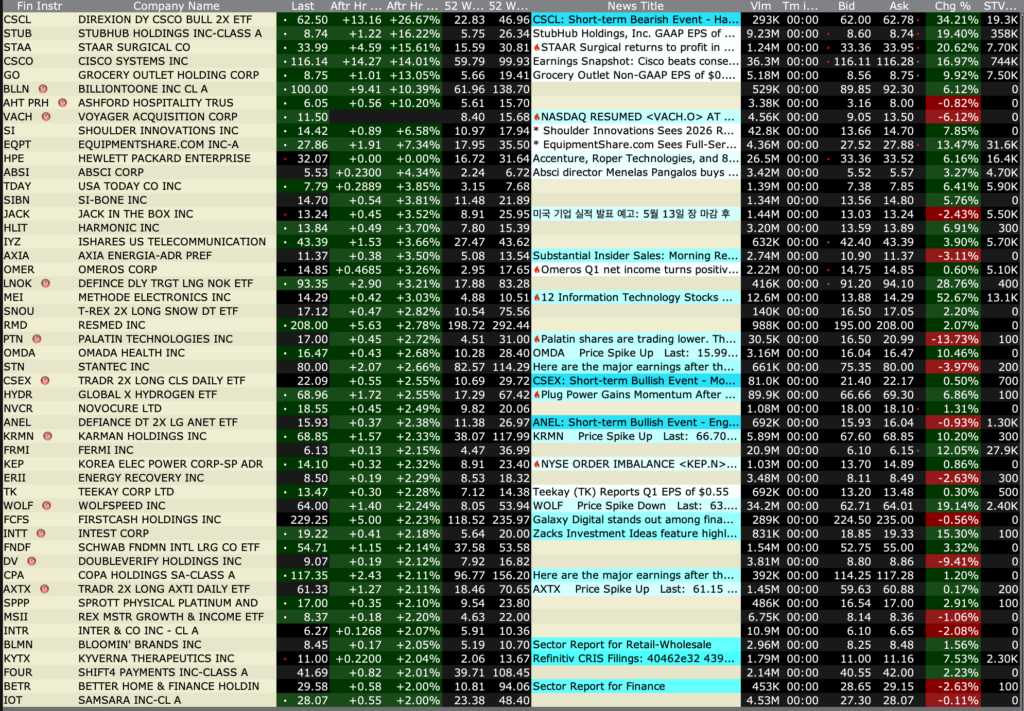

Wednesday After-Hours Advancers and Decliners

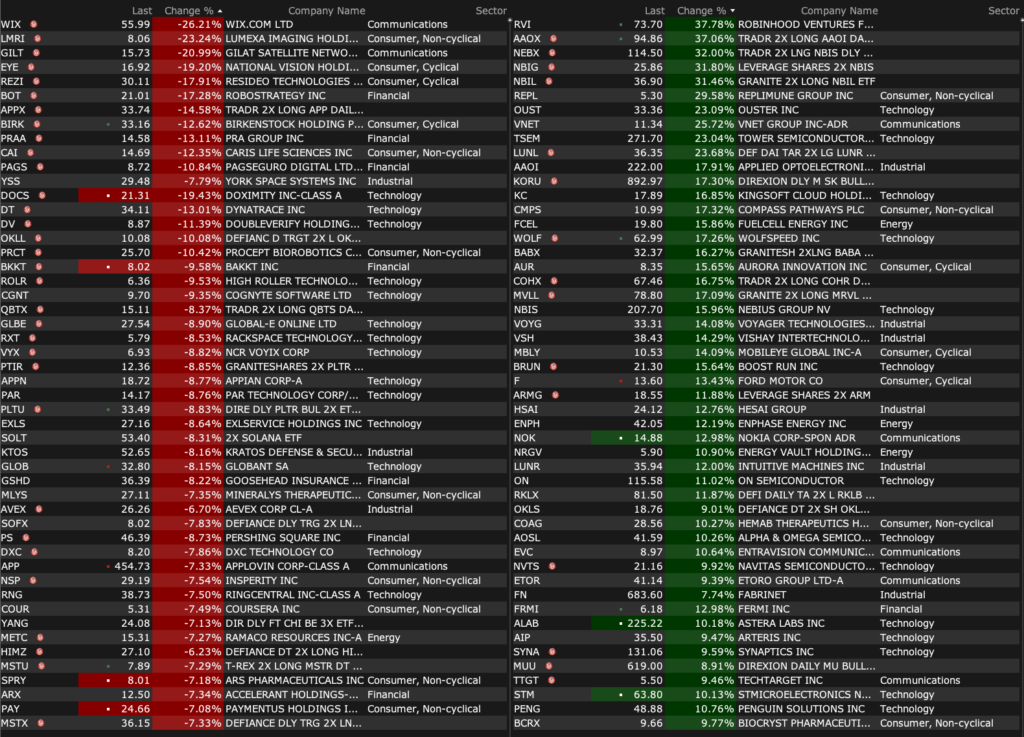

After-Hours % Advancers

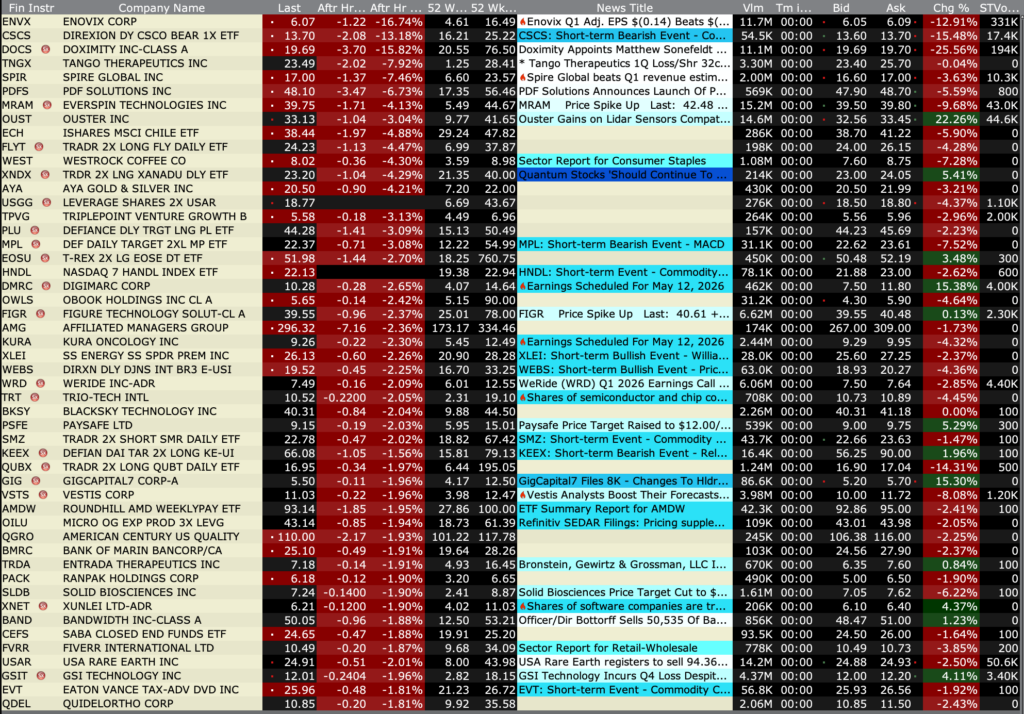

After-Hours % Decliners

Position: None

BY Doug Kass · May 13, 2026, 4:45 PM EDT

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 13, 2026, 4:45 PM EDT

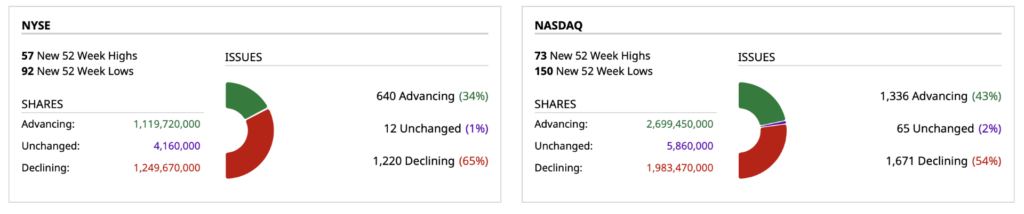

Closing Volume

– NYSE volume 9% above its one-month average

– NASDAQ volume 7% above its one-month average

– VIX index: down 0.61% to 17.88

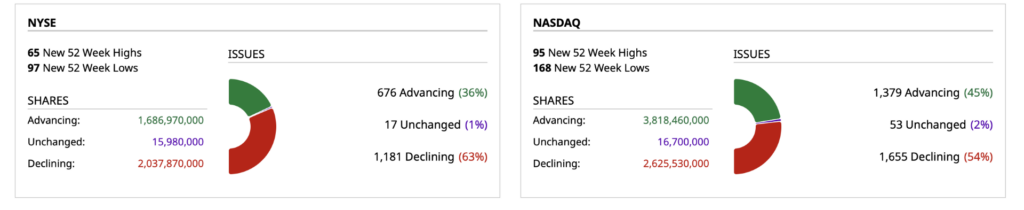

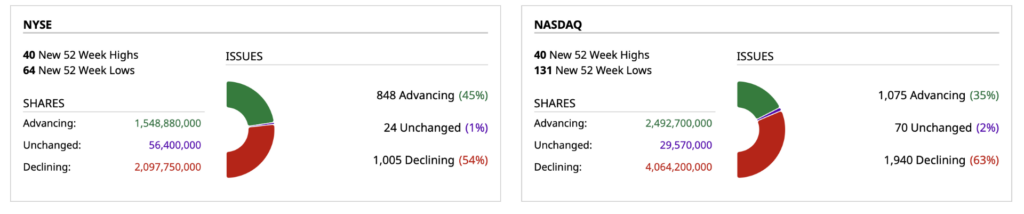

Breadth

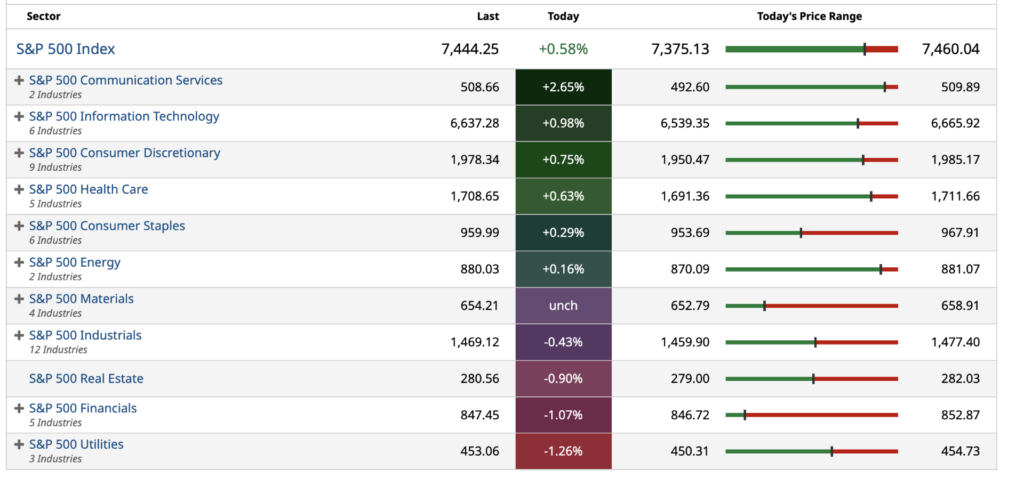

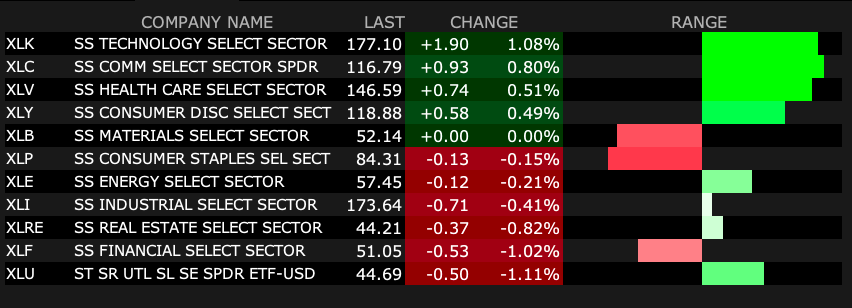

S&P 500 Sectors

% Movers

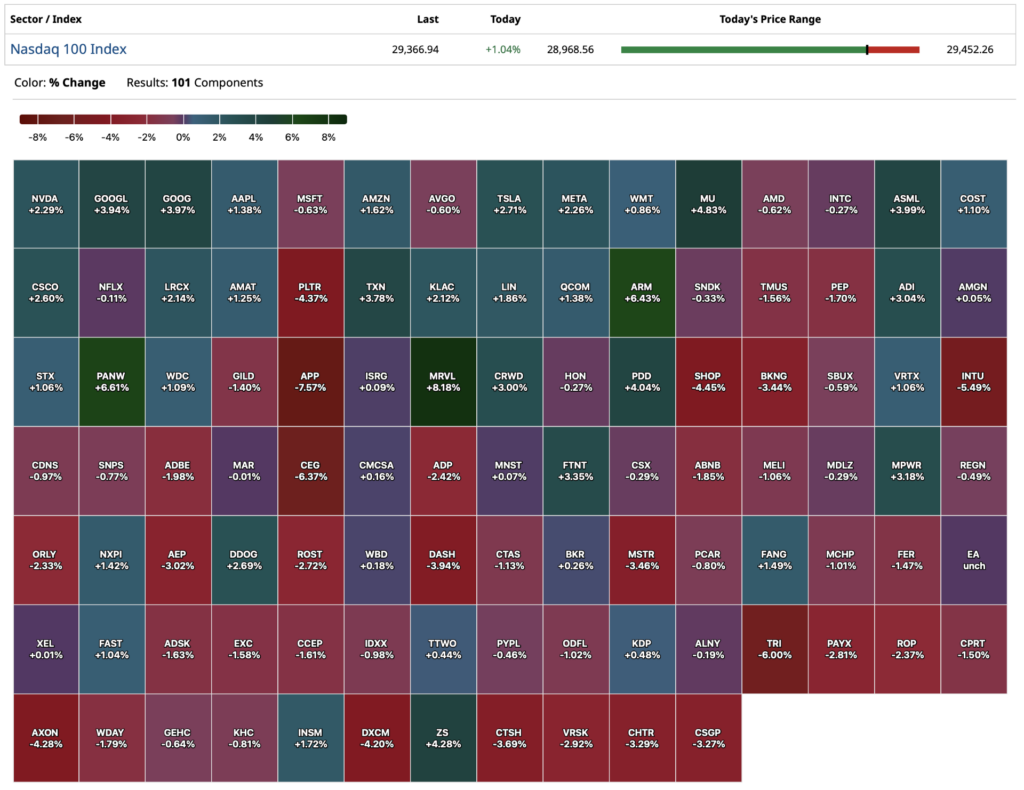

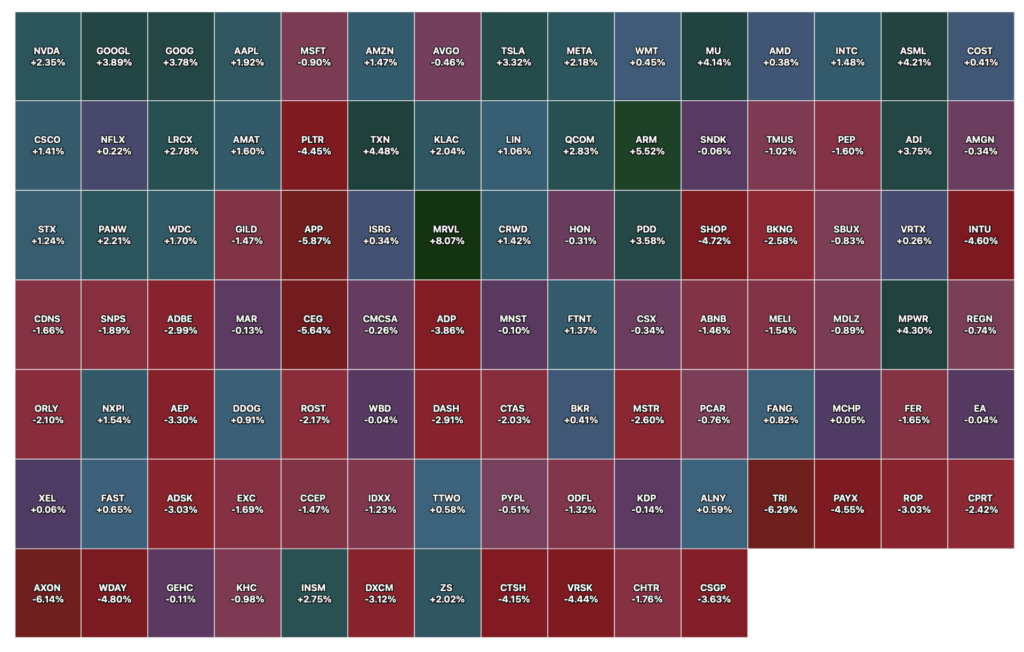

Nasdaq 100 Heat Map

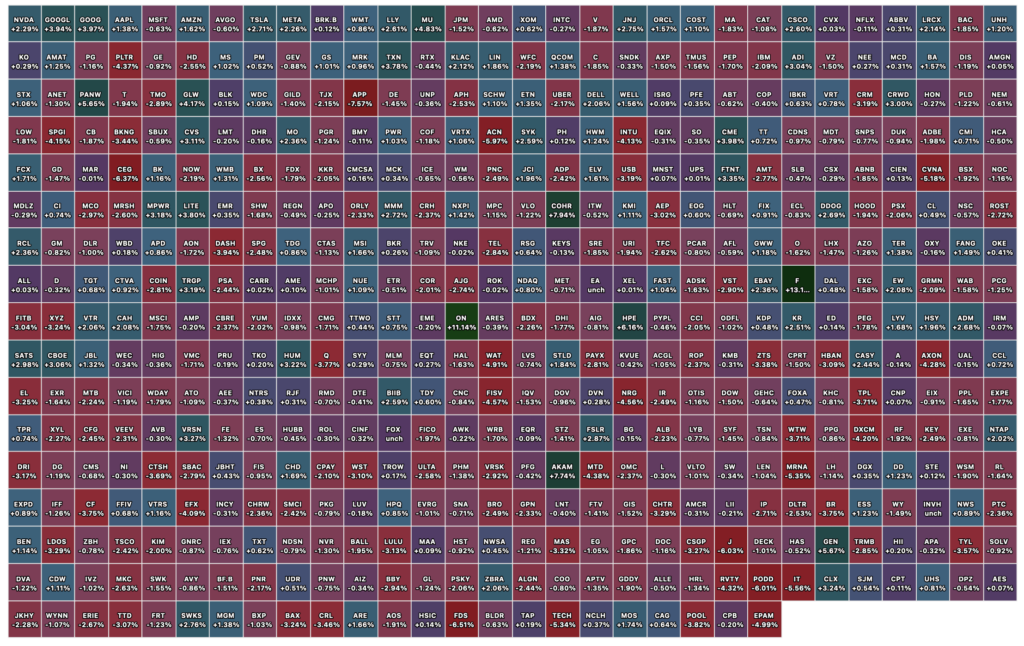

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · May 13, 2026, 4:27 PM EDT

I have re-shorted Tesla TSLA at $444.95.

Position: Short TSLA (VS)

BY Doug Kass · May 13, 2026, 4:05 PM EDT

Out here in the fields

I fight for my meals

I get my back into my living

