Stalemate at the Strait, China Stumbles, SpaceX Countdown Begins

Tough talk heats up in war on Iran, China economy shows trouble, SpaceX could go public soon at out-of-this-world valuation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Crude oil prices, after rising sharply on both Thursday and Friday, have continued to work their way higher overnight as Sunday melted into Monday. Yes, the ceasefire between the U.S. and Iran does appear to be holding for the moment, but so does the stalemate at the Strait of Hormuz. As the impassibility at that crucial maritime passage continues to pressure economic activity around the world, on Sunday, the Associated Press reported that the U.S. and Israel are possibly coordinating a resumption of the air war in Iran. Almost simultaneously, a drone strike believed to have been launched by either Iran or Iranian proxies, caused a fire near a nuclear power plant in the United Arab Emirates.

Bloomberg News is reporting that the U.S. and Iran remain far apart in regard to making any kind of peace deal that would end this conflict. U.S. Pres. Donald Trump posted to his Truth Social account, “For Iran, the Clock is Ticking, and they better get moving, FAST, or there won’t be anything left of them. TIME IS OF THE ESSENCE!” Iran’s semi-official Fars news agency has stated that the U.S. has set five main conditions for such a deal. Apparently, this would include transferring any uranium tied to the Iranian nuclear program to the U.S., while providing no reparations to Tehran and unfreezing less than a quarter of Iran’s frozen assets. This report cites no source. There has been no comment made by the U.S. side.

China’s Struggling Economy

The economy of mainland China truly started to show cracks around the edges in April as that impasse at the Strait of Hormuz and the U.S. naval blockade has deprived that nation of the “below market” illegal Iranian crude that it has survived on. On Sunday evening EST, China’s National Bureau of Statistics reported that for April, retail sales grew 0.2% year over year vs. expectations for growth of 2.0%, and Industrial Production grew 4.1% vs. expectations for growth of 6%. Additionally, fixed asset investment on a year-to-date-over-year basis, decreased 1.6% vs. the consensus view for growth of 1.7%.

This flurry of macroeconomic releases revealed a Chinese economy suffering its weakest growth in retail sales since December of 2022. The decrease in fixed income investment stems from the property sector where flows are down 13.7% this year as of April. Separately released data shows that home prices across seventy Chinese cities dropped again in April. That makes for a stunning 34-month streak of declines in home prices in that nation. Year-over-year decline of -3.5%, made April the worst month for Chinese home values since May of 2025 and came on top of a -3.4% print for March.

Ready for Lift-Off?

Late last week, CNBC reported that for SpaceX, the company’s S-1 initial public offering registration statement could become public at some point this week. With the company valuing SpaceX at potentially $2 trillion with a “T”, investors will be studying the S-1 very carefully. Within a few weeks of the release of this paperwork, SpaceX will begin its IPO roadshow. This is where the firm basically asks investors for capital and would likely take roughly a month to wrap up. For those not tracking the story, SpaceX has plans to place AI-focused data centers in orbit, which will cost some dough.

The Past Week…

The major U.S. equity indexes ended last week nearly unchanged despite the week showing on Friday. That said, a few of the mid-major and narrower in scope equity indices were forced to sail rougher seas as April inflation readings, on both the consumer and producer levels, ran hotter than expected. This pushed Treasury yields sharply higher, and that was pretty much the story of the week. President Trump also visited mainland China. That trip resulted in no major breakthroughs, with exceptions for aircraft manufacturer Boeing (BA) and jet engine maker GE Aerospace (GE).

The catalyst behind late week equity sluggishness was the 6% and 5.2% year-over-year prints for headline and core April producer price index, which truly shocked investors and drove bond traders out of Treasury debt securities. The reason there would be the increased probability that the Fed, even with Kevin Warsh at the helm, may have to raise short-term interest rates at some point in order to try to tamp down on inflation. Never mind that short-term interest rates do nothing to alleviate an event-driven supply shock to an economy, we’re dealing with AI-focused. momentum chasing algorithms here, not human beings.

Week Ahead

What matters moving forward…

– The Geopolitical: The presidential trip to China has come and gone. No news on Taiwan. Nothing new on AI-capable semiconductor chips. Some help for Boeing (BA) and GE Aerospace (GE) and for American soybean farmers, but maybe not as much as hoped for. The ongoing peace process, or should I say “lack” of a peace process between the US and Iran remains the most important item for the broader marketplace as the price of front-month crude oil will drive both corporate and economic performance.

