Wall Street Comes Back Down to Earth

Now we can tell whether the 'Trump Bump' is an actual change in trend or an algorithmic outlier. Also, let's check on Treasuries and a new Berkshire-based ETF.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We all knew that we were in need of it. What "it" is, was an honest "down" day for equities, so that we could truly form a technical base of consolidation. This would be so we could ultimately discover whether the post-election "Trump Bump" was just an algorithmic keyword reading reaction, or an actual change in trend that had turned around some pre-election selling pressure. Can the recent rally be built upon?

Well, at least now we can find out. Should this downward or sideways move take a few days, is not a problem. We actually like to see separation between the actual change in trend and a bona fide confirmation of that move. This way, the change in trend is not seen as one big move taking several days. That can produce misjudgments that ultimately cost investors and traders money.

Treasury Marketplace

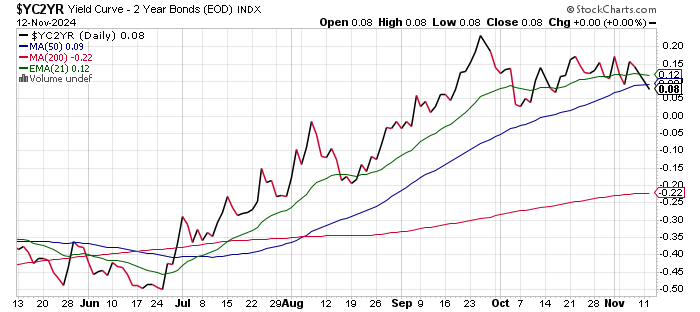

U.S. Treasury debt markets came back from the Veterans Day holiday and showed some weakness on Tuesday. The yield for the U.S. Ten Year Note soared 13-basis points to 4.43%, while the Two-Year Note paid 4.35% by day's end, up 9-basis points. The spread between the two has remained positive since early September:

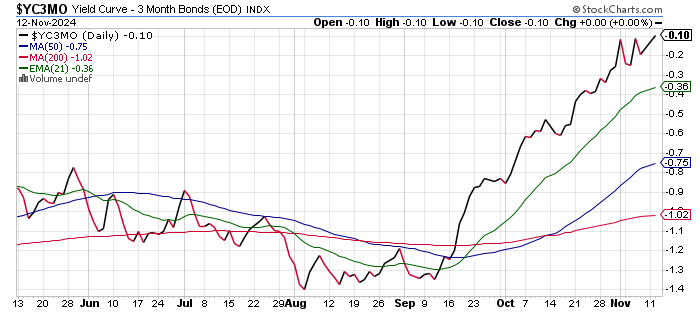

Meanwhile, after Tuesday's weak demand for U.S. Treasuries from the belly of the yield curve on out to the long end, the more important spread between the yields of that same U.S. Ten Year Note and the Three-Month T-Bill is making another attempt at normalization, or as some like to call it ... "un-inversion."

While Treasury yields pushed higher, so did the U.S. Dollar Index. The "dixie" moved above 106 on Tuesday for the first time since early this past summer. As I have been writing, we believe that consumer-level inflation may have bottomed in September. We'll find out more about that later this morning as the Bureau of Labor Statistics releases its data for October consumer price index.

Remember, the Fed is easing policy ahead of hitting its target. It may talk the good game, but as enabler to the fiscal recklessness over the past three years and really since 1913, it is imperative to the Fed to make servicing the federal debt-load more affordable and adding to that debt-load less prohibitive. Aiding in improving the lot of lower- and middle-class Americans in being able to afford a certain lifestyle for their household is not, I repeat, not the Fed's primary objective.

A more highly valued U.S. dollar can help here. So can a normalized slope of the Treasury yield curve. I understand that higher interest rates the further out to maturity we go, may slow nominal economic activity, but would also slow inflation. Inflation has already slowed down, say the economics professor and the politically biased. That's fantastic. The fact that Joe and Jane Doe cannot afford their family's lives anymore even though they both work more than full-time never dawns on these people.

