Doug Kass: It Is Not Different Time

By my calculus, there is three times or more downside potential than upside presently.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Equities, contrary to our expectations, continued to ramp higher during the last month.

The last several weeks have felt like a battle in which I have felt much like the Greek mythological character Sisyphus who was punished by the gods for cheating death and who was condemned to eternally roll a boulder up a hill, only for it to roll back down each time. While the myth symbolizes the endless struggle and futility of human efforts, this missive incorporates what I believe to be a deteriorating fundamental economic and corporate profit proposition on top of stretched valuations — making me feel more like Elpis (the goddess of hope) than Sisyphus as I have growing confidence that my market expectations might be soon realized.

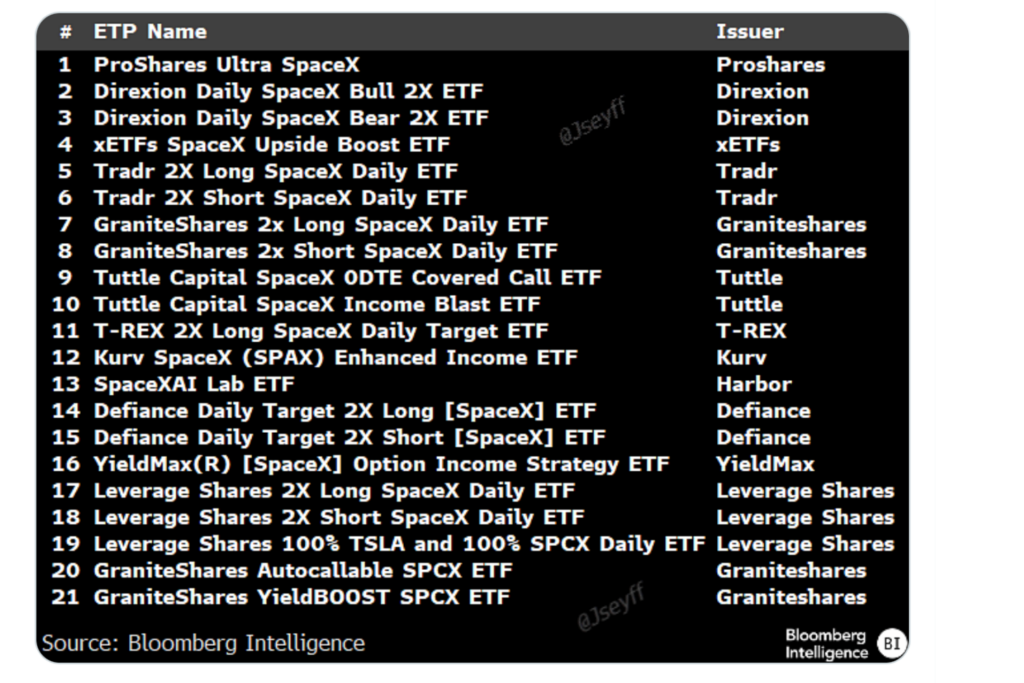

For the second month in a row, it was All AI All The Time, with large-cap technology the dominant contributor to the market’s rise. Only 10 companies contributed to two-thirds of the overall rally over the last eight weeks. (See our comments about the foul market breadth later in this commentary)

