Tom Lee: 3 Reasons the Post-Fed Market Decline Is an Overreaction

We view the magnitude of the equity drop and commensurate surge in yields disproportionate to the FOMC rate decision and press conference.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In today's FS Insight First Word note we discuss why the "hawkish" take by markets from the FOMC ultimately reverses in the next few weeks. There are three reasons, but the most important is the Fed funds YE 2024 is higher by +50bp because growth is raised by +40bp. Wouldn't it be worse if Fed raised its GDP view but did not raise Fed funds?

Please click here to view today's Macro Minute (Duration: 8:54).

----------

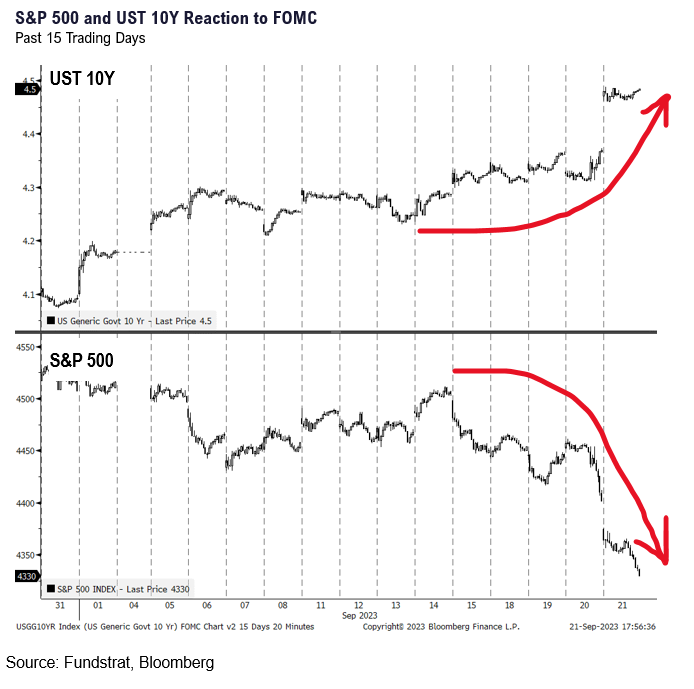

Since the FOMC rate decision (two trading days), the S&P 500 is down -2.5% and down -4% for the month. The markets viewed the September FOMC rate decision (and summary economic projections, or SEP) hawkishly. Stocks have been under pressure the entire month as US 10-yr yields relentlessly marched higher from 4.0% to nearly 4.5%. Unfortunately, our expectation for equities to gain post-FOMC did not materialize.

* For reasons we discuss below, we view the magnitude of the equity decline and commensurate surge in yields disproportionate to the FOMC rate decision and press conference. Understandably, this sounds like a tall order. After all, yields on the US Treasuries surged to multi-decade highs yesterday. So the fixed income market reacted strongly to the FOMC.