– Macro: This will not be an especially active week, from a macroeconomic perspective. The dominant macroeconomic releases this week will be April Housing Starts and Building Permits on Wednesday morning, as well as the Flash Manufacturing and Services PMIs for May on Thursday morning. In addition, the University of Michigan will revise their survey for Consumer Sentiment and Inflation Expectations on Friday.

– The Federal Reserve: The Fed will be out in public this week, but not with a lot of visibility by headline level committee members. The highlight of the week will likely be Fed Gov. Chris Waller’s speech from Germany on Tuesday morning. Waller will speak again on Friday. The FOMC minutes of the late April meeting will be published this Wednesday afternoon.

– Earnings: First-quarter earnings season is now in its closing stages. This will not be another heavy earnings week, but there will be quite a few headline-level names posting their quarterly numbers. Home Depot (HD) will kick things off for the higher profile retailers on Tuesday morning. On Wednesday morning, we’ll hear from Hasbro (HAS), Lowe’s (LOW), Target (TGT) and TJX (TJX). That afternoon, tech giant Nvidia (NVDA) and Urban Outfitters (URBN) will report. Come Thursday, we’ll see results from Deere (DE), Walmart (WMT) and Zoom Communications (ZM).

– Corporate Events: Buckle up kids. This week brings several high-profile corporate conferences. The JP Morgan (JPM) Global Technology, Media, and Communications Conference will run from this morning through Wednesday. IBM (IBM), CoreWeave (CRWV) and Mastercard (MA) are expected to present. On Tuesday and Wednesday, Alphabet (GOOGL) will hold its annual Google I/O developer conference. Lastly, from this morning through Wednesday, Dell (DELL) will hold the Dell Technologies World 2026 Conference where Nvidia is expected to present.

The Week That Was…

By the skin of its teeth, the S&P 500 posted a seventh consecutive winning week over the past five trading sessions. Most of the rest of the U.S. equity marketplace was not quite so lucky. For the period:

– The S&P 500 gave back 1.24% on Friday to close up 0.13% for the week.

– The Nasdaq Composite gave up 1.54% on Friday, losing just 0.08% for the week.

– The Nasdaq 100 also gave up 1.54% on Friday, losing 0.38% for the week.

– The Russell 2000 lost 2.44% on Friday and 2.37% for the week.

– The S&P Small Cap 600 shed 1.62% on Friday and an ugly 3.21% for the week.

– The S&P Midcap 400 surrendered 1.65% on Friday and 2.43% for the week.

– The Dow Transports gained 0.38% on Friday but lost 0.32% for the week.

– The Philly Semis gave up an ugly 4.02% on Friday and 1.59% for the week.

– The KBW Bank Index surrendered 0.7% on Friday and a gnarly 1.8% for the week.

On Friday, ten of the 11 S&P sector SPDR ETFs closed out the session in the red. The losers were led by the materials (XLB), the utilities (XLU), and technology (XLK). Not surprisingly, energy (XLY) was the session’s only winning sector.

For the week, just four of the eleven S&P sector SPDR ETFs closed out the session in the green. Energy was the runway winner, followed by health care (XLV). The Discretionaries (XLY) led the losers followed by the REIT’s (XLRE).

Earnings

As of May 15, according to FactSet, for the first quarter, Wall Street now expects to see year-over-year blended (results & expectations) earnings growth for the S&P 500 of 27.7%, even with last week, but up sharply from 11.6% less than two months ago. This is a stunning increase experienced by the market through this reporting season and underscores just how powerful a force AI-related profitability has become. Wall Street also sees revenue growth of 11.4%, up from 11.3% a week ago. With 91% of the S&P 500 having reported, 84% of companies have beaten earnings expectations, while 80% have beaten sales projections.

For the full year of 2026, the street now looks for earnings growth of 21.5%, up from 21% last week, and up from 14.7% almost two months ago, on revenue growth of 10.3%, up from 10.1% last week and up from 7.7% a rough seven weeks ago. The outlook for the second quarter is also very positive. Second quarter S&P 500 earnings growth is now estimated at 20.5%, up from 19.9% last week.

At the moment, technology and the communication services sectors are projected to have grown Q1 earnings a jaw-dropping 51% and 48.9% for the first quarter, respectively. Just one sector, Health Care is currently projected to have suffered a Q1 earnings contraction (-3.2%).