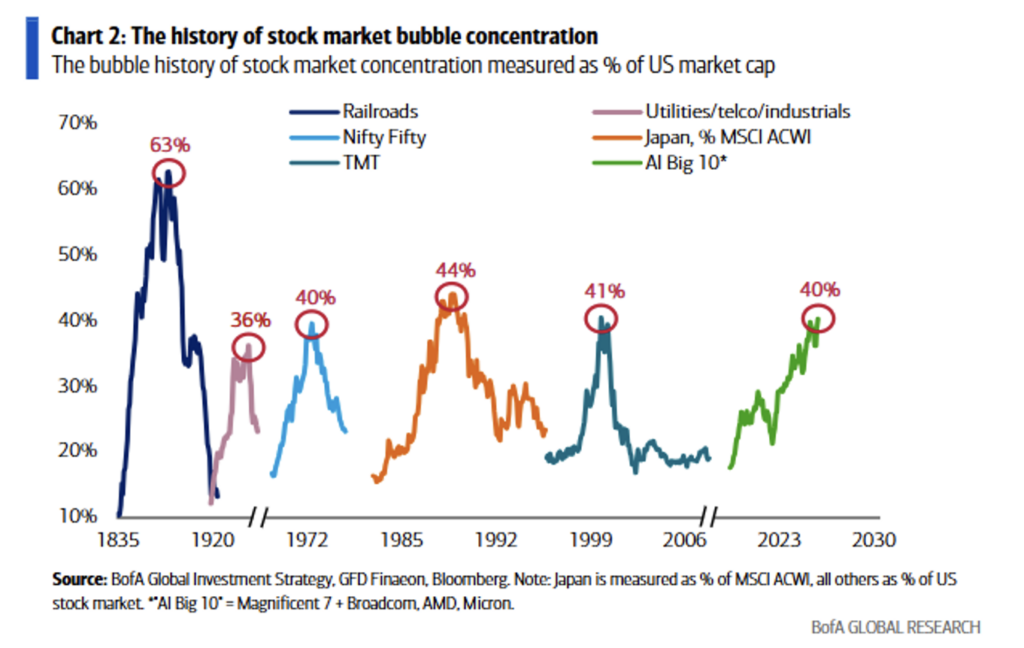

We have not seen a stock market this concentrated around a single theme in 150 years:

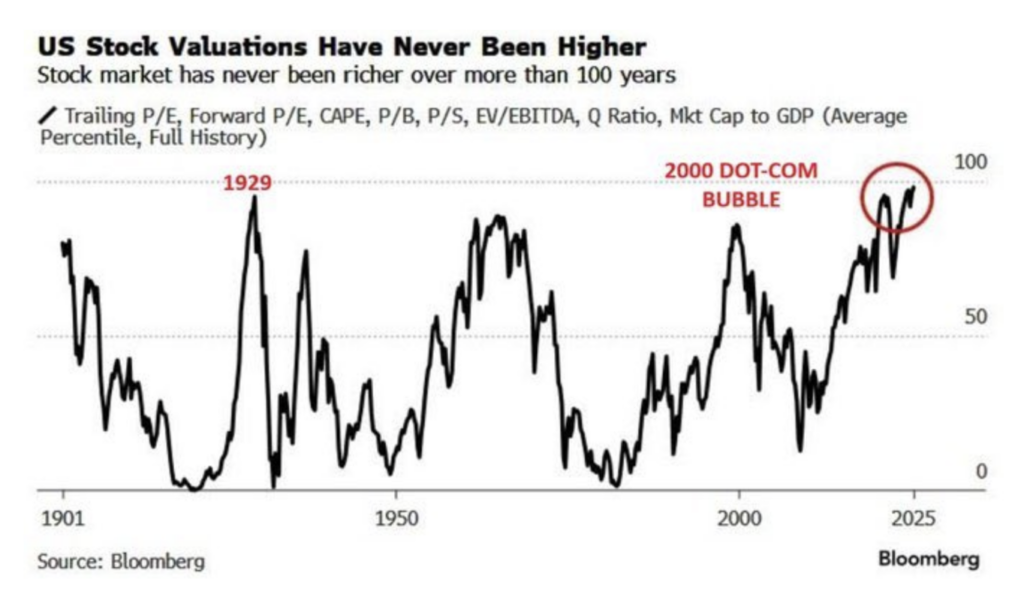

As the S&P Index made a new high last week, only 21 stocks also made record highs. By comparison, only 20 stocks made new highs at the March 2000 top. Beyond the aforementioned concentration levels, there has never been a more expensive market in history:

For these reasons and others, I continue to maintain a cautious investing posture in my investment partnership — sitting in a net short exposure.

As subscribers are aware, I have been defensively positioned for some time, in the belief that the reward vs. risk setup was unattractive. With the exception of the brief market dips in 2024 (April), 2025 (February) and 2026 (March) I have maintained my net short exposure. Disappointingly, that strategy did not allow us to take advantage of the opportunity set provided by the market advance over the last two years, which was a period in which caution became the most expensive position on Wall Street.

