May CPI Up Largely as Expected, But It’s Not That Simple

Ahead of tomorrow’s U.S. May PPI report, China’s May PPI accelerated further.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

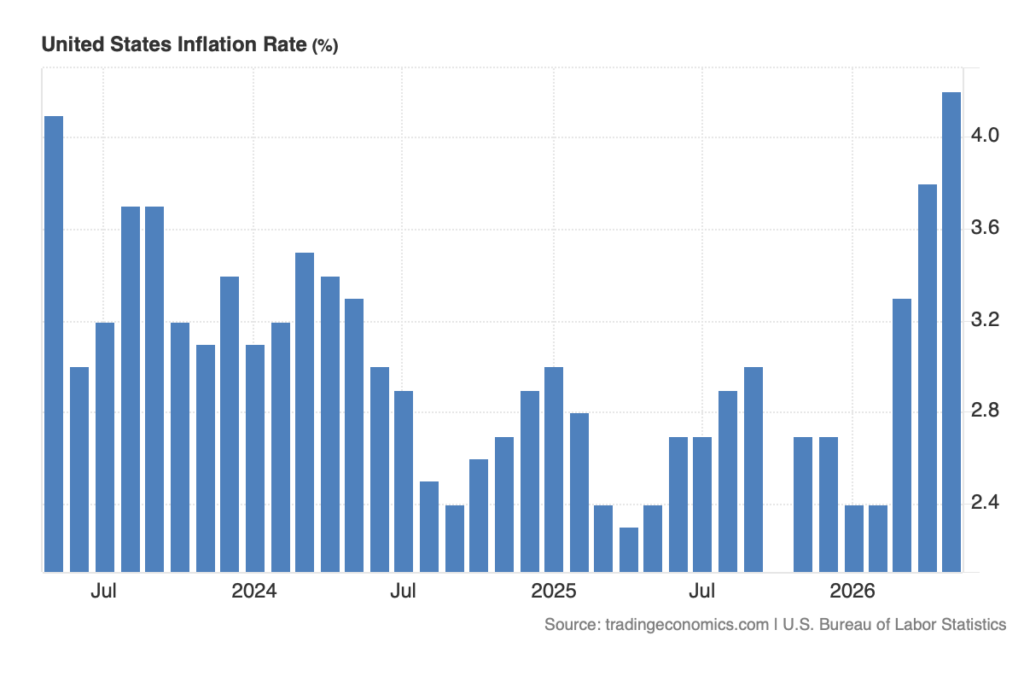

The first part of the back-to-back May inflation reports is out, with the May Consumer Price Index (CPI) largely in line with market forecasts. That means headline inflation accelerated to 4.2% on a year-over-year basis, continuing the steep level of acceleration that began in March. That May figure is the highest since May 2023’s 4.1% reading.

The May Core CPI also matched expectations with a tick higher to 2.9% from April’s 2.8% reading. While not the highest reading for that indicator in the last year, it does continue the upward trajectory that began in March.

We realize that there are those folks who focus on core CPI, and they have their reasons. However, when it comes to the consumer, who spends ~13% of their total annual household expenditures on food and ~10% on energy, higher prices for those items are going to be felt. That’s the difference between reading the data for monetary policy implications vs. consumer spending and investing ones.

We’ll stick with our positions in Costco (COST) and TJX (TJX) as well as Amazon (AMZN) ahead of the upcoming Prime Day event that runs from June 23-26. We will also be on the lookout for opportunities to increase our exposure to those stocks where it makes sense.

