Leaked ASML Release Drags This Holding Lower

We suspect Intel’s woes may be the culprit, but we may not know until a formal update.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The Portfolio’s position in Applied Materials AMAT is under some pressure on Tuesday following an earlier-than-planned release of September quarter results from lithography company ASML ASML.

It seems that the results were posted sooner than even the company expected with the management team sharing that “due to a technical error, information relating to our Q3 2024 results was erroneously published earlier today.”

In any case, what jumped out at the market was the 53% sequential drop in ASML’s booking for the September quarter of €2.63 billion. That was substantially below the consensus estimate of €5.39 billion and ASML chalks that up to a lengthier rebound in lithography demand.

We suspect the miss may be tied to Intel INTC, given its recent problems and restructuring as Intel, Taiwan Semi TSM and Samsung SSNLF account for about 80% of ASML’s revenue stream. A few weeks back, as Intel’s issues were making headlines, we pointed out that it was less than a 10% customer for Applied Materials. That suggests any disruption should be far smaller at Applied — though we’ll want confirmation that Intel is indeed the largest part of the booking’s shortfall.

Complicating this is that we have only the earnings press release to go on because, despite the report being published early, ASML will hold its earnings call tomorrow. That should bring more color behind the sharp drop in September bookings, and why management is comfortable with the December quarter revenue ramp.

While ASML sees current-quarter revenue rising to €8.8 billion to €9.2 billion for the current quarter from €7.5 billion in the September one, its outlook for 2025 was trimmed to €30 billion to €35 billion from €30 billion to €40 billion. For this year, ASML sees its top line coming in at €28 billion, up from its prior forecast of €27.7 billion. We expect there will be many questions about its revised 2025 outlook, including its confidence following the fall in September quarter bookings.

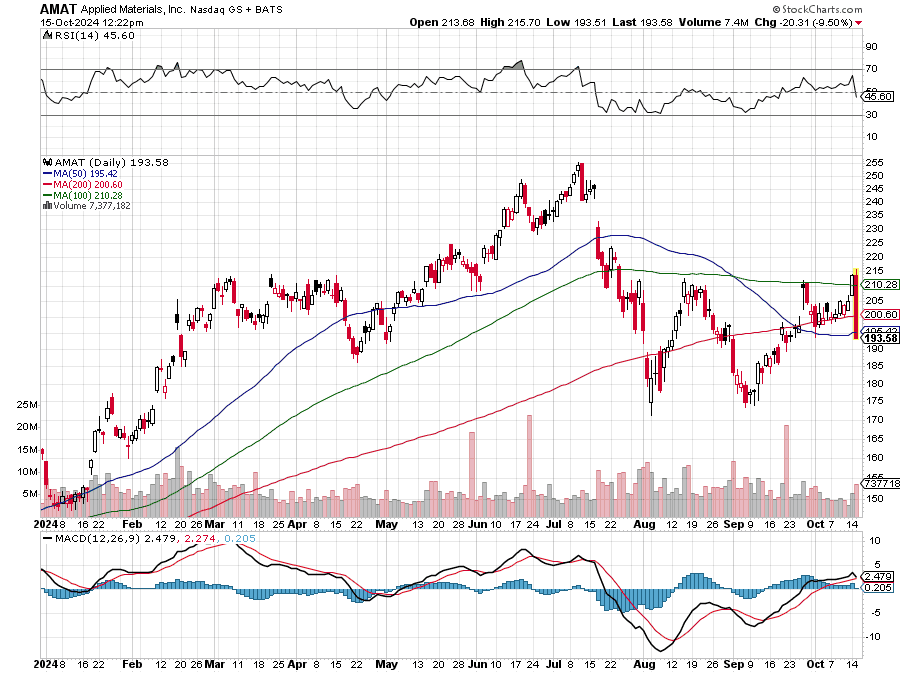

Based on what we learn, if AMAT shares can hold onto support at the 50-day moving average, it could be a place for newer members to pick up a few shares. Should TSM signal its capital spending for this year and next needs to be revised higher when it reports on Thursday that would bring more support for adding some fresh AMAT shares.

More Pro Portfolio

- Why We Opened a Position in a $8.4 Billion AI Name

- Weekly Roundup: Portfolio Begins October With Big Gains and Big Moves

- We Did the Homework for You: Here're the Top Stories on Our Investing Themes

At the time of publication, TheStreet Pro Portfolio was long AMAT.