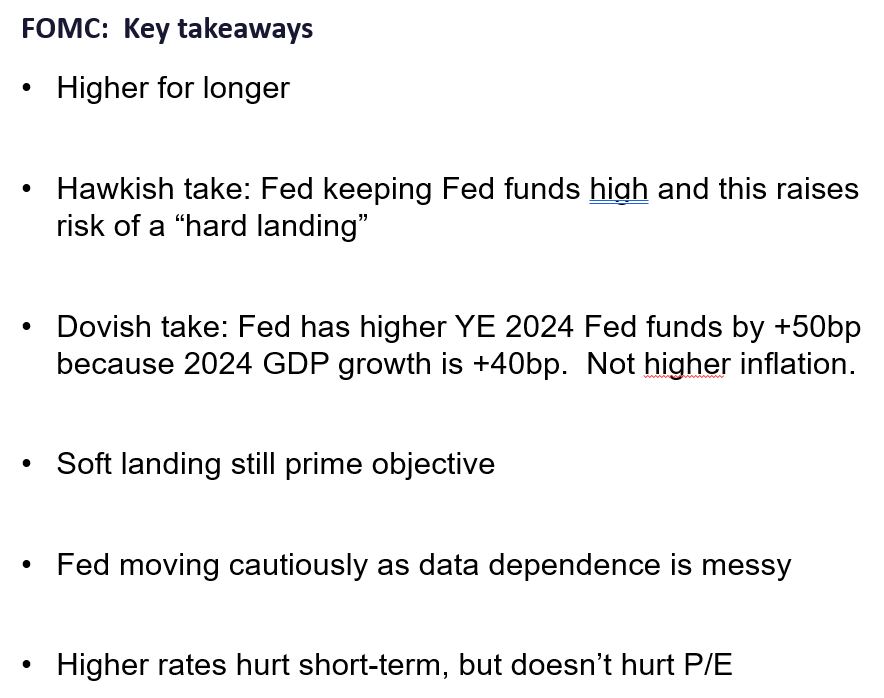

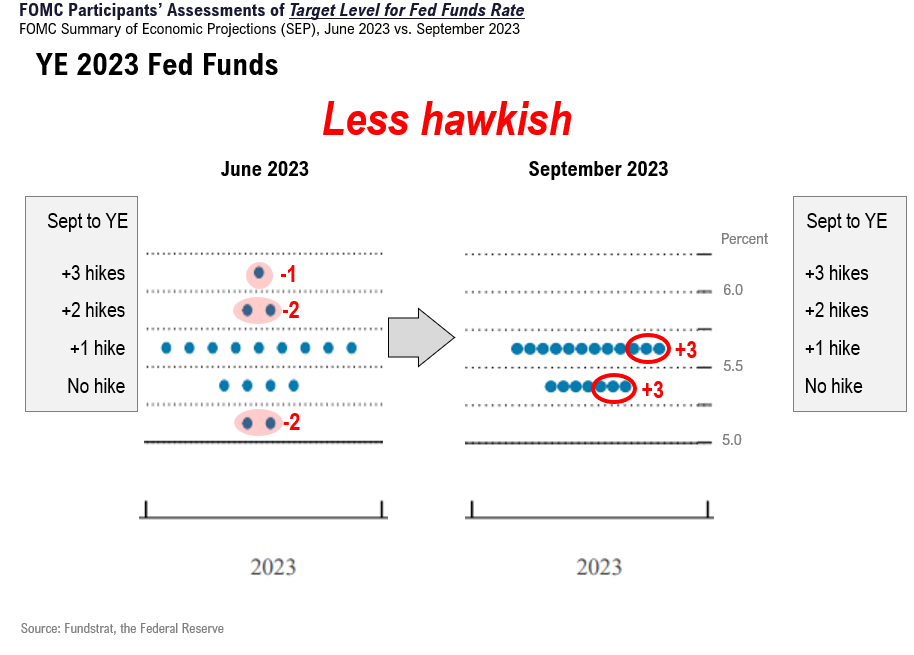

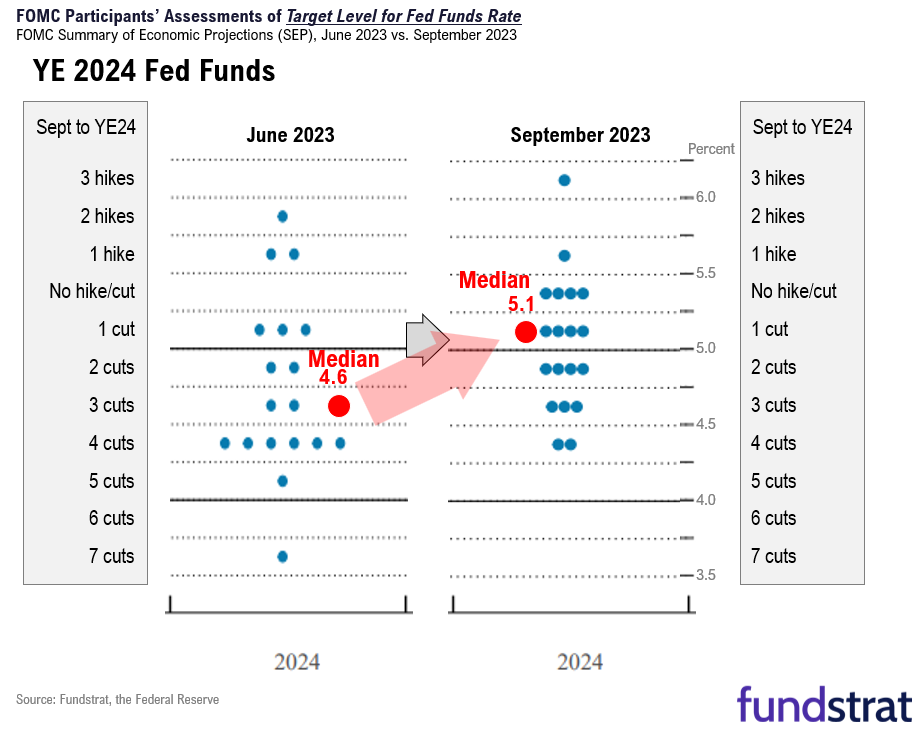

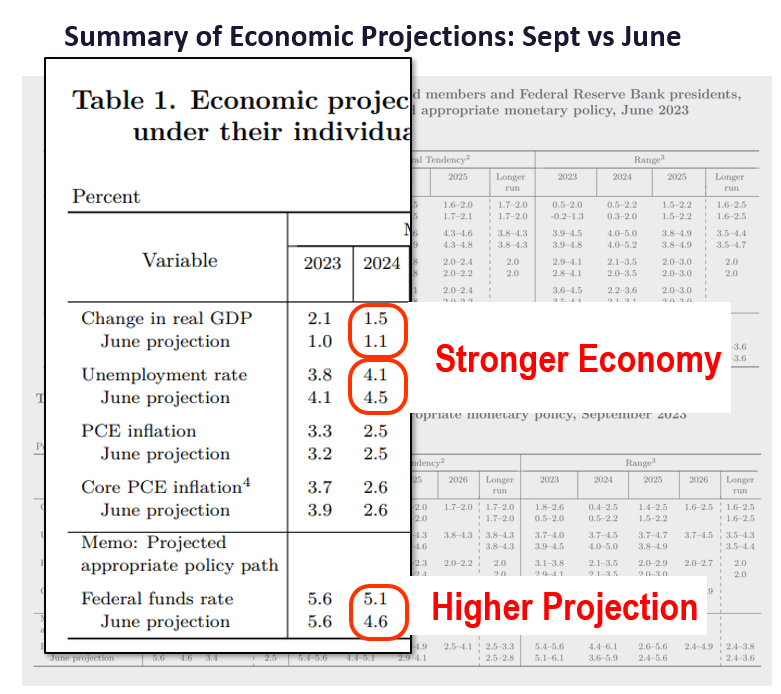

* The primary driver is the market's takeaway for the Fed to stay "higher for longer" as the Fed's SEP (summary economic projections) shows a median "dot plot" of 5.1% for YE 2024, versus 4.6% for the June SEP. In other words, in the past three months, the SEP shows the Fed FOMC now expects Fed funds to be +50bp higher with the passage of just three months.

