From Meltdown to Manic Monday: Erratic Tech Trade, Peace-Fire, Grumbling Chart

Let’s check the latest on the supposed peace deal, make sense of the hot-and-cold tech trade, and sort through the crowded IPO filings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Equities sold off hard late last week. You know that. That’s no longer news. The ceasefire between the U.S. and Iran seemed to fray as did the adjacent ceasefire between Israel and Lebanon. Unfortunately, for those supporting the peace process, the terrorist group Hezbollah is a major force, if not the major political force, inside the nation of Lebanon. Hezbollah appears not just to want nothing to do with a peaceful existence with their Israeli neighbors, the group has traditionally been funded by and often acts on behalf of Iran.

As the Iranian Revolutionary Guard and U.S. Navy traded jabs over the weekend as did the Israeli Defense Forces and Hezbollah. All fighting, however, stopped at the request / command of U.S. Pres. Donald Trump. The U.S. president, while unrelenting in the implementation of the American naval blockade of Iranian ports, remains fixated on reaching a peace deal, or at least something closer to a lasting ceasefire. Somehow, markets or at least the keyword-reading algorithms that have taken control of global financial markets away from human traders, went for it.

They, (they, being these keyword-readers) perhaps correctly, or perhaps, quite naively, are buying the peace story yet again. Don’t get me wrong. I want peace in the Middle East and peace around the planet as much as anyone. I do not like seeing service members in harm’s way. Nor do I like seeing innocent civilians in danger. It has just become difficult for human traders not to become skeptical as this supposedly “imminent” peace deal has slipped through the sewer grate a number of times now.

Manic Monday

It seemed as if, after Friday’s market meltdown (remember what I have told you about intentional algorithmic market overshoot, yes, inefficiency by design), the chipmakers and some other AI-focused names led an “iffy” rebound across the U.S. marketplace. After giving up 2.15% on Thursday, the Philadelphia Semiconductor Index was roasted for another 10.26% on Friday. That same index gained a nifty 5.61% on Monday. Huzzah!

This was a very “hot and cold’ rebound, though. I don’t think it felt very comforting at all. For my mind, this market needs a broader kind of love in order to carry on as was. A true peace that permits consumer prices to retrace somewhat would get that done. We’ll see. On Monday, Intel (INTC) led those semis with a run of 11.2% after reports circulated that both Nvidia (NVDA) and Alphabet’s (GOOGL) Google were considering the idea of making use of Intel’s foundry business.

Behind Intel, among the semis, Micron (MU) gained 9.9%, Marvell Technology (MRVL) took back 9.6% on the S&P 500 inclusion news, and equipment provider KLA Corp (KLAC) added 9.3%. The above-mentioned Nvidia gained “just” 1.7%, which is interesting because the hyperscalers did not have such a great day on Monday.

Looking out over the landscape of mega-cap hyperscalers, Facebook / Instagram parent Meta Platforms (META) lost 1.3% on the day in response to a report at the Financial Times that the company was considering raising tens of billions of dollars in a stock sale. The news should not shock. META has projected capital spending of $145 billion for 2026. This comes after Google parent Alphabet had announced, on June 1, a plan to raise roughly $80 billion that would also include sales of the company’s stock.

The fact that these largest of best funded U.S. companies are seeing the need to dilute their own equity through the secondary sale of common stock has to be eye-opening for some. The “Magnificent Seven” had been something of a safe haven for investors. That’s no longer the case if these huge buyers of AI-focused infrastructure need to sell equity in order to fund this expansion.

Perhaps the new safe haven is where this “inelastic demand” is met. That’s in the semis. All of the semis. That means that longer-term safety, but not necessarily protection from short-term volatility will be found across several key areas. I will continue to look to the designers of GPUs, CPUs and the brains of AI. I will continue to look to the designers of memory or storage space, to the providers of foundry services and to those who make the high-tech, very fine equipment that semiconductor designers require. You and I can tackle this environment. What we can’t do, is hide our heads in the sand and hope it all works out. This is when passive management fails and investors need to get their hands dirty.

Marketplace

How sloppy was Monday? Let’s explore. Treasury yields still moved higher, though we are seeing some relief overnight. Crude oil sold off on Monday and has continued to do so overnight. That’s what we need to see. Something that helps the good people of our nation on the inflation front. At zero-dark thirty on Tuesday morning, I see the sweet stuff (West Texas Intermediate) trading with an $89 handle (per barrel). Rah!

On Monday, the S&P 500 gained 0.3% while the Nasdaq Composite added 0.85%. Small caps did well as the Russell 2000 tacked on 0.77% and the S&P 600 gained 0.61%. The Dow Transports gained an even 1% thanks to a 6.5% run made by FedEx (FDX) as well as gains made by the truckers based on lower fuel prices.

Breadth

Market breadth was not minty fresh at all. It was more garlic-sardine-like than anything else. Only three of the 11 S&P sector SPDR ETFs closed out the regular session on Monday in the green. Obviously, after last week’s date with the “ugly stick,” technology (XLK) left the way north, followed by energy (XLE) despite lower oil prices. In an encouraging move both for the economy and for the markets, the utilities (XLU) placed eleventh as defensive sectors underperformed.

