Was Last Week a Winner? Well, That Depends ...

Let's take stock of the week that saw a wild jobs report and its ripple effects, and see where we're headed now.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A winning week? That depends on what one was trading. U.S. equities closed out the past week on a note of strength, as green lit the screen on Friday. That upward push on Friday permitted the major equity indexes (but not so much the mid-majors) to post winning weeks, even if just barely and completely changed the nature of the week on the whole. Friday's equity market rally, which came in response to a significantly stronger than expected September employment report that had just the opposite effect on other financial markets.

The positive jobs report forced the likelihood of a half-point cut to the Fed Funds rate much lower. This forced U.S. dollar valuations higher, while forcing commodities traders to take profits in gold and silver, and bond traders to sell U.S. Treasury debt securities. Interestingly, crude oil rallied sharply last week, despite dollar strength. The U.S. Ten Year Note went out on Friday yielding 3.98% after paying as little as 3.73% on Tuesday. Early on Monday morning, I have seen U.S. Ten Year paper pay more than 4.01%. The U.S. Two Year Note has been selling off even more sharply as the spread between the two has narrowed significantly. This morning, I saw a Two Year Note that yields an even 4% after going out on Friday at 3.93% and paying just 3.61% last Tuesday.

Of course, Friday's labor market report was not the only major news event impacting markets. On Tuesday, you may have noticed Treasury yields at bottoms for the week. That was the day that Iran's armed forces launched as many as 200 ballistic missiles at Israel in retaliation for killing the leader of the Hezbollah terrorist organization in Lebanon. Markets remain on a "wait and see" setting this week, watching for a potential Israeli response to Iran's largely ineffective attack.

On a positive note, U.S. dockworkers along the Atlantic and Gulf coasts returned to work, after their union, the International Longshoremen's Association reached a tentative agreement with their employers that included a 62% pay increase over six years. Speaking of strikes, it is believed that the union representing 33,000 striking Boeing BA machinists will return to the negotiating table as soon as later today after Boeing had cut off health benefits for its idle workers.

On Jobs ...

The Bureau of Labor Statistics released the results of its two monthly employment surveys on Friday morning. This report not only ran solid from top to bottom, but was difficult to find holes in, unless one goes to the raw data. The raw data was not nearly as positive, and we can argue about seasonal adjustments all we want and the Current Employment Statistics net birth-death model that we suspect has been incorrect for almost two years all we want. The fact is that the financial media takes these adjusted results at face value, and, because they do, the keyword reading algorithms that control financial market price discovery do.

That's what matters to us as traders and investors. It's what the algos do that will decide for us which way the wind blows. The truth is something nice to debate, but that is not what makes money in the short- to medium-term for sure and maybe even in the long run, as well. This does, or at least should, force economists to ask some serious questions. Recently, the Bureau of Economic Analysis revised all of its data for both gross domestic product and gross domestic income going back to 2022.

So ... if the economy is as strong, and has been as strong, as we are being told, and if the employment situation is as strong as we are being told, then why, with consumer level inflation still running above the Fed's 2% target, is the Federal Open Market Committee easing monetary policy?

It is no small wonder that Fed Chair Jerome Powell appeared unable to explain the aggressive rate cut made on Sept. 18 from an economic perspective. It is also no small wonder that his army of public speakers that have hit the circuit since Sept. 18 have been unable to explain why it's so important to ease monetary policy aggressively with year-over-year inflation still above target, but more importantly ... with cumulative inflation over the past four years still averaging more than 5% per year.

More Fun With Fed Funds

All that taken in, Fed Funds futures markets and Treasury markets have reacted sharply to the improved macroeconomic data. Over the past week, the argument for the Nov. 7 FOMC meeting have gone from a majority probability for a quarter-point rate cut and a significant minority probability for a half-point rate cut to a dominant likelihood (93%) for a quarter-point rate cut and 7% chance for no rate cut at all.

In fact, by year's end, these markets are pricing in a half-point worth of rate cuts, down from three-quarter points a couple of days ago. And get this: This morning, they are pricing in a 74% probability for a half-point worth of cuts over the balance of 2024, with a 13% shot at three-quarters point and a 13% shot at quarter-point. That's a far cry from a week or two ago.

The GDP Game

Last week, the Atlanta Fed revised its GDPNow model for the third quarter down to seasonally adjusted quarter-over-quarter growth of 2.5% from 3.1%. Among other central banks running close to real-time GDP models for the current quarter, the New York Fed revised its third-quarter estimate up to 3.06% from 2.99%, so they are now even more optimistic than Atlanta. The Cleveland Fed left its third-quarter estimate at growth of 1.45%, while the St. Louis Fed took its estimate for the third quarter up to growth of 1.70% from 1.41%, which separates them from Cleveland. Suddenly, the Fed models all seem to be running individually and are no longer divided into two camps.

Charting the Marketplace

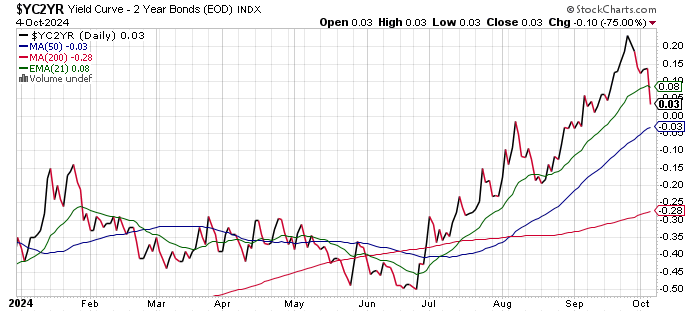

Interestingly, while the yield spread between the U.S. Ten- and Two-Year Notes narrowed from 19-basis points to 3-basis points and a potential re-inversion looms....

