The Market’s Valuation and Second-Half 2024 EPS Are Starting to Matter

June's CPI report brings rate cuts that much closer, and it's lifting some of our holdings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

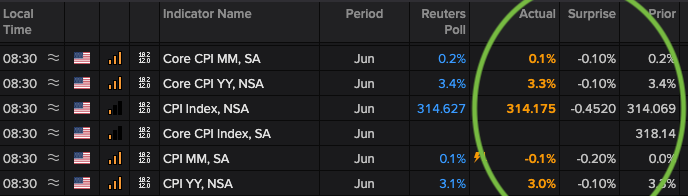

* The June CPI report showed further progress, surprising to the downside across the board.

* This adds another layer of supportive data for rate cuts as Treasury yields move lower.

* As we suspected, the market’s response to these good data points shows its valuation and H2 2024 EPS prospects are coming into focus.

* Delta Air Lines and ConAgra guide below expectations, and we have questions going into PepsiCo’s earnings conference call.

Treasury yields are tumbling this morning in response to what we can only describe as a better-than-expected June CPI report. As we can see in the table below, the June results were not only lower compared to the May figures, but they were also lower than the market expected.

This is more good news for potential rate cuts following Fed Chair Powell’s comments over the preceding two days of congressional testimony. That is driving some of our more interest rate-sensitive positions, such as Builders FirstSource BLDR, United Rentals URI, and Vulcan Materials VMC higher.

The larger knee-jerk reaction we would have expected to see following these fresh CPI figures would be the market moving higher, but this morning is also the start of the June-quarter earnings season. While the reports are few so far, what we’re seeing is raising some questions. As you know, our view has been that past a certain point, the market’s attention would turn to the S&P 500’s valuation and EPS growth prospects for the second half of the year.

It would seem that is starting to happen.

We say this because this morning, Delta Air Lines DAL missed EPS expectations and guided revenue and EPS for the current quarter below market expectations.

Meanwhile, portfolio holding PepsiCo PEP delivered mixed quarterly results, with better-than-expected EPS and revenue that came up modestly short. PepsiCo reiterated its 2024 EPS forecast for $8.15, a few pennies ahead of the Wall Street consensus at $8.13.

Reading between the lines, and without raising its bottom-line outlook following the $0.12 EPS beat for the June quarter, we believe PepsiCo is being conservative in its EPS outlook for H2 2024. We’ll have a clearer picture as we digest the company’s earnings call comments, and we will share our thoughts with you in a follow-up alert. In the meantime, it’s looking like a “shoot first, ask questions later” mentality is taking hold, but depending on what we learn that could spell opportunity.

While frozen and packaged food company ConAgra CAG also reported mixed May quarter results, the company issued downside guidance for the coming year.

More Pro Portfolio:

- Locking in Big Gains on This High-Flying Stock

- Weekly Roundup: Reasons to Be Cautious

- Reading the 'News Signals' From Our Investing Notebook

We recognized this likely shift in market focus earlier this week and the potential risk. But we have to consider this morning brought just three earnings reports, and it will take many more before we have a clear picture about H2 2024 earnings.

Nevertheless, following the market’s run-up over the last several weeks and its overbought status, we could see some of the froth come out. That would give us an opportunity to revisit some of the names on our shopping list at better prices, while recent data points keep us bullish for the medium to longer term. It also means we will continue to focus on companies with superior EPS prospects for the coming quarters.

At the time of publication, TheStreet Pro Portfolio was long BLDR, URI, VMC and PEP.