Losers beat winners by a seven-to-six margin at the NYSE, but winners beat losers by a rough five to four at the Nasdaq. Advancing volume took an encouraging 65.5% share of composite Nasdaq-listed trade on Monday, but a discouraging 46.8% share of composite NYSE-listed activity. What does it all mean? Less than Friday’s activity meant. Aggregate trading volume dropped 12.8% on a day-over-day basis across Nasdaq listings, and by 12.4% across NYSE listings. As a matter of fact, aggregate trading volume across the membership of the S&P 500 on Monday was the lightest it’s been since Friday, May 1 more than a month ago.

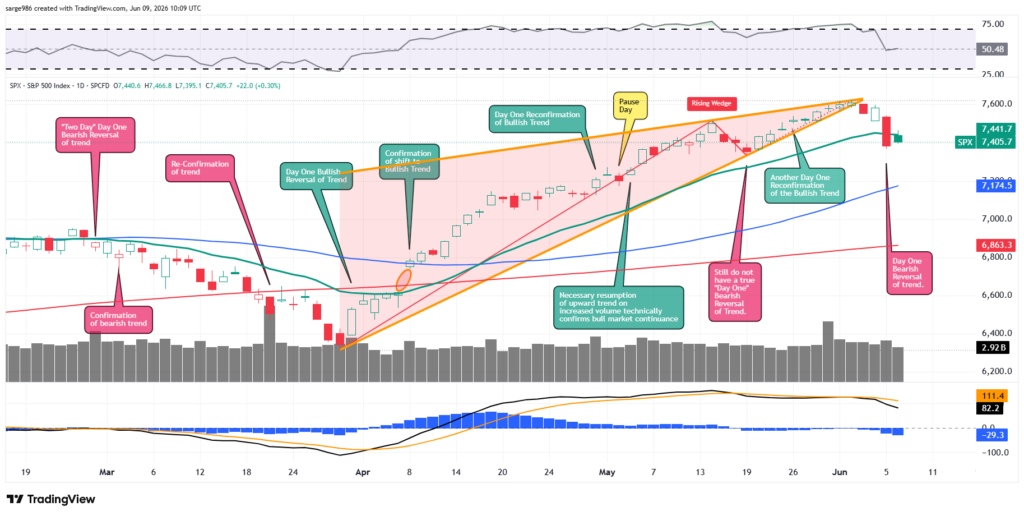

What Are We Looking At?

Readers will see that last week, the S&P 500 broke lower out of a rising wedge pattern of bearish reversal. No, I did not give you a heads up. I recognized this pattern, myself, in hindsight. Readers will see that the swing crowd has put up a fight over the past two trading sessions at the 21-day exponential moving average of this index.

Friday does indeed present as a “Day One” bearish reversal of trend. Monday does present the “necessary” pause. This sets up the rest of this week as quite pivotal. Why the rest of the week? Well, we could get our technical confirmation or technical rejection of a bearish reversal today, but with consumer price index due on Wednesday and producer price index due on Thursday, I would think that any confirmation or lack thereof by volume will likely have to wait.

Turning to the indicators, readers will see that relative strength is now non-committal. More importantly, the daily moving average convergence divergence (below the chart) has turned quite nasty in appearance. The histogram of the 9-day EMA has gone negative as the 12-day EMA has dropped below the 26-day EMA. These are both bearish signals.

Carry On Wayward Son

Masquerading as a man with a reason

My charade is the event of the season

And if I claim to be a wise man

Well, it surely means that I don’t know

On a stormy sea of moving emotion

Tossed about, I’m like a ship on the ocean

– Kevin Livgren (Kansas), 1976

Three’s Company

Yes, SpaceX is set to go public this Friday. Yes, Anthropic confidentially filed for an initial public offering last week. On Monday, ChatGPT parent OpenAI, did the same, filing a confidential S-1 with the Securities and Exchange Commission. This was no surprise as the Wall Street Journal had reported in mid-May that OpenAI was working with investment bankers.

But there is no rush. The company stated in a blog post that they “expect it (the news) to leak so we’re just announcing it.” OpenAI added that it “may be a while” as there are “things we want to do that are likely easier as a private company.”

Economics

(All Times Eastern)

06:00 – NFIB Small Biz Optimism Index (May): Expecting 96.0, Last 95.9.

08:15 – ADP Employment Change (Weekly): Last 35.75K.

08:30 – Balance of Trade (Apr): Last $-60.3B.

08:55 – Redbook (Weekly): Last 9.0% y/y.

10:00 – Existing Home Sales (May): Expecting 4.07M, Last 4.02M SAAR.

10:00 – Wholesale Inventories (Apr-rev): Flashed 0.5% m/m.

4:30 p.m. – API Oil Inventories (Weekly): Last -6.75M.

The Fed

(All Times Eastern)

Fed Blackout Period.

Today’s Earnings Highlights (Consensus EPS Expectations)

Before the Open: SJM (2.64), UNFI (.77)

After the Close: CBRL (-.48)

At the time of publication, Guilfoyle was long NVDA, MU equity.