Here’s Our Plan Following Market Sell-Off and Potential for More

If the market plays out how we expect, we'll pursue these stocks on our shopping list.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

*The market mood is once again back in “shoot first, ask questions later” mode

*We could see the market trend lower as it grapples with the reality of rate-cut prospects

*This could resemble what we saw in early August, and that has us getting prepared but also mindful

Tuesday's market sell-off on the heels of fresh manufacturing PMI data showed that part of the economy contracting is a bit of a retread from what we saw at the start of August. In addition to the renewed concerns over the speed of the economy, at that time, we also had the unwinding of the yen carry trade weighing on the market.

Earnings were mixed and Big Tech announced larger spending plans for the balance of 2024 and 2025. All of that culminated in the Volatility Index popping, the Fear & Greed Index falling into "extreme fear" and the S&P 500 falling from being meaningfully overbought in mid-July to coming within a breadth of touching oversold territory in early August.

At that point in time, the market bottomed, and we were back off to the races with the Portfolio taking advantage of several opportunities. You’ll recall that’s when we called up shares of Meta Platforms META, Eaton ETN and Dutch Bros BROS from the Bullpen, and added to our Amazon AMZN, Microsoft MSFT, Marvell MRVL, Bank of America BAC, Morgan Stanley MS and Universal Display OLED positions. Soon thereafter, the market punched its way higher after Fed Chair Powell’s now infamous Jackson Hole comment that goosed expectations for a September rate cut. But, let’s remember, Powell also reiterated that “the timing and pace of rate cuts will depend on incoming data.”

Data Later This Week Likely to Dictate What’s Ahead

Because of the Labor Day holiday, we’re back in familiar territory, treading water as we wait for the next round of data. On Wednesday, that includes the July JOLTS report and, at 2 p.m. ET, the latest installment of the Fed Beige Book.

Both will be scoured for insights on the jobs market and, in the case of the Beige Book, insights on the speed of the economy, the consumer and inflation. Given the timing of data collection for the Beige Book, it may serve as a nice compliment to Tuesday's manufacturing PMI data.

However, as we discussed on Tuesday, with data from ISM pointing to the manufacturing economy contracting in 11 of the last 12 months, we and the market will be far more focused on Thursday's data – August Service PMIs and the ADP August Employment Change Report – and how they reshape expectations for Friday’s August Employment Report.

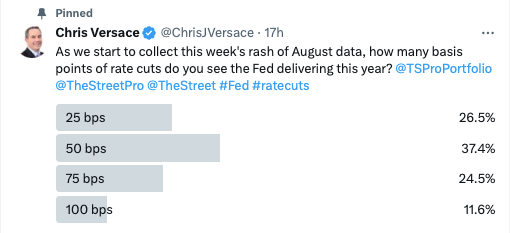

As we see it, what’s at stake is the expected number of rate cuts that the Fed will deliver this year and the potential for S&P 500 consensus 2H 2024 EPS expectations to move lower yet again as we navigate the September wave of investor conferences that begins Wednesday with Citi’s Global TMT Conference. We’ve talked with you about the market likely being out over its skis with its expectation for 100 basis points in rate cuts for this year, and data coming later this week will not only make or break that market expectation, but set the stage for the Fed’s policy action and updated projections that will be delivered on September 18.

Market Support Levels We’re Watching

That brings us back to treading water on Wednesday as we wait for these items to start unfolding.

Periods of nervousness and uncertainty in the market can lead to “shoot first, ask questions later” and other snap decisions that may be regretted later. That is why we will put our emotions to the side and focus on matching opportunity with what the data tells us.

Should that data support something between a no-landing and soft-landing scenario for the economy, it would suggest we’re going to see less rate-cut action by the Fed than the market hopes for. Even though our thinking, based on data to date, has been that the Fed will deliver two rate cuts this year (which matches the early findings in our rate cut poll), as the market’s hopium is dashed, odds are the market will move lower. This has us looking at support levels for the market.

The next level of support for the S&P 500 and the Nasdaq Composite are less than 1% away at 5,504 and 1,7094, respectively, with the next levels 3% to 5% below those from Tuesday night’s closing levels. If we hit those next levels near 5,368 for the S&P 500 and 16,233 for the Nasdaq, it would equate pullbacks of 5% and around 8.5%, respectively. It goes without saying that the market would be well out of overbought territory, and likely closer to being oversold. We’d also have a little more breathing room in the S&P 500 valuation.

The Shopping List

That’s the likely environment, and if that is how it plays out, we may repeat our early August action, taking advantage of the mismatch between stock prices and medium- to longer-term opportunities. We will want to have our shopping list ready, and while the pecking order may evolve, we can share the following holdings are on it.

If the expectation for the total amount of rate cuts for this year moves lower, odds are that we will see more interest rate companies get dragged lower. Let’s remember: we should be more focused on the rate-cutting cycle itself and where that will land in the next 12 to 18 months. For that reason, Builders FirstSource BLDR and Eaton Corp. are on our shopping list.

Revisions in rate cut expectations have made for volatile times in tech, and while we have a relatively full position in Marvell, Tuesday's market action has brought some room in the ones for Nvidia NVDA, Qualcomm QCOM and Universal Display. Meta Platforms and ServiceNow NOW are also ones we’re watching.

REITs have been on a bit of a tear in recent weeks with some, like Omega Healthcare OHI, well into overbought territory. Dashed hopes for rate cuts could bring those and other REITs, like Healthpeak Properties PEAK back down to earth. We’ll also keep our eyes on recent Bullpen addition Netflix NFLX.

Applied Materials and Elevance Health

As it relates to Applied Materials AMAT, we are aware the current share price is below our $195 panic point. In last Friday’s Monthly Roundup, we acknowledged the position was flirting with that panic point, but we also shared we would be paying strict attention to Applied’s presentation at the Citi Global TMT Conference on Wednesday. As we review what is said, the question we’ll be looking to answer is whether we should cut bait and lock in the gain we have or if the fundamental outlook warrants taking advantage of the current drop in the shares. As that answer is determined, we’ll share our thoughts and any actions we take with the portfolio with you.

We’ll also continue to keep watch on those positions that are approaching our price target, and ones that may benefit from this latest round of market fear to move past our price target. Three-rated Elevance Health ELV falls into that camp. And yes, those shares have pushed into overbought territory.

More Pro Portfolio

- Taking Some Profits in a Healthcare Stock and Downgrading Its Rating

- Monthly Roundup: August Brought the Portfolio Several Opportunities

- Why Apple Needs a Wow Moment With Apple Intelligence on September 9

At the time of publication, TheStreet Pro Portfolio was long META, ETN, BROS, AMZN, MSFT, MRVL, BAC, MS, OLED, BLDR, NVDA, QCOM, NOW, AMAT and ELV.