Is the 'Trump Trade' Old News or Fake News?

Market participants currently hold overcrowded trades in sympathy to the 'Trump trade.' But there is good reason to doubt the sustainability of the price move.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There is no shortage of opinions or polls regarding the upcoming U.S. election, but in the end, none of us know what will unfold two weeks from now. Further, will anything unfold at all, or will we be in a “hanging chad” situation?

The markets seem to have priced in advance for Trump's victory; we can see this on several fronts. For instance, the grain markets (corn, soybeans, and wheat) have traded sharply lower since the polling momentum started favoring Donald Trump. Further, we have seen the Treasury market collapse to reprice interest rates for the inflation many economists expect Trump policies to produce.

Perhaps more apparent is the never-ending stock rally linked to the idea that a Republican win would be good for the markets (in reality, both parties have been equally beneficial to financial markets, particularly in the months following the election).

We can argue whether these views on what a Trump presidency would look like to the markets are accurate. However, these premises are being priced in, and that can’t be disputed. But what if the election front-running is either incorrect or overcrowded? The unwinding of these positions could be stunning.

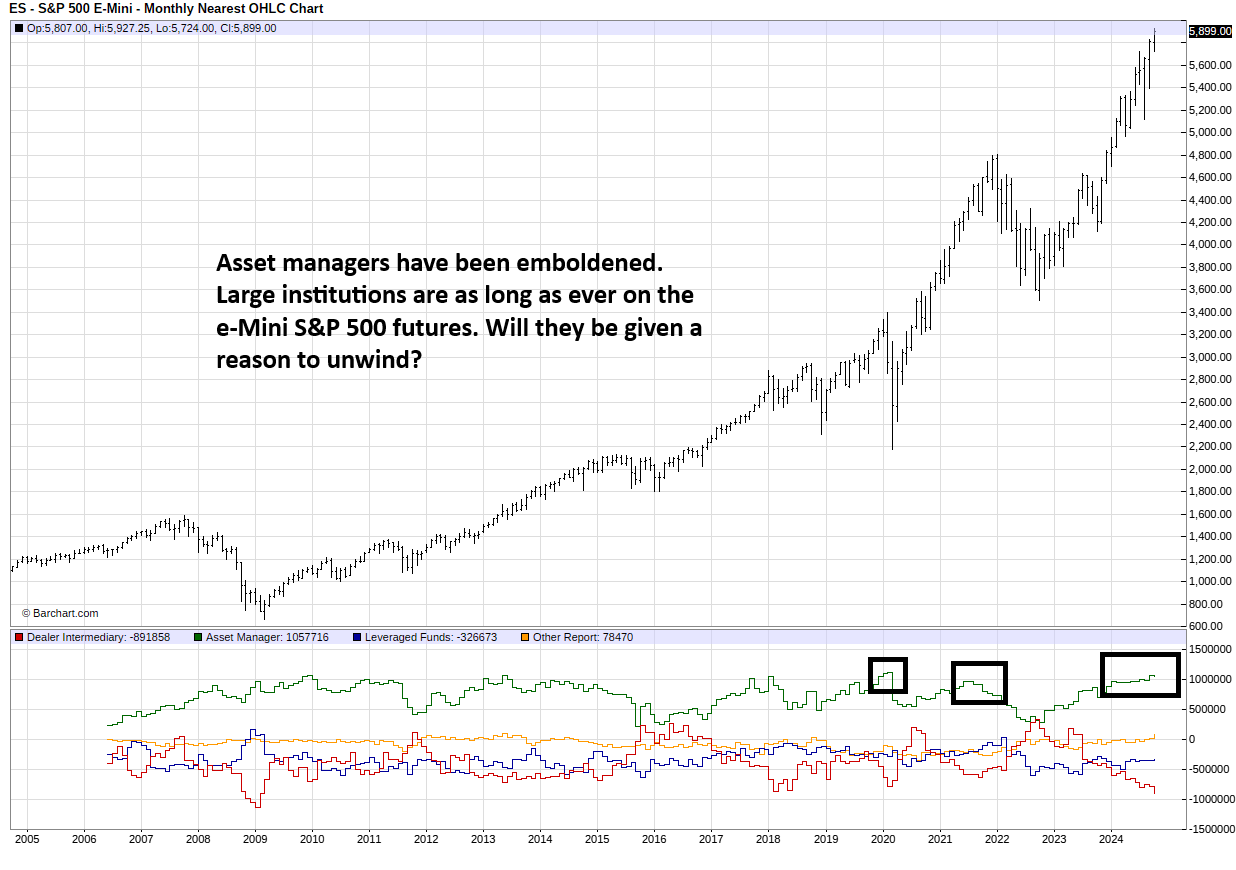

For months, we have been pointing out the historically aggressive net long positions speculators are holding in the equity indexes and the largest net short in Treasury futures on record; it isn’t irrational to expect that these groups of traders might be buying-the-rumor to later sell-the-fact afterward. Or worse, maybe they are completely wrong in their views, and the price squeezes (Treasuries higher and stocks lower) will be tremendously disruptive.

Let’s take a look at soybean futures. A trade war with China suffocated the bean market during the first Trump administration. Of course, other things were going on, such as bumper crops and a strong dollar, but tensions with China worked against soybean rallies before they started.

Yet, even if Trump wins the election, there is no guarantee the markets will behave as they did between 2016 and 2021 because traders are already positioned for a repeat. To be clear, speculators are already net short, and prices are already in a trough.

