Unrealistic Soft Landing, Economy, Fed in a Tough Spot, Lots of Earnings, Week Ahead

This week will be about the Fed's FOMC policy meeting that will culminate on Wednesday afternoon.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Lost in a Roman wilderness of pain

And all the children are insane

All the children are insane

Waiting for the summer rain, yeah

There's danger on the edge of town

Ride the king's highway, baby

Weird scenes inside the gold mine

Ride the highway west, baby

- "The End" Densmore, Morrison, Krieger, Manzarek (The Doors), 1967

What Is and What Shall Be

Evolution. The young girl with golden hair, oddly living with a family of bears (?) had reached out for some more. For more of what was, what had been "just right." How was she to know that what had sated her thirst, and her hunger had been finite in its supply? Perhaps there is more where that came from. Perhaps we were fools to think of such things as "soft landings" as ever being realistic.

Perhaps we were playing the role of mere jesters in the court of folly, when we almost believed that inflation could be tamed with nearly painless adjustments made to the extreme short end of the yield curve. All as labor markets seemed invincible in their ability to adapt. Perhaps, my friends... All is well or almost well, and what we behold to our immediate front is to be forgotten, once the missing cobblestones are replaced, and then the road paved over. How do we know if Pandora laughs from afar? Has the box been opened? Is that even laughter?

Or does someone weep for the unknown and all that is now unknowable.

You Heard the Man...

JP Morgan JPM CEO Jamie Dimon wrote his annual letter to shareholders almost three weeks ago. Readers may remember that he wrote... "Equity values, by most measures, are at the high end of the valuation range, and credit spreads are extremely tight. These markets seem to be pricing in at a 70% to 80% chance of a soft landing — modest growth along with declining inflation and interest rates. I believe the odds are a lot lower than that."

Speaking with the Wall Street Journal's Emma Tucker last week, Dimon expounded on that thought a little bit... “When I look at the range of possible outcomes, you can have that soft landing, I’m a little more worried it may not be so soft and inflation may not quite go away as people expect. I’m not talking about this year — I’m talking about 2025 or 2026.”

There is a real chance that the FOMC stopped short of what would have been appropriately restrictive short-term rates when the target for the Fed Funds Rate hit 5.25% to 5.5%. Should they have gone another 25 or 50 basis points? Would that have stopped consumer level inflation from rekindling as it has in 2024?

The truth is and we know it darned well, that the money supply and the monetary base are still too large. Even now. They will be, quite possibly forever. For-freaking-ever. What fools, we mortals be? To think that a nation, the largest economy on the planet, could spend its way into a drunken recklessness and suffer no lasting consequence. Congress knew better, or at least they should have. No excuses for all of that moola, and even worse, all of that debt. Now, the children wait for the summer rain.

Tug of War

Quite possibly all of that fear mongering was for good reason. We just do not really know. The Fed is now, as the FOMC steams into this week's policy meeting, in a tough spot. It is true that the first quarter GDP print does not really look as bad throughout as it does at the headline, but the fact is that growth of 1.6% (q/q, SAAR) is a deceleration.

Within that first estimate for first quarter economic growth, we see that the federal government paused defense spending, and inventory building took a breather as well. Imports soared as Exports slowed. That could reflect improving demand. Still, that is more cash leaving the ecosystem than being brought in. These are the things that negatively impact GDP performance. Personal consumption was not really strong, but strong enough. Only for services, however. Purchases of goods contracted.

Why do we say that the Fed could now be in a tough spot? On Thursday, quarterly headline PCE inflation printed at 3.4% year over year, well above the expectation for 2.9% and far above Q4's pace of 1.8%. Yikes. At the core? Even worse. Core PCE for the quarter landed at growth of 3.7%, above expectations for 3.4%, way above Q4's 2% pace, and simply the hottest quarterly core inflation print since Q2 of last year.

On Friday, we got monthly data for PCE inflation for March. Everything kind of hit where it was supposed to, or just a touch on the warm side. Headline March PCE printed at monthly growth of 0.3% (as expected) and annual growth of 2.7%. That was above expectations for growth of 2.6% and up from February's 2.5%. At the core, March PCE inflation hit the tape at month over month growth of 0.3% (again, as expected) and year over year growth of 2.8%. That was in line with February and well above what was the consensus view for 2.6%.

What now? The FOMC obviously cannot cut rates anytime soon with inflation reigniting, even with economic growth, while not yet in crisis, overtly slowing down. There are some signs of a decreased demand for labor everywhere we look in 2024. It certainly is not a washout, though. While the vast majority of recent hires have been part-timers and many full-time laborers have been downgraded to part-time status by their employers, initial jobless claims have more or less flatlined. Hordes of individuals have not been thrown to the wolves.

