On Election Day, What Does the Market Want?

It's hard to know what will happen today, given that we're only short-term oversold.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Election Day has finally arrived. Everyone is nervous. Everyone is on edge. Everyone wants their candidate to win. But what does the market want? That’s the question I think every guest on television is asked.

Quite frankly, I don’t know. If we were intermediate-term oversold heading into Election Day, I’d say the market is going to like whatever outcome we get. But we’re only short-term oversold (and at that, it’s not a great oversold condition--yet). We’re not yet intermediate-term oversold.

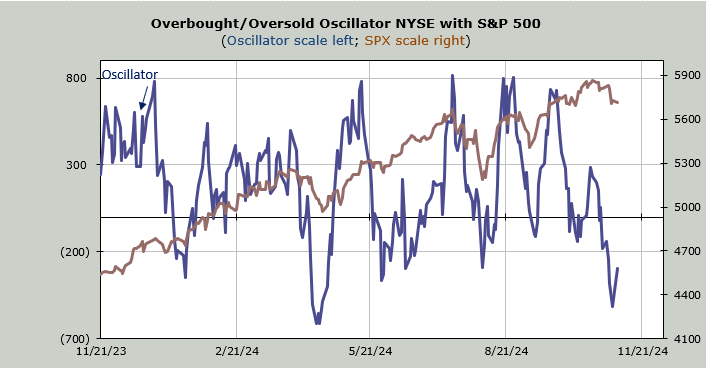

But I consider Monday’s action to be a step in the right direction. By that, I mean we had a morning whoosh to the downside, and there were fewer stocks making new lows. That’s the first time we’ve seen that in weeks.

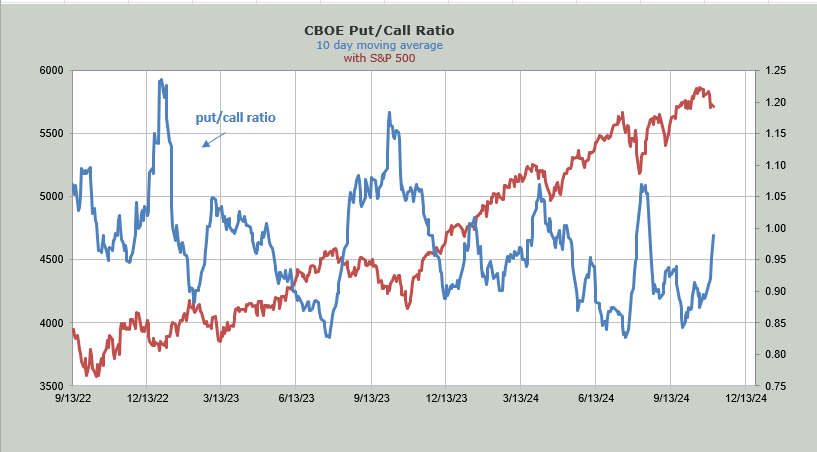

The S&P closed down 20 points, yet breadth stayed positive. We haven’t had many days where breadth has outperformed in weeks. And then there is sentiment. The put/call ratio shot up to 1.30. That is the highest reading all year. We’ve had five other times with readings in the 1.27-1.29 area, most came at the end of a correction.

On Friday, the put/call ratio was high, but it wasn’t as if the ETF or equity ratio was particularly high. Most of the high reading came from the VIX. The VIX’s put/call ratio was 2.32 on Friday. As of this writing, I don’t have the reading for Monday so it is possible that much of the high reading on Monday was also the VIX, meaning folks are loading up on puts on the VIX, believing once the election is done we’ll see volatility come in.

That’s all possible but as long-time readers know, I hate to rationalize an indicator, so let’s check in on the ten-day moving average of the put/call ratio. It is now at .99. A reading over 1.05 was ‘enough’ for the April low and the August low. Last October’s low took a bit more with a reading over 1.15. But the point is that it is finally on the move.

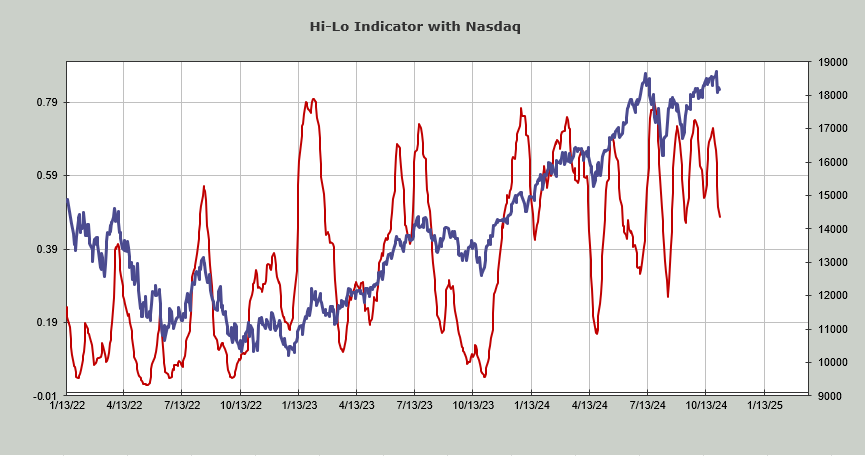

The Hi-Lo Indicator nudged down a bit more Monday and now stands at .48. Let’s see if it can get to a proper oversold condition, down under .19 as it did in April.

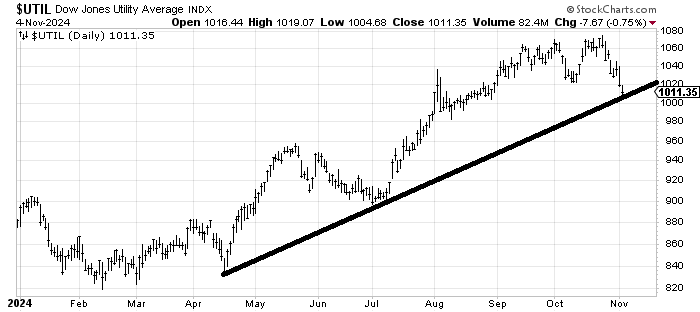

Finally, yes the bonds bounced which I will call a minor relief rally for now. The Utes, however, did not care one whit about the rally in bonds. The good news is that, at 1070, the folks on television were still waxing poetic about the Utes, but at 1010, it’s as if they no longer exist. We no longer hear how the Utes are needed to power AI or whatever narrative they had.

This happens as the Utes come down to tag this uptrend line that has been in place since the spring. I’m not quite ready to jump back into the Utes, but I do think they ought to attempt a bounce this week. At least, that would be my vote.