Live Quarterly Meeting Transcript: Maleeha Bengali on Interest Rates, Crude Oil and Bitcoin

TheStreet Pro's Maleeha Bengali shared her insight on interest rates, crude oil, bitcoin and more during our "Summer Investing Road Trip."

You've reached your free article limit

You've read 0 of 1 free Pro articles.

TheStreet Pro recently hosted our Live Quarterly Meeting around the theme of a "Summer Investing Road Trip."

It was a chance for our subscribers to hear firsthand markets insight from some our leading contributors at a critical point in the calendar. Below is a transcript of commentary from MB Commodities Capital CEO Maleeha Bengali, who touched on how looming rate cuts will impact the market, weakening demand for crude oil and the growing influence of bitcoin.

Read All the Live Quarterly Meeting Transcripts

- Peter Tchir on Geopolitical Risks, Inflation, and Rates

- Chris Versace Shares 3 Picks From the Portfolio

- Helene Meisler Offers Investment Ideas to Watch

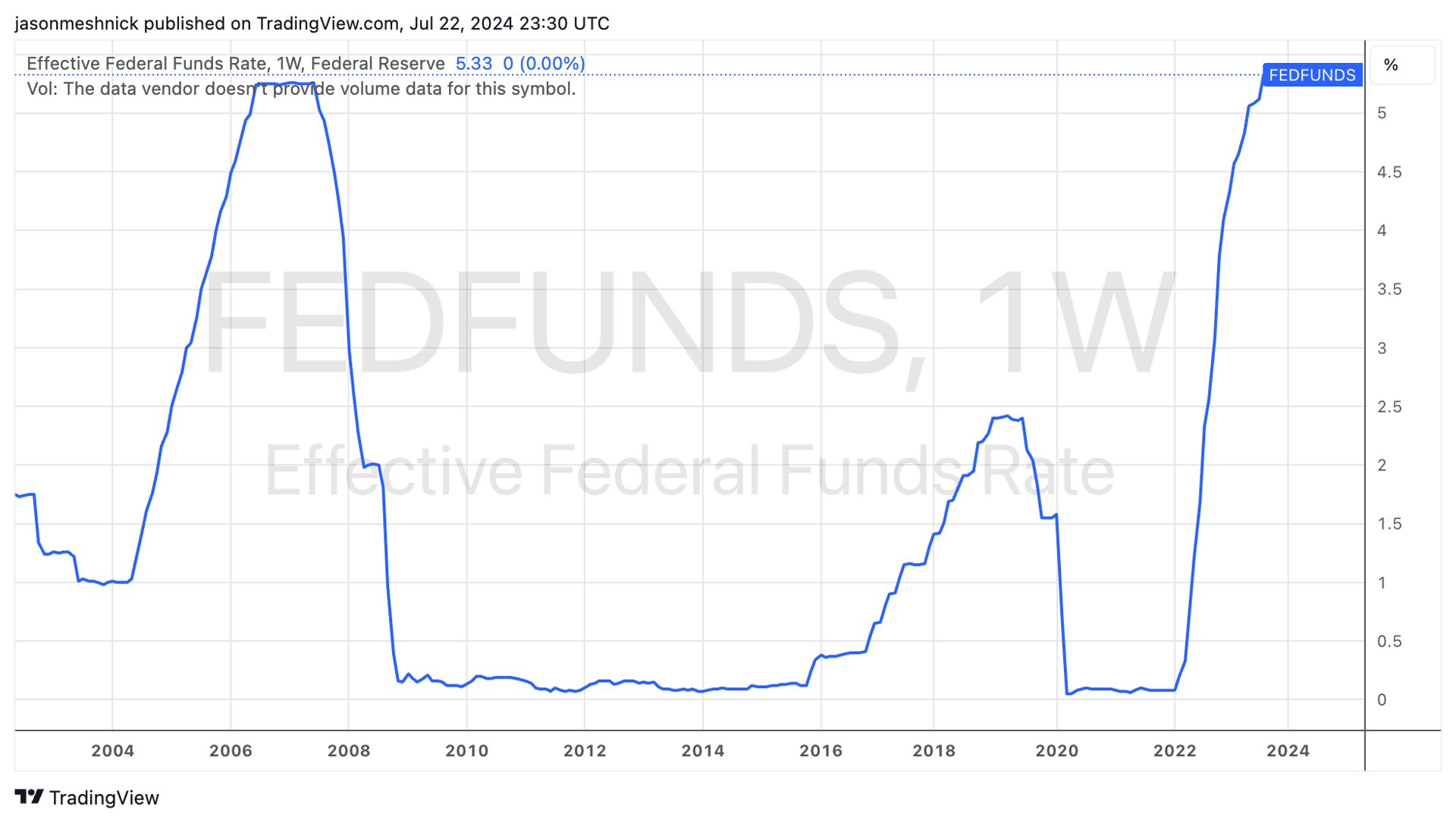

The Fed

OK well, thank you very much for having me on. It's fantastic. It's very topical right now. So let me first talk about The Fed, because I think that's something that's on a lot of people's minds as to this rate cut. Let's go back a year. Last year, every single equity sell-side analyst came in predicting a recession. Given the rate rises, we've seen 500 basis points in a matter of 12 months. Inevitable that there would be a recession. That didn't happen.

So obviously we've had so much fiscal spending in the US that that's masked the weakness in the economy. So we fast forward 15 months, and now pretty much everyone's given up on the recession. The market has been pretty much a two-tier economy. You've seen seven or eight stocks, The Magnificent 7, do really well. But every other sector in the market has been falling. So the Fed's in a bit of a pickle right now, because what they really need to do is actually cut interest rates as they're too high and they're too restrictive. But they're not seeing the evidence of that just yet, because obviously the indexes are high and your PMIs and ISMs are weakening, but they haven't really fallen off.

