Doug Kass: It's Warren Buffett vs. Michael Saylor for the Market Heavyweight Title

Heightened optimism morphing into soaring euphoria has set up a bout for the ages: the 'Standard Bearer of Crypto' pitted against an increasingly risk-averse 'Oracle of Omaha.'

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Despite numerous concerns that we have expressed, equities continued to to surge in November.

Many things have come together to drive the market (bubble) — AI, former President Trump's election, liquidity and market structure — all fed by social media (many of these factors may prove illusory).

Though emotions are contagious and have no business in investing, the Panic of October 1987 stock market is now in reverse — a mass panic (back then) has morphed into a mass euphoria (today).

In one corner (the aggressor) is standard bearer of crypto, MicroStrategy's MSTR Michael Saylor, and in the other (an increasingly risk averse) Berkshire Hathaway's BRK.A BRK.B Warren Buffett.

2024 equity returns have likely borrowed from the future. It is our view that the optimism and reset (higher) in valuations shall pass... as it did forty years ago and, again at the end of the dot-com bubble.

For now, valuation (and other fundamental) concerns are obscured by the sheer force of price (momentum). But, speculation doesn't repeat itself ... it rhymes.

Some things you don't see at the bottom — CNBC's Robert Frank making the case for paying $6.2 million for a duct-taped banana or MicroStrategy trading at 3x the underlying value of its bitcoin holdings and market participants unconcerned about high valuations.

Meanwhile let's keep the windows sealed, as in the immortal words of President Abraham Lincoln who said that he felt "like the boy that stumped his toe, — "it hurt too bad to laugh and he was too big to cry."

I was lyin' in a burned-out basement

With a full moon in my eyes

I was hopin' for replacement

When the sun burst through the sky

There was a band playin' in my head

And I felt like getting high

I was thinkin' about what a friend had said

I was hopin' it was a lie

Thinkin' about what a friend had said

I was hopin' it was a lie

- Neil Young, After the Gold Rush

On Friday, October 23, 1987, days after the previous Monday's fateful and dramatic (22.6%) October stock market fall, Wall Street Week's Louis Rukeyser started the program:

"It was the day the computers went wild and through the wonders of so called 'programmed trading' made a correction turn into an early Halloween.

"It is just your money, not your life. Everybody who really loved you a week ago still loves you tonight. And that's a heck of a lot more important than the numbers on a brokerage statement.

"The robins will sing, the crocuses will bloom and babies will gurgle and puppies will curl up in your lap and drift happily to sleep with you even when the stock market goes temporarily insane.. That said, let me say, ouch, eek and medic."

- Louis Rukeyser, Wall Street Week (October, 1987)

Here is the complete transcript of Wall Street Week. After the Crash - Part 1 - Wall Street Week Oct. 23, 1987 - YouTube and Part 2 - Before the Crash - Wall Street Week October 16, 1987

Before there were chat rooms and Twitter, there was Wall Street Week with Louis Rukeyser.

I and many others religiously watched Louis Rukeyser every week and listened to his educated guests and his craftily devised puns.

Nearly forty years ago market structure, policy and deficit concerns combined to bring fear into the markets, which culminated in Black Monday.

It is almost now as if the market and Fin TV's coverage is the movie in reverse.

The birds are singing, the crocuses are blooming and the puppies are happy and playful.

But, like that unprecedented market decline 37 years ago, today's unprecedented market climb (to all-time levels) seems equally undeserved.

Warren Buffett famously said:

“This imaginary person out there — Mr. Market — he's kind of a drunken psycho. Some days he gets very enthused, some days he gets very depressed. And when he gets really enthused, you sell to him and if he gets depressed you buy from him. There's no moral taint attached to that... Emotions are contagious, and emotions have no business in investing.”

I detailed my market concerns in (Mike) Wilson, For Christ's Sake... Sell! a week ago.

Since then, speculation (in AI, in cryptocurrencies, in MicroStrategy MSTR, etc.) has intensified.

Move over Nvidia NVDA:

Arguably, Mr. Market is increasingly acting like Warren Buffett's "drunken sailor" as The Oracle of Omaha grows ever more risk averse (and the Buffett Indicator rises into a record overvalue):

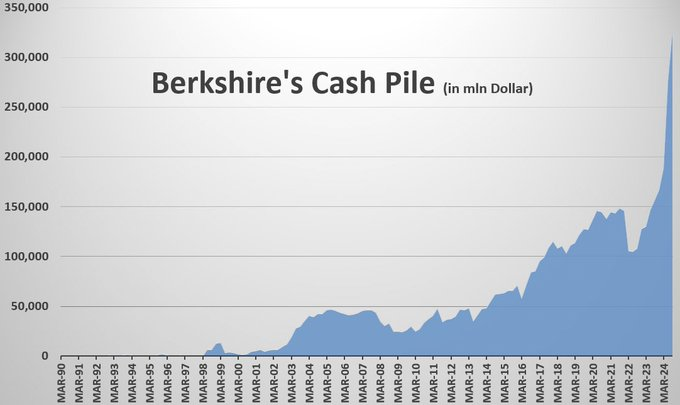

Here is what Berkshire's (BRK.A) (BRK.B) outsized cash reserves mean to me.

