Doug Kass: (Mike) Wilson, For Christ's Sake ... Sell!

Why the market's upside reward is dwarfed by downside risk.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Mortimer Duke: [after Louis and Billy Ray turn the people towards him and the price starts dropping from their short selling] That's not right. How can the price be going down?

Randolph Duke: Something's wrong. Where's Wilson?

Billy Ray Valentine: [On the floor] SELL! SELL! SELL! SELL!

Mortimer Duke: [Sees him and Lewis] What are *they* doing here?

Randolph Duke: They're *selling*, Mortimer!

Mortimer Duke: Why, that's ridiculous!

[Then a look of shock washes over him]

Mortimer Duke: Unless that crop report...

Randolph Duke: [They both look at one another, then start heading to the pit] God help us!

Even previously bearish Morgan Stanley's (Mike) Wilson is now a market enthusiast — he apparently is not familiar with the movie, "Trading Places." Morgan Stanley sees S&P 500 climbing another 11% — to 6,500 — next year

But, something's wrong Wilson, sell!

The bullish cabal, apparently influenced importantly by the strong price momentum of the indexes, have grown more optimistic with higher stock prices. By contrast, we believe there are a plethora of developing market headwinds that are being ignored by most market participants.

From our perch, the market's upside reward is now dwarfed by the downside risk and that there is virtually no "margin of safety" in current share price levels.

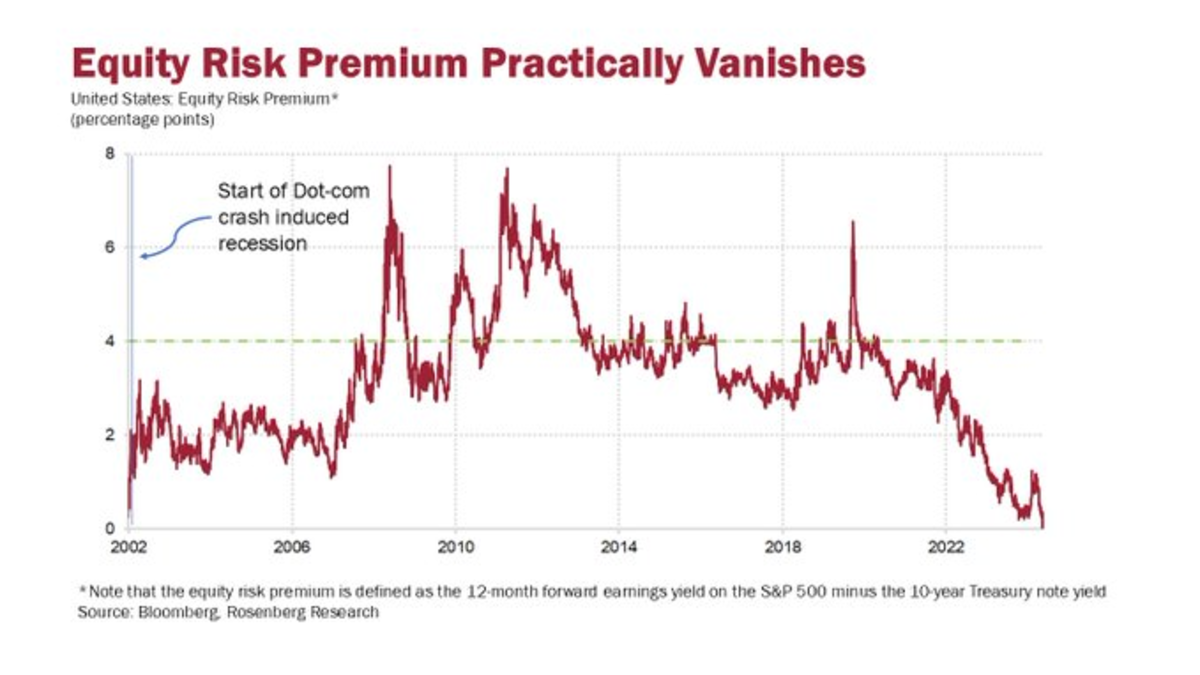

Indeed, given the "paper thin" equity risk premium, it is our view that the S&P 500 Index (using today's prices as a base) will provide substandard to negative returns over the next few years.

Short selling opportunities now abound...

