Doug Kass: It's Time to Return to the Land of the Living

Here's why I am now moving to an expanded net long exposure and what stocks will provide fertile ground for my long selections.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This column emphasizes the obvious and something I should spend more time dwelling on.

It is frankly sometimes lost on myself (and by others) that equities perform better than any other asset class over lengthy periods of time. As well, the asymmetry of returns on long positions vs. returns on short positions are both profound and tautological.

Currently, many equities have been ignored by investors and have performed far weaker than the averages — and this is the fertile ground for my long selections (now).

Moreover, the multitude of my fundamental concerns (listed in this column) are slowly being embraced and are beginning to be discounted in the markets' recent decline.

What follows is a compilation of recent commentary in my Daily Diary on the TheStreet Pro and comments delivered to my investors at my hedge fund, Seabreeze Partners:

In early August I warned my investors:

"As a result, we are growing more confident that stocks will ultimately decline to a level in which we will want to participate on the long side... While a good entry point may lie ahead — it may come from still lower levels."

Over the first few days of September equities quickly declined by about five percent — and have rallied a bit from there but remain lower for the month:

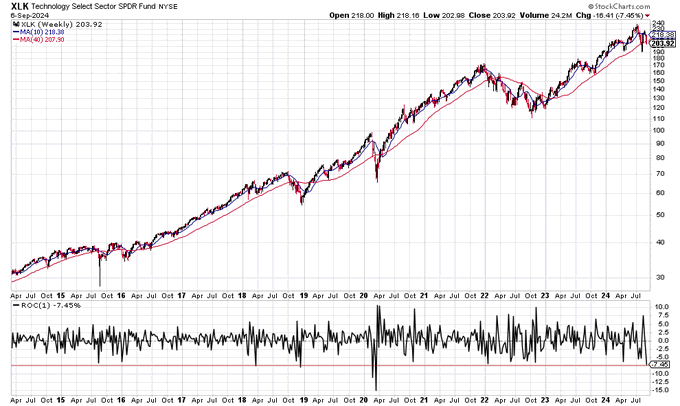

My defensive positioning has insulated our hedge fund (Seabreeze Partners) from the September decline — which has been far worse (on a percentage basis) for The Magnificent Seven (Microsoft MSFT, Amazon AMZN, Apple AAPL, Alphabet GOOGL, Meta Platforms META, Nvidia NVDA and Tesla TSLA) and some of the other former market leaders. Indeed, large-cap technology stocks (as measured by (XLK) ) had its worst week since Covid (and one of its worst weeks in the past decade):

In Act I, Scene 3 of William Shakespeare's "Hamlet," Polonius (Ophelia's father and King Claudius' chief minister) delivers a long monologue that contains several seemingly good pieces of advice — the most important of which appears below:

I have long held to the notion in my Diary and to my Limited Partners that we don't believe in being "Perma" anything — I manage my Partnership's portfolio by evaluating upside reward vs. downside risk — with a calculator in hand and through sharp and hard-hitting primary analysis. As a contrarian — armed with a sense of intrinsic values — I am willing to buy weakness and sell strength. (Of importance I avoid distractions and invest/trade unemotionally. I generally avoid charts of which there are many nice ones that lie at the bottom of the sea! Nor do I listen to the memorized sound bytes and confident but superficial analysis in the business media).

So, to paraphrase Shakespeare, "neither a Perma Bull, nor a Perma Bear be.”