One must ask though... if Jamie Dimon is accurate in what he sees a dark potential for, what will the FOMC do, if the soft landing of Goldilocks does in fact turn into Pandora's recession? What if the demand for labor does hit a wall, and then recedes... while inflation continues to accelerate thanks to the liquid slosh overlaid onto an over-indebted nation?

Marketplace

Treasury yields worked their way higher last week, as traders pressured US sovereign debt across the curve from the six-month T-Bill all the way out to the thirty-year bond. The US Ten Year Note went out on Friday yielding 4.67% after having started the year paying 3.94%. As for the US Two Year Note, that series ended last week yielding an even 5% after starting 2024 at 4.33%. This morning, I saw the US Dollar Index hovering around the 106 level. The "dixie" started 2024 just above 102.

The major equity indexes closed up for the week, snapping three- and four-week losing streaks for the S&P, 500 and the Nasdaq Composite, respectively. The week we left behind was actually quite volatile, as the "Magnificent Seven" once again, became the driving force behind market activity.

First, Tesla TSLA cheered markets, by apparently changing the trajectory of their business, only to be followed by forward guidance provided by Meta Platforms META that scared the stuffing out of shareholders concerning CapEx spending on an AI-driven future. That was all put to rest, at least for the time being, on Friday as both Microsoft MSFT and Alphabet (GOOG) demonstrated that the up-spend on AI can indeed be monetized.

For the week, the S&P 500 gained 2.67%, to stand up 6.92% year to date. The Nasdaq Composite shot 4.23% higher last week, to close up 6.11% for the year. How are the small-caps? The Russell 2000 was able to rise 2.79% for the week and is now down just 1.24% for 2024.

How about the specialty indexes? Well, check this out. The Dow Transports underperformed, but still managed a gain of 0.58% for the week, and now stand down 4.58% for 2024. The KBW Banks gained 2.6% last week and are up 6.93% year to date, but the semis are still where its at. The Philadelphia Semiconductor Index gained "just" 9.95% last week and is now up 13.41% for the year. Nvidia NVDA, as you might have guessed, led the way, up 15.14% for the week.

All eleven S&P sector SPDR ETFs closed out last week in the green, with Technology XLK and the Discretionaries XLY up 3.79% and 3.62%, respectively. Seven of these funds gained at least 1% last week, but there was no clear move into one type of sector. Performance in growth was bifurcated as Tech soared, but Communication Services XLC lagged thanks to Meta. Cyclicals were also found at both the top and bottom of the weekly performance tables, while defensive sectors were packed into the middle.

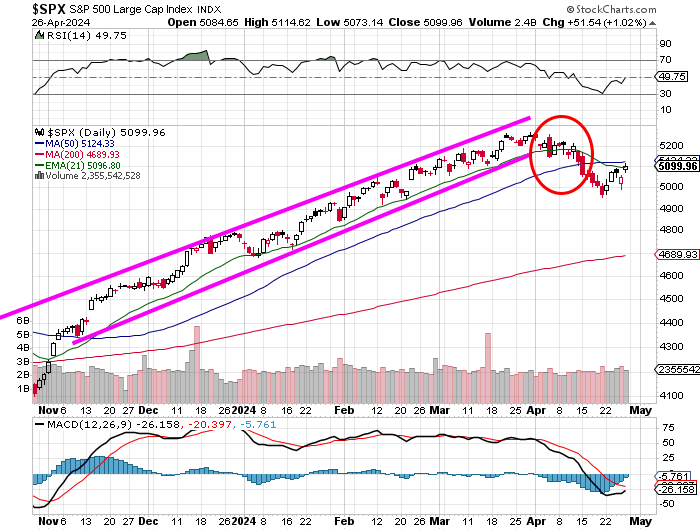

Change in Trend?

We nailed the change in trend on the downside. Now we must ask... Have we already seen another change in trend, as in an upward turn? I would move really slowly in making that determination. Why? Let's take a look.

See the S&P 500 trading volume? What days stick out to you? Red candle days. Very good. There has been a lot more conviction in the selloffs than there has been in the rallies. Even last week, when there was but one selloff. Sure, Relative strength has moved back up towards a neutral reading.

The daily MACD (moving average convergence divergence) looks a lot better too. The histogram of the 9-day EMA (exponential moving average) is so close to breaking above zero, while the 12-day EMA looks about to (bullishly) cross above the 26-day EMA.

