MicroStrategy Shares Have Grown Overvalued and They're No Proxy for Bitcoin

Investing in MicroStrategy is a risky bet, one that only sophisticated traders should consider.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Unless you’re a sophisticated trader, MicroStrategy MSTR is too risky for you. Face it. It is. And I'll tell you why below.

But maybe you're a huge fan of CEO Michael Saylor's vision and I can't talk you out of it.

If that's the case, here are the positives:

- Unlike AAPL or TSLA, MSTR is not heavily represented within any index fund that you probably already own. MSTR isn’t part of the S&P 500 and it’s weighted at less than 1% of the Russell 2K.

- It’s a leveraged play on Bitcoin and is easy to buy and sell. Just like any other stock, but unlike Bitcoin.

- MSTR has reinvented itself as a "Bitcoin Treasury Company" and plans to make significant revenues through the financial engineering of Bitcoin products. It really is innovative and if you believe in a Bitcoin future, then you probably align with MSTR’s vision.

Please be sure to consider your timing. Don’t overpay for companies like MicroStrategy; they’re just too volatile and you could get burned.

Like most investors, I'm not sure that I really understand MicroStrategy. So, consider this article as much an overview of the stock as it is an investment "recommendation."

Please add your comments below and tell me what I’ve missed.

What Does MicroStrategy Do?

Back in 2000, one of my coworkers was the market maker for MSTR at our company. I remember that he made a pile of money trading it until the company was forced to restate a decade’s worth of financial results, and the stock vaporized 60% of its value in an instant.

More recently, Michael Saylor, the company’s CEO, settled a tax fraud lawsuit, paying $40 million in fines and back taxes.

So, it’s a company that lives on the edge.

From 1989 until 2020, MicroStrategy was a business intelligence company.

In 2020, Saylor realized that the company was no longer growing and that he could either sell it or pivot. He is a visionary and chose to pivot.

Today, MSTR is a Bitcoin Treasury Company.

In other words, it’s a company that owns a lot of Bitcoin, $40 billion worth, and creates financial products for sophisticated traders who want to make bets on Bitcoin.

They have been able to borrow money at around 0% interest by issuing bonds that convert into MSTR stock when certain milestones are hit. They claim that they can then lend this money to the crypto community at 60% interest. It’s a nice profit margin. Saylor also says that they can repeat this process at will, unlike a traditional bank that might have a five-year cycle on its loans.

It’s important to note that the traders who play with MSTR products aren’t trading directionally. They don’t really care if Bitcoin goes up or down. They only care that it goes up and down, and does it a lot. They love volatility.

According to Saylor, the type of trader who buys these products require three things: liquidity, volatility and durability.

For example, meme stocks like GameStop GME haven’t proven durable. The trade perks up every now and then. Other meme stocks have come and gone.

Bitcoin, on the other hand, is highly liquid. It’s the seventh-largest asset on earth, according to Saylor. It’s got an annualized volatility of 60%, which is four-times the S&P 500’s volatility. And it’s durable. It’s a trading vehicle that’s seen interest growing over the last decade and doesn’t seem like it’ll fade.

The only thing that can hurt MSTR, according to Saylor, is a loss of volatility.