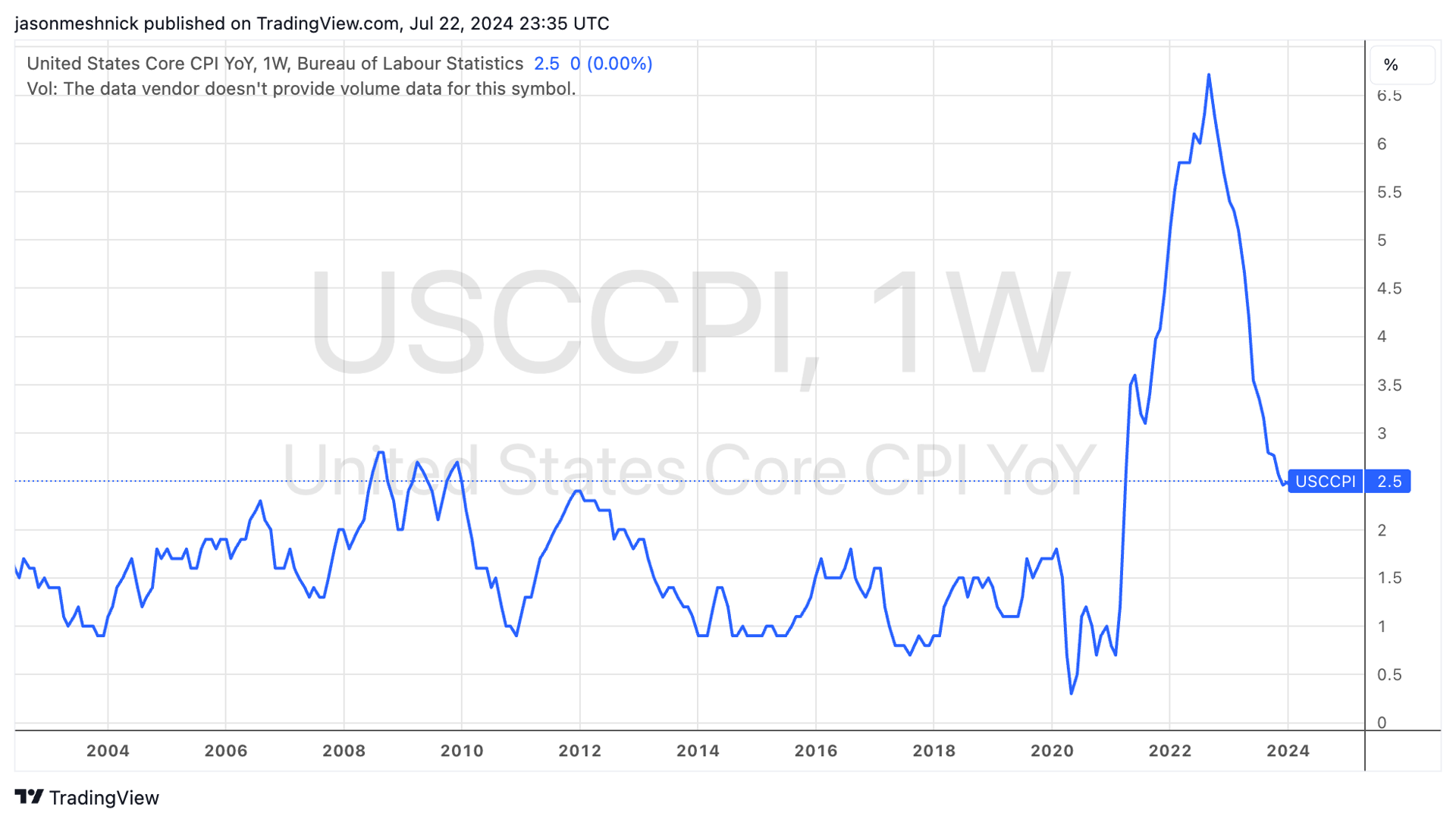

And the other thing is inflation. This chart tells you exactly. They've done a great job in lowering the inflation and they've been patting themselves on the back in terms of immaculate disinflation. They got lucky with the fact that China's been slowing down. That's helped them bring these prices down. But we think it's been actually too deflationary, that inflation was an issue, but right now, the Fed probably has tightened too much.

Why do we say that? If you take a look at the manufacturing side and the services side, the manufacturing side of the economy is not picking up. I mean, we've seen it this rolling goods recession due to China's weakness, but then we see services doing really, really well. The last month, May and June, we've actually seen services roll down as well. And that's really the difference because most people expect manufacturing to pick up second half of this year. And they want to be long the S&P. They want to be long Global Recovery.

We are we seeing it the other way around. We're seeing China's weakness filter into much significant weakness. And the US, for instance, the Fed right now has got his hands tied because inflation has come down a lot from the 8% or 9%. But we're still averaging 2.5% to 3.5% And we know that those are just headline numbers. The actual inflation US consumers are facing is probably not the 25% on a cumulative basis. So they cannot cut right now, even though the economy and the financial system, the bank lending, mortgages, every single part of the economy needs it really badly.

We're seeing the most bankruptcies now than we've seen since 2008 in terms of small and medium enterprises where if they cut too soon, as in July, there'll be too much inflation. And then they've lost the battle. But if they cut in September or later, it'll be a token one cut. And most people are assuming the cuts are going to save the economy magically. It doesn't happen that way.

Back in 2008, when we were in a recession, the Fed cut six or seven times before the market actually rallied. It fell a lot harder. So we take a step back and talk about top-down weakness. We want to talk about the physical markets. And we can talk about exactly what we're seeing in commodity markets.