In this morning's market update I take into account the wisdom of Jerry Garcia, Warren Buffett, Charlie Munger, Richard Russell and Rosie (David Rosenberg)

The foundation of my ursine market view is based on some of the following concerns:

* Interest rates will likely be higher for longer. The peak easing this year priced in for year-end 2025 was an expected federal funds rate of about 2.80%. That is now about 3.90%, so the market has taken away 110 bps of rate cuts. Treasury Sec. Janet Yellen has front loaded Treasury issuance in bills, above the recommended level of 15%-20% of total offerings by the Treasury Borrowing Advisory Committee. This, instead of issuing more longer-term coupons when the 10-year yield was back under 4%.

While no one at the Treasury will admit it, they were playing the yield curve, didn't want to upset the longer end of the curve with too much supply and instead with the back up in short rates, missed an opportunity to term out U.S. debt.

Stated simply, the Fed blew it.

Over the last five decades interest rates (the 10-year Treasury note yields 4.48%) have never been so high, at 3.5-times relative to the S&P dividend yield (1.27%). The S&P equity risk premium (forward earnings yield less the 10-year yield) has turned negative for the first time since 2002. In other words, investors are now paying to take risk rather than being compensated for taking risk:

Here is a longer-term chart of the S&P earnings yield vs. the yield on the 10-year Treasury note:

