Live Quarterly Meeting Transcript: Peter Tchir on Geopolitical Risks, Inflation, and Rates

Our summer investing road trip transcript of Peter Tchir's presentation from July 23rd.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Thanks very much. So, just by way of background, because I think it'll help everyone understand where I come from, I started my career late mid-90s at Banker's Trust, then Deutsche Bank, really in the credit derivative area, structured products. Did a lot of esoteric, funky, high-yield type stuff. I ultimately wound up running the credit beta businesses at UBS and RBS where that was really the credit derivative indices, the ETFs. Was really involved in that fairly early on.

Read All the Live Quarterly Meeting Transcripts

- Maleeha Bengali on Interest Rates, Crude Oil and Bitcoin

- Chris Versace Shares 3 Picks From the Portfolio

- Helene Meisler Offers Investment Ideas to Watch

I've traded about $1 trillion of credit. So fixed income is kind of a background. When I think about macro, I think about it really from a fixed income first perspective, a trading, a positioning kind of standpoint. All that's from that background. I continue to do that. I've been at Academy Securities for about eight years right now. And what's unique is, instead of just talking to asset managers, I actually spend now a lot of time talking to corporations as well as municipalities and state governments.

So, I get a very different perspective, what they're seeing in the world, how they're viewing it. I think that's helped branch out. And then at Academy I've got right now 22 generals and admirals retired who serve as our geopolitical intelligence group. So, they look at the geopolitical landscape. I take a lot of their input. And in many cases, it's very relevant to what we're seeing in this world. I think Bank of America just did a survey of their customer base, and geopolitical risk showed up as their number one tail risk. Jamie Dimon talks about it all the time.

Geopolitical Risk

And so I'll try and go through those two things as I funnel this into my market outlook. And if we want to skip to the Geopolitical Risk slide. So as I've been going through this, I think a lot of people talk Geopolitical Risk, but then they're like, [GROANS] It never does anything. How do you think about this? How does it work? And so, what we're starting to do is, I really think about tactical risk versus strategic. And tactical is when Hamas attacks Israel. Very quickly, how do we think Israel responds? How long does this last? What are the repercussions? How does this work?

And I think that's very helpful in terms of thinking about, OK, what's this going to do for rate market, short-term? What's it going to do for commodity markets in the next week, months? How do we deal with this? And right now, when we think about tactical, right now, Russia, Ukraine is still very much tactical, right? There's some ebbs and flows.

I think we're drawing to the conclusion that this is largely just a stalemate and that probably both sides, regardless of who wins, are going to start pushing towards some sort of an endgame there, where I think our base case is Ukraine gets forced to give up some land, Russia gives up some of their frozen dollar reserves, and some of that goes to repay our equipment. Some of it goes to help rebuild Ukraine. No one's exactly happy. And some mechanism is put in place so that Ukraine has a path to NATO so that this doesn't happen again.

I think both sides are going there. And when you just look at what we've been doing with Ukraine, it's really a shortage of manpower that's their issue. But also, we constrain them every time. We don't give them enough weaponry to do what they need. We restrict where they can use their weaponry. So, it's just kind of bogged down. And we think, from a geopolitical standpoint, that whoever wins will start putting pressure on both sides to come to some sort of truce.

The Middle East, I think the key takeaway here has been that Saudis and most of the Middle East has not wavered from the Abraham Accords progress. Yes, they're not proceeding right now with the Abraham Accord, but there was plenty of opportunity in the last eight months now, I guess, to turn against Israel. They're not. Most of the Middle East is still very anti-Iran. They really helped when Iran launched the missile and drone attack against Israel. So I think that's been probably one of the best outcomes here, is just how steadfast the Middle East has been kind of on that path towards, What's the Middle East of the future look like? Rather than getting bogged down with Iran.

Venezuela and North Korea are kind of wild cards. I would say, the other two things, we're getting more and more questions about shipping, which I won't go into detail on now. But I would say, to summarize, shipping was always a given. You just kind of, OK, it might take x plus or minus y time to get here. And maybe the cost has a variable. I think people are really having a little bit more existential questions about shipping.