Going into the last Trump presidency, speculators were net long, leaving the market vulnerable to liquidation selling. If the masses are already short soybeans, it will be difficult to muster the same bearish selling we saw on the last go around. In fact, maybe beans will be a better buy than a sell in the next Trump reign (assuming it happens).

Ironically, despite the sluggish nature of grain prices between 2016 and 2021, the overall consensus is that Donald Trump taking office in 2025 would translate to faster rates of inflation due to tariffs and spending plans. I’m not an economist, but we didn’t see that during the last cycle. Steel prices appreciated sharply due to tariffs, but most commodity prices (copper, energies, softs, meats) came off a systemic bear market in 2016 and didn’t see significant gains throughout the four-year period. Further, the Fed spent most of the time working to ignite inflation, not fight it.

Even so, the bond market has aggressively priced in higher inflation going forward. While some of the bond selling can also be explained by high supplies (enormous government spending resulting in massive numbers of bonds sold) and a lack of faith in the ability of the U.S. to pay its debts, the implications of the so-called “Trump trade” has its fingerprints all over the tape.

As we noted in our previous analysis, speculators hold the largest net short position ever seen in 10-year note Treasuries. Even if Trump wins and the economists are right about his impact on inflation, the market will rally against the fundamental narrative if nobody is left to sell.

Alternatively, markets and market participants, even the “smart money,” can be wrong. If Trump loses, or if he doesn’t cause inflation, the bond market short squeeze could be full of shock and awe. The last time speculators held historically aggressive net short positions in the 10-year note futures, we saw note futures rally from 118’0 to over 140’0, and the yield dropped from just under 3% to just over 0%.

Lastly, the equity market has stunned the bears and emboldened the bulls. However, we must wonder if all the bulls are already positioned.

We hear about sidelined money that will need to be allocated. Still, with an aging population, it would make more sense for the bulk of the money to flow into more reasonably priced assets such as Treasuries than to chase stocks higher on a minor pullback.