I don’t need to fight

To prove I’m right

No I don’t need to be forgiven

No no no no no no no Don’t cry

Don’t raise your eye

It’s only teenage wasteland

– The Who, Baba O’Riley Teenage Wasteland by The Who

I added to PepsiCo PEP at $149.47 and PG at $142.22 longs this afternoon.

Position: Long PEP (S), PG (S)

BY Doug Kass · May 13, 2026, 3:58 PM EDT

BY Doug Kass · May 13, 2026, 3:55 PM EDT

BY Doug Kass · May 13, 2026, 3:44 PM EDT

Position: None

BY Doug Kass · May 13, 2026, 3:10 PM EDT

* Mama mia, mama mia!

* Carry on, carry on as if nothing really matters…

Is this the real life? Is this just fantasy?

Caught in a landslide, no escape from reality

Open your eyes, look up to the skies and see

I’m just a poor boy, I need no sympathy

Because I’m easy come, easy go

Little high, little low

Any way the wind blows doesn’t really matter to me, to me

– Queen, Bohemian Rhapsody

Inflation rising and interest rates higher, breadth with a foul odor, equal-weighted S&P underperforming the S&P Index, etc etc:

Sometimes I wish I never shorted at all…

Note: I will be traveling tomorrow! You will be in the capable hands of Chris Versace.