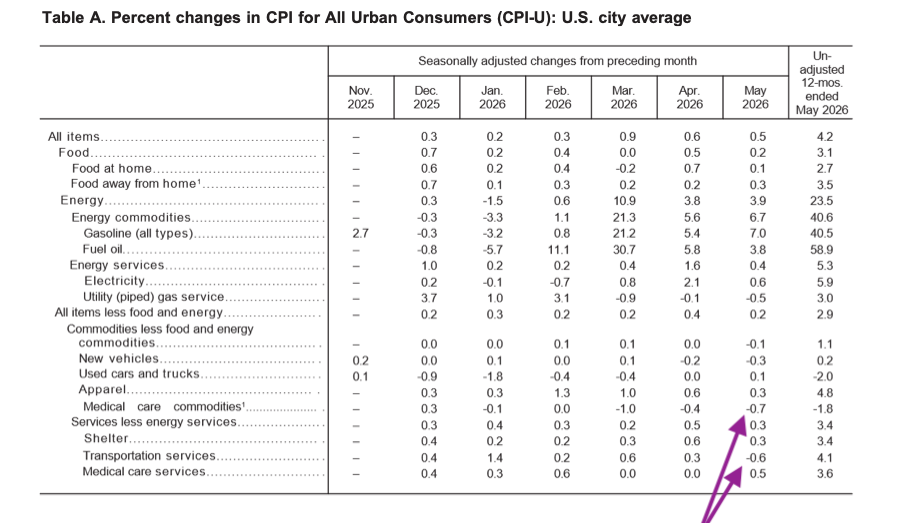

What was a little surprising was the fall in the sequential May core inflation rate to 0.2% from 0.4% in April. This puts it back in the range we saw in February and March. And for the folks who simply annualize that figure, it will give them an argument to rationalize a potential rate cut. After all, the implied 2.4% annualized figure is well below the implied 4.8% if we simply annualized the April figure.

In the face of the other inflation data, our response to that is that annualizing the trailing three-month sequential core CPI figures through May kicks out something closer to 3.2%. That matches what the figure would be for April and is up from the 2.8% reading for March on that basis.

As far as what led the May core CPI to decline on a sequential basis, we can trace that to the following:

Our view remains that Thursday’s May Producer Price Index (PPI) and what it shows compared to March and April will be important. Based on the May PMI reports, we know companies are attempting to push through further price increases to offset rising input costs. We also know the flow through from the PPI data to CPI data is on a lagged basis.

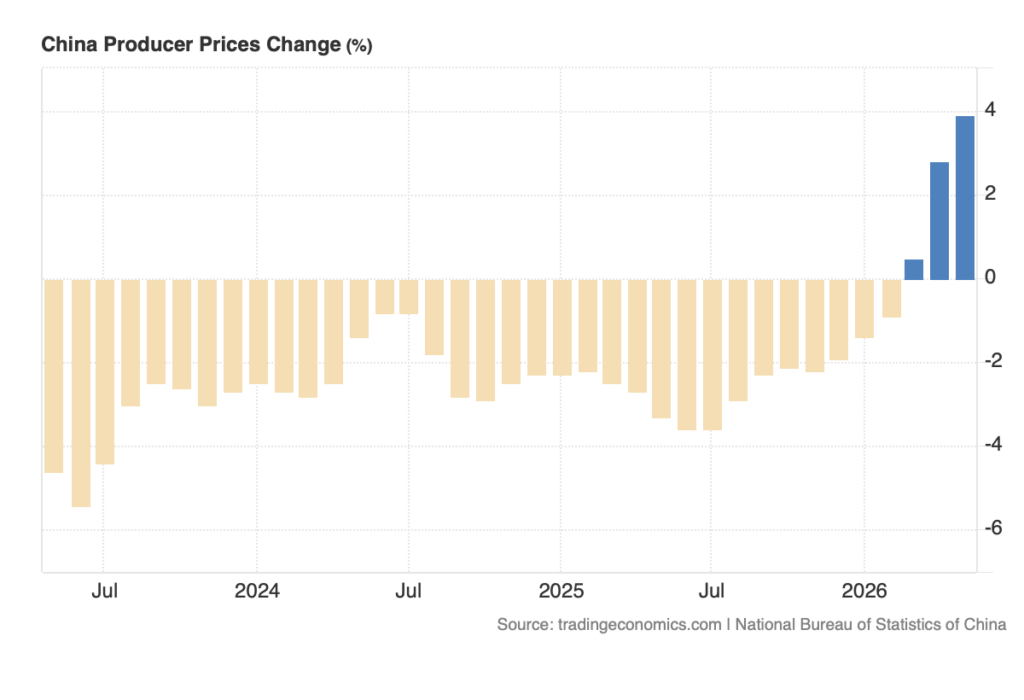

And you may remember that early last month we shared with you the news that Chinese suppliers to U.S. companies and retailers were hiking prices for the first time in not months, but years. Reported increases at the time were in the 5%-15% range, and that led us to keep an eye on China producer prices.

Early this morning, we learned China’s producer prices increased 3.9% year on year in May, accelerating from a 2.8% rise in the previous month. May marked the third consecutive monthly increase and the fastest pace since July 2022. What’s driving those prices higher? Global commodity and energy prices and supply disruptions stemming from the war in Iran.

Putting it all together, we are seeing the first-hand impact of the duration and follow-through of the U.S.-Iran war, and with signs the conflict could re-escalate, we see the growing probability that more investors will come around to raising the same questions we have been about consensus H2 2026 expectations.

We have our updated set of pick-up points and checkpoints, as well as some new candidates to keep our eyes on in the Bullpen. In the near term, we’ll let the Portfolio’s market hedging, inverse ETF positions and its cash do their thing.

At the time of publication, TheStreet Pro was long AMZN, COST, and TJX.