While admittedly not a market timer, Buffett has made a statement by selling large positions in Apple (AAPL) and Bank of America (BAC) towards accumulating a cash hoard of about $325 billion. Moreover, Berkshire has halted stock buybacks for the first time since 2018.

At 28% of assets, Berkshire's cash is at the most in 35 years. In just twelve months, Berkshire's cash has doubled and is rising at the fastest pace in several decades. Note that Berkshire's cash/assets reached 24.5% in Q22005 and remained high elevated until late 2008:

MicroStrategy's Michael Saylor vs. Berkshire Hathaway's Warren Buffett

It's a heavyweight title match....

In one corner, MicroStrategy's aggressor, Michael Saylor:

Well, I dreamed I saw the silver spaceships lying

In the yellow haze of the sun

There were children crying and colors flying

All around the chosen one...

- Neil Young, After The Gold Rush

And in the other corner, a risk-averse nonagenarian, Warren Buffett:

Regrets, I've had a few

But then again, too few to mention

I did what I had to do

And saw it through without exemption

I planned each charted course

Each careful step along the byway

And more, much more than this

I did it my way...

- Frank Sinatra, My Way

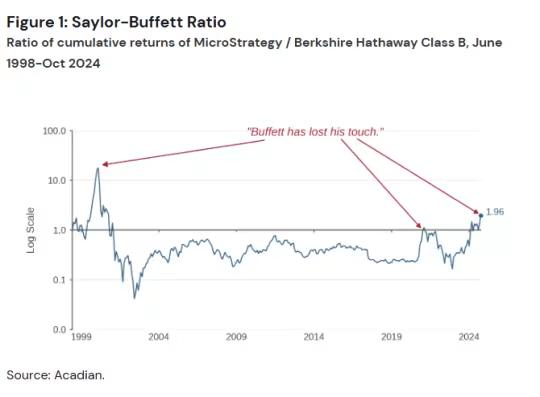

While Berkshire's common shares have performed well, relative to speculative market components, not so much. A chorus of "Buffett has lost his touch" can now be heard and it is growing louder.

The last time criticism of bears (and of Buffett) were so emphatic was at the end of the dot-com stock boom and before a merciless drawdown in equities:

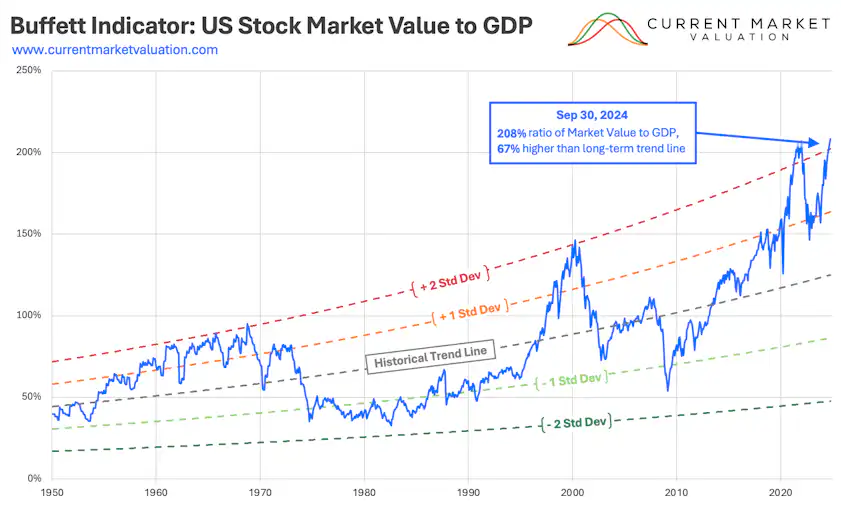

Finally, here is an updated "Berkshire Indicator," which measures the ratio of the U.S. stock market to GDP.