See you back on Friday morning!!!

BY Doug Kass · May 13, 2026, 3:00 PM EDT

Position: None

BY Doug Kass · May 13, 2026, 2:50 PM EDT

I moved up to small sized short the indices:

* SPY $743.72

* QQQ $716.37

Position: Short SPY (S), QQQ (S)

BY Doug Kass · May 13, 2026, 2:40 PM EDT

At 1:54 PM:

Breadth

S&P 500 Sector ETFs

Nasdaq 100 Heat Map

BY Doug Kass · May 13, 2026, 2:15 PM EDT

S&P Index (SPY) +0.61%.

Equal Weighted S&P Index (RSP) -0.45%.

While the market’s breadth is stinking up the joint:

Position: Short SPY (VS)

BY Doug Kass · May 13, 2026, 2:00 PM EDT

I call more B.S.:

Position: None

BY Doug Kass · May 13, 2026, 1:52 PM EDT

This is Part 5 of a multi-part discussion of the markets (Read Part 1 here, Part 2 here, Part 3 here and Part 4 here) …

Now, let’s wrap it up…

“It is always well to accept your own shortcomings with candor but to regard those of your friends with polite incredulity.”

– Russell Lynes

As noted in a previous post It’s a Mad, Mad, Mad, Mad Investment World.

Today’s commentary shares my views and tries to attach empirical evidence and observations that support a skeptical market outlook.

I continue to be reminded of Warren Buffett’s quote:

“What the wise do in the beginning, fools do in the end.”

With the same intended message, Barton Biggs was more colorful when he said:

“A bull market is like sex. It feels best just before it ends.”

Citigroup’s CEO Charles Prince — in July 2007, only months before The Great Financial Crisis (and historic market decline) — had a different view (as reported in an interview he had with The Financial Times):

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

That said, with the S&P 500 making an all-time record in May — and despite my protestations — it is abundantly clear that, for now, neither the markets nor most market participants (human and machine) share my outlier, non-consensus and ursine outlook.

Market participants are still at the bacchanal — while I remain celibate.

Position: None

BY Doug Kass · May 13, 2026, 12:45 PM EDT

This is Part 3 of a multi-part discussion of the markets (Read Part 1 here, Part 2 here and Part 3 here) …

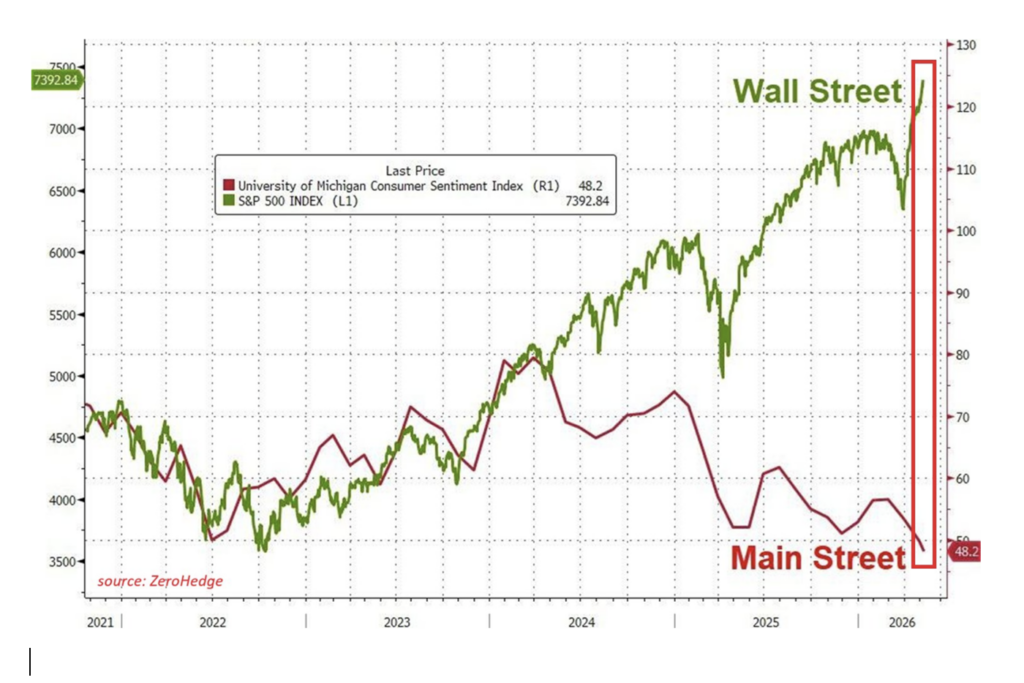

We are mindful of the gap between Wall Street and Main Street:

As an illustration of the Main Street/Wall Street comparison, here is the stock price chart of Home Depot (HD):

With inflation high and the economy weakening, should equities decline, the weakness in the K-shaped economy could begin to impact the middle and upper-middle classes —adversely impacting aggregate economic growth.

As mentioned, the stock market is now acting less like a church (which respects valuations) and more like a casino.

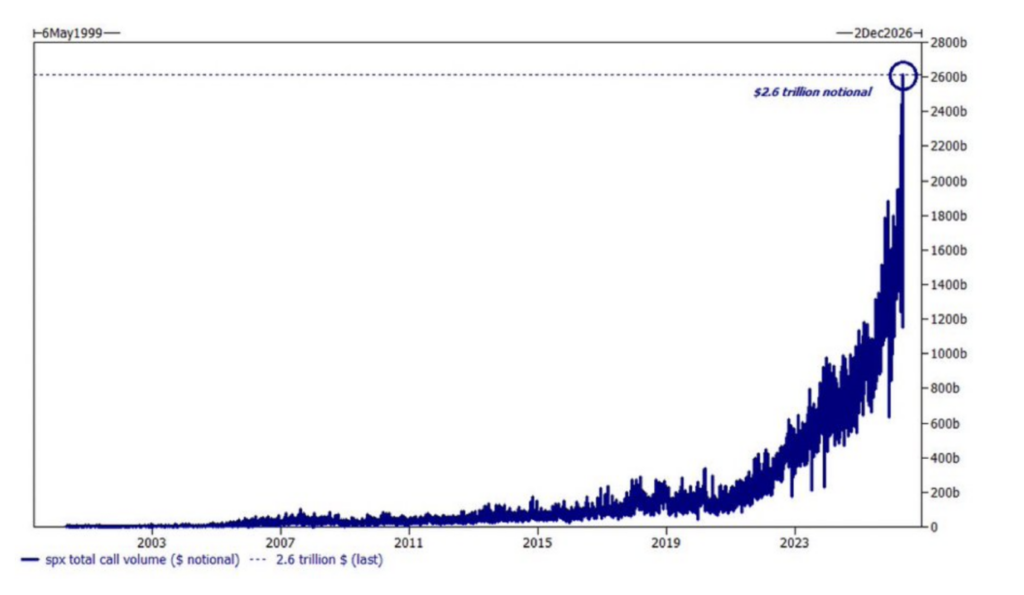

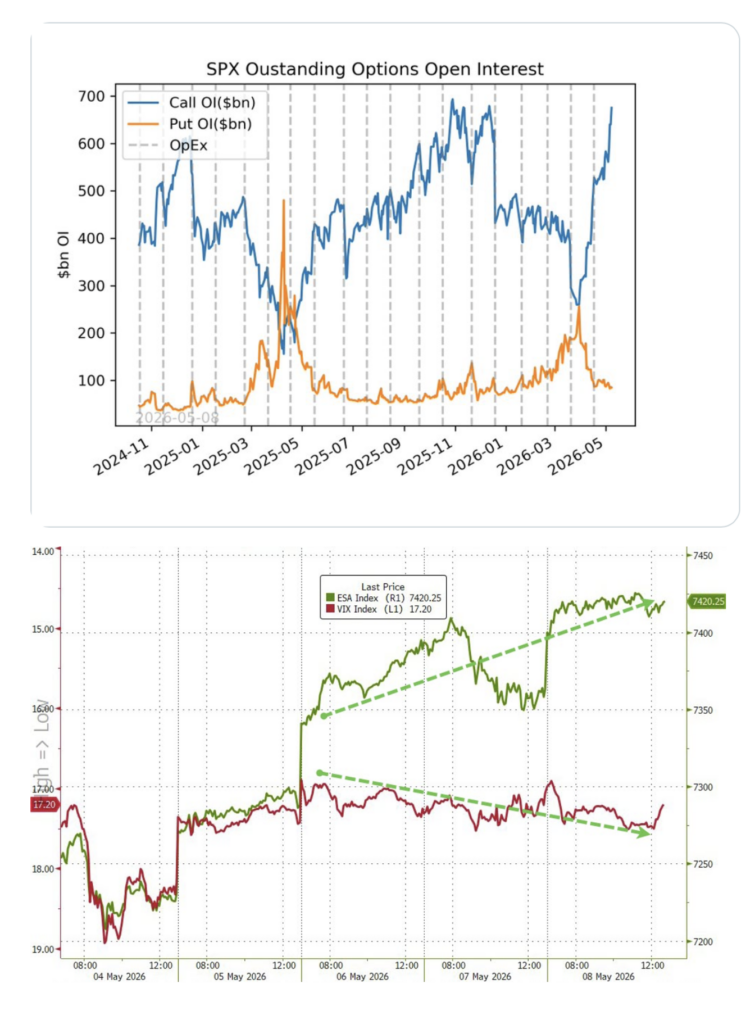

Last Thursday the market did something it has literally never done before. The S&P traded $2.6 trillion in call options — that is the highest single day call volume in market history:

When traders buy massive amounts of calls the market makers selling those calls are forced to hedge by buying the underlying stocks. That buying pushes prices higher. Higher prices force more hedging. More hedging pushes prices higher again. This is called a gamma squeeze. It works well on the way up. It’s brutal on the way down.

The entire market is in an unprecedented gamma squeeze. Open interest at all-time high, outstanding delta above $4.2 trillion — an all-time high:

In the context of this speculation, I plan to continue to have some net short exposure. However, given the respect I have for the historical conditions of late speculative cycle markets (they go further than anyone expects!) and the forceful impact of passive strategies and products (driven by algorithms), I will, consistent with my risk appetite, keep my net short exposure low.

Nonetheless, there will come a time that I will expand my short book.

Stay tuned for Part 5…

BY Doug Kass · May 13, 2026, 12:00 PM EDT

This is Part 3 of a multi-part discussion of the markets (Read Part 1 here and Part 2 here)…

In my view, the markets have ignored the same conditions that set off the January-February selloff. None of the non-war issues that drove stocks lower have been resolved:

* Oil prices are off their highs but are likely to remain elevated because of the magnitude of the supply shock and continued uncertainties related to the Iran conflict.

