Route 493 Is Probably Not the Best Way for Investors to Go in August

As we start a new month, let's consult the market's 'logistics,' sentiment, banks and bond yields. One thing is for sure, though, the index movers own the S&P.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

For a few weeks now I have advocated that come August I thought the market would be intermediate-term overbought. I have not changed my view, despite the fact that earlier this week I said I thought we’d have a short-term oversold rally.

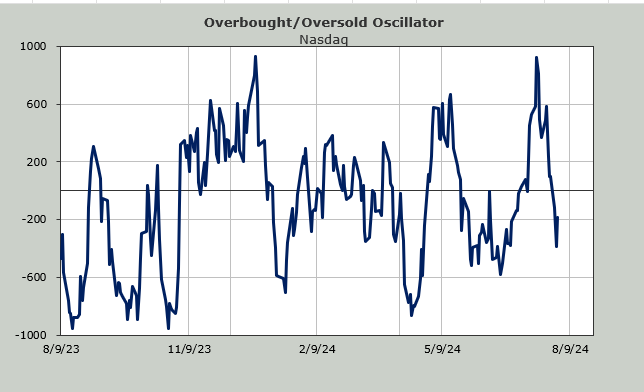

Keep in mind my indicators are based on breadth. Oh sure, I have a few that are based on price, such as the Nasdaq Momentum Indicator we looked at two days ago (showing an oversold condition). But notice that if we match my indicators up with the S&P 500 this year it tends not to match up now that we have a handful of stocks that move the index. And boy was that on display Wednesday.

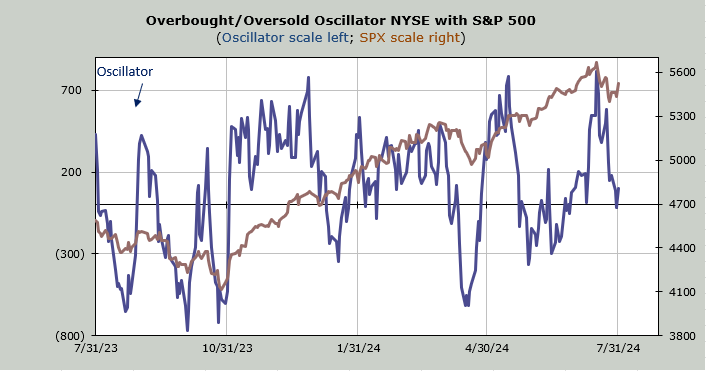

Tuesday’s 27-point decline in the S&P gave us net breadth on the NYSE of +700. I even showed you the chart and said that is a plus for the market. Wednesday’s 85-point gain gave us net breadth of +700 on the NYSE. It’s hard to call that a plus. Bearish would have been if it were negative so we’ll call it "not great." Heck, upside volume chimed in at 59%. That’s nothing to write home about.

But what I think it really shows us is the index movers own the S&P. I know everyone is all aflutter over the small-caps but they didn’t do much on Wednesday. Nope, Wednesday was all about the mega-caps.

If my indicators are set to get intermediate-term overbought in August I think that means the 493 are probably not going to be the outperformers.

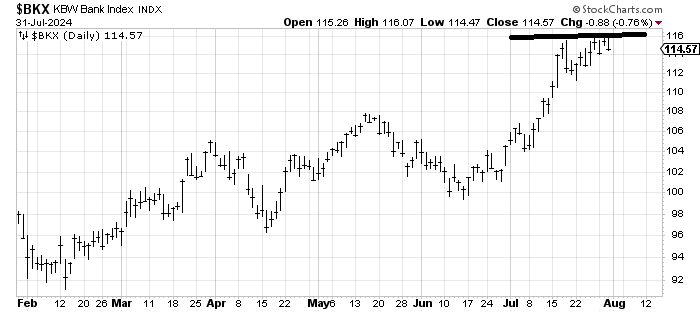

We already know I am not a fan of the banks with the Bank Index at 115. We might see one more push up in the banks but mostly as I have said for a week or so now, they are over-loved, over-owned and at resistance. And if the banks come down I think the small-caps underperform.