We saw China stop shipping during COVID. We're seeing various parts of the world right now, the Panama Canal still somewhat slow due to weather. We've now seen what's going on in the Middle East due to the attacks by the Houthis. And geopolitical inflation, I put it in red because I think this comes across. And this is why I'm so bullish on commodities is almost everything that's going to happen tactically will be inflationary from a geopolitical standpoint. The geopolitical risk will affect commodity prices, particularly energy prices. So that's where we kind of keep with that.

On strategic, I would say China is the biggest thing. And it's really hard, I think, for investors to see it because, OK, this is playing out like a slow moving ship. It's not happening today or tomorrow. For the last probably seven years, I've had the pleasure of working with General Walsh. He was actually part of the group that put together the national security paper that first labeled China as a strategic competitor.

So I think we've been more negative on our relationship with China than Wall Street. And every time Wall Street tries to catch up to us, we've moved a little bit further. We're finally closer. I think the most important takeaway here for you as investors is, whatever is going on with chips is not going to change. So these chip fears are national security and whoever wins again, will be read in on all the things that are going on. So AI and military chips off the table, that's not going to happen.

And I've been watching what happens in DC a lot. And you kind of get these peaks and valleys or ebbs and flows, right? Something becomes topical and dissipates. Nothing about the chip side has been dissipating. If anything, over the last month, what I'm hearing more and more about is dual-use chips. So, yes, it can be used in a washing machine, but yes, it can also be used in a drone. So if anything, I think the risk is more restrictions on the chip industry. I know they're lobbying hard to keep this reasonable, but I think that battleground and chips is going to affect everything going forward.

India isn't my favorite place. I think that will get growth. It'll get traction. It's kind of awkward. We do these geopolitical presentations and you raise your hand and want to talk about India. And everyone's like, Well, India is not really geopolitical. Yes and no. It is, though, going to be this huge opportunity. And one thing I want to highlight, so when we talk to corporations, I think, say you talk about reshoring here, or reshoring Mexico, or you pick your country.

But in most cases, it's about manufacturing. There's not really this view that it might also turn into a huge consumption or actually buyers of your products. India has that for them. And India is great in AI. And more and more you're going to be hearing about the rare earths, critical minerals. I know been talking about this for a while. And sadly, I used to say this about five years ago half jokingly, and unfortunately it's almost still half jokingly, but we've had this vision of where we want to be. No plan on how to get there.

China has absolutely zero vision on sustainability, but a great plan on how to get there. So that's kind of been the issue. We're behind on a lot of this. And it doesn't get a lot of attention, especially with all our domestic issues right now. But North Africa and Africa as a whole is becoming very problematic. Russia and China have great influence there. There have been multiple coups. Our influence is decreasing. And that region is going to be critical to secure the rare earths and critical minerals that we need.

And we are also going to have to figure out, hopefully, again, no matter who wins this, some way to start processing more and more. I think the US has had this mentality like, yeah, we'd love refineries, but not in our backyard. Yeah, we love wind farms, but not in our backyard. So you've seen a lot of pressure on that. The processing of rare earths and critical minerals, where China does somewhere over 90% of that, is going to be crucial to our national security. That's going to have to happen.

And again, I highlight geopolitical inflation. Almost everything we've just discussed is going to have inflationary elements for the next few years. So that's kind of a backdrop for me on how to think about geopolitics as you're looking at your portfolio right now.

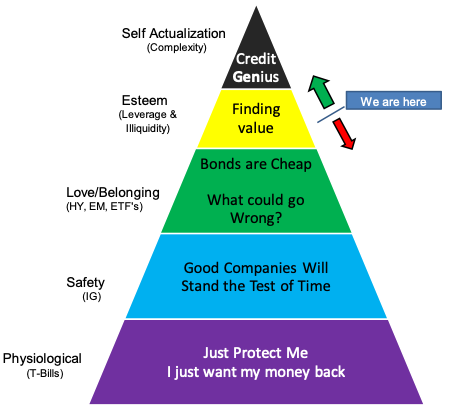

Maslow’s Hierarchy of a Credit Bubble

And then I get asked a little bit with my background, What do we think about markets? What do we think about credit bubbles? And I would say, since the financial crisis, there's an entire I'll call it a "cottage industry" of people who want doom and gloom on the credit market. It just sounds sexy to say, Credit is going to blow up. There's too many BBB credits in the world.

