Rocky Start to Iran Deal, Charting LESS Volatility, Bracing for Price Data

Let’s check the latest on the Iran deal after a bumpy weekend; also, how the bears, bulls and … Sarge sees the chart of the S&P.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Markets started out on the wrong foot on Sunday evening. It was no secret that the U.S. and Iran had signed a “memorandum of understanding” last Wednesday. An immediate and permanent halt to military operations on all fronts had been agreed to. Only the shooting didn’t exactly stop. Over the weekend, fighting between Israel (a U.S. ally) and Hezbollah (an Iranian proxy) in Lebanon threatened to harm the positive diplomatic effort.

On Sunday, talks in pursuit of a more permanent deal between the U.S. and Iran commenced in the Swiss Alps. The U.S. team was led by Vice Pres. JD Vance and included U.S. envoys Steve Witkoff and Jared Kushner (Pres. Trump’s son in law). The Iranian team at least included foreign minister Abbas Araghchi and is being led by Mohammad Bagher Ghalibaf, a now civilian leader who had served as a general in the Revolutionary Guard Corps and as head of the entire Iranian military until June of 2025.

It appears that representatives of the governments of Qatar and Pakistan, that are acting as mediators, said in a joint statement that these talks were “conducted in a positive and constructive atmosphere and that all sides had made “encouraging progress.” This is what turned U.S. markets for the better overnight after a pretty sloppy opening on Sunday night. The mediators also announced the creation of a “deconfliction cell” that will work to help control the violence in Lebanon.

In the Meantime…

There have been conflicting reports on just how open the Strait of Hormuz is. We have all heard reports of up to 19 million barrels of oil sailing out of the region on Sunday. We have also heard reports that this sudden flow has already been pinched. Perhaps we’ll know more once the sun rises.

Last Week

Wall Street closed out the holiday shortened week on a generally positive note despite a mid-week stumble. Investors and traders had to balance the positivity created by what appeared to be the end of hostilities in the Middle East with a probably more hawkish than expected, but not at all awful, first Federal Open Market Committee policy meeting run under the leadership of new chair Kevin Warsh.

On the corporate front, SpaceX (SPCX) continued to attract headlines and trader attention. That stock, despite posting “red candle” sessions on both Wednesday and Thursday, closed up 14.9% for the four-day period. Elsewhere, on Thursday, Pres. Trump announced that Intel (INTC) would partner with Apple (AAPL) to design and manufacture chips inside the United States. Shares of INTC ran 10.6% on Thursday in response to that news. Here at TheStreet Pro, I reiterated the Sarge-folio’s $155 target price for that stock on Thursday.

Only a Dad

Only a dad with a brood of four,

One of ten million men or more

Plodding along in the daily strife,

Bearing the whips and the scorns of life,

With never a whimper of pain or hate,

For the sake of those who at home await.

Only a dad, neither rich nor proud,

Merely one of the surging crowd

Toiling, striving from day to day,

Facing whatever may come his way,

Silent whenever the harsh condemn,

And bearing it all for the love of them.

Only a dad but he gives his all

To smooth the way for his children small,

Doing with courage stern and grim,

The deeds that his father did for him.

This is the line that for him I pen:

Only a dad, but the best of men.

– Edgar Guest (1916)

Week Ahead

What matters moving forward as markets respond to a rapidly evolving news cycle. This week, markets return to a normal five-day schedule. That, however, will only be a one-week thing as the next week, the July 4 holiday will force another four-day business schedule.

- The Geopolitical: Talks between the U.S. and Iran hit a couple of potholes over the weekend that at least to some degree, appeared to improve on Sunday. This has created some overnight volatility in not only equity index futures markets but also in energy, currency and debt security markets as well.

- Macro: The macroeconomic schedule takes center stage this week. The docket gets off to a slow start with nothing at all set for later today and the S&P Global Flash PMIs for June planned for Tuesday. On Wednesday, May new home sales will hit the tape. Then comes Thursday. That day, May Personal Income and Spending will be published as will May PCE inflation numbers. In addition, we’ll see data on May Durable Goods Orders as well as a final estimate for Q1 GDP. On Friday, the University of Michigan will release its revised survey results for June Consumer Sentiment and June Consumer Inflation Expectations.

- The Federal Reserve: Fed officials will start working their way out of their holes this week after last week’s initial policy statement under the leadership of new Chair Kevin Warsh. Fed Gov. Christopher Waller, who is influential, will speak publicly later this morning. Later this week, we’ll hear from NY Fed Pres John Williams and Chicago Fed Pres Austan Goolsbee. Williams, as the NY head, holds permanent policy voting rights. Chicago will not vote until 2027. Separately, the Fed will release the results from the annual bank stress tests for the largest US lenders this Wednesday evening.

- Earnings: Second-quarter earnings season does not begin in earnest until mid-July. All we have now are the few publicly traded firms that report out of season. That said, there are a scant few headline level names reporting over the next few days. On Tuesday afternoon we’ll hear from FedEx (FDX). On Wednesday afternoon, Micron Technology (MU) will post their numbers. Finally, on Thursday, it will be Darden Restaurants (DRI), and McCormick (MKC) that put their results to the test.