* Inflation is now rising on a sequential monthly basis — and is higher than before the conflict in Iran.

* Interest rates will be higher for longer.

* The 2026 annual deficit will approach $2 trillion, and neither political party show any signs of being fiscally responsible.

* The U.S. debt will hit $40 trillion this year — the cost of servicing the debt is over $1 trillion/year.

* With a burgeoning deficit, stiff debt load and persistent inflation, the Fed’s hands are tied.

* While private equity’s problems are not systemic, the leverage they brought us remains in place. KKR Private-Credit Fund Takes $560 Million Loss – WSJ

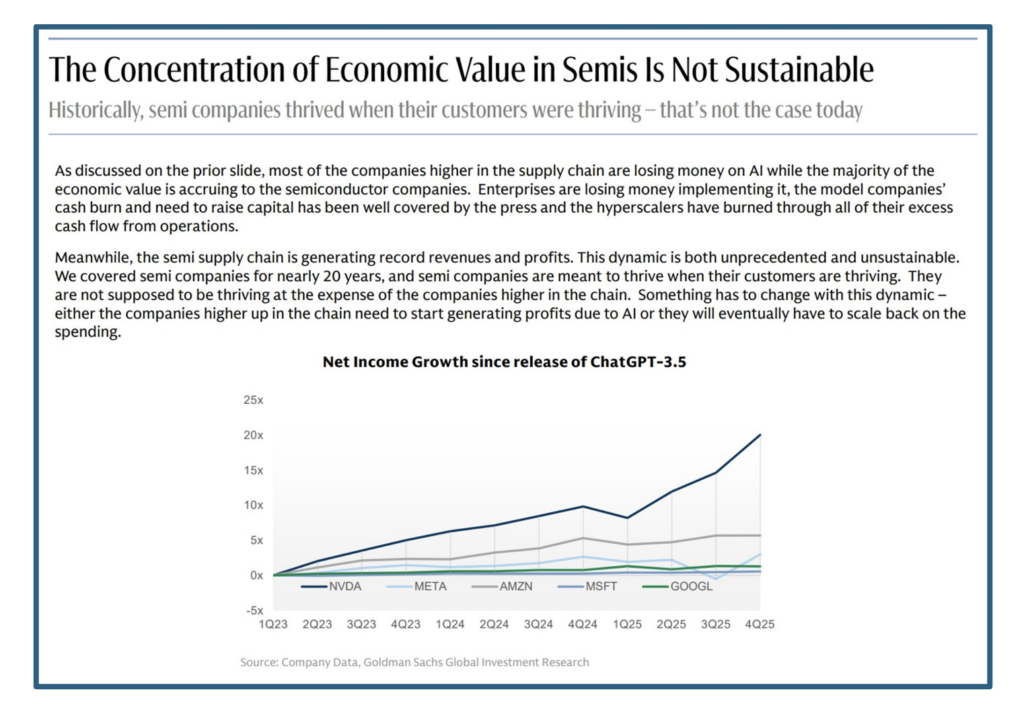

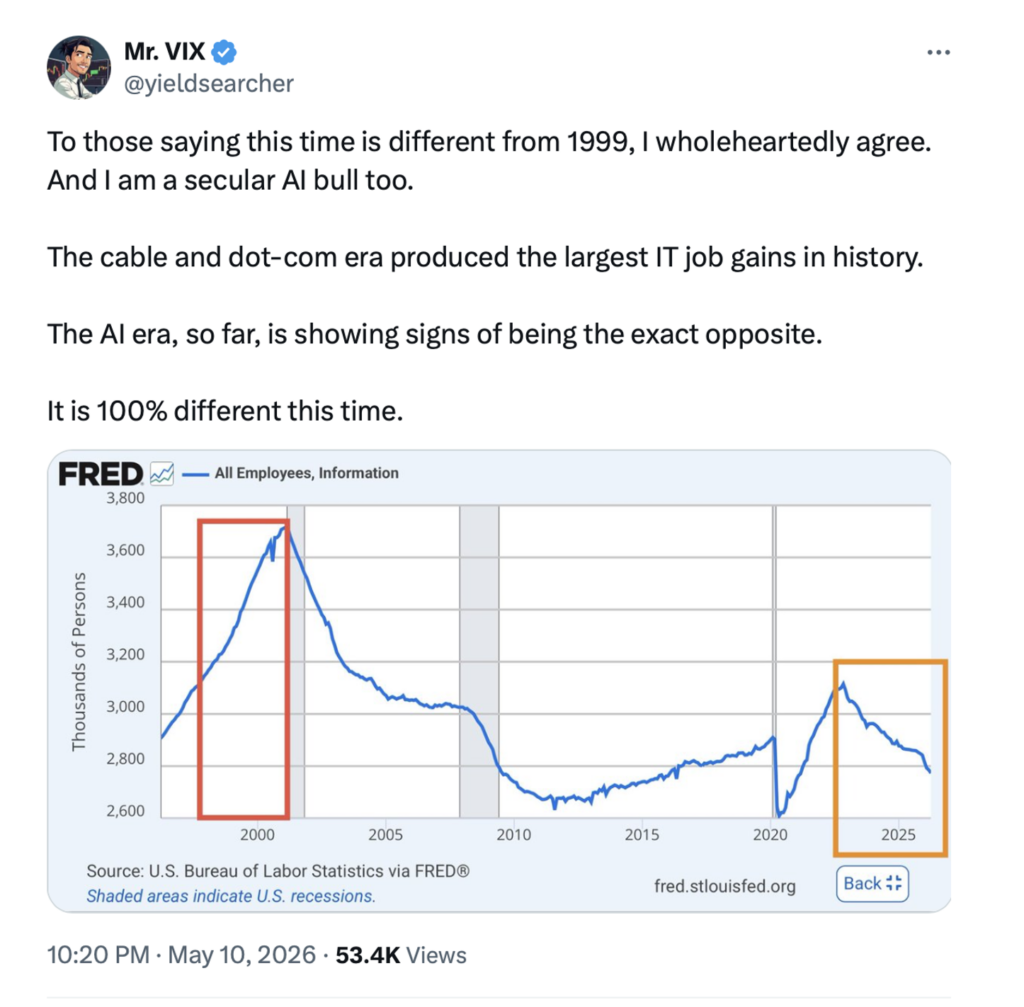

* The enormous amount of money spent on AI will probably never see an adequate return on investment. As noted by Stan Druckenmiller (again!), AI’s societal and transformative impact could rival the internet’s life-changing influence — and so may the stock market consequences (rhyme) be similar:

“If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to fruition. That’s not going to happen with AI. But it could rhyme – AI could rhyme with the Internet as we go through all this capital spending we need to do. The big payoff might be four to five years from now. So AI might be a little overhyped now but under-hyped long term.”

* Valuations are a terrible clock but a good weather forecast. That valuations are stretched is an understatement. See CAPE Shiller in Part 2. The Buffett ratio (the total market capitalization divided by GDP) hit an all-time high this week). Most other traditional metrics indicate that equity valuations are in the 97 percentile.

* Many bulls highlight the improving strength in projected 2026 S&P EPS. They argue that this year’s robust growth in profits (at about +17%) justify current valuations. However, if one takes out Nvidia (NVDA) and Micron (MU), 2026 S&P EPS growth falls to under +10%:

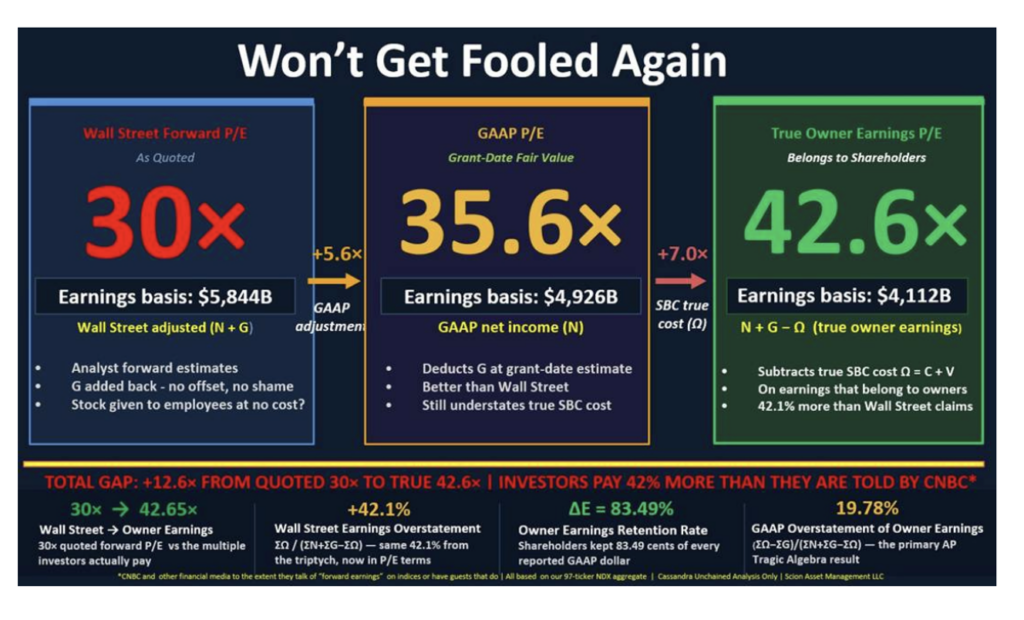

Almost no tech stock, not even the bombed-out software stocks, are inexpensive when held to strict accounting standards, more strict and more forensic in nature than GAAP.

Michael Burry hits the target in his recent commentary:

The NASDAQ 100’s true PE is closer to 43x than the 30x Wall Street tells us.

In addition to the effects of stock-based compensation, previously discussed problems with depreciation policies, construction-in-progress, M&A costs, capital leases, and other necessary adjustments to GAAP net income to find true owners’ earnings.

Including all these adjustments, Wall Street may be overstating by more than 50% the earnings at our fastest growing, most highly valued companies.

In addition, there is the likelihood of future write-downs, in large measure stemming from the numerous circular financings. (Cisco in 2021 and 2002 wrote down years of its best earnings when it had to write off the same types of contracts with its suppliers).

Most investors are now convinced we are in a continued bull market led by AI-related equities.