* Fed Chair Powell made two clarifications to this rise in median YE 2024 dot plot.

-- First, he noted that the "SEP is not a plan that is negotiated or discussed...It's an accumulation, really...what you see are the medians...from 19 people."

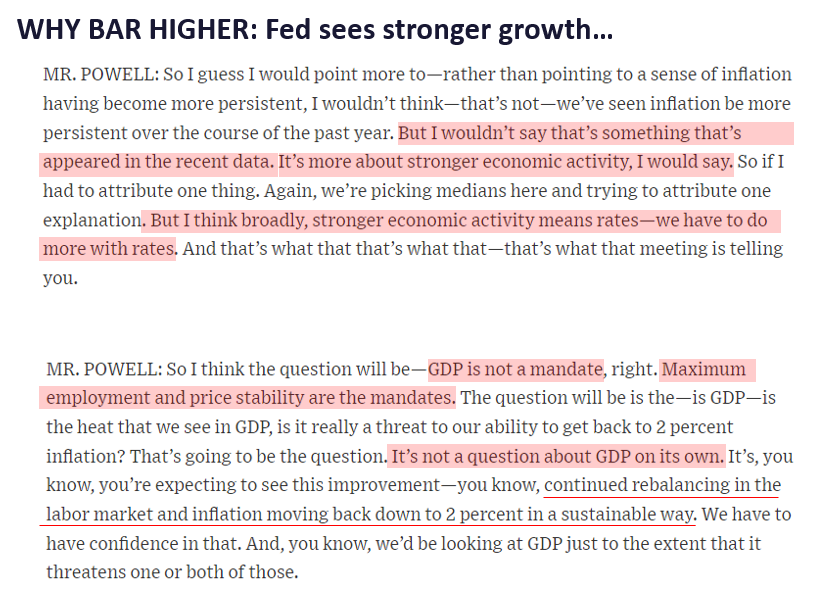

-- Second, the driver for the higher YE 2024 FF is "what it reflects...is that economic activity has been stronger than we expected."

