Nvidia $3 Trillion, Market Igniters, Jumpin' July? Index Trends, D-Day Remembered

What actually did ignite the 'All Things AI' rally on Wednesday? Let me count the ways.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Hello Darkness, my old friend

I've come to talk with you again

Because a vision softly creeping

Left its seeds while I was sleeping

And the vision that was planted in my brain

Still remains

Within the sound of silence

- "The Sound of Silence" Paul Simon (1964)

80 Years Ago, on This Day...

Allied forces landed at Normandy, France in what became the largest amphibious operation in history. From June 6, 1944, through September 14, 1944, the U.S. Army would suffer 135K battle casualties in northern France. The U.K. and Canada would suffer 83K battle casualties. More than 12K French resistance and civilians would die. The numbers just stun the modern brain. So many names. Search for one. Just one. At random.

Pvt. Joseph J. Battaglia

16th Infantry Regiment

1st Infantry Division

U.S. Army

Born in NY in 1922

KIA June 1944 at Omaha Beach

Buried at Normandy, France

I salute your memory and pray this morning for those who mourned you. I thank you, Sir.

Risk On?

There has been concern. A now more than week-long rally in U.S. Treasuries amid a series of weaker-than-expected macroeconomic releases has caused concern that economic activity has slowed. Maybe the results of this Friday's BLS employment surveys won't look so hot. That is what the Federal Reserve Bank has been trying to do, is it not? Actually, slow the economy without bringing about outright contraction?

On Wednesday morning, the ADP Employment Report for May printed private sector job creation at 152K, which was considerably weaker than the 175K-ish that economists were looking for. Mind you, as far as accuracy is concerned, ADP has been far more accurate than has been the BLS for about a year if one simply goes by the size and frequency of "after the fact" revisions.

That said, the keyword-reading algorithms that control price discovery in 2024 are set to react to the BLS data far more so than they do the ADP data, so "hogwash" or not, we do have to trade and invest around the BLS data and respect whatever numbers they throw at us for their ability to impact financial markets. No, the ADP Employment Report was not the reason behind the roaring rally that accelerated throughout the regular session on Wednesday.

Nor was the ISM Non-Manufacturing PMI for May, which printed at 53.8 at the headline, above consensus and climbing out of contractionary territory. That report at least broke up the recent losing streak that the economy had been on. Within that report, among the key components, really only employment slowed, which unfortunately aids the fight against inflation.

The Real Reasons...

What actually did ignite U.S. financial markets on Wednesday? Let me count the ways.

First, on Tuesday evening, during the post-earnings conference call, CrowdStrike CRWD CEO George Kurtz said: "We're the next conversation. Jensen Huang, Founder and CEO of NVIDIA NVDA recently validated this by stating in our Q1 partnership announcement that, quote, Pairing NVIDIA accelerated computing and generative AI with CrowdStrike cybersecurity can give enterprises unprecedented visibility into threats to help them better protect their businesses. End quote."

That set up anything tech and especially anything AI-related for a heck of a run on Wednesday morning. Speaking of Wednesday morning, the Bank of Canada surprised some and led off the coming cycle of perceived easier global monetary policy with a cut of 25 basis points made to Canada's benchmark rate.

The ECB, which steps to the plate this morning, is expected to do the same, as major central banks around the world get ahead of the Fed on this due to persistent U.S. inflation. This is expected to eventually lead the U.S. towards easier policy as well in order to remain competitive.

Until that happens, the U.S. dollar is expected to strengthen against its reserve currency peers, which should cool commodities-based inflation. We're already seeing something of a reversal across that space. The U.S. 10-Year Note rallied further on Wednesday as that yield dropped to 4.28%.

Furthermore...

In addition, in a note to clients, Goldman Sachs global markets division manager and tactical specialist Scott Rubner wrote: "New Quarter (Q3), new half year (2H), this is when a wall of money comes into the equity market quickly." Rubner added "I am seeing a re-emergence in retail traders during the summer, they tend to come around in July."

The fact is that according to TrendSpider, since the turn of the century/millennium July has been positive for the S&P 500 67% of the time for a mean gain of 1.53%, making it the third most successful month of the year in terms of mean return. On average, July is the best month for the S&P 500 from now until November, so Rubner is perhaps on to something. If this is an average year.

Trading Notes

-- Nvidia NVDA surged 5.16% on Wednesday, closing at $1,224.40 (it's up overnight as well), and at a market cap of about $3.01T. That moved Nvidia ahead of Apple in terms of valuation and made Nvidia the second-largest U.S. company (at least for now) behind only Microsoft MSFT. Microsoft went out last night with a market cap of $3.15T, closing up 1.91% for the session. Keep in mind that NVDA will split 10-for-1 over the weekend and may very well give back some of this momentum after the fact.