However, away from the trading volume, something else is also cautionary in the tale it tells. Do you see it? See that thin blue line that seems to have stopped Friday's rally in its tracks? That's the 50-day SMA (simple moving average). That line needs to be taken and held before anyone is declaring a change in trend. Comprende?

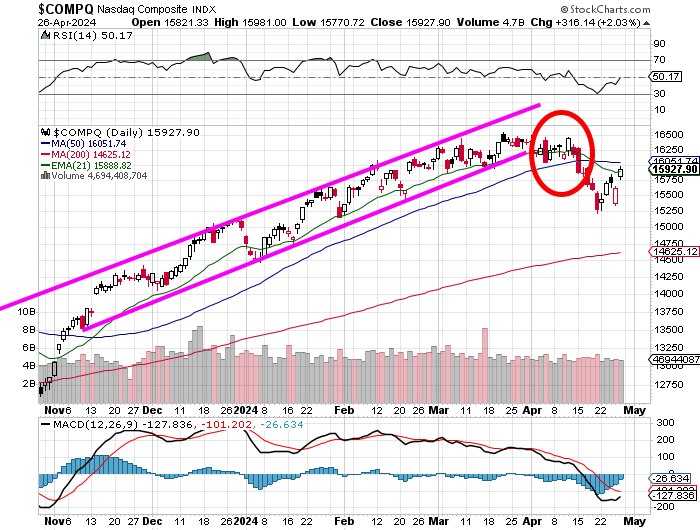

Oh look, the Nasdaq Composite tells the same exact story. From the RSI to the daily MACD to the failure to take the 50-day SMA. One thing is different though. See last week's trading volume? That red candle day on Thursday does not stand out like a sore thumb. If this show does hit the road, it's going to be led by tech. Again.

Earnings

What a difference a week makes!! According to FactSet, which readers know by now, is my earnings-related "go-to", with 46% (up from 14%) of the S&P 500 having reported for the season, first quarter earnings are running at a blended (results & expectations) year over year growth rate of 3.5%, up from just 0.5% a week ago.

Revenue growth is now running at 4.0%, up from last week's 3.5%. For the full calendar year, still according to FactSet, earnings are now seen growing 10.8%, up from 10.7% last week on revenue growth of 5.0%, up from 4.9%.

To this point, Communication Services are running the hottest, at growth of 34.4%, with the Utilities in second place at +23.9%. Three sectors, Materials, Energy, and Health Care are all suffering year over year earnings contractions of greater than 20%.

After all of that, the S&P 500 ended last week trading at 20 times forward looking earnings, up from 19.9% a week ago. This is still above the five-year average of 19.1 times and ten-year average of 17.8 times for the index. However, the S&P 500 was trading at 20.9 times three weeks ago.

The Week Ahead

Let's be honest. This week will be about the Fed's FOMC policy meeting that will culminate on Wednesday afternoon with the official statement and Jerome Powell's press conference. Obviously, there will have to be an attempt made to push out expectations for any rate cuts in 2024.

I don't expect the Fed to go there, but if I ran the Fed, I would not only remain non-committal as far as policy goes, but I would also truly be as open to a rate hike as I would be to a rate cut and I would let the public know what I was thinking. My belief is that if it were not an election year, that this probably should have already been done, especially after GDP appeared to be rather strong for both Q3 and Q4.

There is not a ton of macro on the docket for the week ahead, but what is scheduled will be seen as important. The Treasury Department will project their refunding financing estimates. There will be releases made by the department on both Monday afternoon and Wednesday morning. On Friday morning, the BLS will release the results from their two employment situation focused surveys. Right now, Non-Farm Payrolls are seen at roughly 243K with an unemployment rate of 3.8% and an underemployment rate of 7.3%.

On the corporate side, this will be another heavy week of earnings releases. The Magnificent Seven will send two batters to the plate this week after four members of that group went to the tape last week.

This week you'll hear from 3M MMM, Coca-Cola KO, Eli Lilly LLY, McDonald's MCD, Advanced Micro Devices AMD, and Amazon AMZN just on Tuesday alone. Then on Thursday afternoon, we'll hear from Amgen AMGN, Apple AAPL and Block SQ.

Economics (All Times Eastern)

10:30 -Dallas Fed Manufacturing Index (Apr): Expecting -11, Last -14.4.

15:00 - Treasury refunding Financing Estimates.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DPZ (3.40), ON (1.05), SOFI (.01)

After the Close: FFIV (2.87), MSTR (-.13), NXPI (3.18)

At the time of publication, Stephen Guilfoyle was long SOFI, MSFT, NVDA, LLY, AMD, AMZN equity.