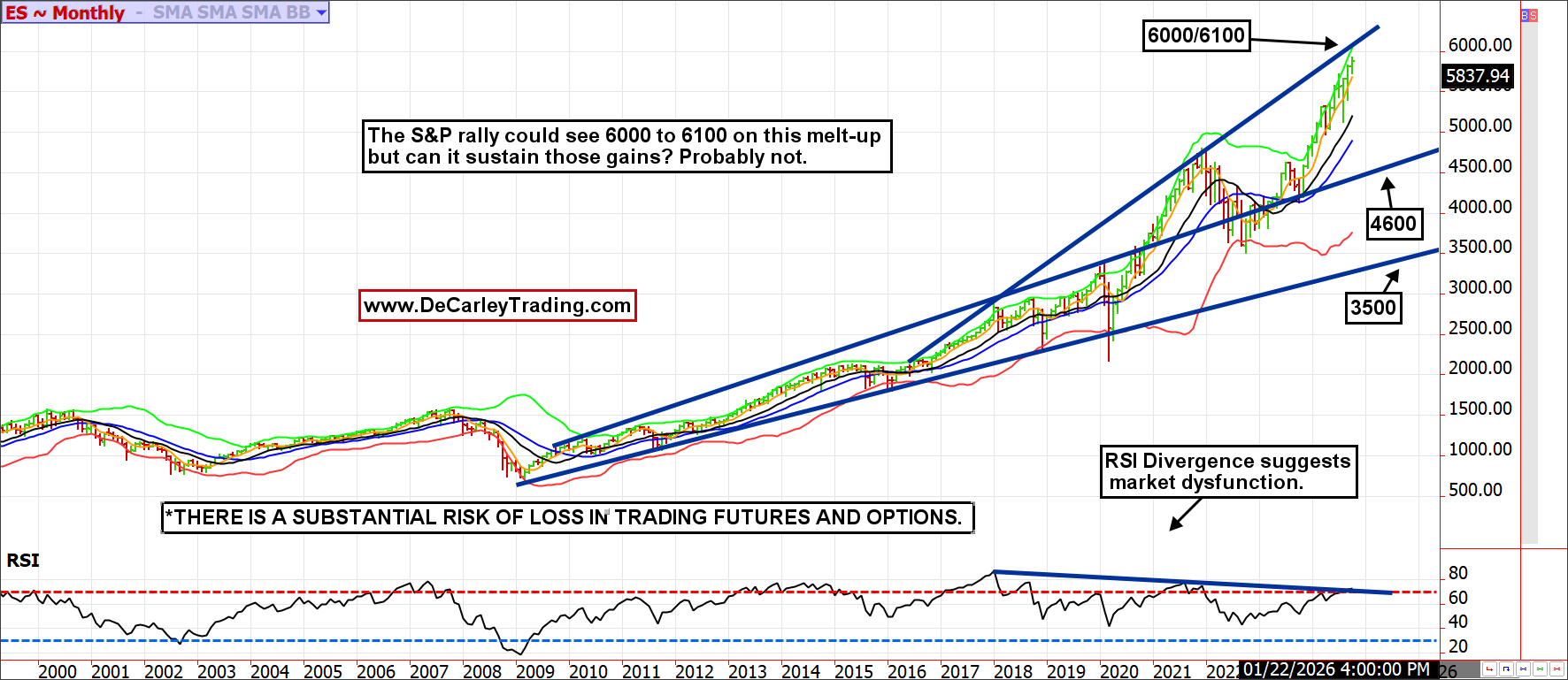

We have been eyeing a monthly S&P chart in awe of its resiliency. The pace of price appreciation is far from normal and can most accurately be attributed to widespread stimulus and money supply growth during the pandemic.

The chart shows the possibility of prices in the 6000 to 6100 range before reaching technical resistance. Yet, with event risk looming and prices as overbought as ever, the rally can fall apart anytime.

Bottom Line

Market participants currently hold overcrowded trades in sympathy to the “Trump trade.” But there is good reason to doubt the sustainability of the price moves. Similarly, the oldest and most common disclosure in the financial markets is “Past results are not indicative of future outcomes.” This is worth keeping in mind as we move forward.

Should President Trump win in November, there is no guarantee the stock market will continue its accent, grains will continue to decline, or interest rates will move even higher.

What seems obvious at the moment is likely far from our future reality. Be careful out there.