Surprise in August CPI Data Adds to Our Rate Cut Thinking

The odds of the Fed pushing back on rate cut expectations are now rising.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

*The core CPI data for August raises the probability for the Fed to push back on rate cut expectations

*Sequential core CPI data ticked higher again in August, while the year-over-year data was unchanged at 3.2%

*The odds of the Fed pushing back on the market’s 2024 rate cut expectations are rising

*As the market rethinks rate cut prospects, we’ll let stock prices come to us

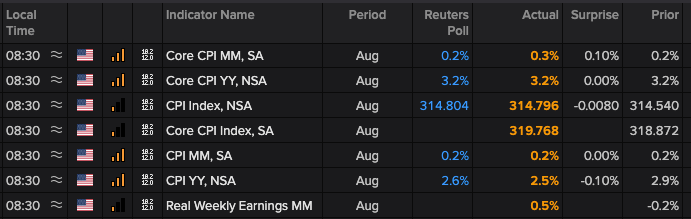

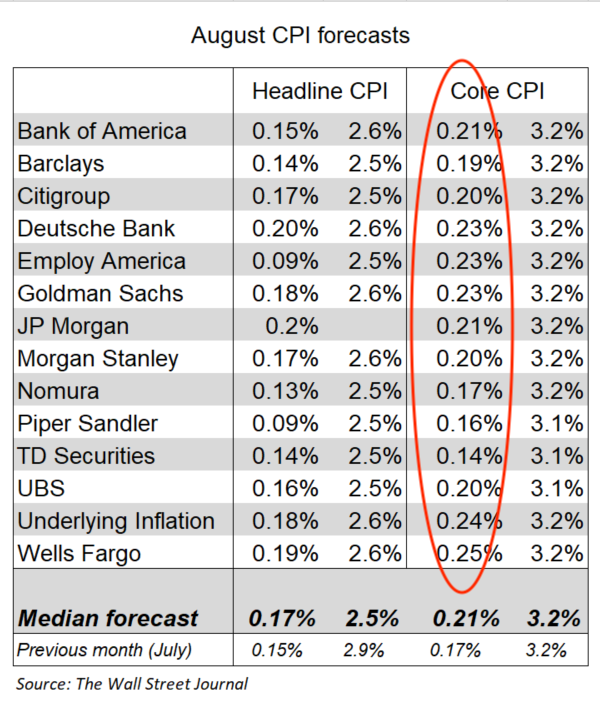

We raised the potential for a surprise in the August Consumer Price Index (CPI) report and it’s fair to say there was one. Granted, the headline CPI figure on a year-over-year basis came in a tad better than expected at 2.5%, down from 2.9% in July and the market forecast of 2.6%, but the sequential uptick on core CPI to 0.3% compared to 0.2% in July and 0.1% in June sticks out like a sore thumb.

That 0.3% print month-over-month core CPI print wasn’t on economists' radar screens either.

The upward trend in the sequential core CPI data plus the year-over-year core CPI reading of 3.2% for August, unchanged with July’s figure and down only a tick from 3.3% in June, is more ammunition for the Fed to deliver only a 25-basis point rate cut next week.

Along with recently-updated GDP expectations for the current quarter, Wednesday's report increased the probability that the number of projected rate cuts in the Fed’s updated set of economic projections will fall short of what’s been depicted in the CME FedWatch Tool.

Ahead of Wednesday's CPI data, it’s been showing 100 BPS to 125 BPS in rate cuts by the end of this year, and 225 BPS by June 2025. Based on the data received so far, we continue to see two rate cuts this year with the pace of 2025 rate cuts determined by incoming data.

We’re likely to see the CME FedWatch figures waver some as the market absorbs the core CPI data, but let’s remember that the August Producer Price Index (PPI) arrives on Thursday. The inflation comments found in the August PMI reports from ISM and S&P Global suggest we could see a surprise in that data as well. If we do, it will up the likelihood of the market being disappointed next week, and if history holds, the resetting of rate cut expectations will weigh on the market.

We boosted our cash levels coming into September and, given the likely scenario laid out above, we’re going to take our time putting it to work.