Reviewing 2025 EPS Expectations for the S&P 500 and Its Sectors

Here's why we are not fans of the GICS classification system used by the Wall Street herd.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We have back-to-back holiday weeks ahead of us, which leaves just over four and a half days of trading left in 2024. Tuesday we’ll be on watch to see if a Santa Claus rally emerges, but U.S. equity markets will close at 1 p.m. ahead of Wednesday’s Christmas holiday.

Odds are, much like today and tomorrow, Thursday and Friday will see slow trading volumes and a lack of fresh economic data and Fed official sightings. We will be on guard for any companies attempting to sneak less-than-favorable news but as you saw this morning with our latest portfolio additions, we’ll be more than just keeping an eye on things.

Quieter times in the market, which have been few and far between of late, allow us to do some higher-level thinking — and this time around that has us revisiting earnings expectations for the S&P 500. As we get ready to close out the December quarter and enter a new year, we are taking a fresh look at what’s expected for 2025.

To get ready for this conversation, we’re sharing the portfolio’s positions in S&P 500 companies by their global industry classification standard (GICS), which is the categorization used by FactSet. We have our issues with schema, and one example as to why is the question of why Amazon AMZN is categorized as a Consumer Discretionary when Amazon Web Services furnishes more than 60% of the company’s operating profit. It’s instances like this that first led us to develop and utilize our thematic framework, which better identifies structural changes and tailwinds as well as headwinds for companies.

With that said here is the GICS classification for the TheStreet Pro Portfolio’s S&P 500 holdings:

Communication Services – Alphabet GOOGL, Meta Platforms META

Consumer Discretionary – Amazon AMZN

Consumer Staples – Costco COST

Financials – Bank of America BAC, Morgan Stanley MS, American Express AXP, Mastercard MA

Healthcare – LabCorp LH

Industrials - Builders FirstSource BLDR, Eaton ETN, Lockheed Martin LMT, United Rentals URI, Waste Management WM

Information Technology - Apple AAPL, Applied Materials AMAT, Microsoft MSFT, Nvidia NVDA, Qualcomm QCOM, ServiceNow NOW

Materials - Vulcan Materials VMC

At this time, we have no positions that fall into the Energy, Utilities, or Real Estate GICs categories. And as you scan over that breakdown, odds are you’ll scratch your head as to why some of those names are in those categories. Part of it is a lazy attempt to categorize thousands of companies into just 11 sectors but we’ll keep quiet about that as it can bring opportunities to those that are willing to do the extra work. You’ll also notice that TheStreet Pro Portfolio holdings Dutch Bros BROS, Elastic ESTC, Marvell MRVL, Universal Display OLED, and The Trade Desk TTD are not listed above, the reason being they are not in the S&P 500.

S&P 500 EPS Expectations

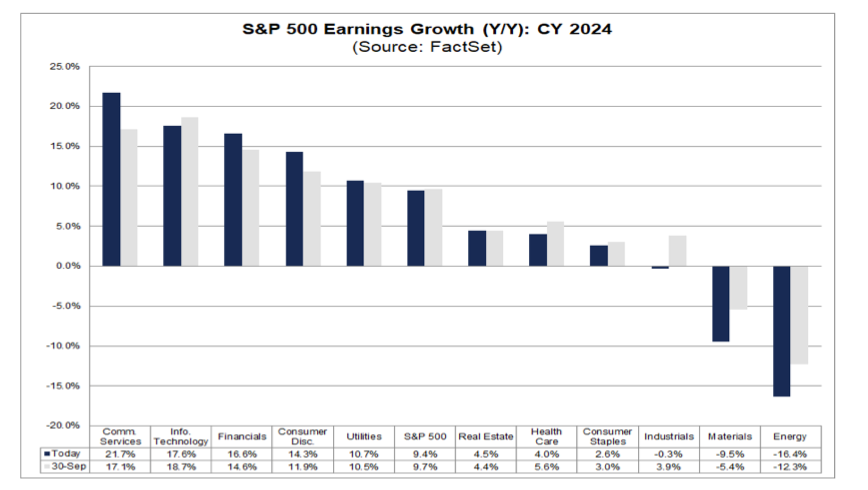

For the fourth quarter, S&P 500 companies are expected to report year-over-year growth in earnings of 11.9% and year-over-year growth in revenues of 4.6%. Sectors that are poised to deliver superior EPS growth include Financials, Communication Services, Info Technology, and Healthcare, which you'll see by the GICS breakdown above sets us up rather well for the upcoming December quarter earnings season.

