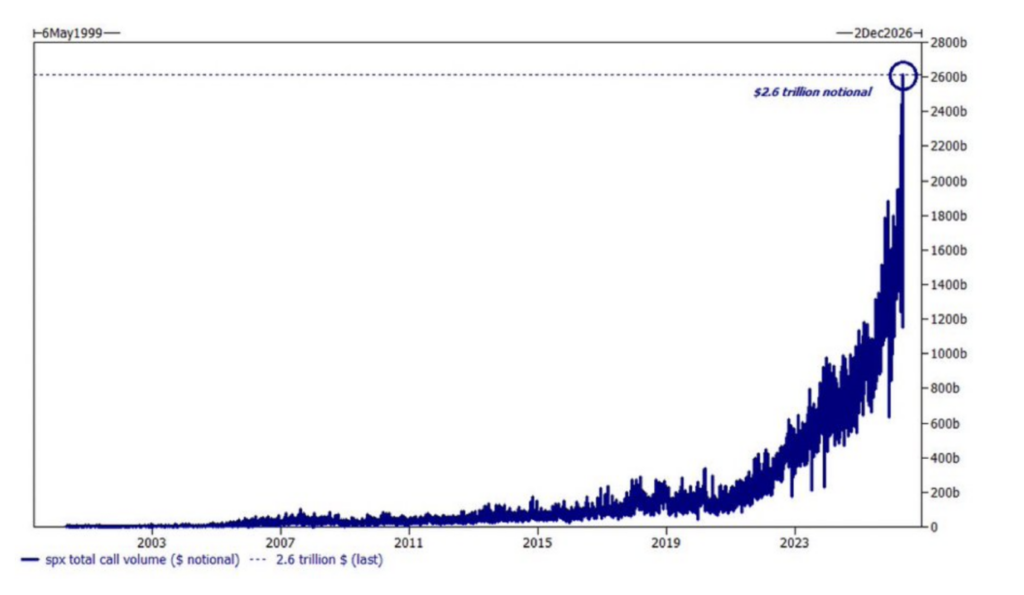

Last Thursday the market did something it has literally never done before. The S&P traded $2.6 trillion in call options — that is the highest single day call volume in market history:

When traders buy massive amounts of calls the market makers selling those calls are forced to hedge by buying the underlying stocks. That buying pushes prices higher. Higher prices force more hedging. More hedging pushes prices higher again. This is called a gamma squeeze. It works well on the way up. It’s brutal on the way down.

The entire market is in an unprecedented gamma squeeze. Open interest at all-time high, outstanding delta above $4.2 trillion — an all-time high:

In the context of this speculation, I plan to continue to have some net short exposure. However, given the respect I have for the historical conditions of late speculative cycle markets (they go further than anyone expects!) and the forceful impact of passive strategies and products (driven by algorithms), I will, consistent with my risk appetite, keep my net short exposure low.

Nonetheless, there will come a time that I will expand my short book.

Bottom Line

“It is always well to accept your own shortcomings with candor but to regard those of your friends with polite incredulity.”

– Russell Lynes

As noted in a previous post It’s a Mad, Mad, Mad, Mad Investment World.

Today’s commentary shares my views and tries to attach empirical evidence and observations that support a skeptical market outlook.

I continue to be reminded of Warren Buffett’s quote:

“What the wise do in the beginning, fools do in the end.”

With the same intended message, Barton Biggs was more colorful when he said:

“A bull market is like sex. It feels best just before it ends.”

Citigroup’s CEO Charles Prince — in July 2007, only months before The Great Financial Crisis (and historic market decline) — had a different view (as reported in an interview he had with The Financial Times):

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

That said, with the S&P 500 making an all-time record in May — and despite my protestations — it is abundantly clear that, for now, neither the markets nor most market participants (human and machine) share my outlier, non-consensus and ursine outlook.

Market participants are still at the bacchanal — while I remain celibate.

This commentary was previously posted in Doug’s Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.