Strange Brew, CPI Report, Mag 7, Nasdaq 100 Juggling, Trading Berkshire Hathaway

Seven stocks apparently change hands so often as to be capable of severely skewing volume. This impacts the perception of the performance of the whole.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

How am I supposed to know

Hidden meanings that will never show

Fools and prophets from the past

Life's a stage and we're all in the cast

You gotta believe in someone

Asking me who is right

Asking me who to follow

Don't ask me, I don't know

-- "I Don't Know" Ozzy Osbourne (1980)

Strange Brew

Welcome to the show. Tuesday morning. November CPI morning. The FOMC will head today into the committee's two-day session that will culminate with Wednesday's policy decision, economic projections and press conference. The day ahead of this CPI release, Monday, was one strange day, though. Treasury securities ended the regular session nearly flat after selling off earlier on in response to some weak demand at auction in D.C., only to recover later.

After what had been a downright ugly auction of $50B worth of U.S. 3-Year Notes, the U.S. Treasury Department stepped back up to the plate roughly 90 minutes later to borrow $37B worth of 10-Year Notes. While I would not term this auction a disaster, it certainly was not strong.

Bid to cover of 2.53 was actually above the recent trend, which has been in the high 2.4's. That said, the bids entered were indeed price sensitive. The high yield printed at 4.296%. That tailed the "when issued" at the time by 1.4 basis points. Indirect Bidders (foreign accounts) took down just 63.8% of this issuance, dropping from 69.7% for this series in November and below the six-month moving average in the mid 66's. Direct Bidders were awarded 18.9% of the $37B auction, which was also (slightly) below average, leaving dealers with 17.3% of this paper, above the 15% or so they probably would as a group have been more comfortable with.

Regardless, Treasuries rallied off of those early afternoon lows. Keeping in mind that Treasury will go to market with $21B worth of brand new 30-Year Bonds on Tuesday afternoon, and the yield for the 30-Year Bond ended the regular session unchanged at 4.32%. That U.S. 10-Year Note went out at 4.24% as the 2-Year ended the session at 4.72%, neither very far from where they had gone out on Friday. These debt securities have rallied further overnight.

Juggling Act

Nasdaq announced some changes to be made to the Nasdaq 100 on Friday night, effective next Monday, December 18. This should add some at least a little more wickedness to this Friday's triple-witching expirations event. Some well-known names such as Ebay EBAY , Enphase Energy ENPH , Lucid LCID and Zoom Video ZM will get the boot from that "elite" Nasdaq index. Others, such as DoorDash DASH , Roper ROP and Splunk SPLK will be added.

A lot of capital tracks the Nasdaq 100, most notably the Invesco QQQ Trust ETF QQQ , so moves like this are significant. Still, ahead of this morning's CPI report, and with these changes not yet made, the Nasdaq 100 rallied on Monday to the tune of 0.85%, despite the fact that the entire "Magnificent Seven" closed lower. The six stocks in the Nasdaq 100 being replaced amount to just 0.83% of the total market cap of the index, so the movement, especially the weakness across the big seven was a bit odd. Meta Platforms META led the Mag 7 lower at -2.24%.

Taking the oddity that was Monday a couple of steps further, the S&P 500, Nasdaq Composite and Dow Industrials all closed at new 52-week highs, breaking the potential top that was November 29 across all three, and with the big seven acting as a drag on performance. Not only that, the Philadelphia Semiconductor Index rallied 3.4% on Monday, even as Nvidia NVDA , which is a charter member of the big seven, surrendered 1.85%.

Semiconductor leadership came from the builders and equipment providers and not the designers. Global Foundries GFS popped for a gain of 5.43% as Applied Materials AMAT , KLA Corp. KLAC and Lam Research LRCX tacked on 5.02%, 4.64%, and 4.61%, respectively.

According to Joseph Adinolfi's piece at MarketWatch, Monday was just the second time since Meta Platforms went public as Facebook in 2012 that the Nasdaq 100 traded into the green, while these seven stocks all traded into the red.

Okay... So, How Was Breadth?

Don't ask. I don't even know (see above lyrics) how on earth I am supposed to analyze breadth such as this. Ten of the 11 S&P sector SPDR ETFs closed in the green on Monday led by the Staples XLP and the Industrials XLI . Only Communications Services XLC , which has a heavy presence across the Nasdaq 100, closed in the red. That's also odd.

Winners beat losers at the NYSE by just a smidge, while advancing volume took an unconvincing 51.7% share of composite NYSE-listed trade. Aggregate NYSE-listed trade increased on a day-over-day basis, which should be a positive. Somehow, with the S&P 500, Dow Industrials and Dow Transports all in the green, I expected better.