-- The loading up of shares of CrowdStrike CRWD and ServiceNow NOW on weakness late last week and early this week has certainly seemed to pay off after Wednesday's "all things AI" rally.

-- Palantir Technologies PLTR announced on Wednesday that nearly 70 customers will showcase their work on Palantir's AIP (Artificial Intelligence Platform) at the firm's fourth "AIPCon" conference in twelve months on Thursday (today), June 6. AIPCon will be accessible via live stream on YouTube starting at 13:00 ET.

Change One to Change Two

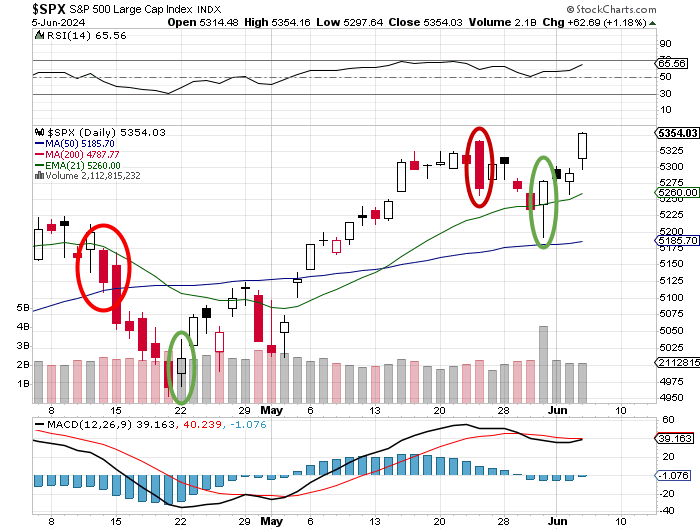

The downward change in trend that we had just confirmed for the S&P 500, but was never confirmed for the Nasdaq Composite, has indeed failed with both of these indexes trading at all-time highs on Wednesday. As one might suspect any attempt to turn the market broadly is considered to have failed once the point of reversal is superseded. Hence, the next significant selloff on increased trading volume will again be a "day one."

It would appear that Friday's high-volume rally for the S&P 500 now becomes a "day one" but that move has not slowed yet. In fact it has accelerated. Does that mean that we still need a break in the rally before confirmation? By our time-tested rules, yes.

However, check this out:

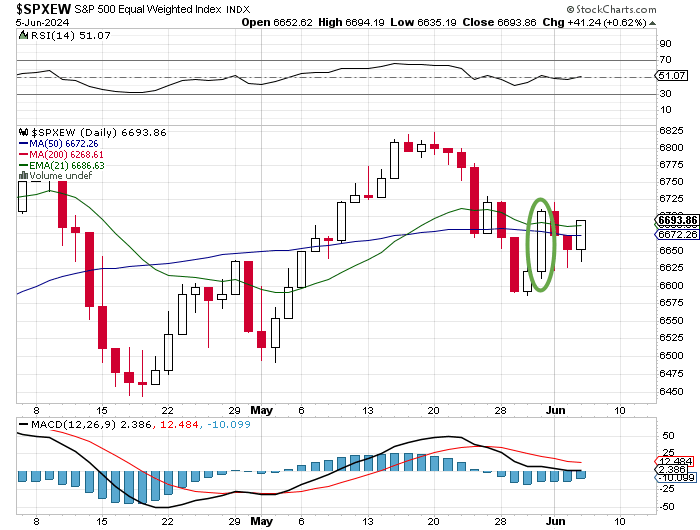

The equal-weighted S&P 500 did get that break and is still a bit away from making a new high. Does this add more credibility to what Goldman's Rubner wrote on Wednesday? It does make one think. I don't know that I know the answer.

I do know that I am making some dough in this environment and the ability to evolve, to adapt, to overcome, is far more crucial to success than being initially correct.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 215K, Last 219K.

08:30 - Continuing Claims (Weekly): Last 1.791M.

08:30 - Balance of Trade (Apr): Last $-69.4B.

08:30 - Non-Farm Productivity (Q1-rev): Flashed 0.3% q/q, SAAR.

08:30 - Unit Labor Costs (Q1-rev): Flashed 4.7% q/q, SAAR.

10:30 - Natural Gas Inventories (Weekly): Last +84B cf.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: SJM (2.33), TTC (1.29)

After the Close: DOCU (0.79), MTN (9.97)

At the time of publication, Guilfoyle was long NVDA, AAPL, MSFT, CRWD, NOW and PLTR equity.