-- GDP 2024 median is now +1.5% versus 1.1%, or +40bp higher. So this makes sense.

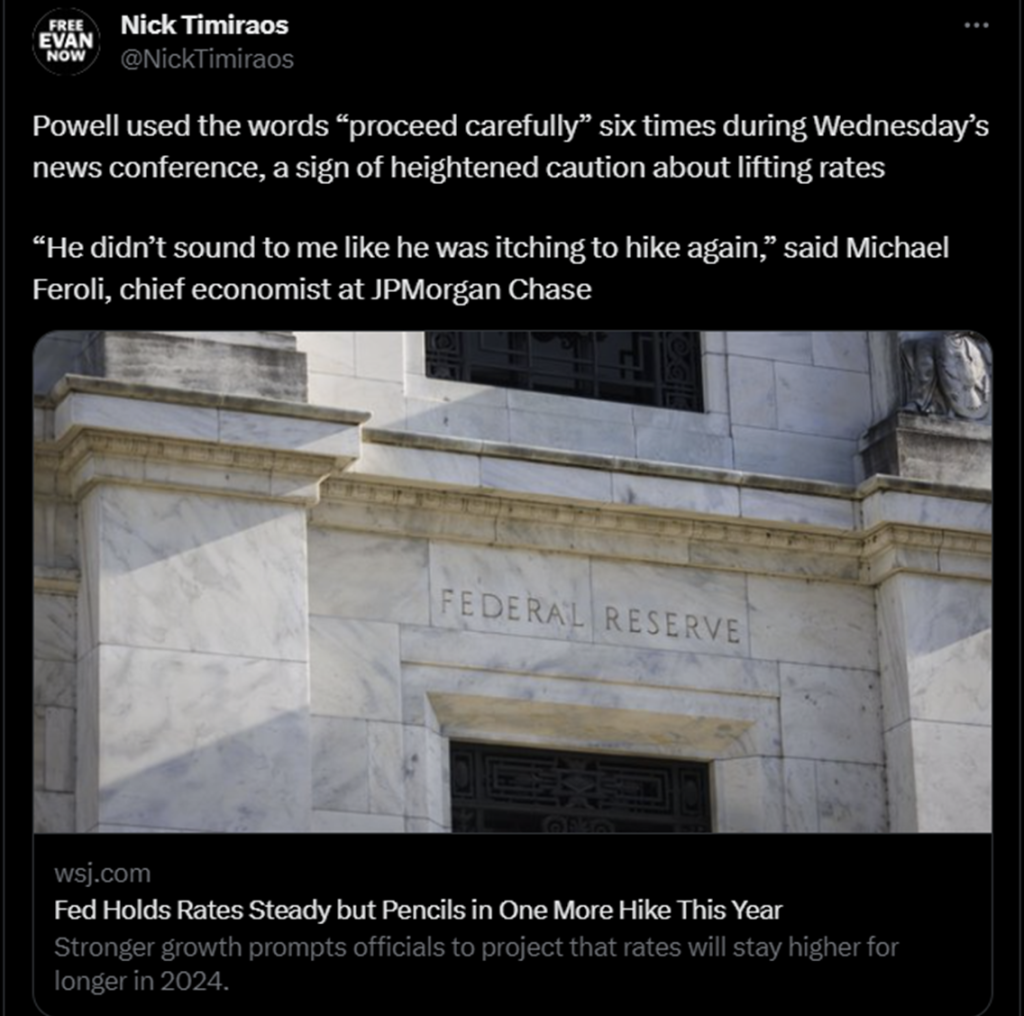

* The "hawkish" take is the Fed has raised the bar for cuts. And the hawkish take is the market driving view. And that means inflation has to come down further and more consistently for the Fed to consider rate cuts. Powell made comments supporting this view:

-- "What people are saying is let's see how the data come in-these good inflation readings that we've been seeing for the last three months, we want to see that it's more than just three months, right?"