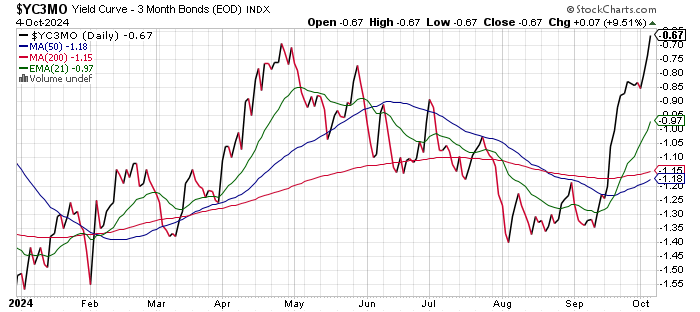

... the spread between the yields of the US Ten Year Note and US Three Month T-Bill have continued to "steepen" if that's the right word and have made further progress towards eventually "un-inverting," or normalizing. This spread moved from -84 basis points to -67 basis points in one week's time.

As for U.S. equities last week, you'll see that nice pop on Friday that left most of our favorite indexes close enough to "unchanged" for the week.

- The S&P 500 gained 0.9% on Friday to close the week up 0.22%.

The Nasdaq Composite gained 1.22% on Friday to close the week up 0.1%.

- The Nasdaq 100 gained 1.22% on Friday to close the week up 0.13%.

- The Russell 2000 gained 1.5% on Friday, but still closed the week down 0.54%.

- The S&P Small Cap 600 gained 1.56% on Friday to close the week down 0.75%.

- The S&P Mid Cap 400 gained 0.97% on Friday to close the week down just 0.03%.

- The Dow Transports gained 0.44% on Friday, to close the week down 2.3%.

- The Philly Semiconductors gained 1.59% on Friday and still closed the week down 0.2%.

- The KBW Bank Index gained 2.54% on Friday to close the week up 0.68%.

On Friday, nine of the 11 S&P sector SPDR exchange-traded funds closed in the green, with the Financials XLF out in front at +1.69% The Financials were one of four sector funds to gain more than 1%. For the week, just five of the 11 S&P sector SPDR exchange-traded funds closed in the green, led by Energy XLE, which soared 6.87% on geopolitical concerns. Including Energy, three of these funds gained more than 1% for the week, while four closed more than 1% lower. Staples XLP and Materials XLB led to the downside.

Earnings

On Friday, Both JP Morgan JPM and Wells Fargo WFC will report third-quarter earnings, and that will unofficially kick off the third-quarter earnings season for all. According to FactSet, which is my earnings-related "go-to", for the third quarter, consensus for S&P 500 earnings to have grown 4.2% year over year, down from 4.9% a few weeks ago, on revenue growth of 4.7%. For the full year, earnings growth is now seen at 9.8%, down from 10.2% a few weeks ago, on revenue growth of 5%.

For the third quarter, double-digit earnings growth is expected from the Technology, Health Care and Communication Services sectors, while the Financials, Materials and Energy sectors are all expected to post year over year contraction.

The S&P 500 goes into the week trading at 21.4-times forward looking earnings, which is well above the five- and 10-year averages for the index of 19.5 and 18 times, respectively. Technology remains the most highly valued sector at 28.4-times forward looking earnings, while the lowest valuation is being assigned to Energy at 13.5 times.

The Week Ahead

Readers may find this difficult to believe, but the kickoff of third-quarter earnings season is not at the top of what's important this week. For starters, another major hurricane (Milton) bears down on the Floridan peninsula from the Gulf of Mexico and could severely impact some areas still not close to having recovered from Hurricane Helene less than two weeks ago.

On the macro side, the September consumer price index and producer price index will hit the tape this Thursday and Friday respectively, while the Fed Minutes of the last meeting will be published this Wednesday. Those Minutes will be released, of course, amid another blizzard of Fed speakers, though there seems to be no one at the moment, able to send a coherent message on policy that makes economic sense.

I think the most important items this week will be on the corporate side, but not earnings-related, and from the semiconductor industry in particular. As you'll recall, Nvidia NVDA CEO Jensen Huang told us last week that demand for his new Blackwell architecture AI-chips was "insane." One must realize that Huang, while a superstar executive, still has a narrative to sell. Not knocking, I am a shareholder.

That said, on Friday, the Semiconductor Industry Association announced that semiconductor sales were up 21% year over year in August. On Saturday, Foxconn posted record Q3 growth. Take that how you want, but Foxconn is Apple's AAPL largest iPhone assembler and also a supplier to Nvidia as well.

Then there are this week's events. Nvidia will hold the firm's AI Summitt from today (Monday) through Wednesday in Washington. The focus will be on AI to drive breakthroughs in healthcare, cybersecurity, robotics and industrial digitization. Then on Thursday, Advanced Micro Devices AMD will hold its Advancing AI event. Think NVDA will fall on its face? Me, neither. Think Lisa Su will rise to the challenge presented by Jensen Huang? Me, too.

Economics (All Times Eastern)

3:00 p.m. - Consumer Credit (Aug): Last $25.45B.

The Fed (All Times Eastern)

1:00 - Speaker: Reserve Board Gov. Michelle Bowman.

1:50 - Speaker: Minneapolis Fed Pres. Neel Kashkari.

6:00 - Speaker: Atlanta Fed Pres. Raphael Bostic.

6:30 - Speaker: St. Louis Fed Pres. Alberto Musalem.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was ong WFC, NVDA, AMD equity.