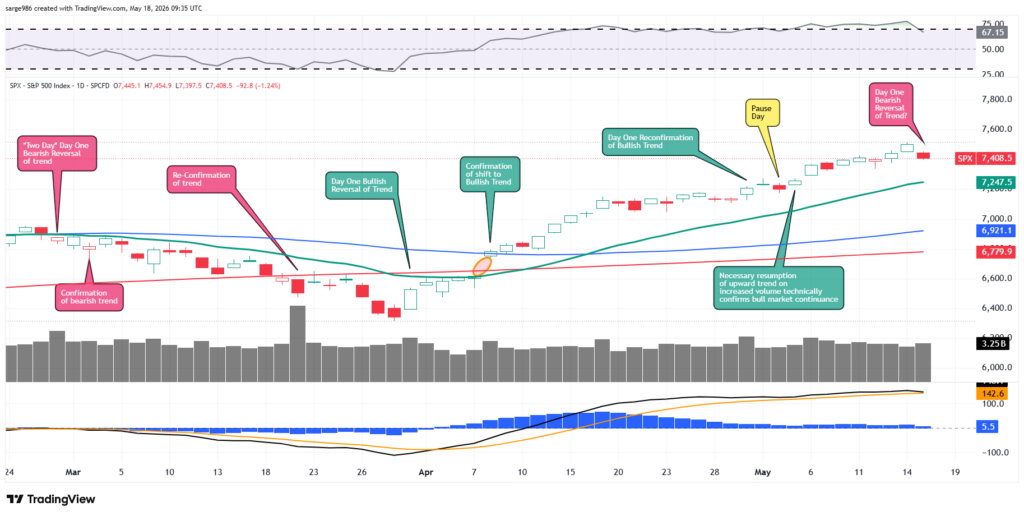

The Chart

Readers will easily see that over the past few months, our day-to-day charting of the S&P 500 has been nearly flawless in predicting the short-term movement of the U.S. stock market. The one question that many have been emailing me over the weekend, was simple. Was Friday a “day one” bearish reversal of trend. I hate to disappoint, but I am not sure as the evidence is not clear.

Sure, here it does look like such an event occurred. The major and mid-major indexes all had a rough day. For the S&P 500, relative strength dropped out of “technically overbought” territory after a two-week stay. That’s not necessarily a negative, but below the chart, readers will see that within the daily moving average convergence divergence, the 12-day exponential moving average appears ready to drop below the 26-day EMA. That would be short-term bearish.

The real “tell,” however, is in the trading volume. While breadth was rather nasty on Friday, and aggregate trade across NYSE-listings increased 6% on a day-over-day basis, activity across the membership of the S&P 500 remained below its 50-day simple moving average. Hardly the stuff of significant turns in market performance. In addition, aggregate trade across Nasdaq-listings actually contracted (-2.8%) on Friday, implying no real, massed change of heart across professional managers.

I could be wrong and markets do appear to be under pressure as I work my way through the zero-dark hours on Monday morning, but I think it would be a stretch to see Friday, in isolation, as anything more than a very short-term move. The low of the day for the S&P 500 was still higher than was the low of the day on Thursday. Not a meltdown. I’m keeping my cool.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 21.4-times 12 months’ forward-looking earnings, up from 21 times last week, but still down from 21.6 times about seven weeks ago. This is above the five-year average of 19.9 times for the index as well as being well above its ten-year average of 18.9 times.

The S&P 500 also ended last week trading at 28.3 times trailing twelve months’ earnings, down from 29 times one week ago, and above levels that the index reached seven weeks back. This also stands well above the five-year (24.6 times) and ten-year (23.3 times) averages for the index.

Only six of the eleven sectors are now trading above their five-year average valuations, led by the discretionaries (27.3 times), and the industrials (25.3 times). Technology (25.7 times), the REITs (18.4 times), the utilities (18.1 times), health care (17.2 times) and the financial (14.5 times) all closed out last week undervalued relative to or even with their five-year norms.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in a 99% probability for no change to be made to the current target range (3.5% to 3.75) for the Fed Funds Rate at the next FOMC policy meeting on June 17. As we know, Kevin Warsh will be running the central bank by then, but Jerome Powell will still have a say. There are no rate cuts fully priced in at any point in the future looking out towards year’s end 2027. That said, there is now a rate hike priced (63% probability) in as early as January 2027.

Economics

(All Times Eastern)

10:00 – NAHB Housing Market Index (May): Expecting 34, Last 34.

16:00 – Net Long-Term TIC Flows (Mar): Last $58.6B.

The Fed

(All Times Eastern)

10:00 – Speaker: Interim Atlanta Fed Pres. Cheryl Venbable.

Today’s Earnings Highlights (Consensus EPS Expectations)

Before the Open: BRC (1.35)

At the time of publication, Guilfoyle was long TJX, NVDA equity.