After September Beat Seasonality Predictions, Headwinds Blow In

Port strikes, jobs data and Israel's increased fighting add to market uncertainties in October.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

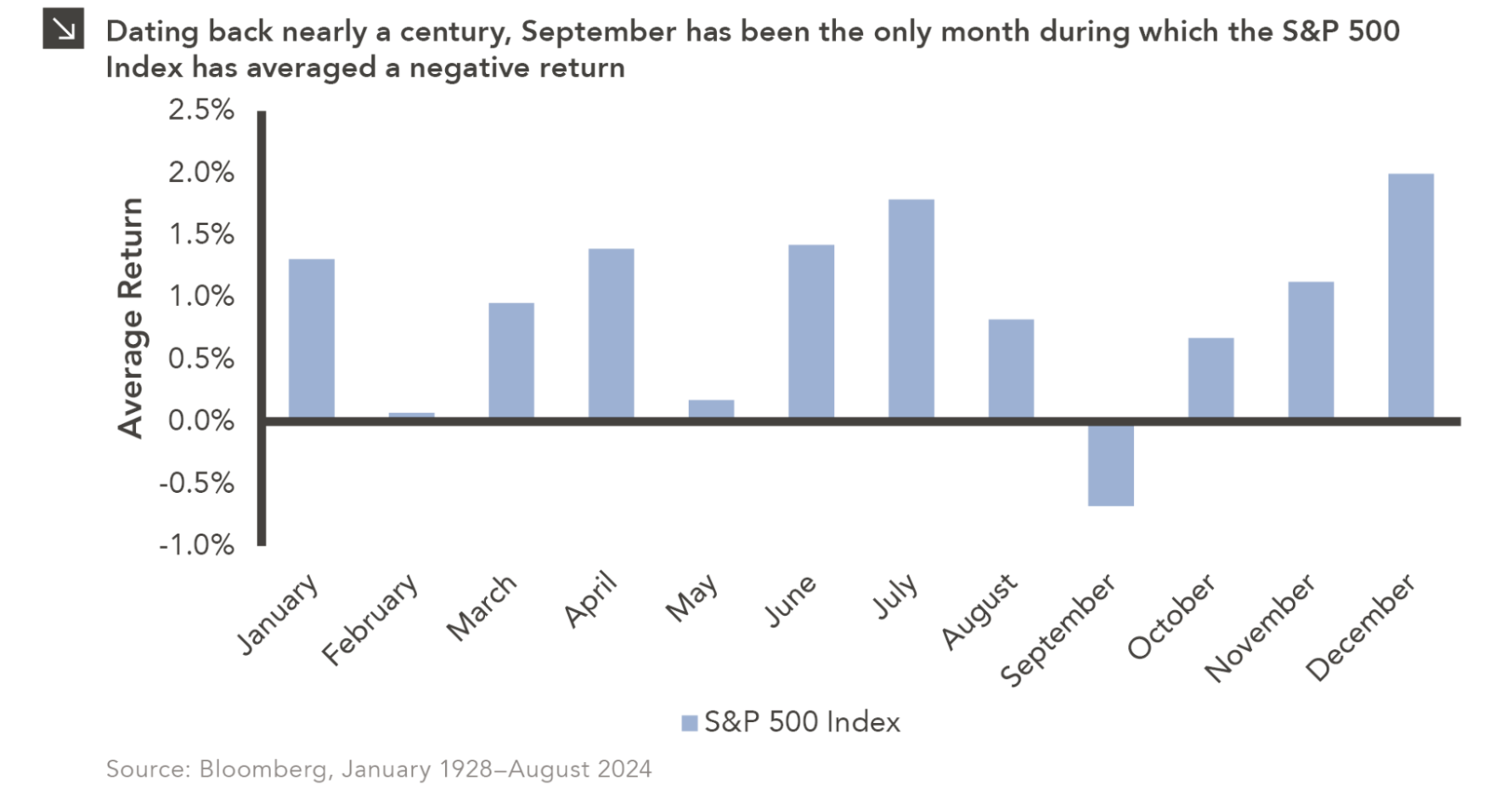

September proved the seasonality predictions wrong. The historical pattern for the month was broken, as the S&P 500 notched a 2.0% increase, while the Nasdaq Composite added 2.7%.

We can attribute that outsized performance for the market to the Fed cutting rates in mid-September and then China’s signaling for further stimulus to prop up its sagging economy.

We’ve discussed the sizable moves in several holdings over the last few weeks, including those for Builders FirstSource BLDR, and United Rentals URI, as they led the portfolio to climb 2.12% during September.

With the S&P 500 notching another record close and the Fear & Greed Index tipping into Extreme Greed yesterday, we see increasing probability the market is extended. As we enter the final quarter of the year -- which is typically positive for stocks -- we can see a few headwinds that have emerged that could challenge the market’s typical path. We must closely watch the pace of job creation, the potential length of the longshoreman strike, and developments in the Middle East.

If we begin to see a vulnerable market, the cash we raised heading into September will be a buffer. Should we feel the need to raise some additional cash, likely candidates for trimming would be holdings near or already overbought, such as United Rentals URI, Lockheed Martin LMT, and Axon AXON.

Jobs Data and Rate-Cut Implications

Fed Chair Jerome Powell said yesterday that the recent half-percentage point interest rate cut shouldn’t be interpreted as a sign that future moves will be as aggressive and reiterated the Fed isn’t on any set course with further cuts. With the Fed balancing continued progress on inflation with supporting the labor market, we expect investors will dig heavily into this week's August and September employment market comments and data.

That begins today with job creation findings in both September Manufacturing PMI reports as well as the August JOLTs job openings report. Those initial indications will be supplemented by tomorrow’s September ADP Employment Report, Thursday’s September Service PMIs, and of course Friday’s September Employment Report. Once again, bad news in the form of weaker-than-expected hiring is likely to be viewed in a positive light for rate cuts and that could give the market some additional lift.

We also have a bevy of Fed speakers today, and we will be mindful of their comments following those from Powell yesterday, looking to see how they interpret today’s data. We will then look to Friday’s September employment report.

Port Strike and Middle East Tensions

Other headwinds that could alter that course include the port union strike that saw 50,000 longshoremen walk off East Coast and Gulf Coast ports. This is the first major strike for these ports in some 47 years and estimates put between 43%-49% of all U.S. imports and billions of dollars in trade moving through those ports. This will have an impact on supply chains and the U.S. economy, but the size of that impact will hinge on the duration of the strike. Because the International Longshoreman’s Association (ILA) rejected an offer from the port management group USMX on Monday that included a wage hike over six years near 50%, it’s possible the strike may not be a short one.

A disruption of one to two weeks will have modest consequences, but a longer strike will be far more disruptive and risk upward price pressures. A lengthy strike could be a major headwind for the holiday shopping season as well as the auto and food industries. A modest and renewed acceleration in inflation pressures could result in the Fed becoming more cautious about future rate-cut timing, potentially weighing on the market.

On top of that, geopolitical tensions in the Middle East continue to rise, adding even more uncertainty into the mix. Israel has sent soldiers into Southern Lebanon, raising the risk of a wider regional conflict. U.S., European, and Arab states have called for restraint and concerns are for a protracted fight and the creation of a long-term “security zone,” something that could risk a wider regional war involving Iran.

August Construction Spending

Today also brings the August Construction Spending report and what it says about the pace of residential and nonresidential construction are potential catalysts for our Builders FirstSource BLDR, United Rentals URI, and Vulcan Materials VMC shares.