Buffett Indicator = Total US Stock Market Value/Gross Domestic Product (GDP)

As of September 30, 2024 the ratio values are:

Total US Stock Market Value = $60.86T

Annualized GDP = $29.24T

Buffett Indicator = $60.86T/$29.24T = 208%

This ratio fluctuates over time since the value of the stock market can be very volatile, but GDP tends to grow much more predictably. The current ratio of 208% is approximately 66.62% (or about 2.2 standard deviations) above the historical trend line, suggesting that the stock market is Strongly Overvalued relative to GDP:

Things You Don't See at the Bottom

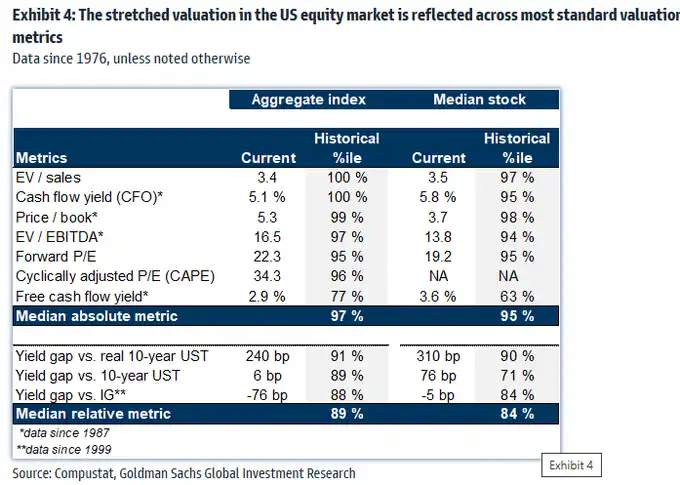

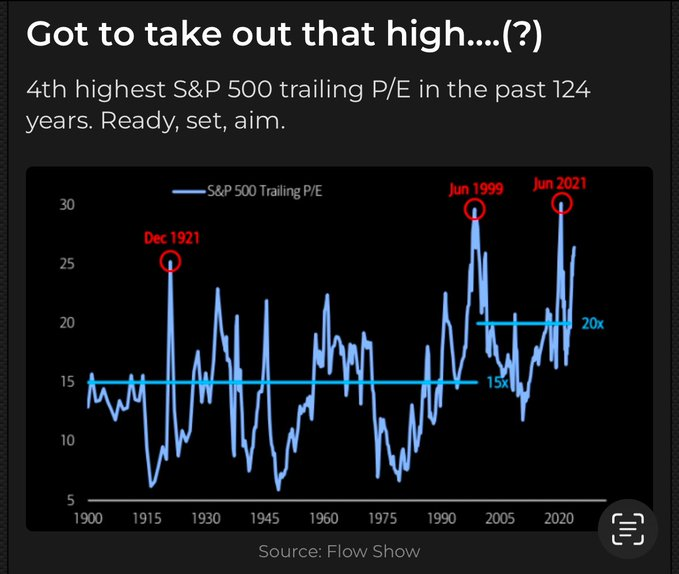

As recently noted in my Diary, most traditional valuations are, on average, in the 95%-tile:

The current zeitgeist is that elevated price earnings ratios no longer matter:

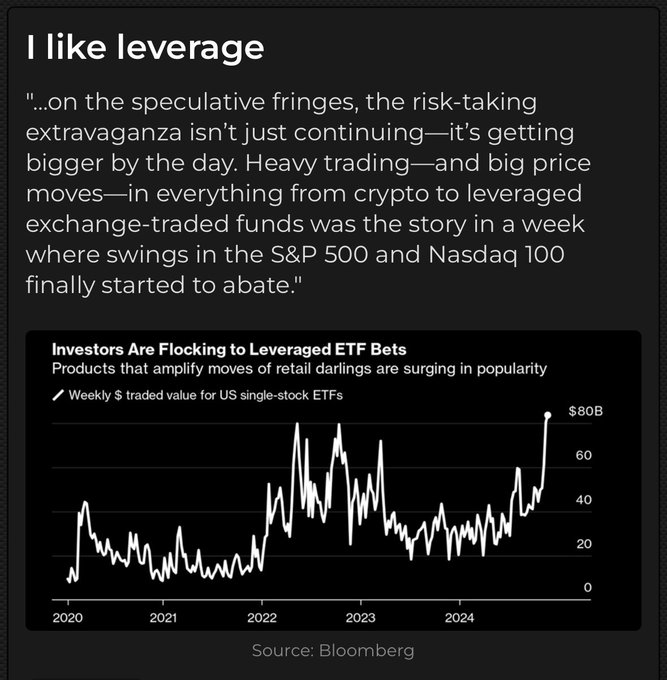

As speculation abounds and traders/investors worship at the altar of price (just look at my daily premarket ETF movers):

As valuation (and other fundamental) concerns are obscured by the sheer force of price (momentum):

Bottom Line

In this missive I outline my description and concerns regarding market speculation and contrast it with market patience.

While many factors have come together to drive the market (bubble) — AI, former President Trump's election, liquidity and market structure — many of these factors (fed by social media) may prove illusory and should be taken in the context of sky high valuations.

I will end by returning to two wonderful quotes:

"What the wise man does in the beginning, the fool does in the end."

- Warren Buffett

"A bull market is like sex, it feels best just before it ends."

- Barton Biggs

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publictaion, Kass was long SPY common (S); Short SPY calls (M), MSTR (VS), BAC (VS), BITO (S).