How I'm Trading Disney, Quiet Markets, Lack of Conviction, Macro to Know

The Nasdaq Composite's five-day winning streak has come to an end, and the S&P 500 enters Tuesday trading with a two-day losing streak intact.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Very early Tuesday morning, apparently a portion of the Francis Scott Key Bridge on I-695 in Baltimore collapsed after the bridge was struck by a large boat or ship. Multiple vehicles and individuals fell into the water below and there are said to be casualties. This bridge is familiar to motorists on the East Coast and the news comes as shocking.

Obviously, the bridge and that roadway are closed. As we proceed with our workday, let's just remember that no one knows when the last day comes. The most freakish of incidents can occur and impact anyone or any family on any day. Say a little prayer or have a quiet moment for those who must have been terrified in their final moments and for those who will grieve for them.

Monday Markets

The first day of a holiday-shortened four-day trading week passed rather quietly. There was some action towards the end of the session that provided some opportunity for quick thinking day-traders. Other than that, however, it was a mild, down day for the major indexes where breadth really was not all that bad and trading volumes remained very low for a second straight session.

Equities were not the only place where some pressure was felt. Treasuries sold off quietly as well. The U.S. 2-Year and 10-Year Notes both gave up roughly four basis points on Monday but have both strengthened overnight.

The S&P 500 declined 0.31% on Monday as the Nasdaq Composite similarly backed up 0.27%. This brought to an end what had been a five-day winning streak for the Nasdaq Composite. The S&P 500 will enter Tuesday trade with a two-day losing streak intact.

None of the major to mid-major equity indexes really displayed any volatility. The Dow Transports were hit the hardest, down 0.64% for the session while the small-cap Russell 2000 actually gained 0.1%. Before celebrating that green close for the Russell, be cognizant that the S&P SmallCap 600 performed in line with the broader marketplace, giving up 0.28%.

Eight of the 11 S&P sector select SPDR ETFs closed in the red on Monday, but like the above indexes, no fund among them moved too far from where they started. Energy XLE led the winners, up 0.93%, while Technology XLK was the weakest sector, down 0.66%.

Within Tech, the Philadelphia Semiconductor Index gave up just 0.34% as Micron MU gained 6.28% on Monday. Both Advanced Micro Devices AMD and Intel INTC came under pressure as news broke of a likely coming of reduced demand for their servers from China. AMD regained its 50-day simple moving average on Monday, delaying (or cancelling) the probability of a forced bout of profit-taking up and down Wall Street.

Breadth

The day's results were truly mixed. Losers beat winners by roughly four to three margins at both the NYSE and Nasdaq. That said, advancing volume took a 56% share of composite Nasdaq-listed trade and a 50.4% share of composite NYSE-listed trade.

Aggregate trade was lower than Friday's anemic levels across NYSE listings as well as the membership of the S&P 500. Trading volume increased slightly on a day-over-day basis for Nasdaq listings and across the Nasdaq Composite but remained about 13% below the 50-day trading volume simple moving average for that index.

In other words, there was no real conviction displayed in either direction on Monday.

The Macro

On Monday, February New Home Sales disappointed slightly, printing at a seasonally adjusted, annualized rate of 662K. This was down from a revised 664K in January and below the 675K or so that economists were looking for.

This morning, the Census Bureau will release Durable Goods Orders for February. At the headline, Wall Street is looking for a month-over-month gain of 1.1%, which would be a rebound from the -6.1% January performance. Ex-transportation, we are looking for growth of 0.4% and ex-defense, the consensus is for growth of just 0.1%. The metric which actually tells us something about business investment is the Core Capital Goods print for new orders, which omits defense and air transportation. This metric is expected to show growth of 0.1%, which would be in-line with January.

After these numbers cross the tape, we'll get dated information on January housing prices from Case-Shiller and a March print for Consumer Confidence from the Conference Board. Note to the new kids, this is not the University of Michigan's twice-a-month report on Consumer Sentiment that includes a very closely watched survey on one-year and five-year inflation expectations.

Lastly, the Richmond Fed will release that district's Manufacturing survey for March. A fifth consecutive month spent in a state of contraction is expected. Both the New York and Dallas Feds have posted awful months for manufacturing regionally, but the Philadelphia district did surprise with outright expansion for March.

