The Fed Will Cut Interest Rates By 75 BPS This Year

Looking at the data, we build a base case for the Federal Reserve to cut interest rates two to three times this year for a total of 75 BPS.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

My base case is that there will be two to three cuts this year, for a total of 75 BPS.

Using the Bloomberg World Interest Rate Probability (WIRP) function, we see the market has been edging towards my viewpoint:

| Meeting | # Cuts | % Cut at Meeting | Cumulative % Cut |

|---|---|---|---|

7/31/2024 | 0.1 | 8% | 8% |

9/18/2024 | 0.8 | 75% | 83% |

11/7/2024 | 1.3 | 43% | 126% |

12/18/2024 | 2.0 | 78% | 203% |

01/29/2024 | 2.7 | 64% | 268% |

Basically, 75 BPS by the end of January 2025, which I expect to be pulled forward.

No Cut in July?

We have argued, quite aggressively, that the Fed should make their first cut in July.

I think the data supports it, but almost as importantly, a first cut in September seems highly likely to spark a lot of controversy on social media. It is easy to see how one side would argue that the cut was to help the incumbents (that wouldn’t be the reason, but easy to see it playing out that way on social media and on the campaign trail).

I don’t think the Fed will cut in July, but I do think it should!

Jobs

We wrote on Friday that there were more “flaws” in the recent jobs data than appeared obvious when simply seeing the headlines. The jobs situation is “fine” but no longer robust and certainly not one sided in terms of job seekers like it was for much of 2023.

When I examine various measures on online help wanted, I’m left with the impression that it not only are the number of jobs declining, but the evidence of “ghost jobs” is accumulating (job postings that are out there, but not really active).

Again, sticking to a view that the labor market is softening enough for the Fed to cut.

We are also starting to hear more about the Sahm Rule Recession Indicator. I strongly believe that economists are too quick to label things as “rules” that are merely conjectures, but this one deserves recognition.

The “rule” is that when the three-month moving average for unemployment rises 0.5% above the minimum three-month average in the past year, we are about to enter a recession.

One year ago, the three-month moving average was 3.6% and today it is 4%. Not quite triggering the Sahm Rule, but certainly something the Fed should be consider.

The Taylor Rule

OK, I’ve already admitted that I don’t like the term “rules” as they are applied in economics, but since we are on the subject let’s look at the Taylor Rule.

The Atlanta Fed Taylor Rule Calculator lets you estimate the Taylor “Rule” rate. Using three pre-filled scenarios, the calculation came up with estimates of 4.61%, 3.91% and 3.79%, all of which are below today’s rate of 5.375%.

Financial Conditions

While financial conditions remain easy, and are one thing those not looking to cut rates could point to, I think there are some mitigating circumstances. Before diving into inflation, which warrants being the final section, at least in terms of how we are framing the argument, we want to touch on a few more “fringe” views:

- AI: Risk taking feeds into most measures of financial conditions. While the stock market is higher, it has been driven by a handful of stocks and a few sectors (value and, more noticeably, small caps, have been underperforming). If we really are at a pivot point in technology, maybe we shouldn’t look to stocks as a sign of excess or exuberance?

- Net income: With yield curves inverted, with so many companies and individuals locking in “lower for longer” during the post-COVID ZIRP policy, many are benefitting from their money market funds and are spending that money. A rate cut might slow some activity (especially on the bank lending side, where the deposit rate is sticky and low, but the income side would drop with a rate cut).

- Forward Guidance: I cannot articulate this argument well (at least not yet), but given how much “guidance” markets receive (dot plots, speakers, press conferences), I wonder if financial conditions reflect more than they once did, making them less useful as a standalone measurement?

Inflation

We get CPI on Thursday morning.

Yes, inflation remains too high, but it has been coming down. It is 100% clear to anyone that housing inflation, which has been propping up overall inflation, merely reflects stale data. That is one reason why the Fed looks to PCE more than to CPI.

In any given month, CPI might be doing anything, but generally, I’ve been very comfortable with the direction, and barring a commodity spike linked to some geopolitical action (that risk has been increasing), that trend should continue.