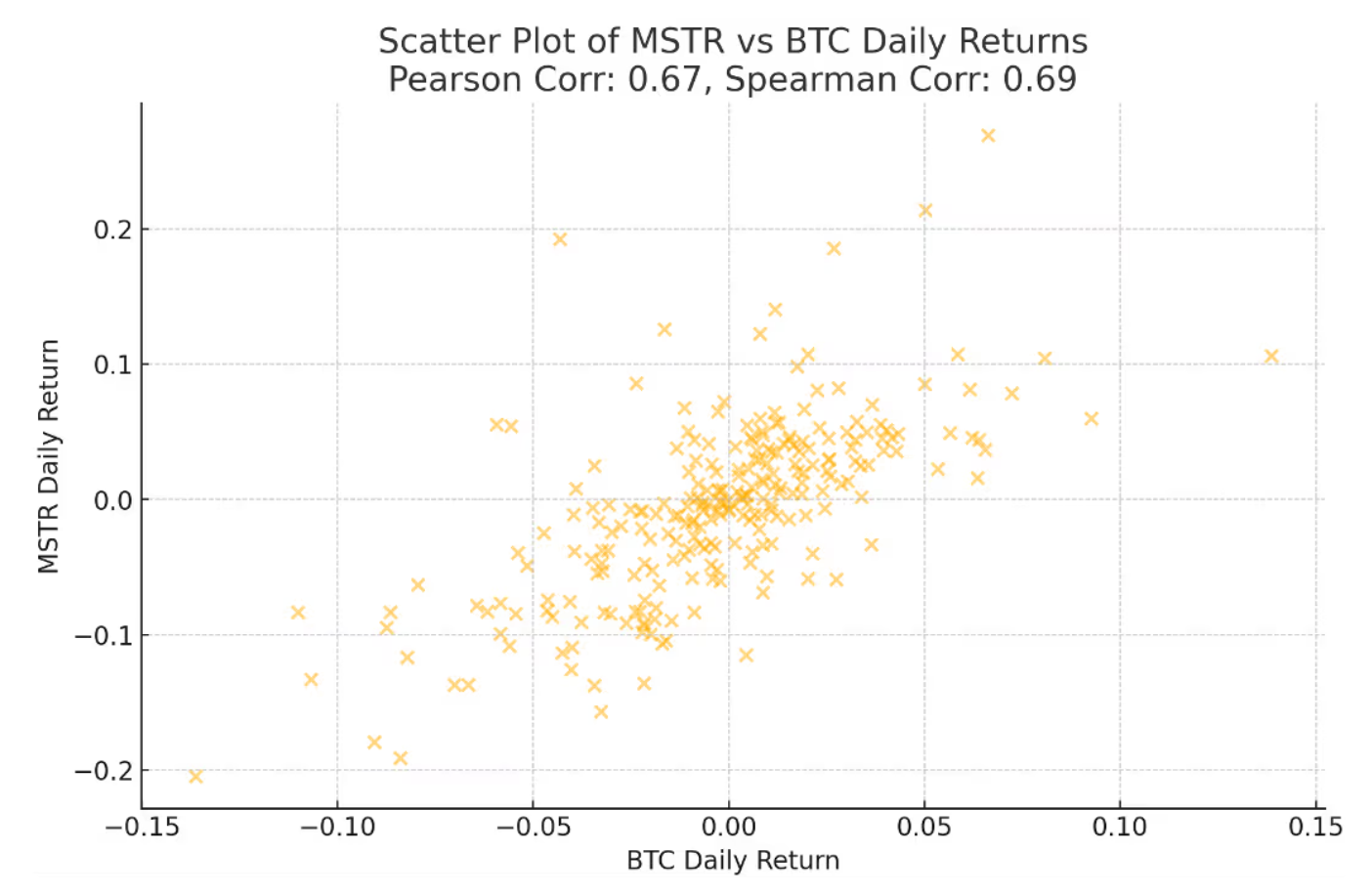

MSTR currently trades like a leveraged play on the price of Bitcoin. For every percentage increase in Bitcoin, MSTR currently rises by about 2.2%.

Saylor also says that other financial instruments are engineered to be uninteresting. Think about your portfolio. You want it to rise, year in and year out, with minimal volatility. Bitcoin, on the other hand, is engineered to be interesting, volatile.

An old curse says, “May you live in interesting times.”

I’ll take boring in my portfolio, thank you.

Look, I’ll never tell you to short MicroStrategy in this market. But you should be aware of the red flags.