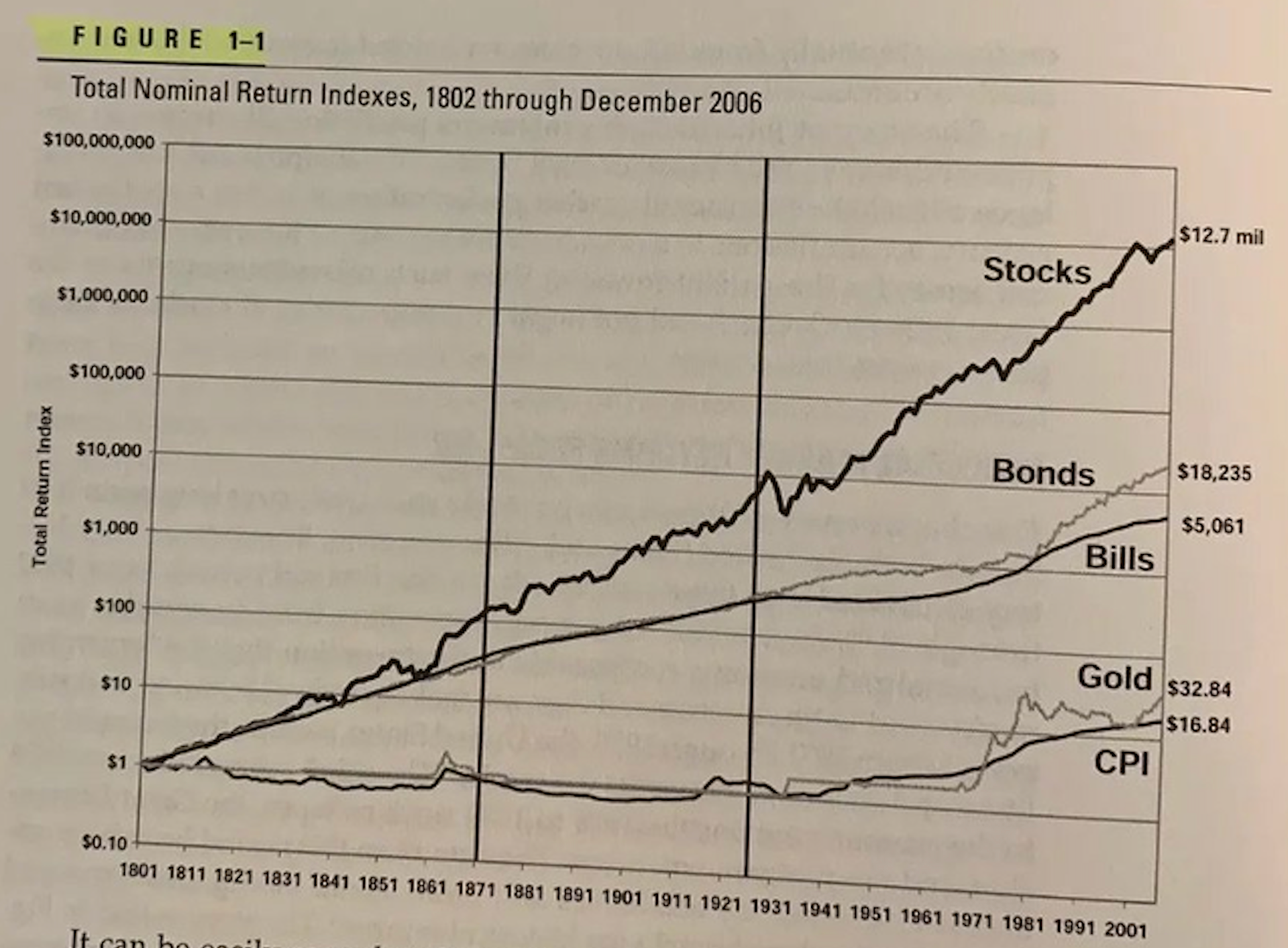

The most important feature of this morning's column is that I want to emphasize, again, that I fully recognize that equities perform better than any other asset class over lengthy periods of time.

Long investments generally create and generate wealth (see the chart below) while being short equities (though providing asymmetric returns over extended timeframes) can protect capital over more limited intervals:

This year I have held to an ursine market outlook reflecting the prospects for slowing global economic growth and sticky inflation (we call this "slugflation"), that high short-term interest rates provided equity-like returns (with little volatility and risk), the perils associated with market structure and a changing market landscape (in which machines and algos had a disproportionate role on stock prices), feckless fiscal (the massive annual deficit and accumulated U.S. debt load are draining the potential for economic growth) and wrong-footed monetary policies, growing political and geopolitical risks and too ebullient bullish investor sentiment (which was reflected in high valuations).