For 2024, the basket of S&P 500 companies is expected to report year-over-year growth in earnings of 9.4% and year-over-year growth in revenues of 5.1%. That’s down slightly from the late-September figures of 10% and 5.4%, respectively.

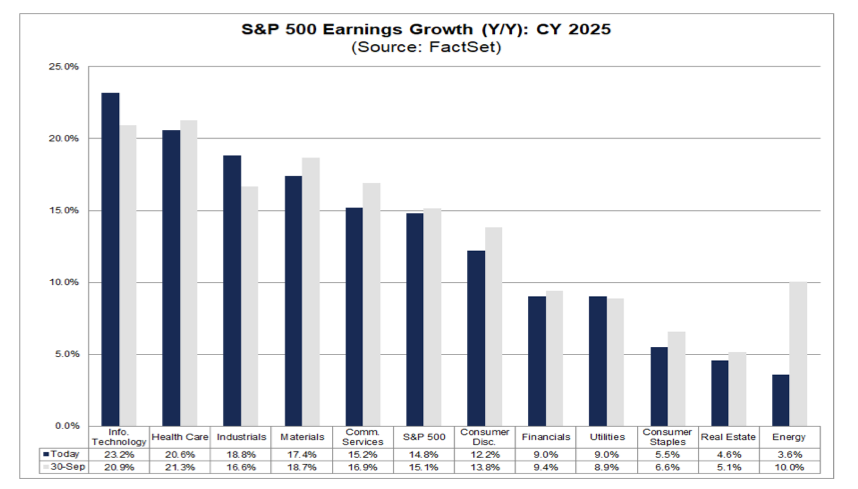

For calendar year 2025, analysts are projecting earnings growth of 14.8% and revenue growth of 5.8%, which is also down modestly compared to the late-September figures of 15.2% and 5.9%, respectively. However, when we look at the composition of EPS growth, there has been some noticeable movement:

Information Technology is now expected to deliver EPS growth of 23.2% next year, up from 21.2% in late September and 21.7% for 2024.

Prospects for EPS growth in the Healthcare sector have been trimmed back to 20.6% from 21.3%.

Consensus EPS growth for Industrials has been lifted to 18.8% from 16.6% in 2025, a much quicker pace compared to -0.3% for 2024.

EPS expectations for the Materials sector have been trimmed to +17.45 next year, down from 18.7% about three months ago. Much like Industrials, however, that’s a far better outlook compared to the EPS decline of 9.5% penciled in for this year.

After delivering double-digit EPS growth this year, the consensus calls for the Communication Services sector to deliver addtional 15%+ bottom-line growth in 2025. Granted that is down a modest amount compared to early September, but that likely reflects higher capital spending levels this quarter and in H1 2025 as we’ve discussed for Meta and others.

Consumer Discretionary is still expected to deliver double-digit EPS growth next year albeit at a slightly slower pace than previously thought — up just over 12% compared to almost 14% in early September. Our recent mall walks found aggressive sales and promotional activity even before we move past the Christmas holiday. That suggests retailers could be taking it on the chin in terms of margins as they clear out product to make way for the spring selling season. While this is potentially good for shoppers and our shares of Mastercard and American Express, it's not good for retailer earnings.

EPS expectations for Consumer Staples companies have inched lower to 5.5% from more than 6.5%, which likely reflects the rebound in food prices. Spotting that data led to our recent downgrade and subsequent removal from the portfolio of PepsiCo PEP.

The market expects the Financial sector to deliver a slower pace of EPS growth in 2025, near 9.0% compared to more than 16% this year, but if we see the expected strength in IPO and M&A activity come to fruition that 2025 figure will need to be increased.

Sticking to Our Strategy

One of our strategies for the portfolio is focusing on companies with superior earnings growth compared to the S&P 500. We have no intent of straying off that path, but we also have to recognize that not all companies in a GICS sector are the same.

This means that even though we will focus on superior earnings growth prospects, we won’t ignore companies just because they are in a particular sector. As we pointed out above, we are not exactly fans of the GIS classification system even though it is a Wall Street staple. We’ll continue to focus on differentiated business models and companies benefiting from structural tailwinds.

At the time of publication, TheStreet Pro Portfolio was long AMZN, GOOGL, META, COST, BAC, MS, AXP, MA, LH, BLDR, ETN, LMT, URI, WM, AAPL, AMAT, MSFT, NVDA, QCOM, NOW, VMC, BROS, MRVL, ESTC, OLED and TTD.