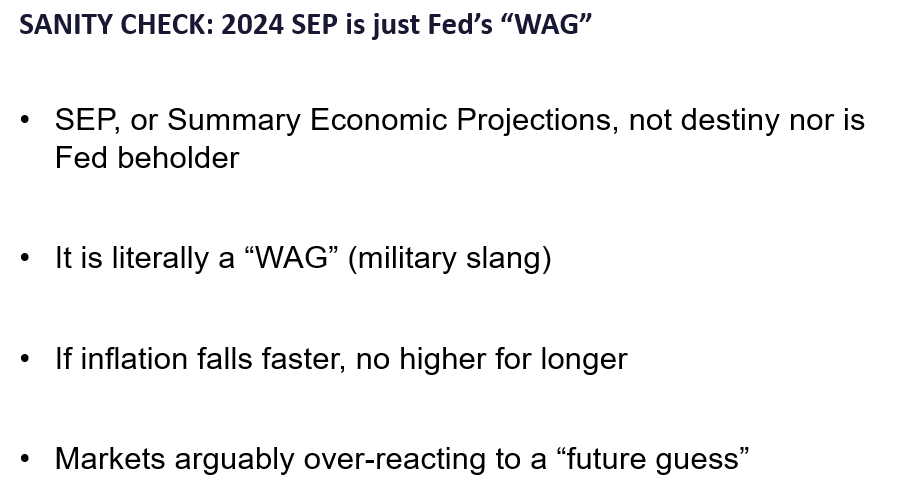

* The "dovish" take is simply, the SEP is merely the Fed's guess of the future. And that incoming data will impact that path of that future. There is a military term called "WAG" (wild assed guess) and this is essentially what the SEP is. It is literally the Fed's guess of the future.

-- And with GDP expected to be +40bp

-- Could the YE 2024 Fed funds have stayed at 4.6%?

- Wouldn't the market have been more negative if that was the case?

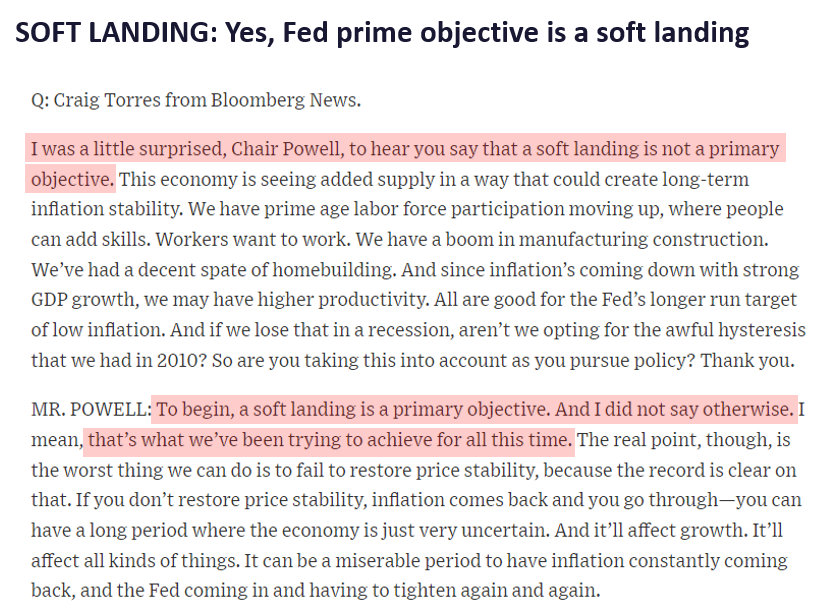

* Moreover, the Fed reiterated a "soft landing" is a primary objective and was declarative of that. But many only focused on an earlier exchange:

-- Q: Would you call the soft landing now a baseline expectation?

-- A: MR. POWELL: No. No, I would not do that.

-- Powell likely misspoke or misheard, but that answer drove an immediate selloff in equities.

BOTTOM LINE: Why is this -2.5% an over-reaction? 3 reasons

There are three reasons we believe equities overreacted to the FOMC press conference.

* First, after re-listening and re-reading the transcript, the "higher for longer" message is not as hawkish given the rise in Fed funds by YE 2024 stems from higher growth. Think about that, wouldn't it be less logical for the GDP forecast to go up, but the Fed doesn't think Fed funds needs to adjust?