Red Flags

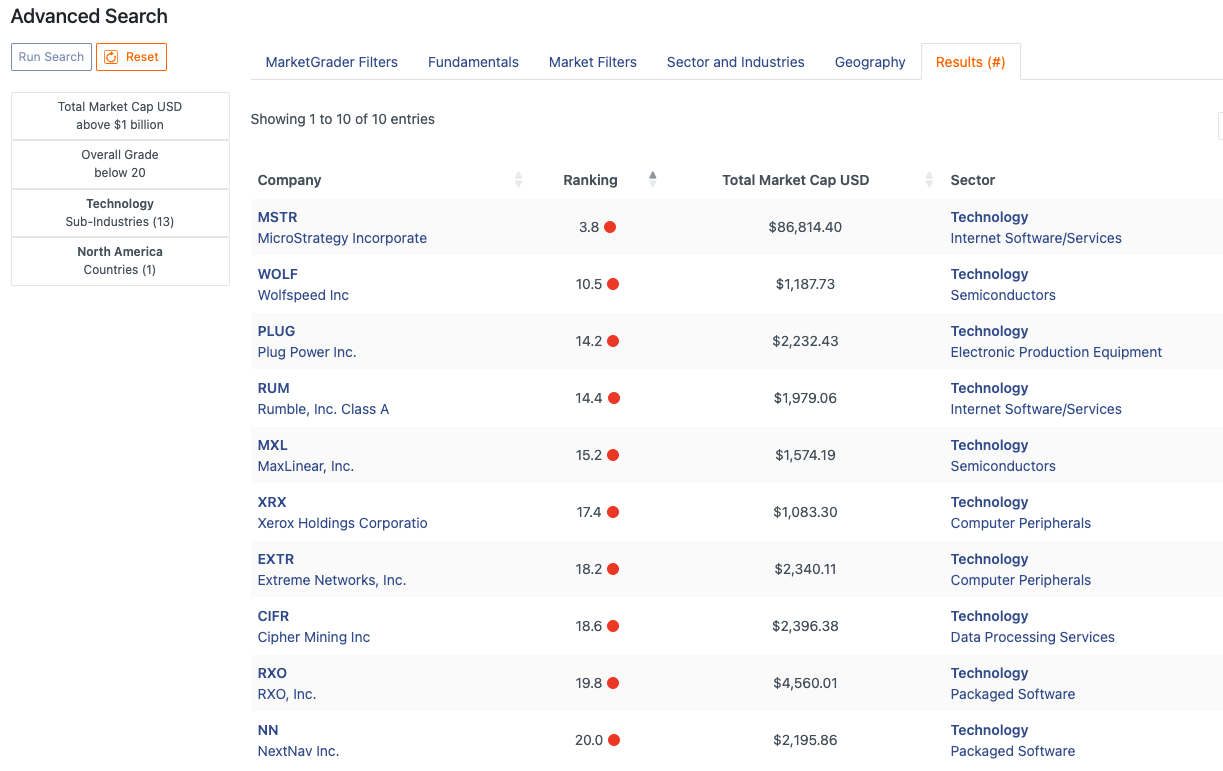

For one thing, of all tech stocks trading in the U.S. with a market cap of greater than $1 billion, MicroStrategy has the worst MarketGrader Overall score.

That’s right. 3.8. Out of 100.

This doesn’t mean you should sell it short. It just means you should understand how risky it is if you own it or are considering jumping in.

That said, I’m not sure that you can fully analyze MSTR using MarketGrader. MarketGrader is a quant platform that relies heavily on analysis of earnings and growth. According to MarketGrader’s CEO, MSTR is like a closed-end fund that uses leverage to hold Bitcoin. It’s also a company that’s in the midst of a longer-term refocusing into a financial services company that provides trading vehicles to sophisticated traders.

I have nothing against that. Just be aware that traditional fundamentals are not great.

Investing is about risk management. And MSTR is anything but low risk.

Maybe you want Bitcoin exposure and MSTR is the vehicle you’d like to do it with.

MSTR is highly correlated with the price of Bitcoin. According to Coinbase, 65% correlated. So, it sounds like it’s a reasonable proxy for Bitcoin.

The thing is, it’s highly leveraged. The company has taken on debt to buy additional Bitcoin and, while they’re currently deep in the money on that trade, Bitcoin is a volatile asset. When it drops, MSTR will drop more.

