2 Stocks on Our Radar as Iran Halts Talks and Inflation Pressures Continue

Let’s discuss the latest out of the Middle East and break down May Manufacturing PMI.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Dynamic situations mean paying close attention to developing news, and that is what we have this morning.

In our opening comments, we shared that we were “cautiously optimistic that despite a series of skirmishes over the last week, peace talks between the U.S. and Iran have continued.” However, those continued talks now appear to be over following reports that Iran is stopping message exchanges with the U.S. through mediators due to attacks on Lebanon and may completely block the Strait of Hormuz. Whether or not the pause is temporary or the start of renewed conflict will be determined by Israel, its attacks in Gaza and Lebanon, and its withdrawal from occupied areas in Lebanon.

Whether President Trump can rein in Israel’s Prime Minister Benjamin Netanyahu is one of the underlying questions. Can the fragile peace talks hold up and give way to a ceasefire that can deliver more long-lasting results is another.

Time will tell, and that means we will be closely following developments in oil, which is rebounding in response, and the Cboe Volatility Index (VIX). In the back of our mind is the overbought nature of the market we discussed in Friday’s Monthly Roundup following nine weeks of gains. We’ll tread carefully near-term, keeping the Pro Portfolio’s inverse ETF positions in play but continue to look for new blood for the Bullpen.

ISM’s May Manufacturing PMI

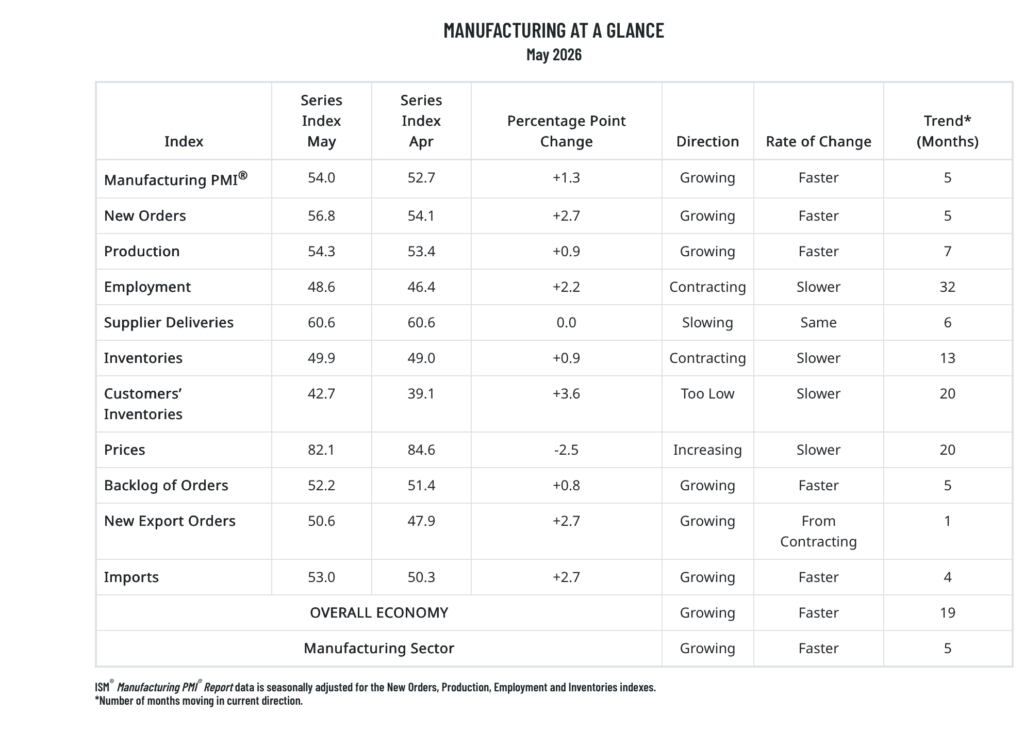

Adding to our decision to stay on the sidelines is this morning’s May Manufacturing PMI from ISM. In the summary table below, you will see there were several positives in May data compared to the corresponding April figures — and those will lead the likes of the Atlanta Fed GDPNow Model to deliver positive revisions for current-quarter GDP expectations. On Friday, that model pegged Q2 2026 GDP at 3.8%, while the New York Fed Staff Nowcasting model was at 2.5%.