Crude Oil and Commodities

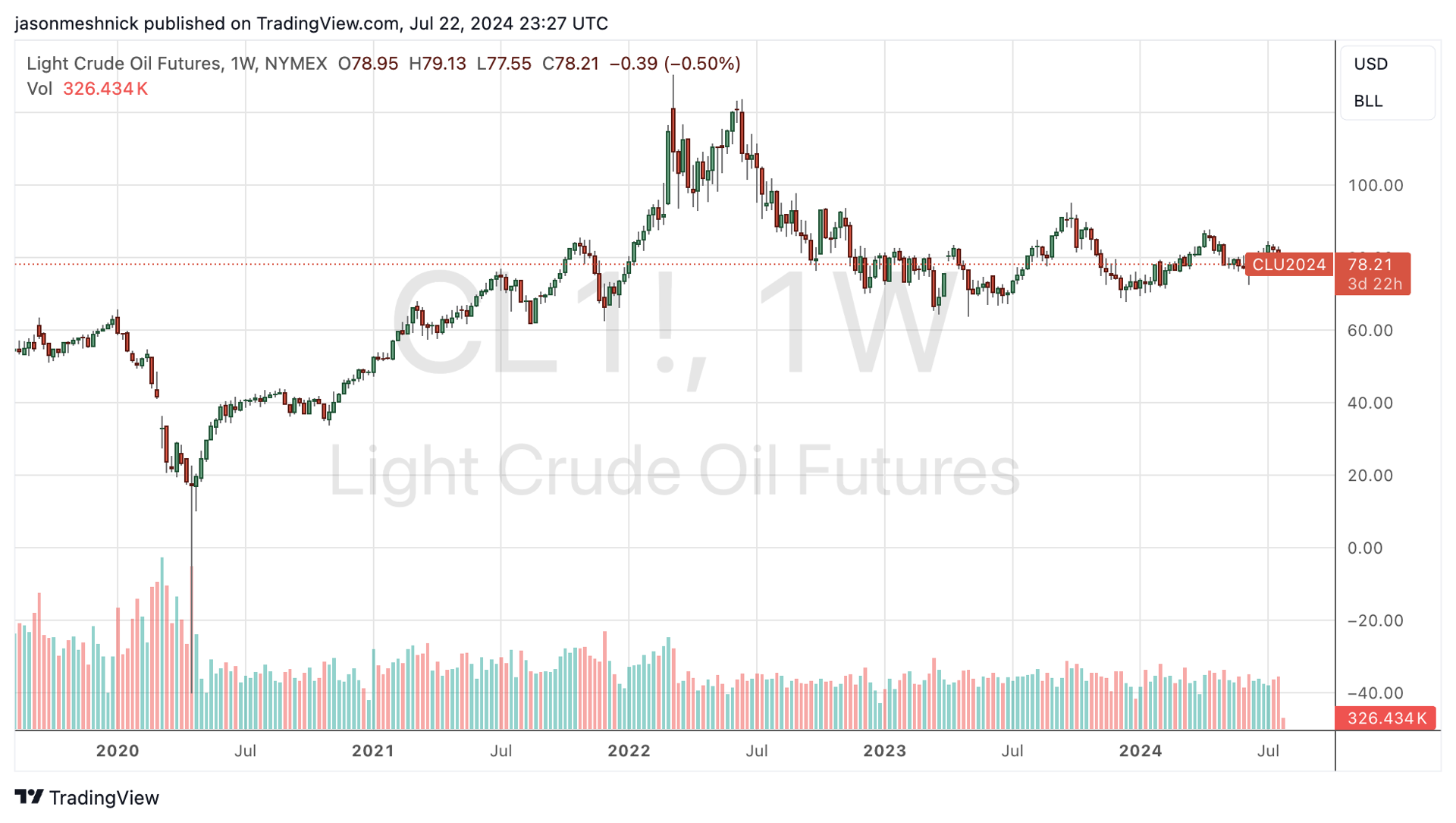

Now talking about oil, oil's been a very interesting sort of commodity right now because obviously, most people are playing this magical rotation, selling technology and buying crude oil, the massive growth versus value tech trade. It is the ultimate trade for 2024. But timing is just not right. Why? OPEC is taking about 6 million barrels of oil out of the market right now. And just because they've tightened supply, people assume the demand is going to go up. Now, that's really interesting, because demand has been weakening. And that's what we've been saying for the last eight months.