Despite the net short exposure and a wrong-footed investment view, on a positive note, through a combination of opportunistic trading, good risk control/management and some excellent shorts — we have had a long streak of positive monthly investment performance.

To me, the current AI-driven equity rally increasingly resembles a late-stage speculative bubble: extremely narrow market leadership, stretched valuations (in the 97% percentile), euphoric positioning (and absence of fear), collapsing volatility, massive IPO supply ahead and, of course, excessive concentration in mega-cap tech. Central banks still remain too loose globally, which is prolonging the bubble, but once policy tightening meaningfully bites, the unwind could resemble prior post-bubble rotations (with the historical analogs a combination of 1929, Japan 1989, Dotcom 2000 and China 2007 and The Great Recession (2008-09)).

As noted, I am increasingly confident that my concerns will be reflected in lower stock prices and in today’s commentary I will discuss the equity risk discount, a foundational part of my ursine market outlook.

My Concerns Are Multiplying and Intensifying

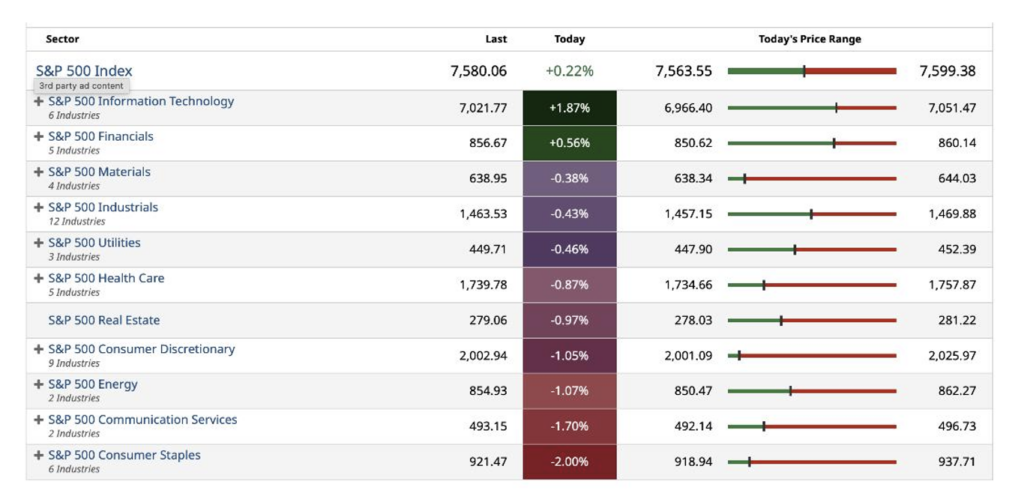

An increasingly slender sector participation underscores the market’s narrowing leadership, as last Friday’s action demonstrated:

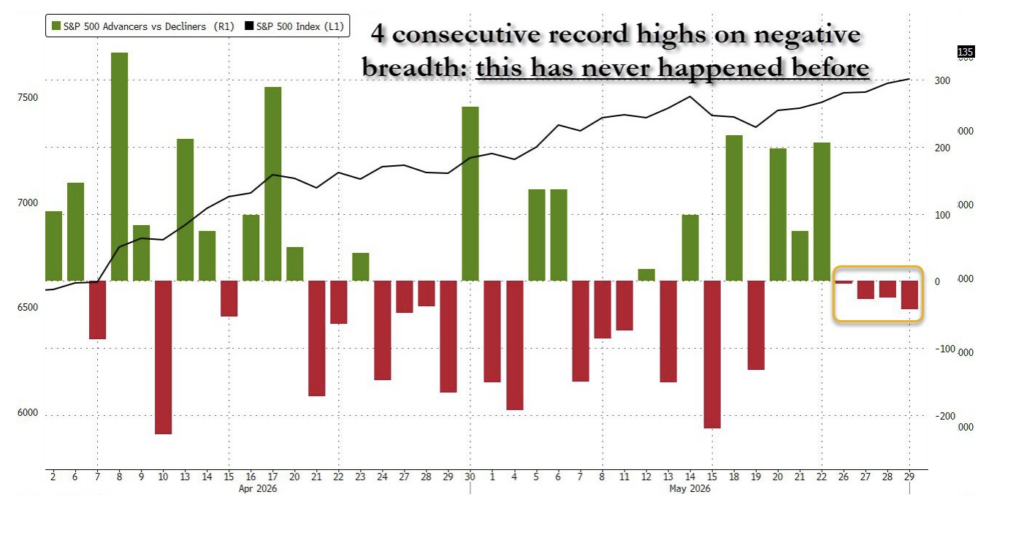

In this past week, the S&P 500 has recorded four consecutive all-time highs while a majority of equities were actually falling. This has never happened before:

The S&P advance/decline line hasn’t made a new high since April 17, despite multiple all-time highs made by the Index. The last time we had such a divergence was November 2024 to February 2025 and that eventually led to a 20% drop:

Call me “old school,” but I continue to adhere to one of Bob Farrell’s 10 Lessons of Investing:

Lesson #7: Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

Translation: Breadth is important. A rally on narrow breadth indicates limited participation and the chances of failure are above average. The market cannot continue to rally with just a few large-caps (generals) leading the way. Small- and mid-caps (troops) must also be on board to give the rally credibility. A rally that lifts all boats indicates far-reaching strength and increases the chances of further gains.

Last month we wrote:

In our view, the markets have ignored the same conditions that set off the January-February selloff. None of the non-war issues that drove stocks lower have been resolved:

* Oil prices are off their highs but are likely to remain elevated because of the magnitude of the supply shock and continued uncertainties related to the Iran conflict.

* Inflation is now rising on a sequential monthly basis — and is higher than before the conflict in Iran.

* Interest rates will be higher for longer.

* The 2026 annual deficit will approach $2 trillion, neither political party show any signs of being fiscally responsible.

* The U.S. debt will hit $40 trillion this year — the cost of servicing the debt is over $1 trillion/year.

* With a burgeoning deficit, stiff debt load and persistent inflation, the Fed’s hands are tied.

* While private equity’s problems are not systemic, the leverage they brought us remains in place. KKR Private-Credit Fund Takes $560 Million Loss – WSJ