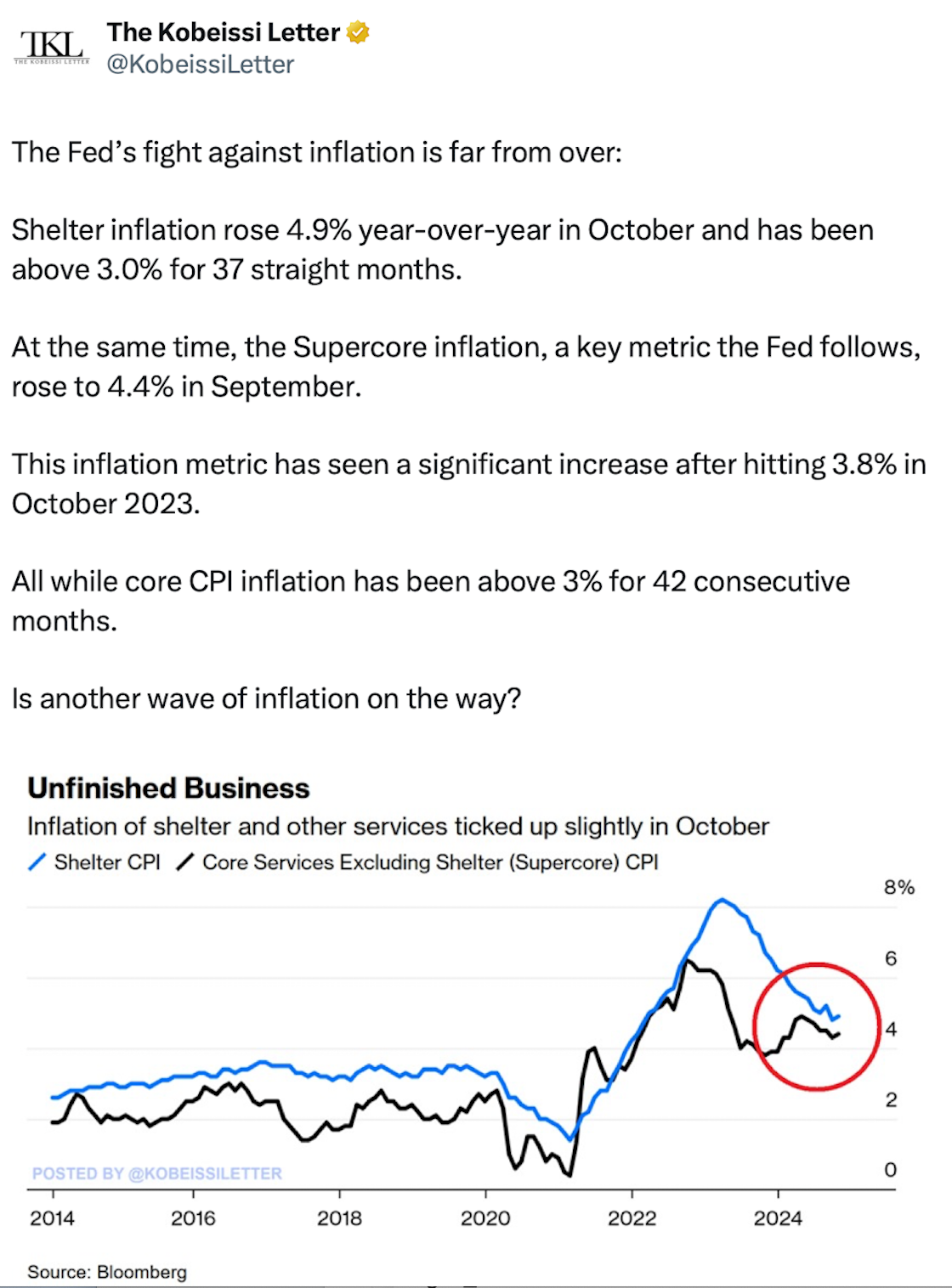

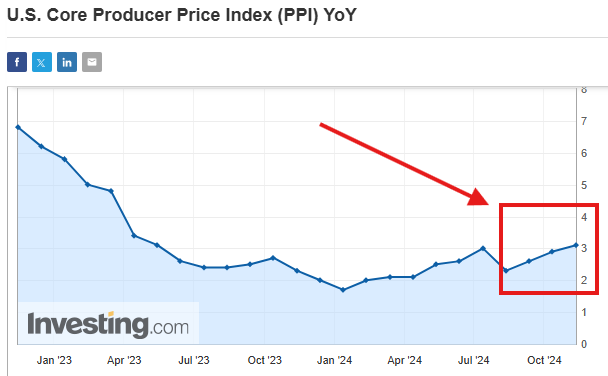

* Inflation will likely remain sticky. For the first time since April 2023, core producer price index and consumer price index inflation are back above 3%. Even as the Fed thought inflation was heading to its 2% target, it clearly is not. Inflation has leveled off well above the Fed's 2% target, yet the Fed keeps cutting interest rates.

While the Fed still prefers the PCE inflation statistic (mistakenly we believe) and running monetary policy off it, core consumer price index has risen by +0.3% (month over month) for a third straight month and remains sideways (year over year) still above three percent. Services inflation continues to be where it is coming from, as it always does, while goods prices are about flat:

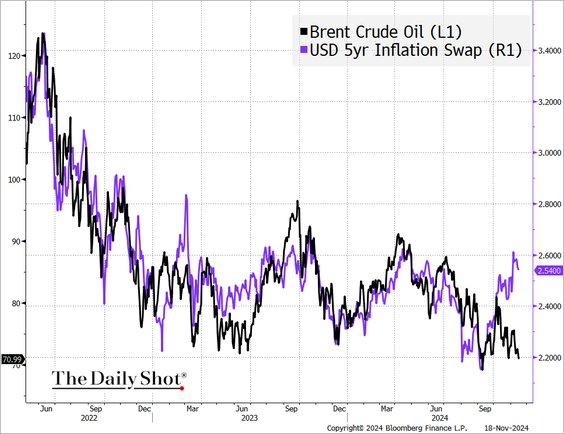

It is important to note that inflation is rising despite weakness in the price of oil:

Inflation will worsen if the new administration follows through with tariffs (raising import prices) and a tough immigration policy. The first Trump Administration took tariffs from 0.5% to 3%. Currently the President Elect is talking about taking tariffs to at least 15%. This will likely drive import and export prices higher.

* Sluggish global economic growth with persistent inflation means that the era of "slugflation" has likely begun. Indeed, as mentioned previously, for the first time since September 2022, both CPI and PPI inflation are officially back on the rise just as economic growth is decelerating.

The Liscio Report just updated its state-level tax sales receipt database, which has been an excellent indicator of domestic growth. According to the state tax data, there are recessionary warnings as reflected in that only about 1/3 of the states met their targets in October and just half recorded any year over year growth at all. This data is consistent with The Beige Book which also has struck a recessionary tone.

* Reduced corporate profit expectations. Last month we noted diminished third-quarter 2024 S&P expectations (in July +8% EPS growth was forecast, now +4% seems likely). Fourth quarter 2024 profit expectations have come off by an additional -2.1% since the start of the quarter and are currently at their lowest point since estimates began (at $62.40/share). Full year 2025 EPS projections are not far behind, falling -1.1% over the same time frame and at the lowest level since March (at $272.30/share).