* There will be a circuit of Fed speakers over the next few weeks, and our take is the "higher for longer DUE to higher GDP" has a more dovish tone, in my view. A hawkish take would be if inflation persistence went up and therefore Fed funds needs to stay high. But the SEP does not have a rise in inflation.

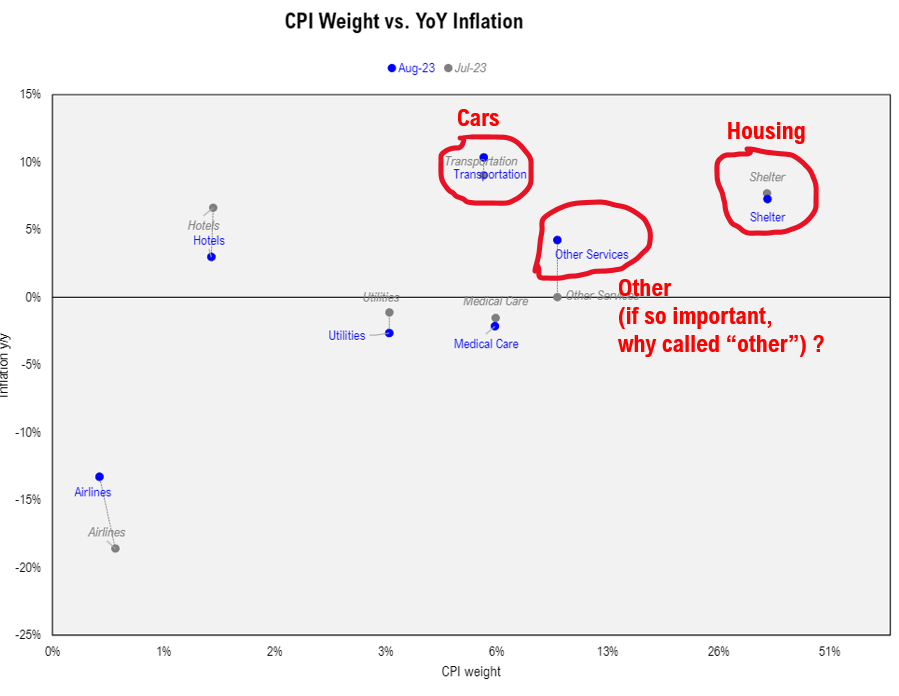

* Second, we need to be mindful that the Fed's SEP is merely a WAG of the future. And their prior forecasts have seen substantial error relative to what actually happened. As our chart below highlights, the only three CPI service categories with high inflation are:

-- housing (set to fall)

-- transportations services (set to fall)

-- "other" - an motley category, hence, called "other"

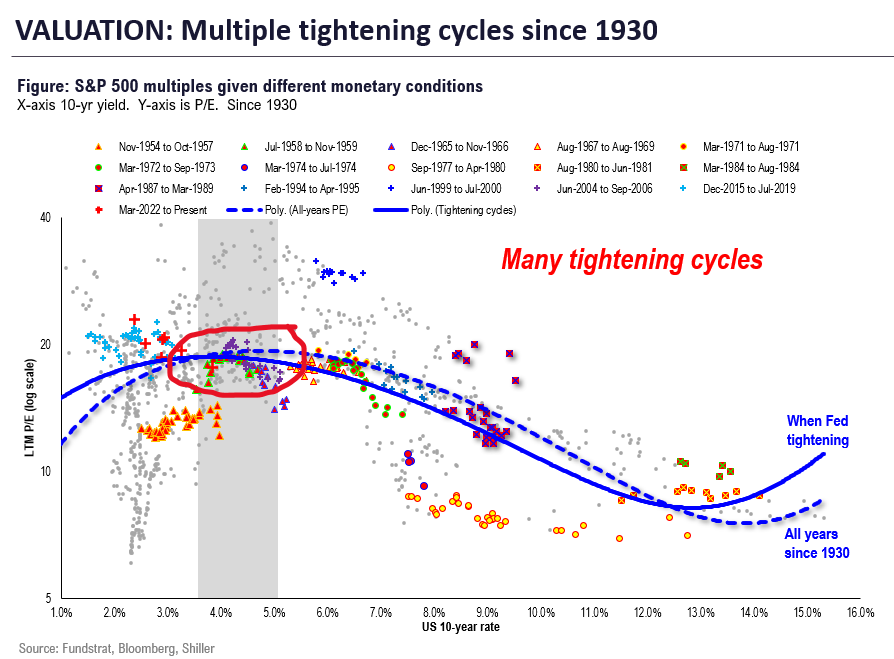

* Third, since 1930, a 4.5% US 10-year yield is not a P/E killer. In fact, the "sweet spot" for P/E is 3.5% to 5.5% yields which have seen an average P/E of ~20X. In fact, US yields below 3.5% are associated with lower P/E.

