Let the Earnings (Really) Begin

We've got a mixed bag with Alphabet, Snap and Visa moving up as Chipotle, SoFi and others take it on the chin. Let's check the macro, rates and a plan for AMD.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As the closing bell finished ringing both at 11 Wall Street and at Times Square, it did not take long for the high-profile corporate earnings to start pouring in. The busiest week of third-quarter earnings was underway. On Monday, Ford Motor F had disappointed. On Tuesday morning, someone punched SoFi Technologies SOFI in the mouth (this stock did need to consolidate), while McDonald's MCD failed to impress.

That was, however, before the music really began. On Tuesday afternoon, what was described as the busiest week of this earnings season or really the busiest two and a half days (through Thursday night) of earnings season kicked the pace of high-profile releases into the next gear. Overnight, after earnings: Alphabet GOOGL, Snap SNAP, and Visa V moved higher, while Advanced Micro Devices AMD, Qorvo QRVO, and Chipotle Mexican Grill CMG all took one on the chin. Reddit RDDT, while not quite on the same headline level as these other names, was up more than 22% after posting a surprise profit.

As we work our way through the zero-dark hours of Monday morning, U.S. equity index futures are trading higher, despite a weak opening across Europe and a soft day across Asia, outside Japan. That's probably because yields across the spectrum of U.S. Treasuries are sharply lower than where they peaked on Tuesday (implying increased demand), as the U.S. Dollar Index tumbles a bit thanks primarily to yen weakness.

You Can Also Thank the Macro

The Bureau of Economic Analysis will release its first of (at least) three estimates for third-quarter gross domestic product this morning. Down below, readers can see that I am looking for a report of rough 3% growth quarter over quarter, at a seasonally adjusted annual rate. Not that I truly believe that the economy is growing at 3%, I think that this is what will be reported. On Tuesday, the September Goods Trade Balance printed much worse than expected and down huge from August, while the preliminary report for September wholesale inventory building showed a surprise month-over- month contraction.

In addition, the JOLTs report on September job openings printed down 418,000 open positions (at 7.443 million) from August and way, way below the 8 million or so open jobs that Wall Street economists had been looking for. This put the Atlanta Fed in the position of having to revise its GDPNow model estimate for Q3 growth down to 2.8% from 3.2% (q/q, SAAR), with the real damage coming from the input from the contribution of net exports. Atlanta will revise that model again this Thursday morning in response to September data for personal income and outlays.

Rate Cut Chances

Futures markets trading in Chicago are now pricing in an almost 98% probability for a quarter-percentage point cut made to the target range for the Fed Funds Rate when the Federal Open Market Committee makes that decision next Thursday, two days after Election Day. These markets are now pricing in a 77% likelihood for a total of a half point in rate cuts by the end of the year, with a 0% probability for anything more than that.

Tuesday's Child: AMD

Equity markets were mostly mixed on Tuesday as the flow of capital rotated out of small caps and back into growth. The S&P 500 gained just 0.16% for the regular session, while the Nasdaq Composite gained 0.78%, setting another record closing level, while posting a ninth green daily candle in 10-trading days. Among the mid-majors, the Dow Industrials were slightly lower as the Dow Transports gained small. However, the Philadelphia Semiconductor Index ran 2.31% higher.

We are going to have to put an asterisk on that gain, though, as AMD was one of the leaders on Tuesday, gaining 3.96% during the regular session, before giving all of that and more back overnight. As I write this morning note, I see AMD trading more than 8% lower. CEO Lisa Su will appear on CNBC at 9 a.m. ET Wednesday morning.

Breadth was truly sloppy on Tuesday. Only two S&P sector SPDR exchange-traded funds ended the day in the green, led by Tech XLK. One would think that Tech will show some weakness this morning. Communication Services XLC also had a nice day. Alphabet earnings should support that strength this morning. Interestingly, defensive sectors littered the lower rungs of the daily sector performance tables.