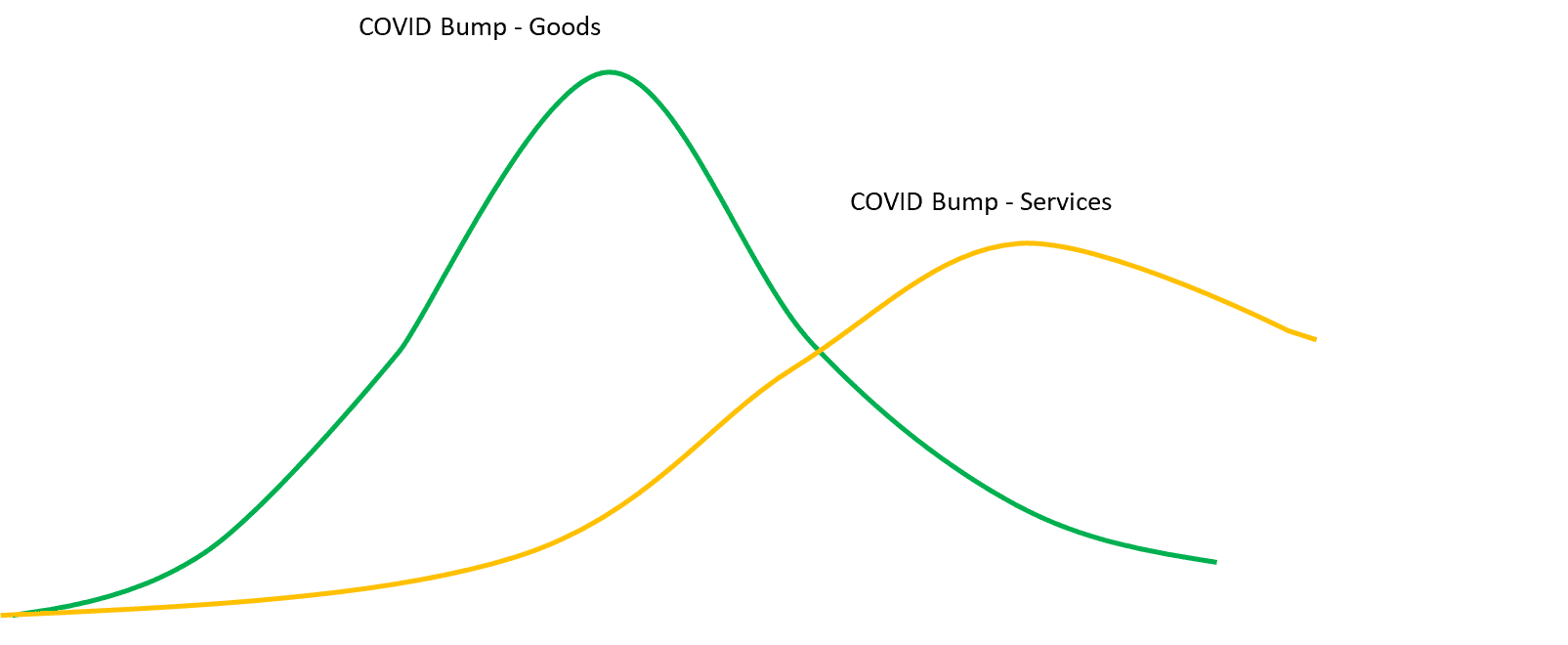

While simplistic (and the chart is admittedly elementary) the COVID “bump” theory seems to be a great way to think about inflation and has been playing out in real-time.

Goods had a much larger jump in inflation, and it started sooner as Americans were flush with cash and had immense built-up demand for goods, especially for those who were experiencing lifestyle changes enabled by work from home. The Manheim Used Vehicle index is a good one to watch on this.

Services took longer to start and were slower to ramp up. Not only were there rules, which varied by state, but individuals also differed on when they were comfortable doing things post-COVID. So, the services bump took longer to generate, and we continue to view Summer 2023 as the summer of vacations, representing peak services demand (relative to availability). As that normalizes, we should see less and less inflation pressure on the services side (as mentioned Friday, the ISM services employment index has been below 50 and shrinking for the last five months in a row).

Maybe this chart is far too simple? Possibly, but I think that it has captured the gist of inflation and is the basis for me remaining comfortable that the worst is behind us.

Bottom Line

We didn’t even touch on lag effects (even Fed Chair Powell seemed to admit that because of this they should start sooner rather than later).

Continue to look for 75 BPS of cuts this year (with two or three cuts). I don’t see July as likely, though I think it would be prudent to start then.

Less inverted curves. That is why I continue to like to buy “duration” products when the 10-year yield is at or near 4.5% and sell them when it gets to 4.3% (my main allocation in the fixed income portion of my portfolio is to closed end muni funds).

At the time of publication, Tchir had no positions in any securities mentioned.