Fed Speakers

Atlanta Fed President Raphael Bostic, who does vote on policy this year, more or less, reiterated expectations for rate cuts that he expressed this past Friday. On Friday, Bostic said, "I'm definitely less confident than I was in December." Bostic added, "If we have an economy that is growing above potential, and we have an economy where unemployment is at levels that were deemed to be unimaginable without pricing pressures, and if we have an economy where inflation is moderating... Those are good things. That gives us space for patience."

Bostic repeated that sentiment on Monday, not quite word for word, but close to it. Bostic supports the idea of just one rate cut of 25 basis points for 2024 at some point later in the year. He also would like to start tapering the Fed's quantitative tightening program rather soon.

Elsewhere on Monday, Chicago Fed President Austan Goolsbee expressed his support for 75 basis points for the calendar year (Can anyone say higher (inflation) for longer?), as Fed Governor Lisa Cook spoke on the Fed's dual mandate at Harvard. Cook spoke on balancing risk and not moving to change policy too soon or too late but striving to reach the Fed's 2% target on inflation without drawing from employment. She taught an economics class more than expressed opinion on forward-looking monetary policy.

Disney Price Target Adjustment

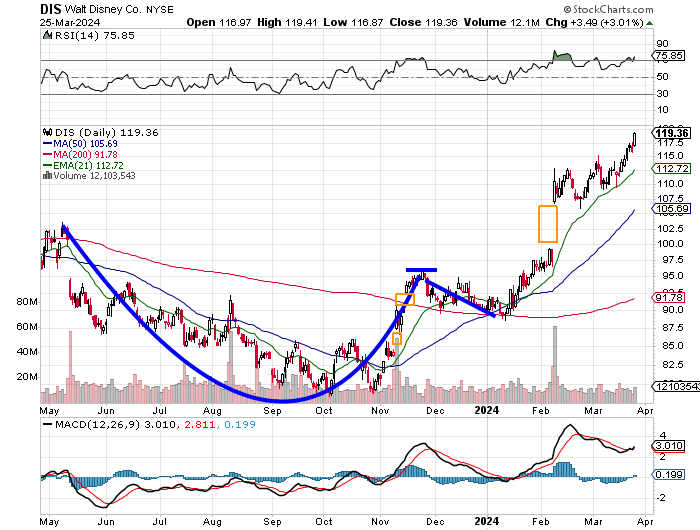

On Monday, Barclays analyst Kannan Venkateshwar upgraded his rating on The Walt Disney Company DIS from "equal-weight", which is a hold-equivalent, to "overweight," which is a buy-equivalent. Venkateshwar also increased his price target for the House of Mouse from $95 to $135. The four-star rated (by TipRanks) analyst cited surprising free cash flow and expected moves around ESPN and Hulu.

Elsewhere, CFRA analyst Kenneth Leon reiterated his "buy" rating on DIS, while increasing his price target from $120 to $139. Leon is also rated at four stars.

I also had a $120 target on Disney that I published in early February and again at the Doug Kass Diary on Friday. DIS knocked on that door on Monday, sporting a pop of 3% for the day and has been knocking on that door overnight.

DIS broke out of a seven-month cup-with-handle pattern in late January/early February. The stock created a still unfilled gap around earnings as it has continued to rise. Relative Strength borders on being technically overbought, as the daily Moving Average Convergence Divergence (MACD) expresses a new optimism illustrated by a histogram of the 9-day exponential moving average (EMA) that has just gone positive and a 12-day EMA that appears to be crossing above the 26-day EMA.

Do I think that DIS will just go parabolic to the upside? No, I expect a basing period of consolidation to develop, and the upper bound of that range will become my new pivot.

The stock will trade sideways for a period of time and then, in my opinion, continue to recover. I remain a Nelson Peltz fan, but also believe that CEO Bob Iger is capable of maintaining the company's momentum with or without Peltz.

With my old target reached, my MO is to take at least a small profit at target and go higher. That is what I will do. For now, I will use my old target as my pivot as the base that I expect will have an upper bound that at least runs with my old target. Of course, this new target will be adjusted once a recognizable pattern develops.

Walt Disney Company (DIS)

Price Target: $144 (up from $120)

Pivot: $120 (up from $96)

Add: Between 21-day EMA and 50-day SMA

Panic: Loss of the 50-day SMA

At the time of publication, Guilfoyle was long DIS and AMD equity.