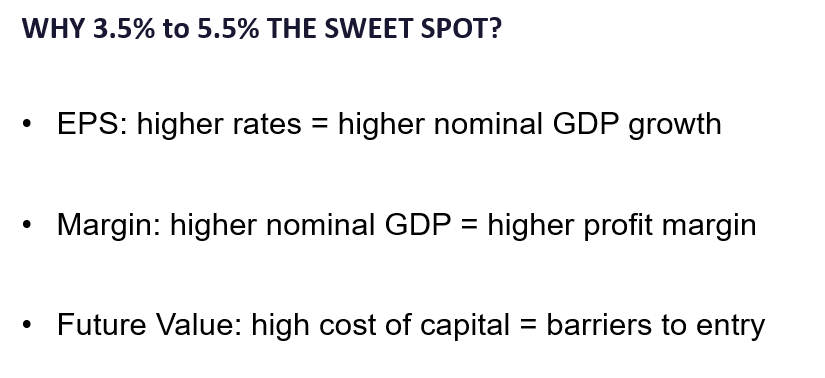

* Why does a US 10-year have the highest P/E? There are three reasons:

-- EPS: higher rates = higher nominal GDP growth

-- Margin: higher nominal GDP = higher profit margin

-- Future Value: high cost of capital = barriers to entry

* So these argue P/E today should be higher than P/E at the end of 2019 when Fed funds was 0% and US-10 year was 1.6%. Yet, P/E today is about the same as in 2019.

* Finally, we are exiting some seasonal weakness. And this, in our view, is supportive of stocks recapturing some of that decline.

Source: Fundstrat

Source: Fundstrat

Source: BLS

Source: X.com

Source: September FOMC Press Conference

Source: FOMC

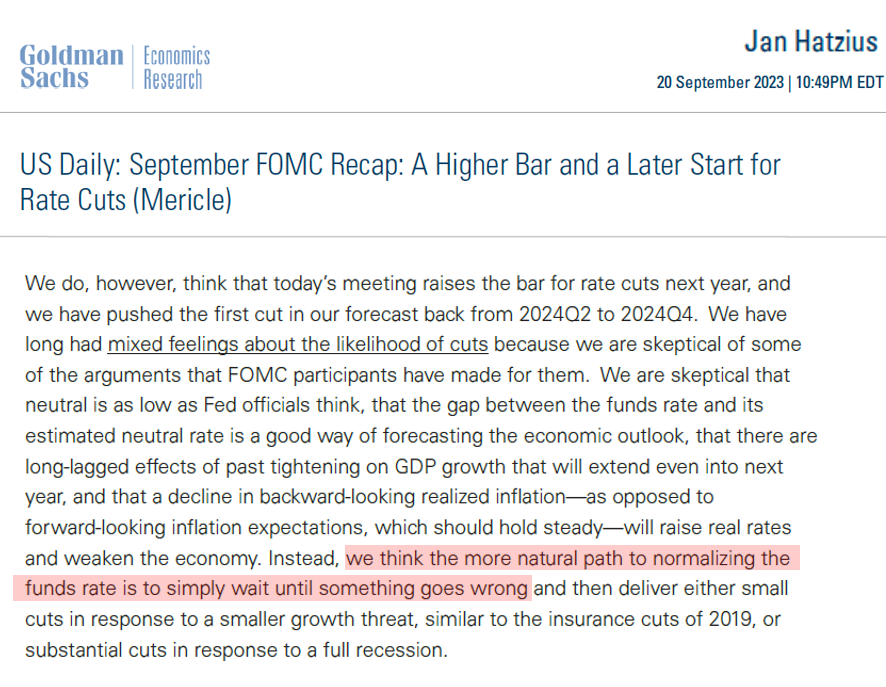

Source: Goldman Sachs Research

Source: FOMC September Press Conference