There's also, I think, now increasingly a doom and gloom crowd about the US fiscal deficit, and the budget deficits, and the ongoing amount of debt outstanding. Those are legitimate concerns. So I've used this Maslow's hierarchy of a credit bubble to try and frame how I think about credit markets and fixed income. And partly it shows that I took Psych 101 in college and that it was somewhat useful. But when you think about this, Maslow says you have to fulfill one level before you move up to the next level, or vice versa on the way down.

And during the financial crisis, you were right in that T-Bill, Physiological. People wanted safety at all costs. We've been moving up. And I put us in what I call this "Finding value" range right now. There's a little bit of leverage. People are taking on lack of liquidity. There's more and more structure coming in. But we're not to that Credit Genius stage where we were before. And if we pull back, it's going to affect the bond market a little bit, but it's going to be more high-yield, EMs, some of the ETF rates.

I think investment grade is incredibly safe. I love the municipality side of things. So I'm very comfortable with credit as a whole. I think it's very balanced on what's moving it next, whether we continue to go tighter and get a little bit more aggressive. Like everything else, and I think Helene did a great job, this tends to ebb and flow, right? When you get to Credit Genius, getting there makes everything go tighter. Once you get there, it makes any problems escalate and you tumble way down. We're not there.

I would say the one thing I've never considered in this is that the Treasury market would become the problem, that it would be T-Bills or inability or unwillingness to pay. I think we saw some of that last September and October when every single day, the Treasury market was up for sale. No matter what the economic data was, 10 years went from 4% up to 5%. I think we're going to get more and more bouts like that where people really worry about the deficit. But that, to me, is a 3, 5, 10-year problem. It's not going to mount up overnight.

People talk about supply, but these things get issued all the time. People also never really talk about when they talk about Treasury supply, how much redeems every month. So the bond market's fairly good at adjusting to this. It takes time. I think it will have a creeping effect of having higher yields at the long end, but nothing dramatic.

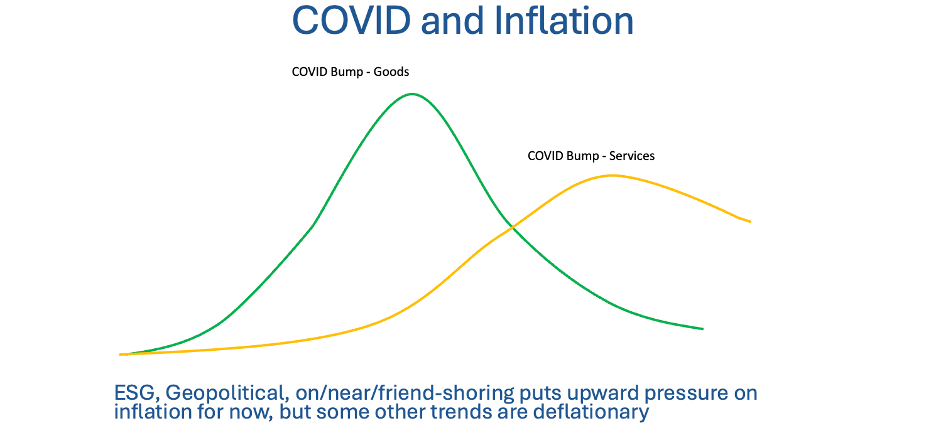

Covid and Inflation

Now those two things let me tie into my Rate Outlook and Market Positioning. We hop to the next slide. And yes, so obviously, Inflation. We talked about Geopolitical Inflation. Inflation is going to affect the Fed. I think we're getting inflation coming down and that's what's going to elect the Fed to act. And this has been very simplistic. And my charting technology is incredibly simplistic and probably bad.