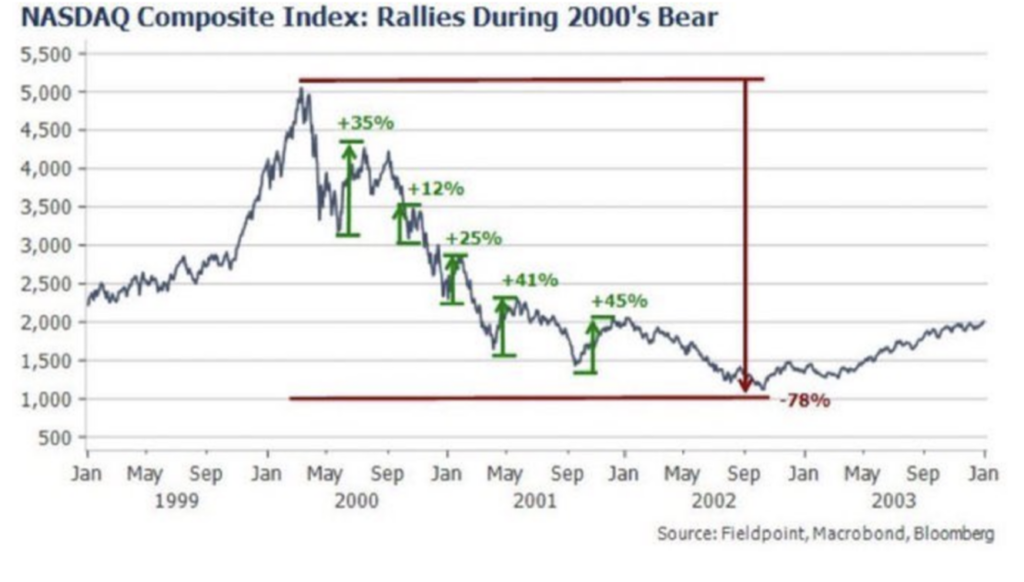

However, the anatomy of a bear market (we will not know until after the fact!) is that there are violent rallies.

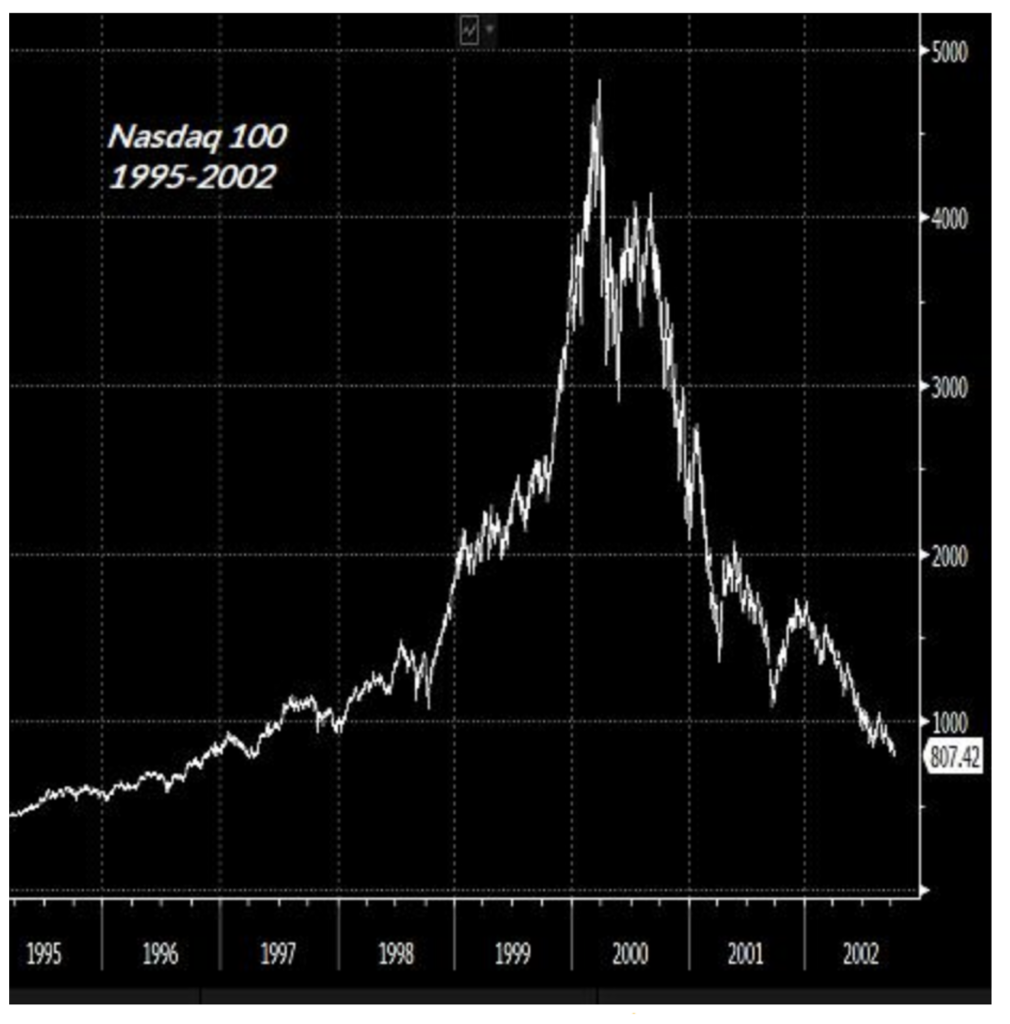

As noted earlier, a classic and extreme example was when the Nasdaq declined by -81% (2000-2002) following the dot-com boom in which the revolutionary impact of the internet was heralded and applauded in the indexes.

Along the way to the nearly 80% drop, there were five robust rallies of between +12% and +45%. The average gain in the rallies was +33%.

Every rally felt like a bottom, but every rally was a trap:

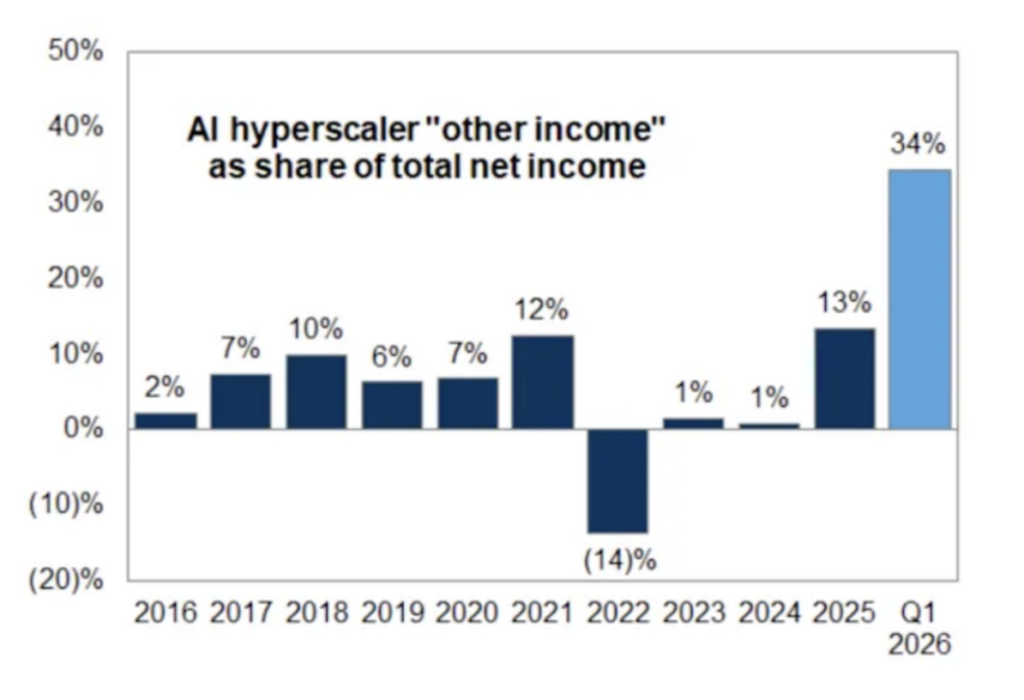

I see multiple traps ahead, including financing circularity and quality of earnings (the other income line has been aided by sizeable increases in private investment valuation marks – below), among other issues (like the large erosion in hyperscaler free cash flow):

Stay tuned for Part 4…

BY Doug Kass · May 13, 2026, 11:15 AM EDT

This is Part 2 of of a multi-part discussion of the market (read Part 1 here)…

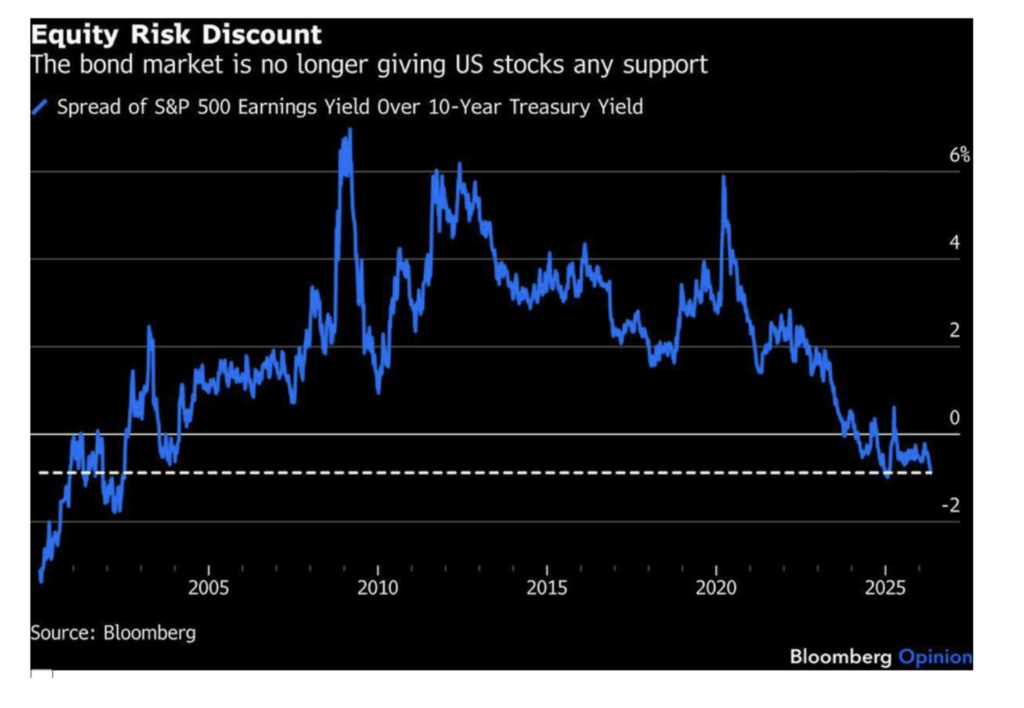

The chart below, of the equity risk premium, is probably the most important reason for my ursine market view.

