Looking for a Reset, After the Holidays

Markets tend to need a reset at times, and this one surely does. But it's most likely after a holiday. We ought to get that in the others/the 493, because that’s where we are most oversold.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Since the August low, the S&P has been one giant group rotation. Most of tech sat it out during the summer, including those index movers, or Mag 7 or whatever you want to call them. But certainly the hot semis of the first half have not participated much of the second half of the year.

The banks and industrials were the go-to stocks. Then in September/October software started to emerge as did the smaller tech stocks. That’s when industrials and financials backed off. Oh sure, some groups went on to make higher highs in the days post the election but the majority of stocks are now trading under where they were the day after the election.

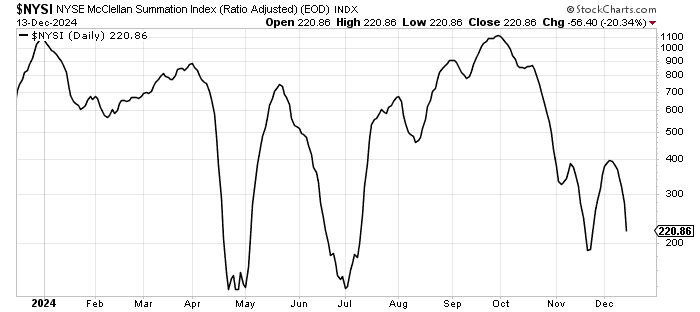

Just look at the McClellan Summation Index. It began its trip down in early October and has barely recovered. Since then, the S&P is up five percent. This means the narrowing in the market didn’t start at Thanksgiving, it really started well before that.

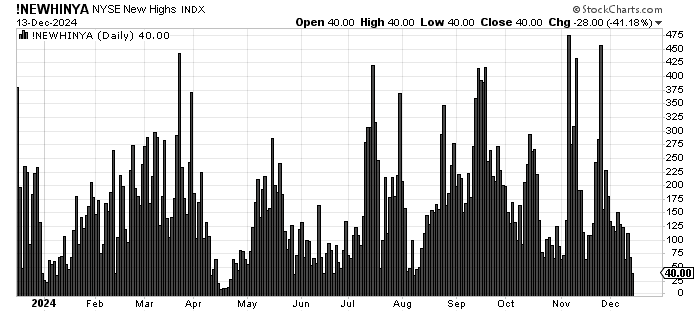

Look at the chart of stocks making new highs, and you can see it more clearly. Sure, we had a peak of 475 new highs on the NYSE the day after the election, but we had 423 in mid-September. Is 50 more stocks making new highs really a big expansion? We have mostly seen the number of stocks making new highs dwindle as the S&P has climbed. That’s not broadening, it’s narrowing.

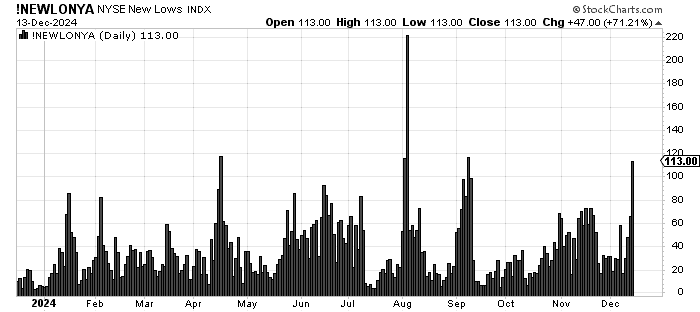

Now look at the number of stocks making new lows since that October peak in the Summation Index. It was a steady rise into the election, we backed off a bit but in the last week, they are surging again with Friday’s reading clocking in at the same level we saw in September when the S&P was more than ten percent lower.

In that time, we have seen bullishness rise to levels of euphoria in some cases. The Citi Panic/Euphoria model sits firmly in Euphoria. The 10-day moving average (and the 30-day ma for that matter) is near lows last seen in July of this year (right before the August whoosh) and in July of 2023, right before a ten percent pullback in the market.

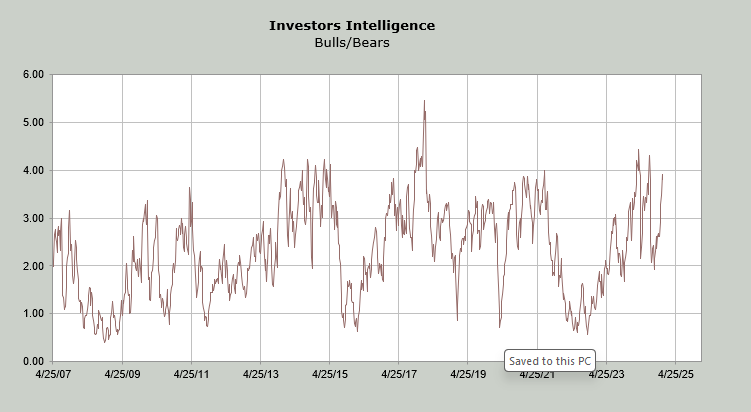

The Investors' Intelligence bulls are 63%, while the bears are in the teens. The ratio of bulls to bears sits at 3.9. Readings over 4 have tended to tell us that’s ‘enough,’ and the market usually corrects from there.

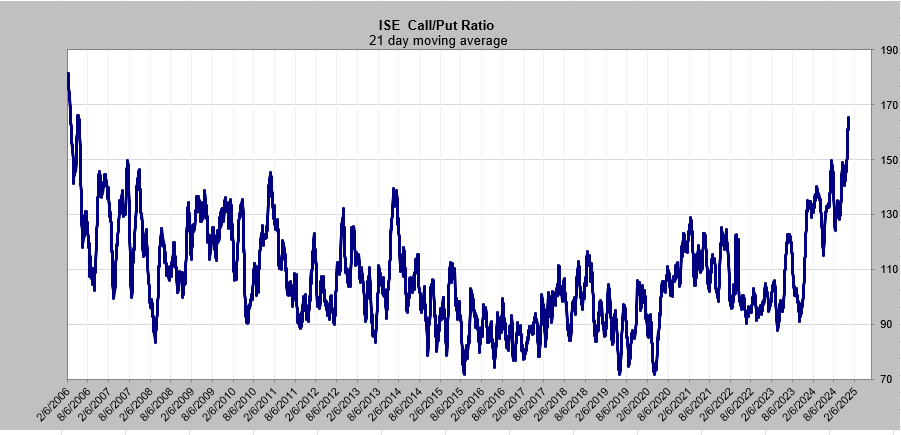

The ISE Call/Put ratio’s 21-day moving average is now sky high, the highest it has been since the spring of 2006 (that’s when they started tracking data). Sure, it can go higher, but take a look at the S&P in the year 2006 and notice that there was an eight percent correction that spring/summer.

Markets tend to need a reset at times, and this one surely does. But I did say in the shorter term, I thought we’d get an overbought pullback in early December, and we have. I also said I expect we would have the traditional Santa Rally which tends to show up right before Christmas week. I still believe we will get that. We ought to get that in the others/the 493, because that’s where we are most oversold. Heck, wouldn’t that just be more of the group rotation we’ve been seeing?

But, I don’t believe the last few weeks have done much to temper sentiment. That’s why, after an oversold rally, I would expect the market to have a more substantial correction.