But how we viewed inflation, it's turned out, I think, to be exactly spot-on, was you had these bumps due to COVID. And goods spiked very quickly. Once people could buy goods, they had a lot of money from all the COVID money that had been sent. And people would go into the store and say, well, you know what? I'm going to buy the bike and the skis because who knows what will be available next time I go in.

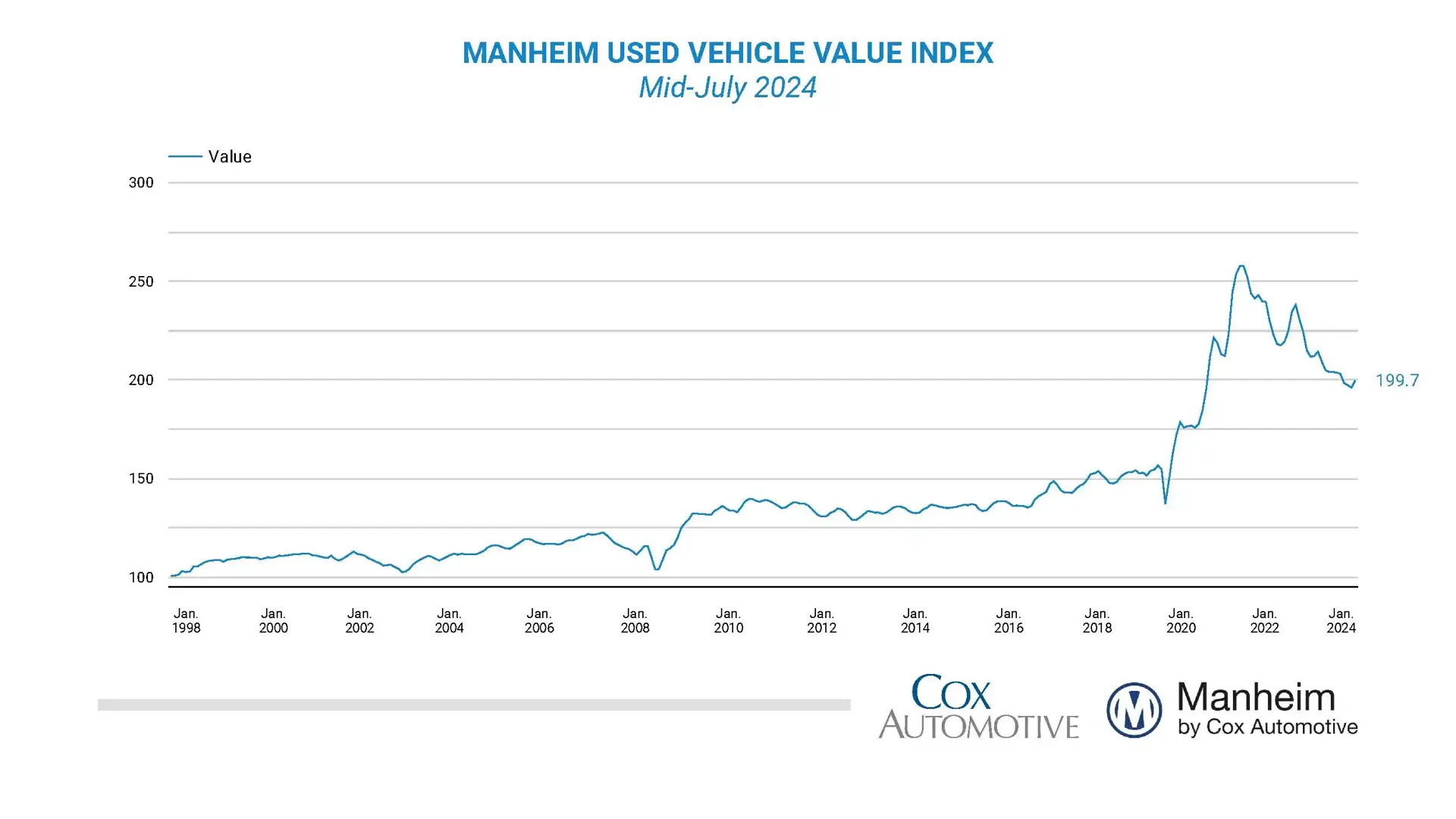

You had this massive spike. You had this whole change too where all of a sudden people were work from home. People were spending outdoor time. So they loaded up on those things. So you saw this massive spike. And it's been going down fairly quickly. I always look at the Manheim Used Auto Index. It's coming down. It's still higher than it was pre-COVID. But it's given up almost all those gains. And it had that parabolic shape.

On the services side, it's been slower to go up. Partly every single state and country had their own rules about when you could participate in various things, when you could travel, when you could go to hotels. More importantly, I think individuals had their own set of rules. I might be comfortable getting on a plane and traveling tomorrow. You might not have been. So it took longer for that surge.

And we've been calling the summer of 2023 at Academy, The Summer of Vacation. And everyone was hell-bent on taking their vacation. I'm taking my two-weeker. I'm going. I'm locking my family. We're doing whatever we promised to do because we've had such an erratic time. You're starting to see that tail off. Less and less vacation. Some of the corporate travel slowing down again. So I think that's declining.