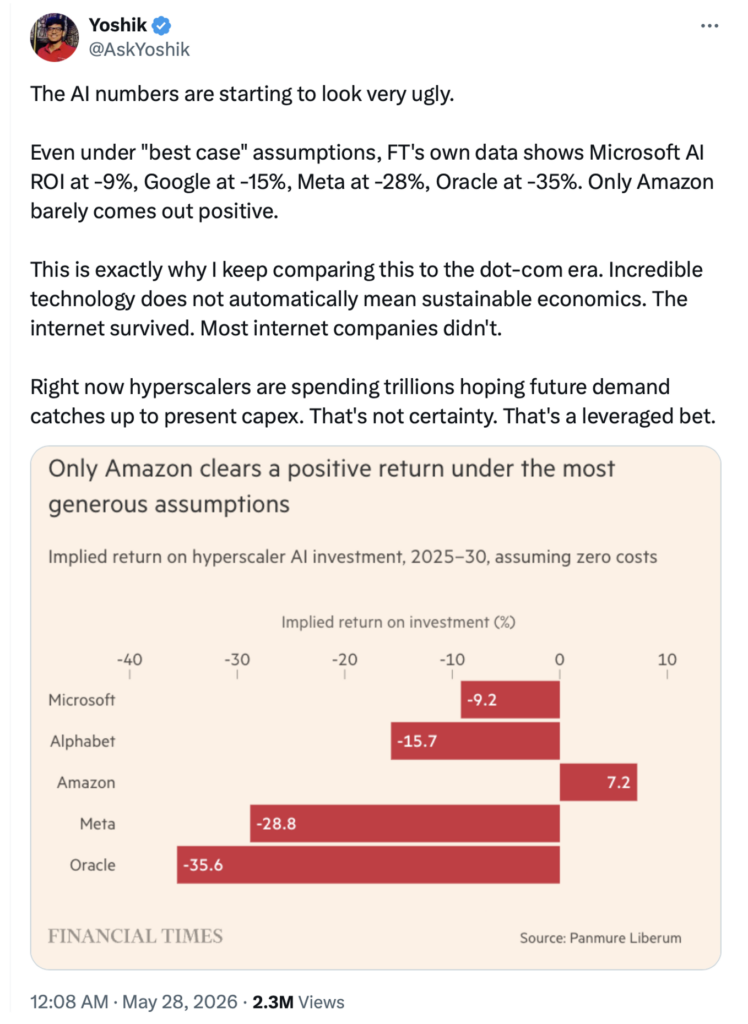

* The enormous amount of money spent on AI will probably never see an adequate return on investment. As noted by Stan Druckenmiller (again!), AI’s societal and transformative impact could rival the internet’s life-changing influence — and so may the stock market consequences (rhyme) be similar:

“If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to fruition. That’s not going to happen with AI. But it could rhyme – AI could rhyme with the Internet as we go through all this capital spending we need to do. The big payoff might be four to five years from now. So AI might be a little overhyped now but under-hyped long term.”

With 45% of the S&P Market Cap AI or AI-adjacent, What if the AI boom… goes in reverse? Panmure Liberum – Strategy

Or even worse, what happens if, at the limit (as two professors have recently written) companies “automate themselves to boundless productivity and zero demand — an economy that produces everything and sells it to nobody:

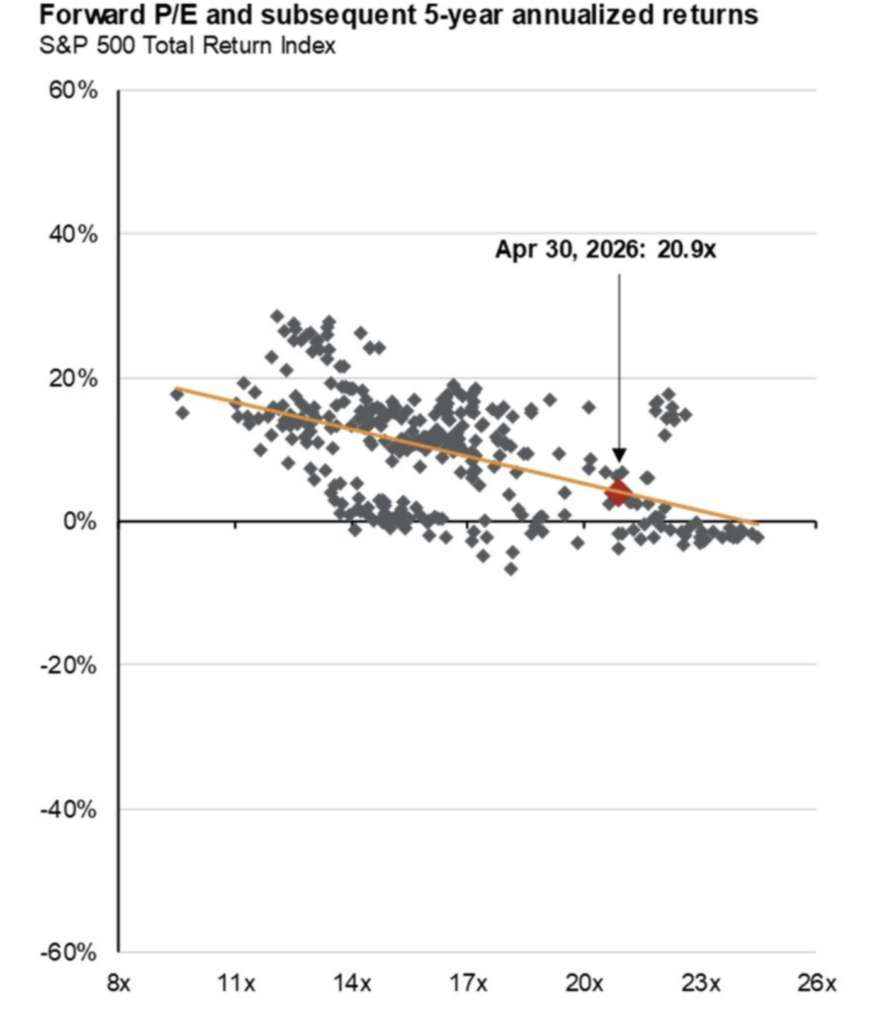

* Valuations are a terrible clock but a good weather forecast. That valuations are stretched is an understatement. See Cape Shiller above. The Buffett ratio (the total market capitalization divided by GDP) hit an all-time high this week). Most other traditional metrics indicate that equity valuations are in the 97 percentile.

