We're Not in Kansas Anymore Folks ...

... But we're watching out for the Kansas City Fed, and for what's lurking in the shadows of Wall Street.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Rawhide

Keep rollin', rollin', rollin'

Though the streams are swollen

Keep them "dogies" rollin' rawhide

Through rain and wind and weather

Hell-bent for leather

Wishin' my gal was by my side

All the things I'm missin'

Good vittles, love and kissin'

Are waiting at the end of my ride

- Tiomkin, Washington (Frankie Laine), 1958

Two weeks ago, we came off of a tough ending to the week prior and sang with Judas Priest. Some heads certainly did roll. A week later, Dirty Harry asked us if we felt lucky. Well, he did, and apparently, we did. Last week, both the S&P 500 and Nasdaq Composite, not too many other indexes, but those two "majors" and the Nasdaq 100, which is really a sibling to the majors, posted a sweep.

That's five "up" days in a normal, five-day workweek. It's even better than that. The S&P 500, Nasdaq Composite and Nasdaq 100 have all posted seven consecutive "up" sessions. Futures are lower this morning. I see it. Not by too much. For joy, for joy. What got the ball rolling in the right direction after the short-term oversold lows of two weeks ago was the lousy macro. How could the Fed not head into a cycle of easier money now? How could our central bankers not cut short-term borrowing costs? We're headed into recession, oh my.

A week later stocks kept rallying. Why? Oh, because the macro economic data released had been a bit better than expected. How can we sell stocks if there will be a "soft-landing" or a "Goldilocks" economy? In short, stocks have rallied over the past week and a half, both because we were undeniably headed into recession (Hey, the Sahm Rule, dummies) and the Fed would save us all, and because we were no longer as likely to enter into a period of contracting economic activity. Sounds good? The Fed will shift gears regardless. Something tells me we're not in Kansas anymore. But we are headed to Jackson Hole, Wyoming for the Kansas City Fed's Economic Symposium. Like I said above ... we're coming in hot. More about that recession in a few minutes, gang. We've got something cooking this week that the entire financial media seems to have missed. Which, sad as it is, surprises not a soul.

The Week in Review in Macro

When last week began, the focus was on inflation. On Tuesday, the Bureau of Labor Statistics put July producer prices to the tape. It was all any of us could have wished for. The month-over-month and year-over-year prints for both the headline and the core numbers all showed some cooling since June. In fact, the core consumer price index on a month-over-month basis, showed no growth at all. On Wednesday, the same Bureau of Labor Statistics released July consumer prices. There were no surprises here. The month-over-month and year-over-year prints for both headline and core CPI hit the tape precisely in line with consensus view. The year-over-year prints coincidentally showed a slowing from June as the headline number ran with a "2" handle for the first time since March of 2021, back when Pandora's Box of economic horror had just been opened.

The story gets messy from here. Markets took Wednesday's July retail sales report as strong, when in fact it showed some problems. I tried to explain this in Friday's column. The headline print landed at 1.0% month-over-month which crushed expectations for growth of about 0.4%. Not including autos, the print was still strong at 0.4%. Looking into those sales, though, motor vehicles were hot, as were electronics, appliances and groceries. What was not so hot? Fun was ice cold. The fun index is what I have always called the line item in the report labeled Sporting Goods, Hobbies, Music & Books. This single item best represents in my opinion, what households are willing to spend in a discretionary way, on themselves, on what they like, not what they need. This item printed at -0.7% month-over-month for July and at -6.8% year over year. This tells you all you need to know. People are further behind the eight ball than they have been in a very long time.

Markets simply ignored the Empire State and Philadelphia Fed regional manufacturing surveys for August as they were both shrinking, especially for labor. Markets simply ignored the Fed's July report for Industrial Production and Capacity Utilization, both of which made like a pea rolling off of a table. The markets had what they needed, some semi-cool data on inflation and a retail sales print that at the headline, if one doesn't dig in at all, makes the consumer seem healthy. I mean heck, why pay for the necessities of life with cash when you can borrow through a revolving line of credit at an exorbitant rate? Only a really aggressive and healthy consumer would do that right? Not some foolish mortal trying to hide a declining household standard of living from the little ones. Nope, not that guy or gal.