Even more interestingly or eerily if you will, breadth was outright negative for Nasdaq listings. Check this out: With the Nasdaq 100 up 0.85%, the Nasdaq Composite up 0.2%, the Philadelphia Semiconductors up 3.4% and the S&P SmallCap 600 up 0.53%, losers beat winners at the Nasdaq on Monday by roughly 5 to 4. Advancing volume took just a 33% share of composite Nasdaq-listed trade, as aggregate trade across all Nasdaq listings increased on a day-over-day basis.

How is that? How is it that every single equity index that is known to have a greater impact upon overall Nasdaq performance than on overall NYSE performance closed out Monday in the green, yet breadth across Nasdaq-listed securities broadly was overwhelmingly negative? Just seven stocks? Those seven stocks apparently change hands so often as to be capable of severely skewing volume. This impacts the perception of the performance of the whole. Every day, week, month.... and so on.

Tell Us What You Really Think

By now, we all know that Arkhouse Management and Brigade Capital Management placed a $21 per share bid for Macy's M in order to take that company private. The deal at the headline, is worth $5.8B. Including debt, the deal is worth $8.5B.

Very interestingly, as seen at Bloomberg's website, Bloomberg Intelligence analyst Mary Ross Gilbert (in the piece authored by Jeannette Neumann) estimates that Macy's real estate assets alone, including the Herald Square address in New York City, could be worth $8B. Just in case you were wondering what kind of value these investors placed upon the Macy's retail business.

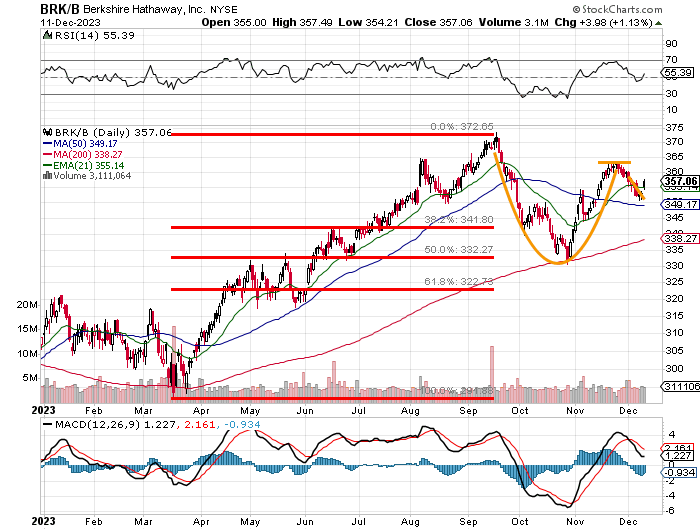

Updating Berkshire Hathaway "B"

This past September, I (must have been somebody else) gave you Berkshire Hathaway's "B" stock BRK.B as my stock for the balance of the year. The stock immediately sold off from there and then rallied with the broader market in November only to start selling off again as Vice Chair Charlie Munger passed on.

Interestingly, at Barron's on Monday, Andrew Bary pointed out that Berkshire's Class A shares BRK.A are now trading at a 2.5% premium to the Class B shares. Remember that Class A shares are convertible to 1,500 Class B shares. (Class B shares are not convertible to class A shares.) There is usually a value premium assigned to the A shares, but that premium has historically been around 1%. Bary points out that CEO Warren Buffett has said in the past that investors favor the B shares when this premium rises above 1%.

So, are we about to witness a run into the year's end for BRK.B? Or is BRK.B going to act as a drag on BRK.A? One thing we think we probably know is that the current premium is not likely to stay where it is.

Readers will see that in late October BRK.B used its 200-day simple moving average (SMA) as support, which also just happened to be at that time, the stock's halfway back (50% retracement) point of the March through September rally.

BRK.B's November rally apexed at $363, completing a September into late November cup. The cup has since added a handle. This makes $363 my new pivot. This also takes my price target up to $417 from $409. That said, should I be wrong on this name, my out (panic point) would be a failure at the 50-day SMA (now $349) with an intent to re-enter at that 200-day line (now $338), which not only provided support in October, but also this past March.

Economics (All Times Eastern)

06:00 - NFIB Small Biz Optimism Index (Nov):Expecting 90.8, Last 90.7.

08:30 - CPI (Nov):Expecting 0.0% m/m, Last 0.0% m/m.

08:30 - Core CPI (Nov): Expecting 0.3% m/m,Last 0.2% m/m.

08:30 - CPI (Nov):Expecting 3.1% y/y, Last 3.2% y/y.

08:30 - Core CPI (Nov):Expecting 4.0% y/y, Last 4.0% y/y.

08:55 - Redbook (Weekly):Last 3.0% y/y.

13:00 - Thirty Year Bond Auction: $21B.

14:00 - Federal Budget Statement (Nov): Last $-67B.

16:30 - API Oil Inventories (Weekly):Last +594K.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: JCI (0.69)

At the time of publication, Guilfoyle was long NVDA and BRK.B equity.