And that's the backdrop, when I look at it. Right now, I believe 20% of items tracked by the Fed for CPI are now actually in deflation mode. And about 70% are actually at 2% or below annualized for the last three months. So this is all coming through. The inflation fears are over. You have this geopolitical that's going to artificially keep inflation a little bit higher than it would be, but the normal things are coming down. I think we're going to be in this 2% to 3% range and that's going to give the Fed the ability to act. Which ties into my rates calls next.

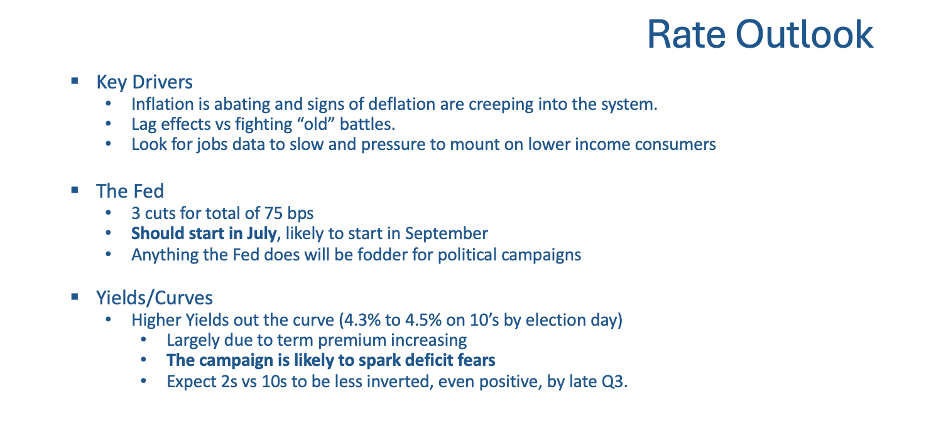

Rates

We talked about this inflation coming down, the lag effects. When I talked to the real insiders right now, the Fed is very torn on cutting. And the Bank of England loves dissent. So the Bank of England, when they do it, they actually really vote honestly. The Fed hates dissent. So whenever they put out their dissent, it's always almost unanimous or maybe one on either side. Right now, what I'm told, it's pretty contentious. Close to half the Fed [AUDIO CUTS OUT BRIEFLY].

The people who don't want to cut are fighting old battles. They're either fighting that they miss transitory or back to the '70s where they took their foot off the brakes too quickly. I think we're going to get three cuts. I think they should start in July. I think the first time they cut, all hell is going to break loose on social media, where they are being portrayed as helping the incumbents. I don't think they are. But for that reason, I would cut in July.