The GDP Game

On Friday, the Atlanta Fed revised its GDPNow model for the third quarter down to growth of 2.0% (q/q, SAAR) from 2.4%. The model had started the week at growth of 2.9%. Among other central banks running close to real-time GDP models for the current quarter, the New York Fed has third-quarter humming along at +1.84%, the Cleveland Fed shows growth of 1.6%, and the St. Louis Fed shows growth of 1.3%. The St. Louis Fed was the most accurate among the four for the first quarter, while Atlanta was the most accurate for the second quarter. The Bureau of Economic Analysis will revise the initial second-quarter gross domestic product estimate of 2.8% on Thursday Aug. 29. Remember, we have not yet seen the second quarter real gross domestic income, and you do need two to tango. If GDP and GDI are not close, you know the math is wrong somewhere and for the full year of 2023, the two were not close at all.

Marketplace

Where we've been is interesting. What exactly is being priced in is the stuff of fantasy. Or is it? Goldilocks tried every plate until the porridge was "just right." Is the market seeking out its sweet spot? Or is the market just squeezing out the shorts, before headed back for new lows? Hard to tell. I mean even if the central bank goes into "easy money" mode, if the economy is not ready to act on that increased liquidity, then we'll have to wait and see.

Remember when the Federal Open Market Committee first took inflation on and started raising rates? We all debated on how long the time lag might be between action and quantifiable results. Well, that hitter can swing from both sides of the plate. So, just because the Fed reduces its target for the Fed Funds Rate by a half-percentage point or three-quarters point by year's end, that won't mean diddly to the head of household who loses his or her main line of income in a corporate headcount cut, will it?

Here, by the way, are the numbers:

- The S&P 500 gained 0.24% on Friday to close the week up 2.94%.

- The Nasdaq Composite gained 0.21% on Friday to close the week up 5.29%.

- The Nasdaq 100 gained 0.09% on Friday to close the week up 5.38%.

- The Russell 2000 gained 0.3% on Friday to close the week up 2.93%.

- The S&P Small Cap 600 gained 0.25% on Friday to close the week up 2.55%.

- The S&P Mid Cap 400 gained 0.08% on Friday to close the week up 2.58%.

- The Dow Transports gained 0.47% on Friday to close the week up 2.21%.

- The Philly Semiconductor Index gave up 0.06% on Friday to close the week up 9.78%.

- The KBW Bank Index gained 1.13% on Friday to close the week up 3.86%.

The Ballroom Blitz

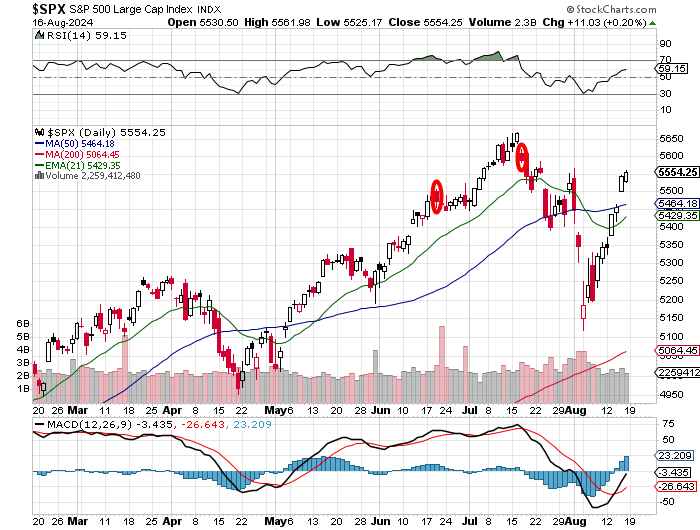

Readers will see that not only did the S&P 500 fill the second of those two early August gaps last week, but the index took back its 21-day exponential moving average, bringing swing traders online and then its 50-day simple moving average like a hot knife through butter. This forced portfolio managers who had raced each other only two weeks ago in a desperate effort to hit whatever bids had not been canceled, to pay up in order to increase long-side exposure.

Relative strength has improved nicely and the daily moving average convergence divergence indicator went from being cheap horror movie material to looking sharply bullish in a hurry. I'll tell you what: This index fails to hold these levels, a lot of year-end bonuses will go right out the window.