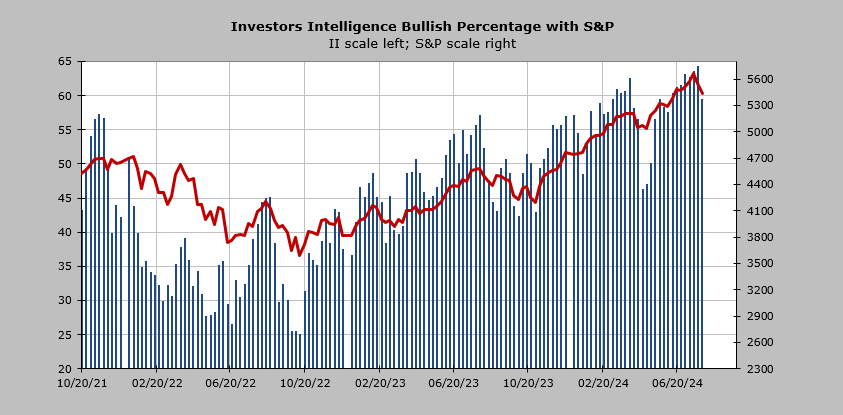

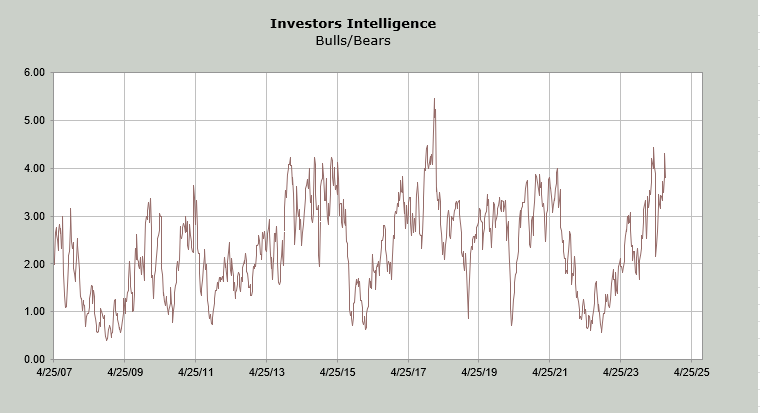

Then there is sentiment. I have some good news! The Investors Intelligence bulls backed off four points and now reside at 59%, which is actually the lowest since May. The bears haven’t moved very much. Most folks hopped right to the fence (the correction camp).

However it was enough to get the Bull/Bear Ratio back under 4.0. It’s only 3.8 now but it did back off.

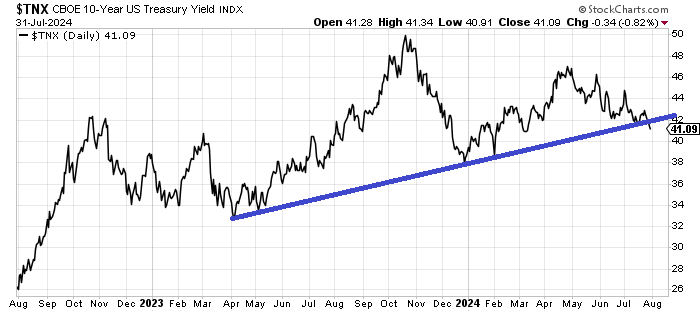

Elsewhere, bond yields finally broke that line I have been drawing in. It’s not by a lot but a break is a break. Even if rates rise back up over 4.2% in the next week or two I am inclined to think rates will head lower over time.

I don’t yet have a time frame for when we will be back to a short-term overbought condition. I have penciled in early next week so I think I will stick with that as the guideline.