We'll get PCE data on Thursday. I'm hoping it gives them the rationale to start in July. I think all else being equal, they would have started in July or maybe even last month. They're just so cautious. They're feeling that. So, I think that's going to be-- you'll see front-end yields go down a little bit. A lot of that's priced in. I do think 10-year yields are going to stay in this. 420 to 450, 430 to 450 range. And you're going un-invert the yield curves finally. Which turned out to be the worst recession signal ever. [CHUCKLES] We've sat here, I think three-some-odd years now with inverted yield curves.

2s, 10s is going to go back to zero a little bit. So, you're not going to get this massive rally in duration, which leads me to where my favorite trades are right now.

Ideas

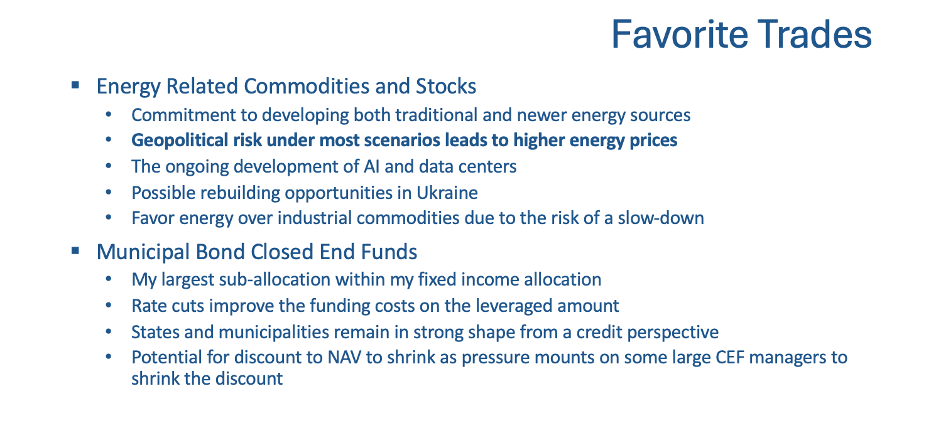

I love energy-related commodities and stocks. Partly, I think they're the greatest geopolitical risk hedge right now. I also think what's going on with the data centers is great. When I look at various administrations, I think how they do it will be a little bit of a difference, but we're going to build out the chip industry.

We are, finally, I think, understanding that to get to sustainable energy, we have to build sustainable energy faster and more quickly than we've been. But we're also going to have to contain and build more traditional energy sources. So, I think that's going to be a lot of spending. There's going to be a lot driving this. In three to five years, you'll probably go over this hump where some of it becomes deflationary. The wild card to me here is India. If India gets their act together, you will see global inflation, possibly like we saw with China in the mid-2000s.

And, if you watch India and listen to their politicians, they are all about access to commodities. They see that potential. It's one reason they're in Venezuela. It's another reason why they continue to trade with Russia. So, I think there are so many reasons to like commodities. Data centers on the positive side. India growth on the positive side. Geopolitical Risk is kind of a negative reason to own it, but still a reason.

And then pulling away from that, I still love, and it was my start-of-year report, Muni Closed End Bond Funds. I really like them. I think that's the best place to be where you can get yield. You take a little bit of duration risk. You take a little bit of leverage. If I'm right, yields still stay higher, so you don't get a big price appreciation right now. But you've already had some nice price appreciation.

You do get your cost of funding on the leverage to go down a little bit because the closed end funds will borrow slightly better. And certainly Boaz Weinstein, amongst others, have been leading a charge trying to get discounts to NAV going down. And when I look at this, normally we're at 6%, 7% discount to NAV on a lot of the closed end funds I like, down from 10% to 12%. I think there's room for that to go down to 3% to 4%. So I'm not yet trying to trade out of that, trying to capture some of those gains, but I am watching that.

But that's my favorite. When I think about where I want my fixed income portfolio to be, that's my biggest and by far heaviest allocation is to the closed end bond funds. And on the equity side, I really do like the commodities stocks better than anything else right now.