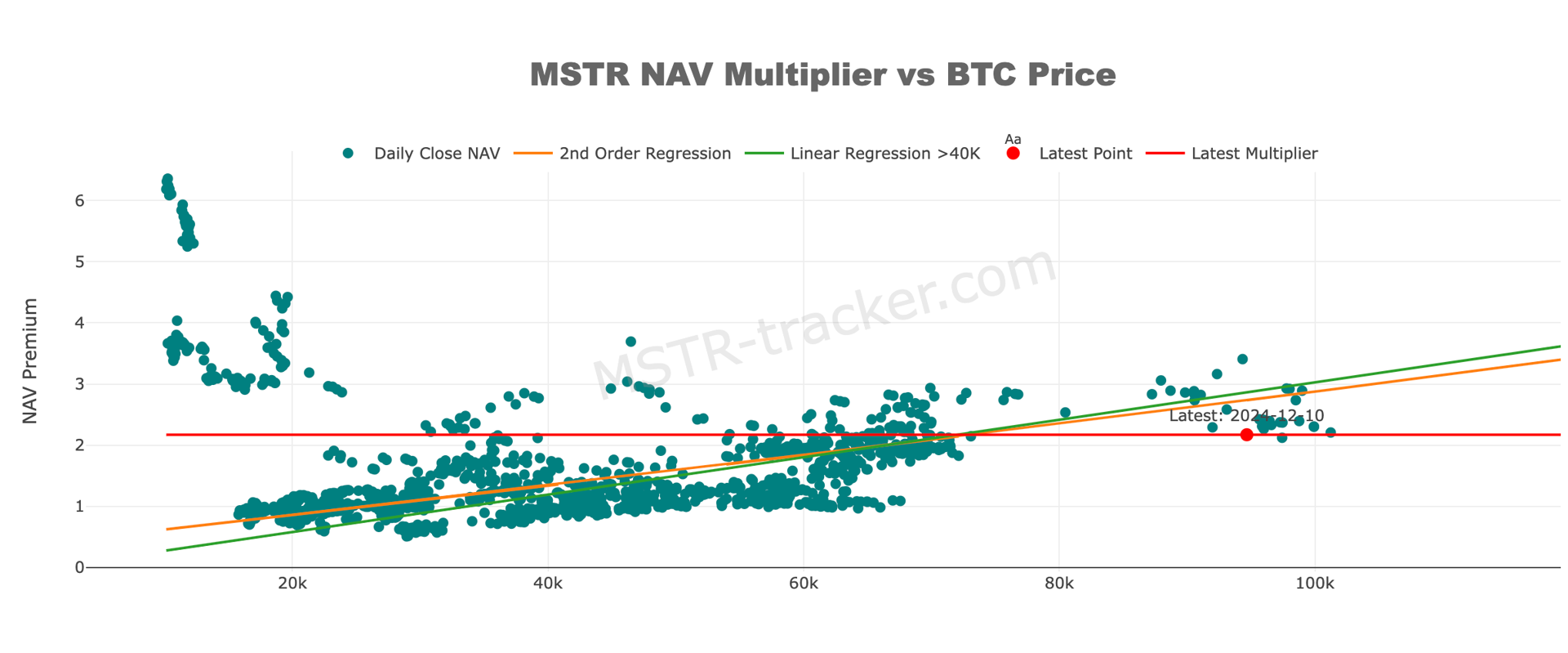

MSTR holds 402,100 Bitcoin. Those have a current value of $40 billion. We can figure out the value of Bitcoin relative to each share of stock, too. With 234 million shares outstanding, each share has a Bitcoin value of $163. With shares trading at $362, that’s a ratio of 2.2.

In other words, each share of MSTR is trading at 2.2 times the value of its Bitcoin. This is the NAV Premium.

I like this chart that shows the premium to the price of Bitcoin. The red line represents the current premium of 2.2. The linear regression suggests that as Bitcoin increases in value, MSTR’s ratio will increase. So, $120,000 Bitcoin could coincide with a premium of 3.75. That would give MSTR a price of about $772. Not bad!

But is that reasonable?