The Nasdaq Composite has accomplished just about everything that the S&P 500 has over the past two weeks. That's with the exception of going through its 50-day SMA like a hot knife through butter. This index has not yet cleared that hurdle. This week's work? Recipe for disaster? So frantically hectic, it was electric.... the ballroom blitz. (Sweet, 1974)

Earnings & Valuation

According to FactSet, for the second quarter, with 93% of companies having already reported, the S&P 500 is sporting earnings growth of 10.9% on revenue growth of 5.2%. That's down from 11.5% on 5.3% a couple of weeks ago. So far, 79% of S&P 500 companies reporting have posted earnings beats while 60% have reported revenue beats. Interestingly, earnings growth projections for the third quarter have been coming in quite rapidly for a while and continue to do so. FactSet now sees third quarter earnings growth of 5.2% down from 6.1% two weeks ago and down from 8.1% at the start of the quarter, with revenue growth of 4.9%. For the full year, projections are for earnings growth of 10.1%, down from 10.9% two weeks ago on revenue growth of 5.1%. For the second quarter, four sectors are running at 15% earnings growth or greater. Those sectors would be Utilities (+20%), Technology (+18.9%), Financials (+17.5%) and Health Care (+17%). There are two sectors running in a state of earnings contraction for the quarter. Those groups would be the Industrials (-0.5%) and Materials (-8.8%). Incredibly, the Communication Services Sector is now running at 4.5% earnings growth for the second quarter after ending the calendar quarter with estimates for growth of 18.5%. The S&P 500 closed out the past week trading at 21 times forward looking earnings, up from 20.2 times a week ago. That was the kind of week it was. This remains well above both the five-year average (19.4 times) and the ten-year average (17.9 times) for the index.

The Main Event

This will not be an especially busy week for earnings releases. There will be a few headline worthy corporations posting results and issuing guidance. Among those will be Palo Alto Networks PANW on Monday afternoon, Lowe's (LOW) on Tuesday morning, and Macy's M, Target TGT, and TJX TJX all on Wednesday morning. Snowflake SNOW and Zoom Video ZM will report on Wednesday evening followed by Workday WDAY on Thursday evening. That's about it. The macro calendar is even thinner. What will matter this week, will be the economic symposium at Jackson Hole, Wyoming this Wednesday through Friday hosted by the Kansas City Fed. Yeah, there will be white papers, guest speakers and a whole lot of nothing to the folks pushing the buttons on Wall Street. Fed Chair Jerome Powell speaks on Friday at 10 a.m. ET. It is here that the street expects Powell to pave the road to a rate cut on Sept. 18 that could most probably only be disrupted at this point by an extraordinarily strong August jobs report on Sept. 6. That leads us to our last and potentially most important segment of this column.

Lurking in the Shadows

For how long, you tell me, have I been beating up on the financial media for covering GDP over GDI or for reporting only the strongest labor market "guesstimates" and barely covering the BLS quarterly BED reports that have warned us that employment data had been grossly overstated since the start of 2023. The media wanted no part of these less optimistic numbers that suggested the economy might not really be roaring after all.

I hate being right on these matters all the time while economists with more impressive academic backgrounds stumble and bumble around. (No, I don't. I actually love being more accurate than these clowns.) Such is life.

This Wednesday, at 10 a.m. ET, the Bureau of Labor Statistics will reveal the preliminary estimate for the upcoming annual benchmark revision to the establishment survey data for the period covering April 2023 to March 2024. It is anticipated by many that as many as, or maybe more than one million fewer jobs were actually created during that period than were reported in the monthly non-farm payrolls numbers.

Are we already in, or are we close to recession? On Wednesday, you may find out more than you will on Friday. (Again, we have to trust these numbers to be honest) If so, then how far back do they backdate the onset of this economic contraction? Maybe I'll be wrong, and we'll find out the Establishment Survey numbers were correct all along? Or even close to correct. As an American, I have to root for that outcome. As a realist, I think that not too likely.

Economics (All Times Eastern)

8:55 a.m. - CB Leading Indicators (July): Expecting -0.4% m/m, Last -0.2% m/m.

The Fed (All Times Eastern)

9:15 a.m. - Speaker: Reserve Board Gov. Christopher Waller.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: EL (.25)

After the Close: PANW (1.41)

At the time of publication, Guilfoyle was long TJX equity.