China's demand numbers from OPEC assume that China's going to grow 1.5 million barrels per day magically. They're not. China's first half numbers are actually showing the demand fell, did not go up. So the window is getting narrower and narrower as to what China can do. But China has no more bullets left. We saw the [INAUDIBLE] right now. Xi Jinping cannot go on a massive bazooka stimulus. China is seeing a perennial decline in the economy, the property sector bust. They've got a domestic consumer demand problem.

So, the entire Western world is waiting for China to actually come up with a trillion dollar stimulus, which is not happening. So, OPEC is sitting there, assuming demand is going to pick up. We don't see it. In fact, we see demand weakness across distillates, around gasoline, around every sector in the market, taking oil prices down. So just because it's cheap, our view has always been that commodities do not care how cheap it is, if the demand is not there. We know the supply side, but the demand is getting weaker and weaker, so prices are falling.

And this is surprising a lot of hedge funds because they are playing this long energy trade. But it doesn't work that way. Your timing has to be exactly right on the bottoms-up side. Same thing in copper. Look at copper. Everybody's so gummed up on copper in terms of the data center, power demand, which we believe is going to happen. But that's a 2030, 2035 story. It's not going to happen today.

Today, it's China's demand from the copper side actually is very weak. And that's 30% of copper demand comes from China's property market. So we're seeing that filter through. So there's a short-term trade and a long-term trade. And I think most people in the market, traders, hedge funds are looking past the weakness by saying, Oh, the Fed cuts are going to save all. We don't think so. We think they've over tightened. We are probably in a recession right now. Most people do not expect it. And I think they'll be surprised as to how weak Q3 is going to be.

And then we have all the political uncertainty right now, right? We have fiscal policies that's pretty much played its course all throughout the last three years. We have US national debt trading at $37 trillion. We have debt to GDP is close to 150%. Where are we going to go? Today every dollar we're printing, only half of it is going to productivity. We're printing more money to pay back old debts. So this AI productivity boom that everybody talks about is not going to save the US market.

And I think that's really the dilemma and that's how we solve standards very different compared to other analysts. So the dollar is still very strong. We can talk about why silver, and gold, and copper are all doing well because the dollar is higher for longer because the Fed is going to be very, very late to cut. As always, they always wait for an emergency and then react as opposed to pre-empt it happening. And that's the reason why commodities are weak.

Bitcoin

While the whole world, like Japan and China, are waiting for the Fed to cut because their own currencies are in massive decline, almost at devaluation territory. And that's sort of another issue, which is a very, very important point to talk about. We can quickly touch on Bitcoin. Now Bitcoin is something that we love, but it is not a replacement to gold. It is another alternative digital asset class. And we think the future of fiat currency debasement about the debt we were talking about, there will be more upside.

But Bitcoin is not going up in a straight line. It's a very speculative asset class that's driven by Fed liquidity. It is not like gold or silver, even. So, why is Bitcoin doing what it is? Yes, there was a massive ETF launch. There was a lot of money coming in right now. But if the dollar stays higher, and right now liquidity is cold, Bitcoin is going to get hit too, versus with other soft commodities. And we are all in the crypto summer. Bitcoin, as an asset class, has changed because it's not just traded by cryptocurrency traders. It's become a macro asset class.

So if we see a risk of deleveraging event, Bitcoin is going to get hit too. So short-term, pain. Long term, we see massive upside. We can see Bitcoin falling to maybe 60 or 50, even lower. If we see a massive recessionary risk on the tape right now or dollar collateral shortage, Bitcoin will get hit too. But long term, we know that there's only one eventual fate of the US economy. They'll have to print even more and cut even more. We don't see rates going back down to 0% to 2%

Most people assume that that's the normal world. But when I started my career, 5%, 6%, that's the normal world. The 0% rates that we've had for the decade, that's not going to happen anymore because we have too much inflation in the system. So we have to live in a world where we have between 3.5% to 4.5% rates or even 5% and sort of adjust our risk preferences and assumptions based on that. And I think that's going to be pretty much a game-changer because the next 10 years are not going to be like the last 10 years. But the only problem is that everybody who's trading or managing money is so used to that playbook, they sort of enacting the same sort of investment bets.