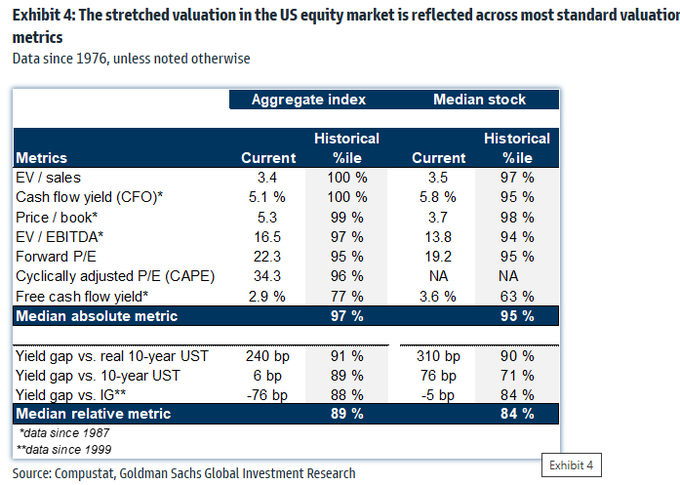

* Elevated valuations. The chart below highlights the stretched valuation of the U.S. stock market along almost every traditional valuation metric:

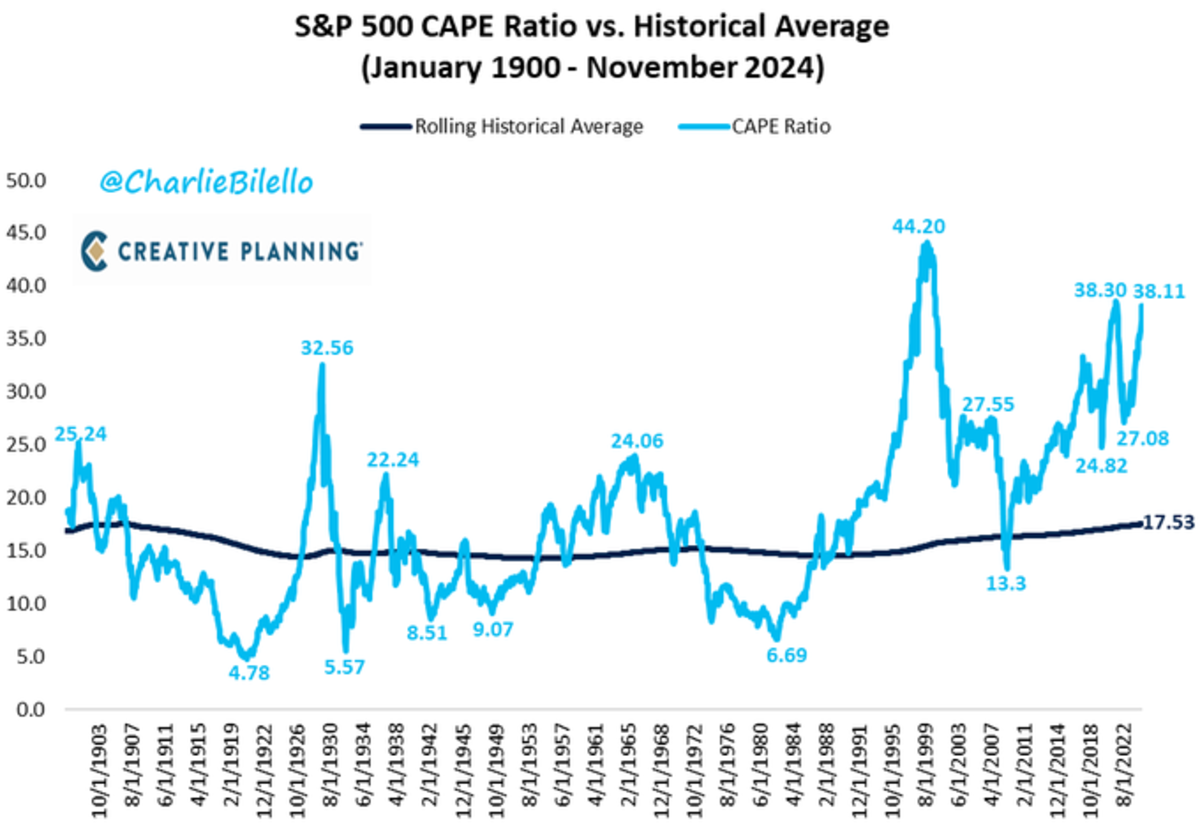

The S&P CAPE Ratio (the cyclically adjusted price-to-earnings ratio) has crossed above 38 for the third time in history and is now higher than 98% of all historical valuations:

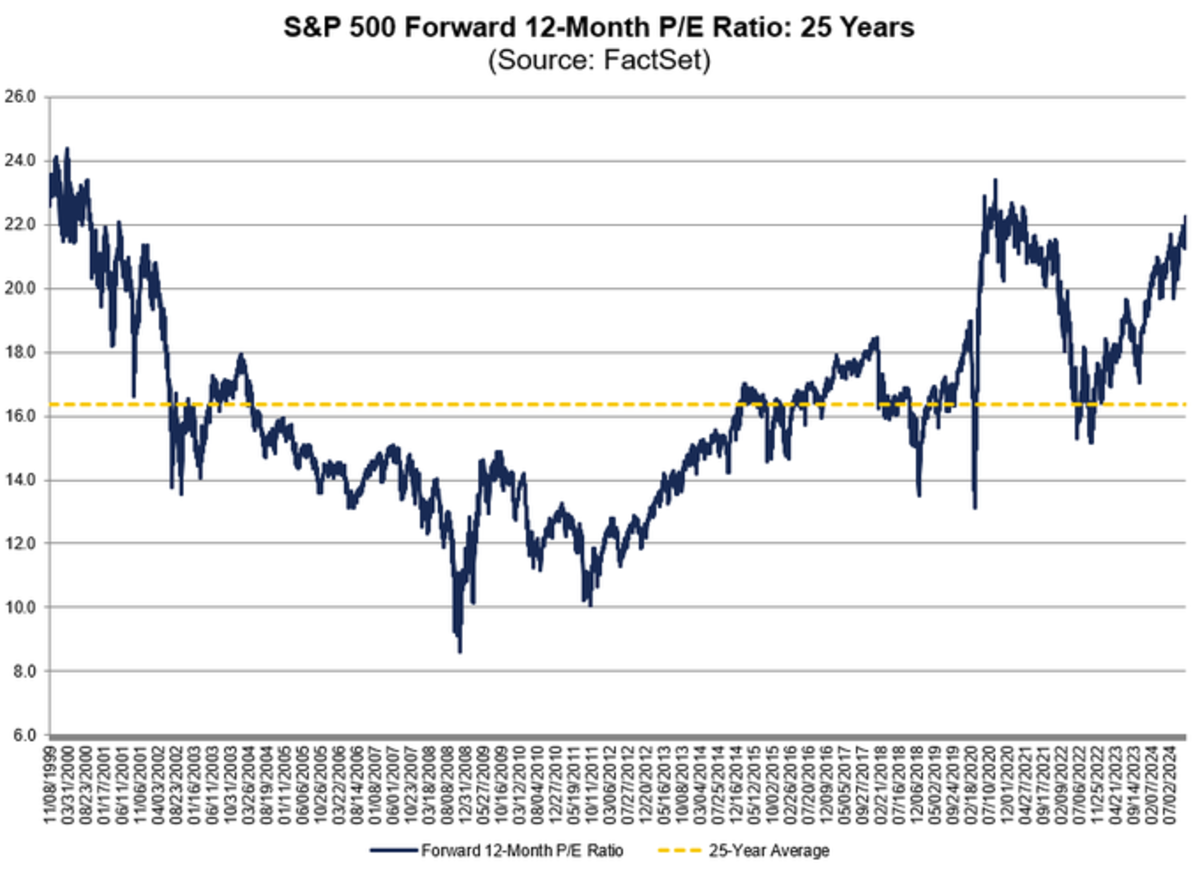

Here is a chart which demonstrates how high forward multiples are with an historical perspective:

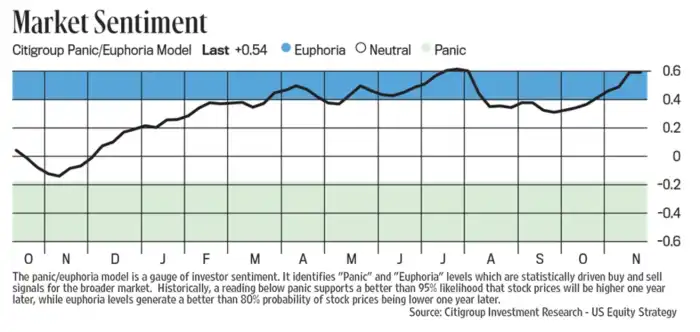

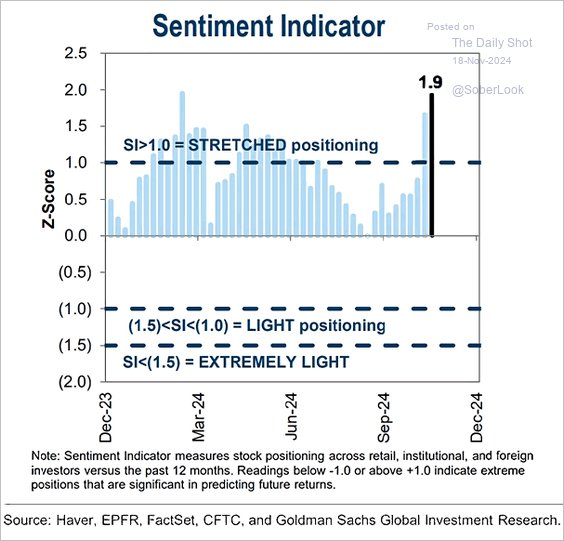

* Bullish investor sentiment (and positioning):

* Feckless monetary and fiscal policies (leading to ever higher deficits and unprecedented national debt loads). We have covered this issue extensively over the last twelve months.

* Geopolitical risks abound as evidenced by Ukraine's retaliation into Russia and Putin's saber rattling and threatening response. Arguably, should the new Administration become more isolationist those risks will likely multiply.

* Market structure risks. We have also covered this subject extensively.

Bottom Line

Trouble ahead

Trouble behind

And you know that notion

Just crossed my mind

- The Grateful Dead, Casey Jones Grateful Dead - Casey Jones (Winterland 12/31/78)

Four weeks ago in my Daily Diary on TheStreet Pro, I underscored our risk-averse strategy by quoting Warren Buffett and Charlie Munger:

Warren Buffett: I would rather be 100x too cautious than 1% too incautious — and that will continue as long as I'm around.

Charlie Munger: If we had used the leverage that a lot of successful operators did, Berkshire would be a lot bigge — but we would have been sweating at night.

This month, too, we have widely quoted Buffett — whose cash hoard he manages at Berkshire Hathaway BRK.A BRK.B has risen by another $50 billion (to $325 billion) in recent weeks.

The troubling factors and conditions included in today's commentary suggest to us that the market's upside reward is dwarfed by downside risk.

Thus far in 2024 our fears have not been well realized as the equity market has advanced meaningfully. Though we have managed to deliver a positive investment return this year — while being net short (!) — we have, thus far, failed to capture the opportunity set in equities. (We give ourselves a "D" grade for market outlook (and positioning) and an "A" grade for risk control).

Nonetheless, we feel more strongly that we will be correct in view and continue to embrace a cautious and defensive strategy based on the expectations that stocks will fall to more attractive levels to buy in the next few months.

To be direct, "group stink" (a term we use for the consensus) has a foul odor these days.

Investment data is available more conveniently and faster today, but the behavior of investors is often no more intelligent than in the past. How people react will not change. Their psychological makeup stays constant. In managing money through multiple market cycles, an investment manager should often divorce his mind from the crowd.

The herd mentality and the dominance of passive products and strategies that worship at the altar of price momentum sometimes causes market participants' IQs to become paralyzed. Arguably, this is one of those times.

Given the rising risks and nosebleed valuations, we don't think investors in the last few months are acting very intelligently.

In markets, smart doesn't always equal rational and can produce some unexpected and unwelcomed outcomes:

Long Term Capital Management had hundreds of millions of dollars of their own money and had all that experience. The list included Nobel Prize winners. They probably had the highest IQ of any 100 people working in the country — yet the place still blew up. It went to zero in a matter of days. How can people who are rich and no longer need money do such foolish things?

- Warren Buffett

We are of the strong belief that to be a successful investor over several market cycles, you must divorce yourself from the fears and greed of the people around you, although, at times, it is almost impossible.

It remains our view that the U.S. stock market is overvalued against interest rates, earnings, cash flow and sales — and most other metrics that have stood the test of time.

As reflected in the vanishing equity risk premium, fear and doubt has left Wall Street.

Slugflation may lie ahead as the labor market weakens and, for the first time in over two years, both consumer price index and producer price index inflation are back rising — at a time in which price earnings multiples are, on average, in the 95%-tile and interest rates are resuming their rise (the yield on the 10-year Treasury now stands at near 4.50%).

Again, we take our cue from Buffett:

Be fearful when others are greedy.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.