This Is the Kind of Market Structure We Usually See Before Corrections

Cumulative breadth remains mostly bearish with valuation extended.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As we close out trading for the first half of 2024, let's survey the market landscape.

The major equity indexes closed mostly higher Thursday with positive internals as only one posted a loss. Near-term trends are a mix of bullish and bearish projections while cumulative market breadth is mostly bearish and a concern.

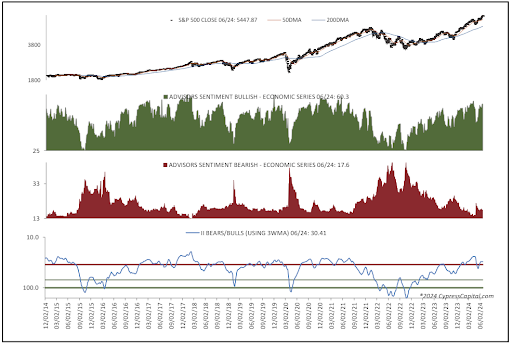

On the data front, two of the three psychology data points (contrarian indicators) are cautionary due to the excess of bullish investor sentiment. Additionally, the forward 12-month valuation of the S&P 500 remains significantly above ballpark fair value.

As such, we have not seen any shift in the weight of the evidence to imply a change in our current cautious approach to equities.

Chart Trends Unchanged at Bullish & Bearish

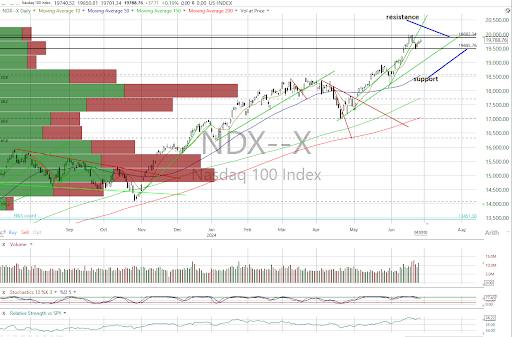

On the charts, the bulk of the major equity indexes closed higher Thursday with only the Dow Jones Transports posting a loss.

Most closed near the midpoint of their intraday ranges, which did not result in any changes in their near-term trends that remain bullish for the S&P 500, DJIA, Nasdaq Composite and Nasdaq 100 (see below) while the Dow Jones Transports, Midcap 400 and Russell 200 remain bearish.

We remain concerned regarding the bearish cumulative advance/decline lines on the All Exchange and Nasdaq that still show a notable weakening of the market’s foundation. They suggest an unstable underlying structure usually seen ahead of market corrections while the NYSE’s A/D remains neutral.

No stochastic signals of import were registered.

Digging Into the Data

The data remain mixed.

The 1-Day McClellan Overbought/Oversold Oscillators are still neutral (All Exchange: -4.52 NYSE: -7.62 Nasdaq: -2.19).

The percentage of S&P 500 issues trading above their 50-day moving averages (contrarian indicator) rose to 48% staying neutral.

Of note, the detrended Rydex Ratio (contrarian indicator) remains bearish as it slipped to 1.05.

Again, two of the three sentiment indicators are still cautionary with this week’s AAII Bear/Bull Ratio (contrarian indicator) a neutral 0.69, but the Investors Intelligence Bear/Bull Ratio (contrary indicator) (see below) staying bearish at 17.6/60.3 as bulls well outweigh bears.

The Open Insider Buy/Sell Ratio remains neutral at 32.7. However, insiders have been on the sell side over the past several sessions.

Leveraged ETF sentiment is 5.1 remaining neutral.

Valuation Extended

The 12-month consensus earnings estimate for the S&P 500 from Bloomberg lifted to $253.53 per share. But its forward P/E multiple of 21.6x remains well above the “rule of 20” ballpark fair value at 15.7x. It is an important concern for us as an almost 600-basis point premium remains significant.

The S&P's earnings yield is 4.62%.

The 10-Year Treasury yield slipped to 4.29%. Support is 4.18% and resistance is at 4.35%. Its near-term trend is bearish.

The U.S. dollar, via the UUP ETF, closed lower at $29.13. Its trend remains bullish. Support is $28.89 and $29.23 is resistance.

Bottom Line

The fact that the number of stocks lifting the averages has been notably shrinking while losers have increased implies a weak foundation. Meanwhile, valuation and investor sentiment are flashing yellow lights. Thus, caution remains appropriate, in our opinion.

We continue to believe the best course of action is to honor sell signals on individual names as we remain extremely selective on the buy side.