Though I maintained a negative market view, I elected not to run a large short book.

Rather, I adopted a defensive pairs trading and investing strategy that incorporated both longs and shorts (much like the father of the hedge fund industry, Alfred W. Jones, introduced 75 years ago).

On top of our pairs strategy, I superimposed a short book of between 10% and 20% gross short exposure, on average, throughout 2024. Many of those unhedged and core investment shorts fared well, despite the market's gains (e.g. RILY, WGO, CHGG, WOOF, FIGS, MCD, SBUX, etc.). Others (like Index hedges) sometimes proved problematic in the FOMO — like rally this year. But also helping was opportunistic trading — the benefit of which was derived by the dominance and influence of machines and algos that often exaggerate short term price moves.

This strategy provided our hedge fund with positive returns — without taking unnecessary risks — despite our gloomy market view.

While I continue to be concerned about the equity markets I am now less so for the following reasons:

* The multitude of my concerns (listed above) are slowly being embraced by the consensus and are beginning to be discounted in the markets' recent decline.

* While overall valuations are still elevated, a number of individual equities have suffered even as the averages have enjoyed robust market gains this year. This expanding universe of beaten-down stocks provide us with fertile territory for selecting new long investments.

* Interest rates are likely to drop significantly — providing less of an alternative to equities.

Accordingly, I am now transitioning from our pairs strategy and I have retreated from our layer of shorts. I envision returning to "the land of the living" and an expanded net long exposure — particularly if those specific stocks that I currently deem attractive on a risk/reward basis continue to the fall as they notably have during the first week of September and over the last few months.

As always, my plan to increase our net long exposure is a dynamic one. It will be a function of a continued evaluation of the bigger picture (economy, interest rates, inflation, policy, sentiment, valuations, etc.). But given that many stocks have retreated far deeper than the Indices, our exposure decision will now be as much subject to the opportunities presented in individual securities as in our market macro view/judgment.

I have already shifted from a sliver of being net short to a sliver of being net long — with a number of opportunistic buys late last week. This shift is consistent with last month's comments to my investors in which I wrote:

"As (or if) stocks continue to fall and we begin to transition from a defensive pairs strategy into a modestly more bullish (and opportunistic) longer positioning, our monthly returns are likely to exhibit much more volatility than we have experienced over the last nine months."

Bottom Line

I expect more volatility ahead. While this may scare some investors, at my hedge fund I relish the opportunity to invest opportunistically and unemotionally. The continued lack of predictability will also provide us with trading opportunities intended to complement our investing.

I remain confident in my ability to navigate the volatile markets and uncertainties of economic outcomes because my analysis is objective, fundamental (understanding intrinsic values), hard-hitting and my investing is dispassionate.

Currently, many equities have been ignored by investors and have performed far weaker than the averages — this is the fertile ground for my long selections (now).

Moreover, the multitude of my fundamental concerns (listed in this column) are slowly being embraced by the consensus and are beginning to be discounted in the markets' recent decline (as always we should be "second level" thinkers).

For these reasons and others I am now transitioning somewhat from my pairs strategy of the last nine months. I have also retreated from my layer of shorts that were superimposed with the pairs.

I am now returning to "the land of the living" and an expanded net long exposure — particularly if those specific stocks that I currently deem attractive on a risk/reward basis (MSOS, OXY, SLB, OIH, DIS, VVV, CMG, etc.) and others that I am yet to own — continue to the fall as they notably have during the first week of September and over the last few months.

As often stated, high stock prices are the enemy of the rational buyer and low stock prices are the ally of the rational buyer.

Since I am a value buyer, my fundamental approach and emphasis on in-depth security analysis (hopefully) provides me with a clear understanding of the intrinsic value of equities — allowing me to be increasingly greedy when others are overcome by fear.

This commentary was originally posted Wednesday, September 11, in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass was long AMZN (VS) OXY common (VL), calls (S), SLB (VS), OIH (M), MSOS common (L) and calls (S), CMG (S), VVV (S); and short WGO (S), CHGG (VS), FIGS (VS), RILY (VS), SBUX (S).