Losers beat winners by more than 2 to 1 at the NYSE and by a narrow margin at the Nasdaq. Advancing volume took a 31.6% share of composite NYSE-listed trade on increased trading volume. This would normally signal forward looking weakness, but with so many earnings due, with much key macro coming, with the election less than a week away and the next FOMC policy decision little more than a week away, I'd prefer to drag my feet than write something profound at this time.

Very interestingly, advancing volume took a 58.2% share of composite Nasdaq-listed activity, on greatly increased trading volume? Is that a positive, despite the losers outnumbering the winners by just a bit at the Nasdaq? Ahead of most of the rest of the "Magnificent 7" tech stocks this week? Very possibly. The market is, however, in my opinion, setting itself up for a tougher stretch at some point before Santa shows his face.

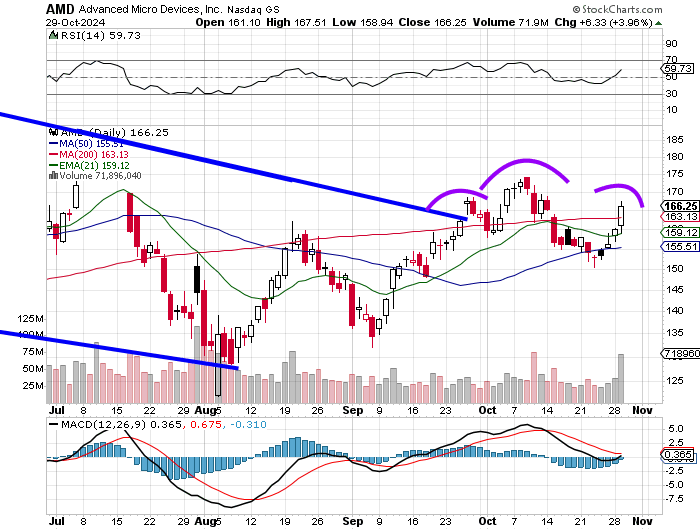

Seeking Shelter: Looking at AMD's Chart

Trading with a $152 handle overnight, AMD is set to lose its 200-day simple moving average, 50-day simple moving average and 21-day exponential moving average all in one fell swoop. This should turn the swing crowd against the stock and force portfolio managers to reduce long-side exposure. This will also likely develop the chart over the past six weeks or so in a way that will display a head-and-shoulders (bearish) pattern. If you've been with me since the stock apexed this past March, and are still long, that long should be down to roughly 25% of what it was at that peak.

Should the stock open in the way I described here, I would be slow to add, as the stock could go as low as the low $130s to low $120s before the cavalry arrives. If one is still in the green, (if you have been with us throughout, you are) then one can be slow to act. If one is now in the red, reducing the risk might not be the worst idea.

Economics (All Times Eastern)

07:00 - MBA 30 Year Mortgage Rate (Weekly): Last 6.52%.

07:00 - MBA Mortgage Applications (Weekly): Last -6.7% w/w.

08:15 - ADP Employment Report (Oct): Expecting 107K, Last 143K.

08:30 - GDP Growth (Q3-Adv): Expecting 3.0%, Last 3.0% q/q SAAR.

08:30 - US Treasury Refunding Announcement.

10:00 - Pending Home Sales (Sep): Expecting 0.9% m/m, Last 0.6% m/m.

10:00 - JOLTs Job Openings (Nov): Last 10.334M.

10:00 - JOLTs Job Quits (Nov): Last 4.026M.

10:30 - Oil Inventories (Weekly): Last +5.474MM.

10:30 - Gasoline Stocks (Weekly): Last +878K.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ABBV (2.92), BIIB (3.79), CAT (5.35), LLY (1.74), GEHC (1.05), HUM (3.39), VMC (2.32)

After the Close: AMGN (5.11), COIN (.41), DASH (.81), KLAC (7.05), META (5.27), MSFT (3.10), HOOD (.26), ROKU (-.34), SBUX (.89)

At the time of publication, Guilfoyle was long SOFI, MCD, AMD, MSFT equity.