The equity risk premium is the difference between the S&P earnings yield (the inverse of the P/E ratio) and the risk-free rate of return.

Surprisingly, the equity risk premium has morphed into an equity risk discount — standing at the deepest discount since 2003. As of Tuesday, the S&P Index’s earnings yield was 90 basis points lower than the risk-free rate of return (using the 10-year yield) — meaning that market participants believe there is more risk in holding bonds than in holding equities!

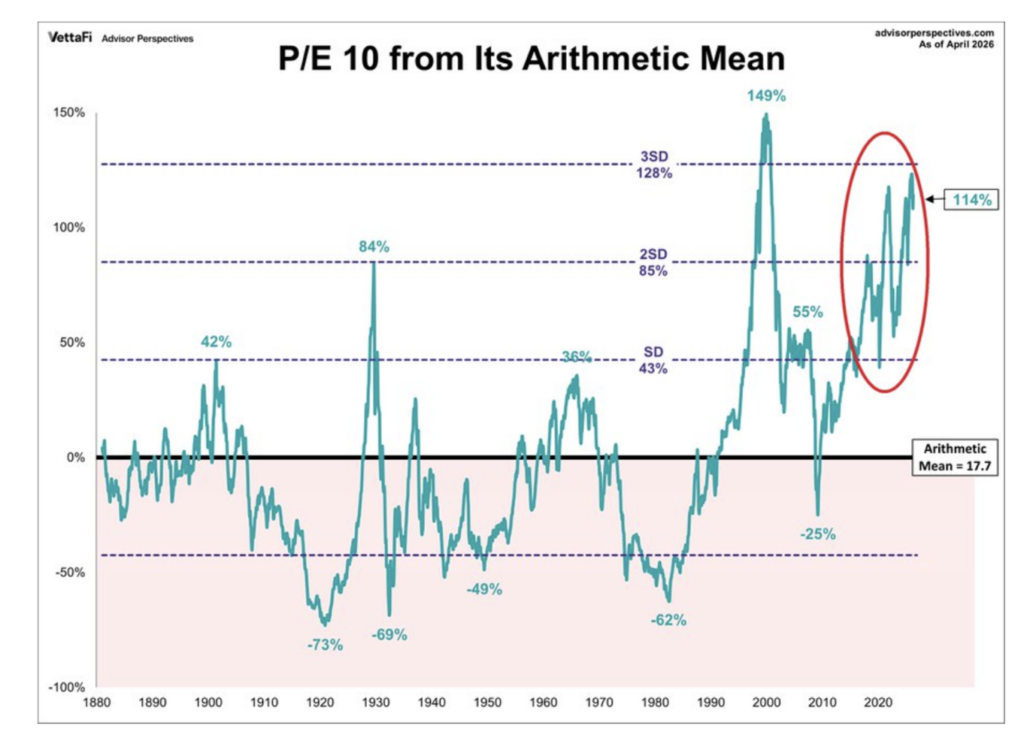

Here is another chart that has concerned us — the P/E 10 ratio. This ratio measures stock prices against the average of 10 years of inflation-adjusted earnings to smooth out short-term business cycle distortions. Thursday’s reading of 37.9 is +114% above its long-run arithmetic mean, placing into a zone only visited once before in the last 150 years — during the dot-com bubble (when it stood at 44.2). Today’s P/E 10 reading is above the level hit in 1929:

The P/E 10 chart above is a derivative of the Shiller CAPE Ratio shown below (which I have presented to you often over the last 24 months). Shiller CAPE now stands at 42.05, a whisker away from the dot-com bubble high of 44.0.

It would take a 60% fall in stocks to reach the historical mean of 17:

Over the last century, every time the equity risk premium narrows considerably (as it currently has (in the extreme) transitioned into an equity risk discount) and the P/E 10 ratio moves as far as it is today from its arithmetic mean — a large decline and mean reversion in investment returns occur.

Stay tuned for Part 3…

BY Doug Kass · May 13, 2026, 10:30 AM EDT

I have covered my index shorts from early this morning for a quick profit:

* SPY $735.68

* QQQ $705.01

Dougie Kass

Back shorting in the premarket 739AM

SPY $739.75 QQQ $711.85

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · May 13, 2026, 8:38 AM EDT

Position: None

BY Doug Kass · May 13, 2026, 10:05 AM EDT

This is Part 1 of a multi-part discussion of the markets…

* Investors are ignoring a number of clearly defined and intensifying fundamental and valuation headwinds

* Investor sentiment and expectations are inflated — market risks are being underappreciated

* Equities remain overvalued — perhaps materially so

* The stock market is a church with a casino attached to it — the casino has grown much more active in recent months

* It feels like deja vu all over again

The magnitude and strength of the recovery in the major indexes during the past month have been anathema to me (and to others who have a taste for value and don’t have a momentum-based orientation). The size and the rapidity of the market’s rally (especially since March) have likely been momentum-driven (due in part to market structure changes over the last decade in which passive products and strategies have dominated the investment landscape).

This backdrop of momentum based machine-driven dominance — in which buyers buy strength (and, ultimately, sellers sell weakness) — has, in turn, led to a great deal of fear of missing out (FOMO). These factors and others (including a strong belief in an AI productivity miracle) have contributed to a record pace of recovery, producing another “V”- type rally from the March 2026 lows.

I did not see the extent of this rally coming and remain skeptical of it continuing. Indeed, despite the growing optimism of the consensus, I now see stunning similarities between today’s equity market and previous market tops. Most noticeable is the comparison to the dot-com top in 2000 (a similar period of narrowing/concentrated market leadership and the belief in technology’s new big thing (the internet) to deliver robust revenue/profit expectations (which failed to pan out)):

At times like this I am reminded that incredulity robs us of many pleasures and gives us very little in return! Or as Samuel Johnson wrote:

“To revenge reasonable incredulity by refusing evidence, is a degree of insolence with which the world is not yet acquainted; and stubborn audacity is the last refuge of guilt.”

In today’s opening missive I have several points to make:

* Though it may appear — to Samuel Johnson (in his above quote) and others — that I am in stubborn denial of the facts (and the market’s amazing advance), I feel I have many justifiable reasons to maintain our doubt and skepticism. I have discussed my reasoning and evidence in my past Diary commentaries and I will expand on those reasons again today.

* Though bullish market participants seem to disagree, it is an unusual and potentially threatening period for the global economy, our markets, our society and for innovation (in which AI is distorting stock prices and profits). I have had a lot to say about this in the past and I will continue in this missive and in the future.

* Main Street and Wall Street have diverged dramatically.

* I will further explain why — despite growing ever more bearish — I have maintained a relatively small net exposure on the short side (and have no current plans to meaningfully expand my short portfolio further).

With the fear of missing out reverberating, there is growing pressure to speculate today. Nonetheless, I will not abandon my disciplines nor forget the lessons of history.

Before expanding on our market view, I wanted to recite a relevant quote from Georg Hegel and cite two examples of differing behavior towards the end of the dot-com boom in 2000:

”What we have learned from history is that too many have not learned from history.”

Below are examples of Berkshire Hathaway’s (BRK.A, BRK.B) avoidance of the dot-com bust and Stanley Druckenmiller’s emotional purchase of tech stocks at the height of the dot-com boom.

1. The stock market, to paraphrase Warren Buffett, is a church with a casino attached to it. In the last several months the casino has become very active!

At the top of the dot-com bubble (and before a -81% drawdown in the Nasdaq), a Berkshire Hathaway shareholder asked Warren Buffett and Charlie Munger “to just speculate” in technology:

2. An example of the consequences of succumbing to speculation (and emotion) occurred around the same time when Stanley Druckenmiller (arguably the greatest modern-day investor) acquiesced to the markets and, within hours of the dot-com top purchased billions of dollars of technology stocks.

Here Stan recounts his investment boner in March 2000, when he purchased $6 billion in tech stocks at the peak of the dot-com bubble, which resulted in losses of about $3 billion in only six weeks:

Another Technology Victim; Top Soros Fund Manager Says He ‘Overplayed’ Hand – The New York Times

Druckenmiller on his $3B loss.

Stay tuned for Part 2…

BY Doug Kass · May 13, 2026, 9:45 AM EDT

From Peter Boockvar:

Global sovereign bond yields are a definite focus but I do want to add another influence in addition to inflation worries, along with concerns with excessive country debts and deficits. That being, sovereign bonds in markets that foreigners own a big piece have been a source of funds as countries bring some money home to manage the energy price/volume shock some are experiencing.

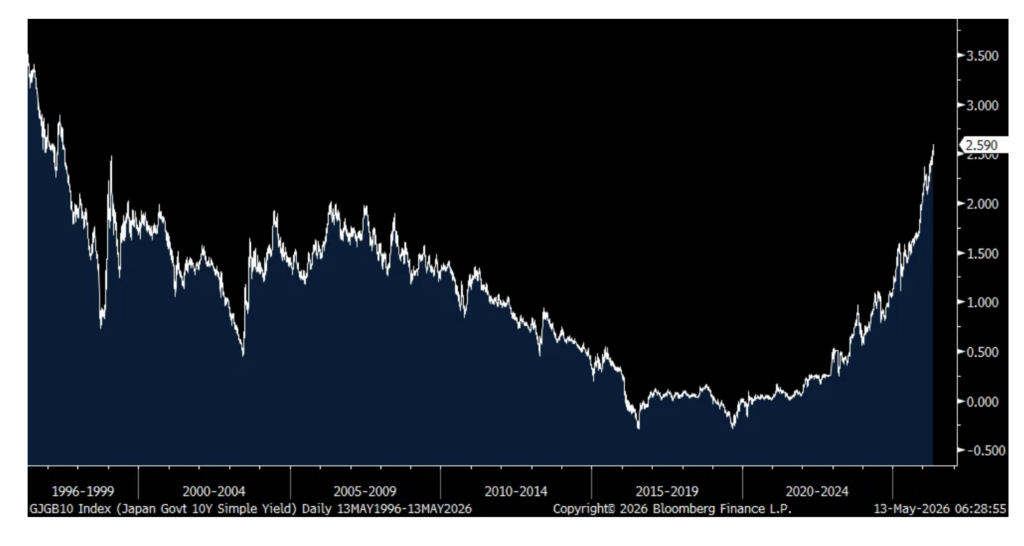

Foreigners own about 30% of the US Treasury market. According to Gemini, foreigners own 77% of the German bund market and about 50% outside the Euro area. Foreigners own about 50% of the French oat’s market. Of the UK gilt market, overseas investors held about 30%. It’s really only the Japanese JGB market that foreigners hold little but bond yields are rising anyway as the long end of their yield curve has taken over monetary policy from the BoJ. The 10 yr JGB by the way closed overnight at a fresh 29 year high, up another 3 bps to 2.59%. And with the Japanese the largest owner of US Treasuries, there is a JGB yield level where that money is going to come back home to the JGB market.