* Many bulls highlight the improving strength in projected 2026 S&P EPS. They argue that this year’s robust growth in profits (at about +17%) — justify current valuations. However, if one takes out Nvidia (NVDA) and Micron (MU), 2026 S&P EPS growth falls to under +10%.

I am increasingly confident that our concerns (are multiplying and intensifying) will be reflected in lower stock prices and in today’s commentary, I will discuss one factor, the equity risk premium (now a discount), which incorporates some of the foundation of our ursine market outlook.

It Is Not Different This Time

To borrow a phrase from Warren Buffett, the voting machine is overwhelming the weighing machine.

For nearly three years, the markets and its participants have ignored elevated valuations.

How much longer can the S&P 500 and the other major indices deliver upside when price-earnings multiples and equity risk premiums are in the 95th percentile or higher?

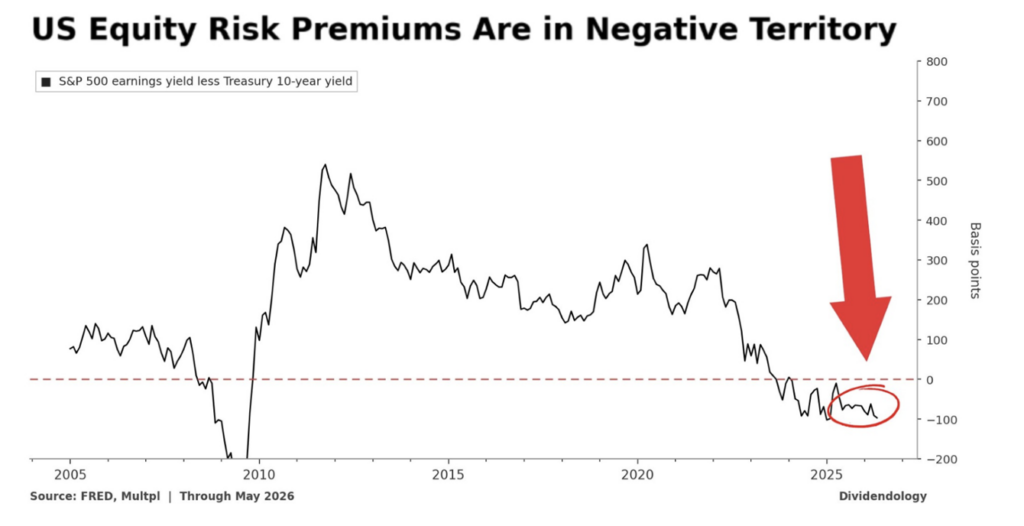

With consensus (I think overly optimistic!) 2026 S&P EPS at $330/share, the senior average trades at 23x and the equity risk premium is negative.

On projected 2027 S&P EPS consensus of $375/share (I think overly optimistic as well) the S&P trades at 20.5x and the equity risk premium is only at 50 basis points, both in the 93rd percentile.

The steady decline in the equity risk premium is a metric I pay very close because. Historically, it has been an excellent indicator future investment returns…

My focus on the ERP has contributed importantly to my incorrect market view and a missed opportunity set on the long side.

The Equity Risk Premium

Let’s examine the equity risk premium, which is the difference between the S&P earnings yield (the inverse of the P/E ratio) and the risk-free rate (the 10-year Treasury note yield is typically used):

The equity risk premium tells us how much excess return investors are being paid to own stocks over a risk free Treasury bond.

Historically, equities typically offer a three-to-four percent premium over Treasuries. Such a premium makes sense because it compensates investors for volatility, drawdowns and uncertainty.