More likely, as Bitcoin matures, volatility will decrease. Then, the premium that investors are willing to pay for MSTR will decrease. Assuming that Bitcoin remains around $100,000, if the ratio were to decline toward what appears to be the all-time average of around 1.5, MSTR shares would be worth only $257. Given a premium of 1.5, for MSTR to remain at its current price of $365, Bitcoin would have to rally to $150,000. Possible? Absolutely. But when?

Here’s my point.

Relative to the price of Bitcoin, MSTR is long-term overvalued.

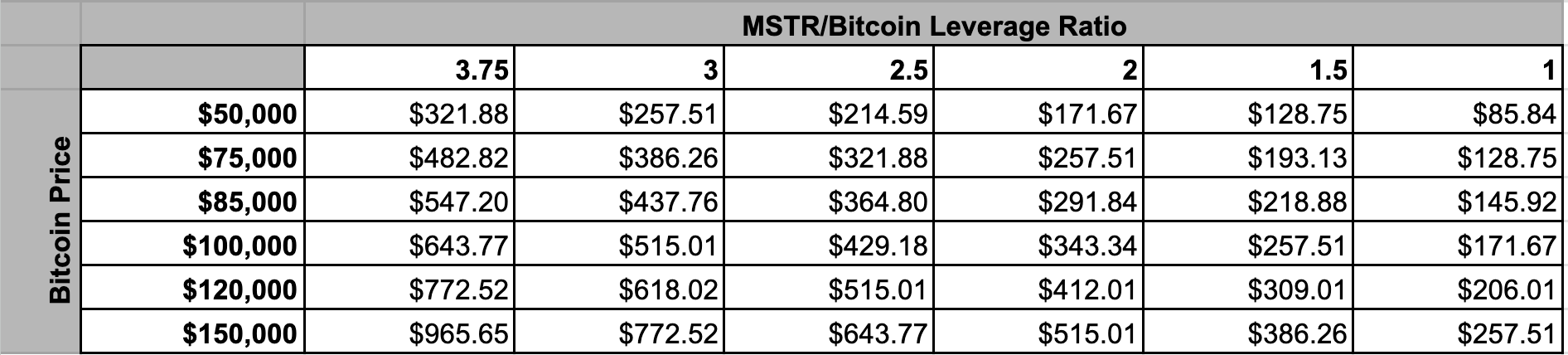

Here’s a chart I created that shows how MSTR could be priced based on different levels of Bitcoin prices and changes in the ratio.

Take your pick. Will Bitcoin end the year at $100,000? $120,000? $85,000? And will the ratio of MSTR to Bitcoin increase or decrease?

Despite the crypto win in this year’s election, our own Peter Tchir is skeptical that the incoming administration will follow through on some of its promises. Read about it here. Meanwhile, Maleeha Bengali makes a better-timed argument than the one I’m making today. She let us know that 3x was the wrong price to pay for MSTR, back on November 28, when shares were around $390. Read it here.

Combining Peter's and Maleeha’s analyses, you might say that all of the good news for crypto fans from November is already reflected in the prices of Bitcoin and MSTR.

Doug Kass would agree.

If that’s the case, I would expect Bitcoin volatility to decrease, if not its price. That’s bad for MSTR. Bitcoin is also about 6% off of its highs and could certainly continue lower without a catalyst.

If the leverage ratio declines back below 2x and Bitcoin declines by another 5% to 10%, MSTR will have a hard time staying above $300.

That said, in this market, I would never bet against MSTR. It’s a meme stock that’s got a loyal following and momentum on its side. In other words, it’s durable.

If you’re a sophisticated trader, then you know what to do with MSTR.

If you’re an investor, however, MSTR is not for you. If you want Bitcoin exposure, you’d be better served by buying the less-interesting product, and that’s Bitcoin itself, either through actual Bitcoin holdings or an ETF like the iShares Bitcoin Trust IBIT.

We live in interesting times. If you're an investor, your portfolio shouldn't be too interesting.

At the time of publication, Meshnick had no positions in any securities mentioned.