10 yr JGB Yield

We know rents/housing is the biggest component of CPI and I’ve been arguing that any moderation in new rent growth we’re currently experiencing, mostly in overbuilt sunbelt states, is only temporary as there is a sharp reduction in the pace of new supply that will start to show up in higher rents by the end of 2026 and into 2027.

I was at the Sohn Conference yesterday in NYC and heard one presenter pitch Camden Property Trust, a stock we own. It was Leslie Sturgeon from Maynard Capital Management and a key part of her bull case was her 2027 new lease growth estimate of 7% vs the Street which is currently at 1%. Her renewal lease growth rate forecast of 4% is in line with the Street and the combination brings a blended rate of growth of 5% vs the Street at 2%. If she’s right, and I believe she will be, the inflation story will continue on next year.

After hearing from Maersk last week, Hapag Lloyd reported today and said this of note on their earnings call:

With respect to the Middle East, “I think the thing which is a little bit special about that is while the conflict itself is geographically quite isolated and as such does not impact global flows all that much, the effect it has on costs, of course, have a global effect because with the surge of energy prices, we have seen significantly higher costs hitting us. I think if we look at what we have today, then we definitely look at $50, $60 million extra costs every week.”

“Of course, we try to pass that on, similar to when you go to the petrol station and you also have to a higher fuel price, but clearly that puts pressure on our business. As far as the militia is concerned, we still have a number of ships stuck there and we cannot go in and out of the Strait at this moment in time.”

Under Armour got roughed up yesterday, a stock we still own but still like believing in the turnaround that’s happening under the surface. A few things of note from them:

“as we look ahead to fiscal ‘27, we do expect to stabilize with revenue down slightly. That outlook reflects both continued consumer uncertainty and the deliberate choices we’re making to reshape the business. We are prioritizing revenue quality over volume, strengthening the foundation and positioning the company to return to growth with stronger profitability and a more consistent brand expression.”

North America sales were down but “In EMEA, the business remains solid and continues to serve as a stable anchor for the brand.” Sales are rising too in APAC with a particular focus on China.

They got hit hard from tariffs but are expecting some refunds. “This is a brand that has been navigating tariffs, softer consumer demand and supply chain disruption” in the Middle East.

Positions: None.

BY Doug Kass · May 13, 2026, 9:30 AM EDT

Upside:

-EOSE +22% (earnings, guidance; forms Frontier Power USA with Cerberus and files mixed shelf of indeterminate amount)

-VNET +17% (signs share purchase agreement with PJ Millennium)

-TSEM +15% (earnings, guidance)

-WOLF +15% (hearing Citrini Research makes constructive comments)

-NBIS +14% (earnings, guidance; announces new second owned gigawatt-scale site in the US)

-ELAB +9.7% (acquires A&B Aerospace for $4.5M cash and debt-free basis)

-MU +5.4% (momentum)

-CMPS +5.1% (earnings, color)

-BOBS +4.1% (CEO buys shares)

-SATS +4.1% (FCC approves Echostar $40B sale of Wireless spectrum to SpaceX and AT&T)

-CRWV +3.8% (price targets raised at Citi; higher in sympathy with Nebius)

-INTC +3.0% (momentum)

-SNDK +2.7% (S&P raises rating one notch to BB+ from BB; Outlook Positive)

-UMAC +2.7% (ROTH Initiates UMAC with Buy, price target: $25)

-ST +2.6% (Truist Raised ST to Buy from Hold, price target: $58)

-NVDA +2.0% (momentum)

Downside:

-WIX -22% (earnings, guidance)

-RCAT -14% (prices upsized ~23.9M shares at $9.40/share for gross proceeds worth ~$225.0M)

-DT -13% (earnings, guidance)

-KRMN -9.6% (earnings, guidance)

-WRD -7.3% (earnings, color)

-BIRK -5.7% (earnings, guidance)

-GTM -2.2% (Mizuho Securities Cuts GTM to Underperform from Neutral, price target: $3)

-BABA -2.1% (earnings, color)

Position: None

BY Doug Kass · May 13, 2026, 9:20 AM EDT

Position: None

BY Doug Kass · May 13, 2026, 9:10 AM EDT

Repeating for emphasis: The investment world and the business media (that provides Cathie Wood with a frequent platform) are both offsides.

Position: None

BY Doug Kass · May 13, 2026, 9:04 AM EDT

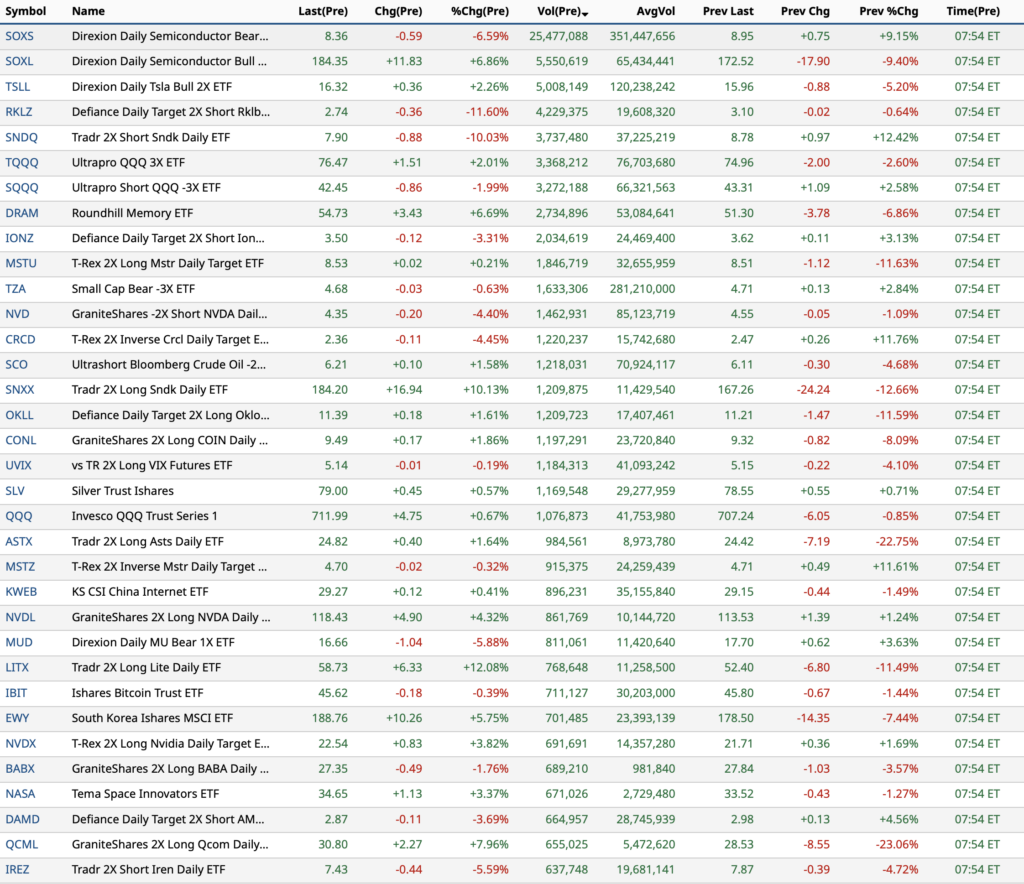

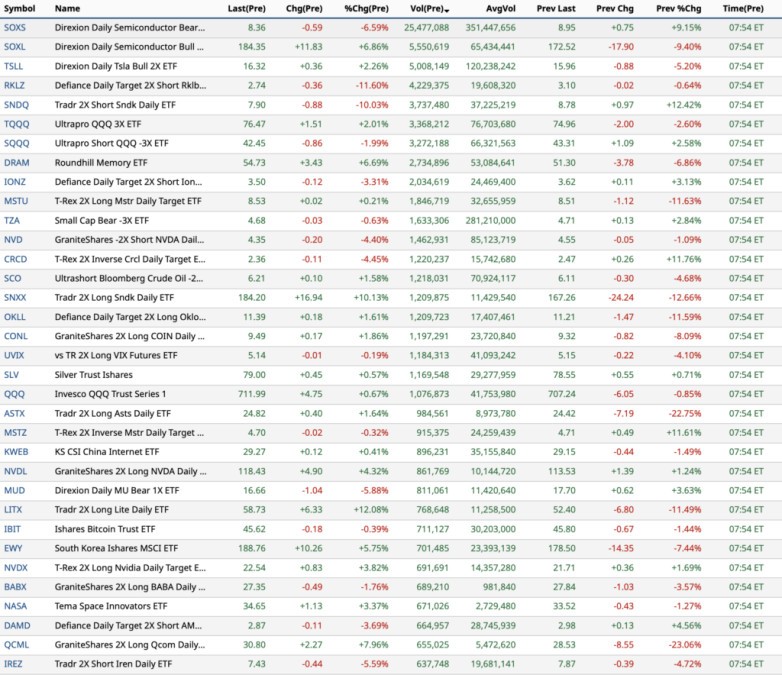

Most Active Premarket ETFs as of 7:54 AM:

Position: None

BY Doug Kass · May 13, 2026, 8:45 AM EDT

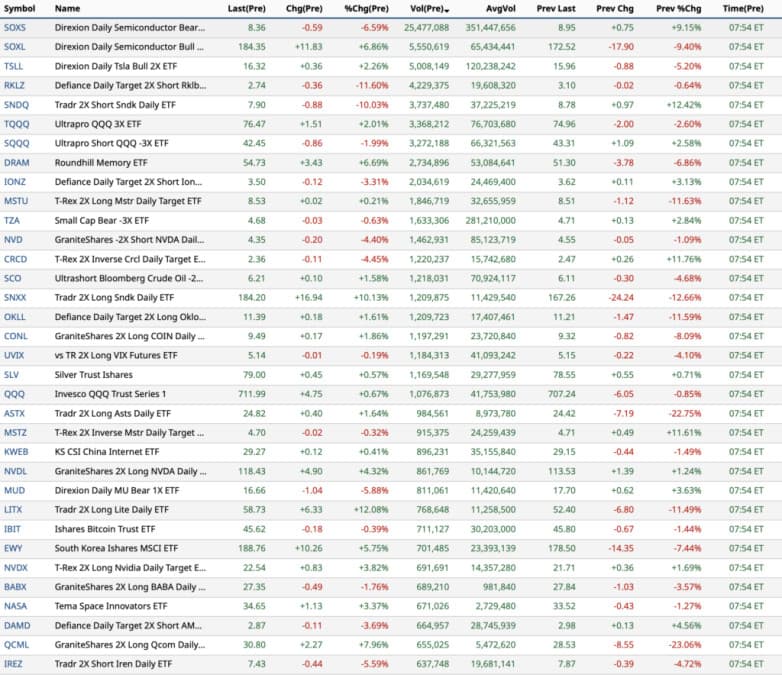

Most Active Premarket ETFs as of 7:54 AM:

Position: None

BY Doug Kass · May 13, 2026, 8:45 AM EDT

Dougie Kass

Back shorting in the premarket 739AM

SPY $739.75 QQQ $711.85

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · May 13, 2026, 8:38 AM EDT

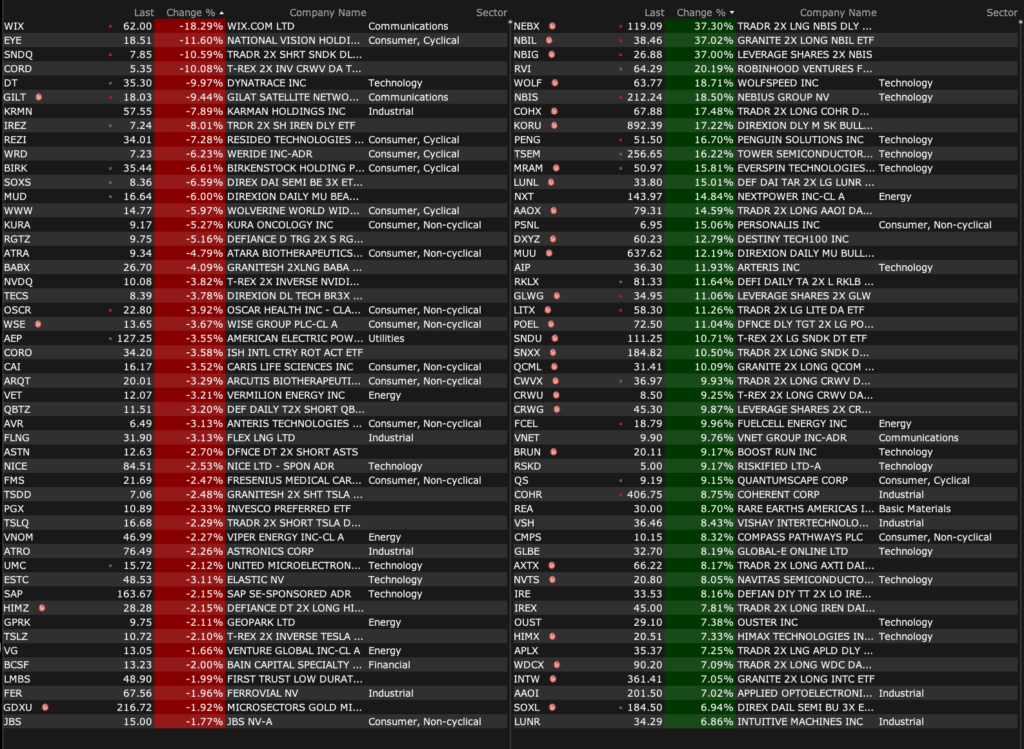

% Movers at 8:19 AM:

Position: None

BY Doug Kass · May 13, 2026, 8:30 AM EDT

TREASURY AUCTIONS:

11:30AM: Treasury hosts a $69B 17-Week Bill Auction

1:00PM: Treasury hosts a $25B 30-Year Bond Auction

2:00PM: Treasury buyback (liq support)

FED SPEAKERS:

11:30AM: Fed Bank of Boston President Collins (Non-Voter) delivers remarks and participates in fireside chat before the Boston Economic Club, Boston, MA (No media Q&A. Livestream at bostonfed.org)

1:15PM: Fed Bank of Minneapolis President Kashkari (Voter) participates in moderated discussion hosted by the St. Paul Area Chamber, St. Paul, MN. (Audience Q&A expected. No media Q&A. No prepared/embargoed text. Livestream at minneapolisfed.org/live);

7:00PM: Fed Bank of Dallas President Logan (Voter) participates in moderated conversation on the energy sector before a “Global Perspectives” event hosted by the Federal Reserve Bank of Dallas and the Dallas Citizens Council, Dallas, TX (Livestream available)

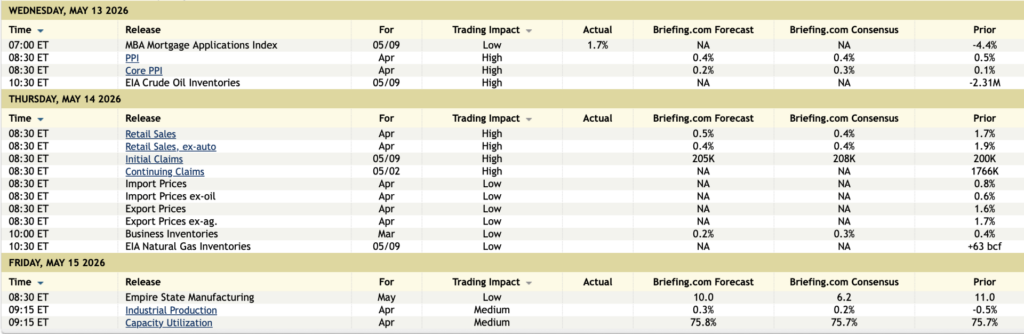

ECONOMIC CALENDAR

Position: None

BY Doug Kass · May 13, 2026, 8:23 AM EDT

* In which the irrational is being rationalized (or ignored) by the bullish cabal

Amid deteriorating market breadth,

rising interest rates,

and inflation, improvisational foreign policy, the proliferation of 0DTE options and two-to five-time inverse ETFs, Cathie Wood’s proud admission of large investment losses (which is not viewed as an “asset” to her strategy),

and a +$5 overnight rise in Nvidia’s (NVDA) share price (because Jensen Huang is accompanying President Trump to China)

— equity futures are rebounding mightily this morning (after yesterday’s short-lived swoon).

Like Stanley Kramer’s 1963 movie It’s a Mad, Mad, Mad, Mad World, a legendary, star-studded comedic epic about a group of strangers racing across California to find a hidden treasure. It is famous for its massive slapstick scenes, numerous cameos, and an ensemble cast including Spencer Tracy, Milton Berle, and Ethel Merman.

But our markets have their own cast of contributing perennial bulls (and comediennes) that worship at the altar of price — that we watch daily in the business media. We no longer mention these actors (and nameless machines/algos) that are looking for investment treasures as we prefer to criticize by category and praise by individual.

It’s truly A Mad, Mad, Mad, Mad World.

Read on about the markets which, to paraphrase Warren Buffett, are now feeling less like a church and more like a casino…

Position: None

BY Doug Kass · May 13, 2026, 6:30 AM EDT

Only in Cathie Wood’s world would anyone have the nerve to tweet this out:

Position: None

BY Doug Kass · May 13, 2026, 6:04 AM EDT

The S&P Short Range Oscillator is only slightly overbought at 0.74% vs. 1.101%.

Position: None

BY Doug Kass · May 13, 2026, 5:45 AM EDT

It's official: Nvidia, $NVDA, has surpassed silver as the second largest asset in the world, worth $5.52 trillion. Google is less than 4% away from becoming the second company in history to hit $5 trillion in market cap. We are witnessing a historic technological revolution.

BREAKING: President Trump says "the great" Jensen Huang of Nvidia, $NVDA, is currently on the Air Force One with him on the way to China. Trump says Elon Musk, Tim Cook, Larry Fink, Stephen Schwarzman, David Solomon, and many other CEOs are joining him on the trip.

At the top of the dot-com bubble, a Berkshire shareholder asked Buffett and Munger to “just speculate” 10% in tech. Their answer aged perfectly. April 29, 2000.

The U.S. 30-Year Yield is now 5.03%. It has only been higher for a handful of days in the last 19 years. And it is now just 8 basis points from a new 19-year high.

Enough is enough. Read this tweet from @InTheAssembly on $ARKK performance and Cathie Wood... it is not ad hominem, its factual- "Cathie Wood might be the most expensive lesson retail investors have ever paid for. Her flagship ARK Innovation ETF is down 23% in the last 5 Show more

Cathie Wood might be the most expensive lesson retail investors have ever paid for. Her flagship ARK Innovation ETF is down 23% in the last 5 years. The S&P 500 is up 77% over the same period. She has underperformed the index by 100 percentage points. And she has done it

$QQQ Eventually, this will turn into a big problem at this pace. If you understand the depths of these two charts. — Capex vs Operating Income — Cash vs Liabilities

It’s a very under-appreciated asset associated with her strategies

It’s a very under-appreciated asset associated with her strategies

Cathie Wood might be the most expensive lesson retail investors have ever paid for. Her flagship ARK Innovation ETF is down 23% in the last 5 years. The S&P 500 is up 77% over the same period. She has underperformed the index by 100 percentage points. And she has done itShow more

@KellyCNBC The Micron analyst you are interviewing is bullish on $MU. This morning he raised his price target from $500 to $800 (where it is currently trading). Why even interview him if he was so far off in his expectations for $MU share price? He is making it sound that he Show more

Ugly, Tailing 30Y Auction Makes History With First 5%+ Yield Since The Great Quant Crash Of Aug 2007 zerohedge.com/markets/ugly-t…

🔴The US tech sector has NEVER been this large: Tech and tech-related stocks now make up ~57% of the total US market cap, a record high. This is 6-7 percentage points higher than at the 2000 Dot-Com Bubble peak. As a result, defensive stocks, including healthcare, utilities, Show more

“Combined free cash flow across Microsoft, Alphabet, Amazon, Meta, and Oracle is projected to FALL more than -70%, to ~$100 billion, by the end of …. AI capital expenditure is consuming nearly every dollar, with the combined 2026 CapEx expected to surpass $715 billion….. In Show more