- Events: Amazon (AMZN) will hold its four-day “Prime Day” sale starting this Tuesday. Several competitors including at least Walmart (WMT), Target (TGT), Best Buy (BBY) and Kohl’s (KSS) will run simultaneous promotions meant to prevent huge losses in market share.

The Week That Was…

The S&P 500 posted an eleventh winning week in the past twelve. This is how it went…

- The S&P 500 gained 1.08% on Friday and 1.44% for the week.

- The Nasdaq Composite added a nice 1.911% on Friday and 2.74% for the week.

- The Nasdaq 100 rallied 2.48% on Friday and an impressive 3.26% for the week.

- The Russell 2000 gained 2.12% on Friday to add 2.01% on the week.

- The S&P Small Cap 600 tacked on 1.82% on Friday and 0.88% for the week.

- The S&P Midcap 400 gained 1.13% on Friday and 0.58% for the week.

- The Dow Transports tacked on 0.48% on Friday but lost 3.93% for the week.

- The Philly Semis soared 6.42% on Friday to scream 8.89% higher for the week.

- The KBW Bank Index lost 0.65% on Friday but gained 1.71% for the week. On Friday, five of the 11 S&P sector SPDR ETFs closed out the session in the green. Technology (XLK) and the discretionaries (XLY) led markets higher. Energy (XLE) was the big loser.

For the week, six of the 11 S&P sector SPDR ETFs finished in the green. Technology, again, led all sectors higher, followed by the Industrials (XLI). Energy and health care (XLV) struggled mightily. For the week, cyclicals out-performed defensives, which can often be taken as positive for both the marketplace and the general economy.

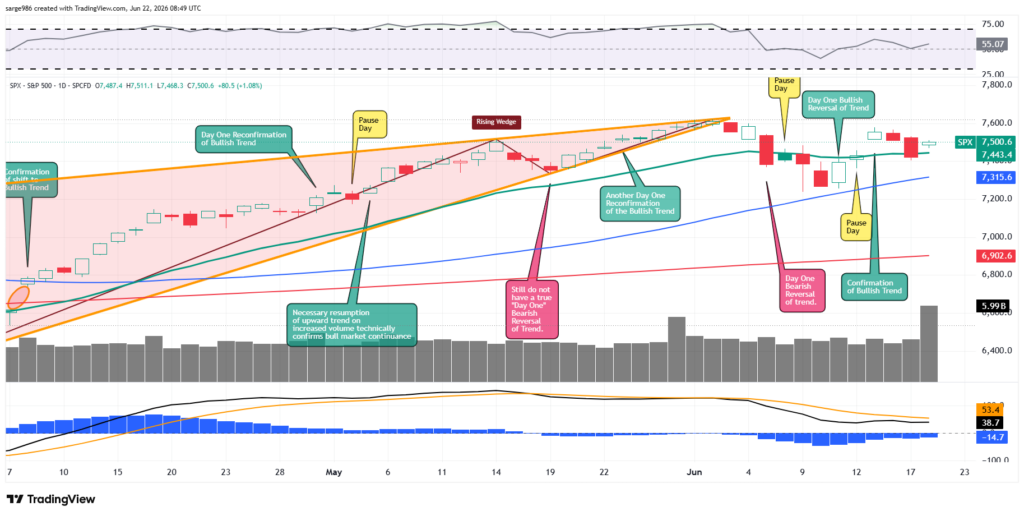

The Chart

Readers will see that the S&P 500 has gone on to seemingly build the mini “Cup with Handle” pattern that we spoke of last week. To this point, the index has been able to make use of its 21-day exponential moving average as new support after structural support had been provided by the 50-day simple moving average. To the common trader this simply means that traders jumped on board after the professional money bought the dip.

That’s what the bulls see. The bears see three consecutive days of lower-highs. The pragmatists? They see an “inside” day on Friday. This simply means that volatility, at least for the short term, will quiet down and is probably a market positive. Then again, I tend to be an optimist. For the S&P 500, Relative strength has returned to better than neutral levels, but the daily moving average convergence divergence still needs some work in order to leave its bearish posture behind.

Earnings

As of June 18, according to FactSet, for the second quarter, Wall Street now expects to see year-over-year earnings growth for the S&P 500 of 22%, up from 21.9% last week. Wall Street also sees revenue growth of 12.1%, up from 12% one week ago. For the second quarter, 48 S&P 500 companies have issued negative earnings guidance while 62 have issued positive guidance.

For the full year of 2026, Wall Street now looks for earnings growth of 23.2%, up from 22.8% two weeks ago, and up from 14.7% more than two months ago. This would come on revenue growth of 11.1%, up from 11% last week and up from 7.7% a rough 10-plus weeks ago. The outlook for the third quarter is also very positive. Third-quarter S&P 500 earnings growth is now estimated at 25.6% year over year.

At the moment, the energy and technology sectors are projected to have grown Q2 earnings an absolutely jaw-dropping 121.8% and 59.6% respectively. Just one sector, health care (at -9%) is currently projected to have suffered a Q2 earnings contraction.

Economics (All Times Eastern)

No major domestic macroeconomic data-points scheduled for release.

The Fed (All Times Eastern)

09:00 – Speaker: Reserve Board Gov. Christopher Waller.

Today’s Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long MU, AMZN equity.