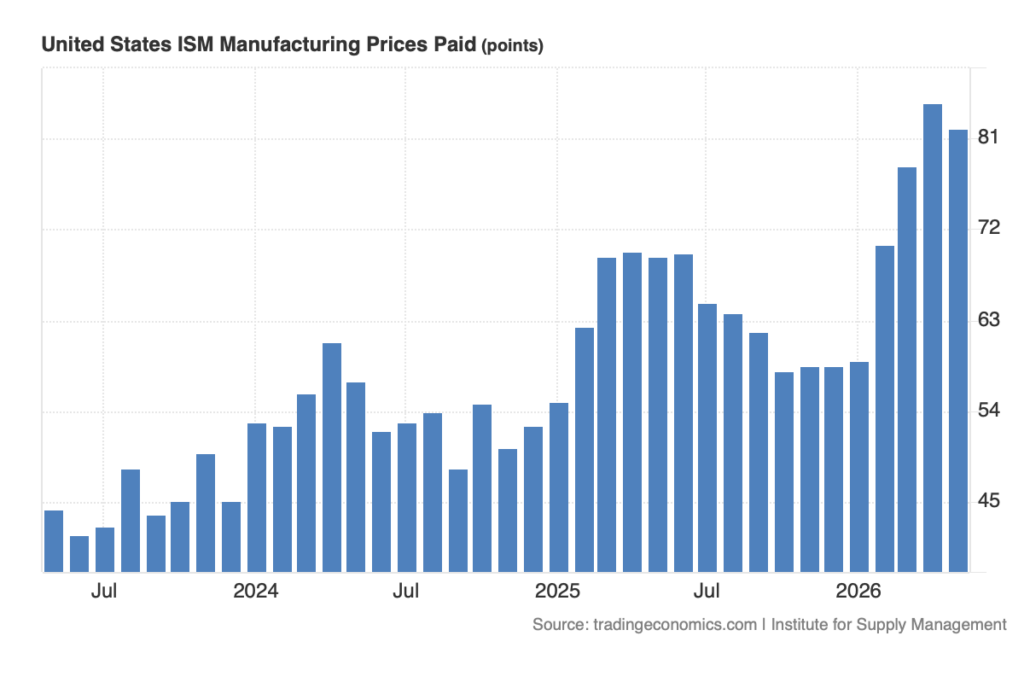

Sticking out like a sore thumb, however, is the Prices index figure of 82.1. Yes, it’s down a smidge from April’s 84.6 but as the chart below clearly depicts, it’s still at very, very elevated levels.

And let’s be sure to connect the dots with S&P Global’s Final May Manufacturing PMI that was also published this morning. Though it confirmed the uptick in manufacturing and increased staffing levels, it called out the following on the inflation front:

Manufacturers’ own charges rose to the greatest extent since September 2022 as they sought to pass through their own higher expenses to clients wherever possible.

Oil prices may have retreated from their highs in recent weeks, but the pain is still flowing through the system. Efforts to hike output prices in May remind us it will take time for those pressures to flow through the economy, and for any relief to do the same.

Circling back to our comments above about being in a holding pattern, we are once again seeing shares of Costco (COST) under pressure. The glass-half-full view is that the shares are getting cheaper and the risk-to-reward tradeoff even better. It’s safe to say, the shares are back on our radar screen. Same goes for new Bullpen resident Dutch Bros (BROS). If you missed that Alert, you can our rationale for adding the shares to the Bullpen here.

More Pro Portfolio:

- Locking in Big Gains and Downgrading This Sleeper Position

- We’re Tracking 29 Signals Across 9 Portfolio’s Investment Themes

- May Monthly Roundup: Sell in May? No Way!

At the time of publication, TheStreet Pro Portfolio was long COST shares.