Equities

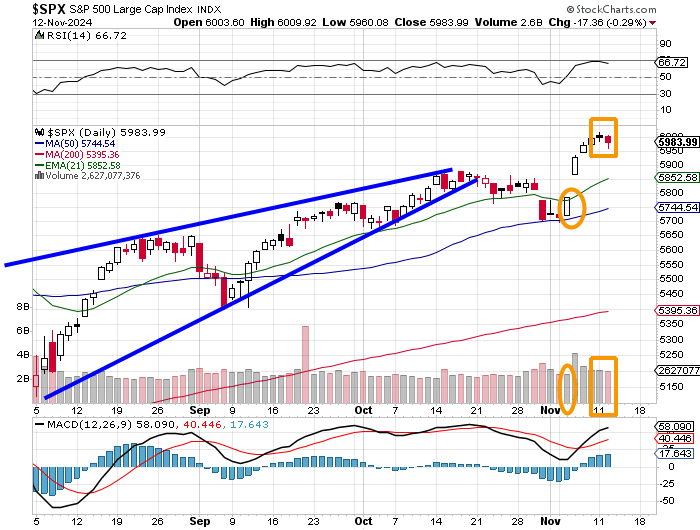

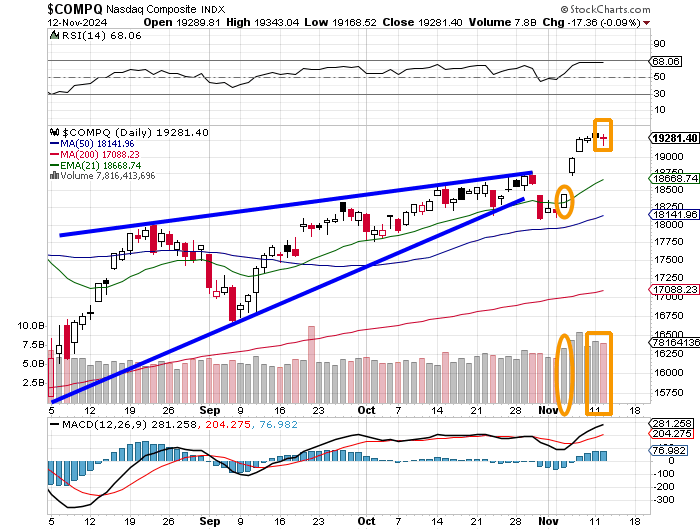

The S&P 500 gave up 0.29% on Tuesday as the Nasdaq Composite gave back 0.09%. Not much of a "down" day if you ask me, but a red candle, nonetheless. It was for both, their first red candle day since Nov. 4, the day ahead of the national election. The one-day outperformance of the smaller cap indexes reversed on Tuesday big-time. The Russell 2000 surrendered 1.77%, as the S&P 600 and S&P 400 gave up 1.54% and 1.01% respectively. The Dow Transports were also taken out to the woodshed (-1.04%) as truckers, maritime shippers and airlines were all slapped around.

A mere three of the 11 S&P sector SPDR exchange-traded funds closed out Tuesday in the green, with growth at the forefront. Communication Services XLC and Technology XLK led the way, as five of these funds gave up more than 1% for the session. The laggards were the Materials XLB and Health Care XLV sector funds.

Breadth was weak, which would be expected. Losers beat winners at the NYSE by a rough 4 to 1 and at the Nasdaq by about 11 to 5. Advancing volume took a fairly stout 48.3% share of composite Nasdaq-listed trade and a paltry 23.8% of composite NYSE-listed activity.

What leads me to believe, at least for now, that this may be the start of a period of consolidation and not another reversal of trend, is the aggregate trading volume. It just was not there. Aggregate trade was down 3.4% on a day over day basis across Nasdaq-listed securities and down 2.1% day over day for their NYSE-listed counterparts.

Do You See What I See?

The S&P 500:

The Nasdaq Composite:

Double the Berkshire Fun

Anyone else notice the story reported by Bloomberg News regarding Berkshire Hathaway Class B BRK.B shares? Apparently, Kiwoom Securities, which is one of South Korea's largest retail brokers, has gotten together with Tidal Investments out of Milwaukee to form an exchange-traded fund that will be designed to produce twice the daily performance of Berkshire Hathaway, according to a regulatory filing and reported on by Bloomberg, which is where I read about it.

As is explained in the article, Warren Buffet has a significant following in South Korea. Individual investors in that nation hold more than $800 million worth of Berkshire's Class A and Class B shares. While I have never been a fan of leveraged ETFs, and I don't think Warren Buffet is a fan of ETFs of any kind. He once referred to them as "financial weapons of mass destruction." I expect to remain long BRK.B, as I have been long for years not months. As for the 2x ETF? Probably not my cup of tea.

To the Moon!

I am sure that most of my loyal readership saw the release of Rocket Lab USA RKLB earnings last night and the euphoric market response. I will be releasing a separate piece solely devoted to RKLB this morning.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.81%.

07:00 - MBA Mortgage Applications (Weekly): Last -10.8% w/w.

08:30 - CPI (Oct): Expecting 0.3% m/m, Last 0.3% m/m.

08:30 - Core CPI (Oct): Expecting 0.2% m/m, Last 0.2% m/m.

08:30 - CPI (Oct): Expecting 2.6% y/y, Last 2.4% y/y.

08:30 - Core CPI (Oct): Expecting 3.3% y/y, Last 3.3% y/y.

08:55 - Redbook (Weekly): Last 6.0% y/y.

2:00 p.m. - Federal Budget Statement (Oct): Last $64B.

4:30 - API Oil Inventories (Weekly): Last +3.12M.

The Fed (All Times Eastern)

09:45 - Speaker: Dallas Fed Pres. Lorie Logan.

1:00 p.m. - Speaker: St. Louis Fed Pres. Alberto Musalem.

1:30 p.m. - Speaker: Kansas City Fed Pres. Jeffrey Schmid.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: SHOP (.27)

After the Close: CSCO (.87)

At the time of publication, Guilfoyle was long BRK.B, RKLB equity.