Right now, according to the chart above, the investor is being paid negative in equities vis a vis bonds. The ratio is saying that holding bonds is more risky than owning stocks — this is a radical notion, at an extreme! Again, this means:

1. Investors are not being paid extra to take on risk in stocks.

2. Stocks are offering similar or worse “yield” than bonds.

3. Valuations are materially stretched relative to interest rates.

Stated simply, this means that holders of equities are taking more risk for less reward (than bonds). When this has happened in the past (most notably during the dot-com bubble and leading up to The Great Recession in 2007-09), forward returns have been somewhere between non-existent and negative:

Bottom Line

“What we learn from history is that we do not learn from history.”

– Benjamin Disraeli

As noted earlier in this opener and based on historical metrics, there has never been a more overvalued market in history.

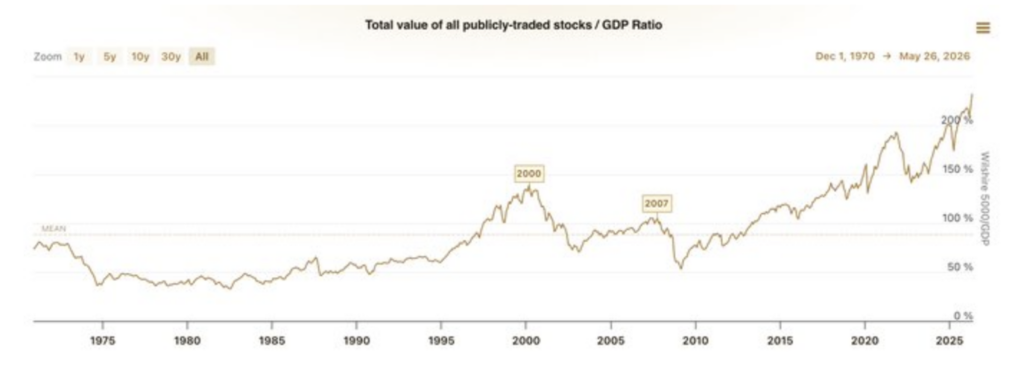

It is hard to understand why stocks have been impervious to elevated valuations (a record high in overvaluation in both the Buffett Indicator and a near record in Shiller’s CAPE ratio), as well as an equity risk discount. As an example, the Buffett Indicator (the total value of all publicly traded stocks divided by GDP) is at 236%, making this the most expensive stock market in history:

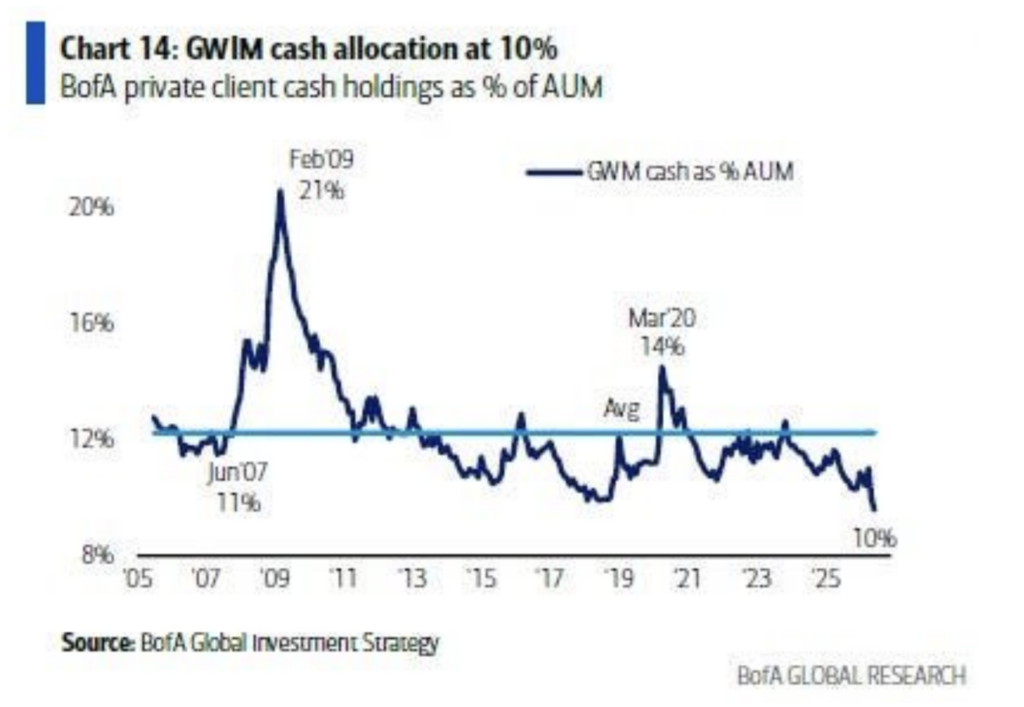

Investors are euphoric — Bank of America’s private wealth clients hold the lowest amount of cash in two decades):

The market has become a casino — with more ETFs (many of them 2x leveraged) listed on the New York Stock Exchange than individual securities. 0DTE (zero-day to expiration options) account for about 70% of total option activity.

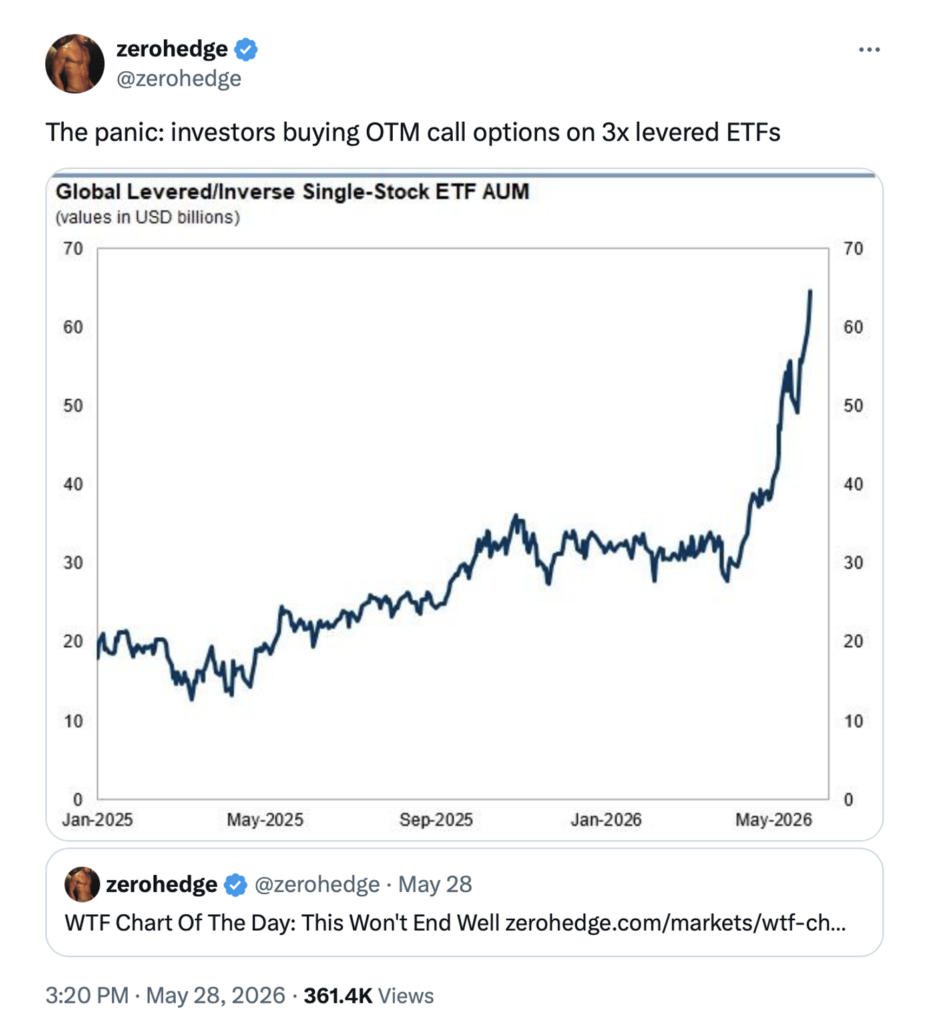

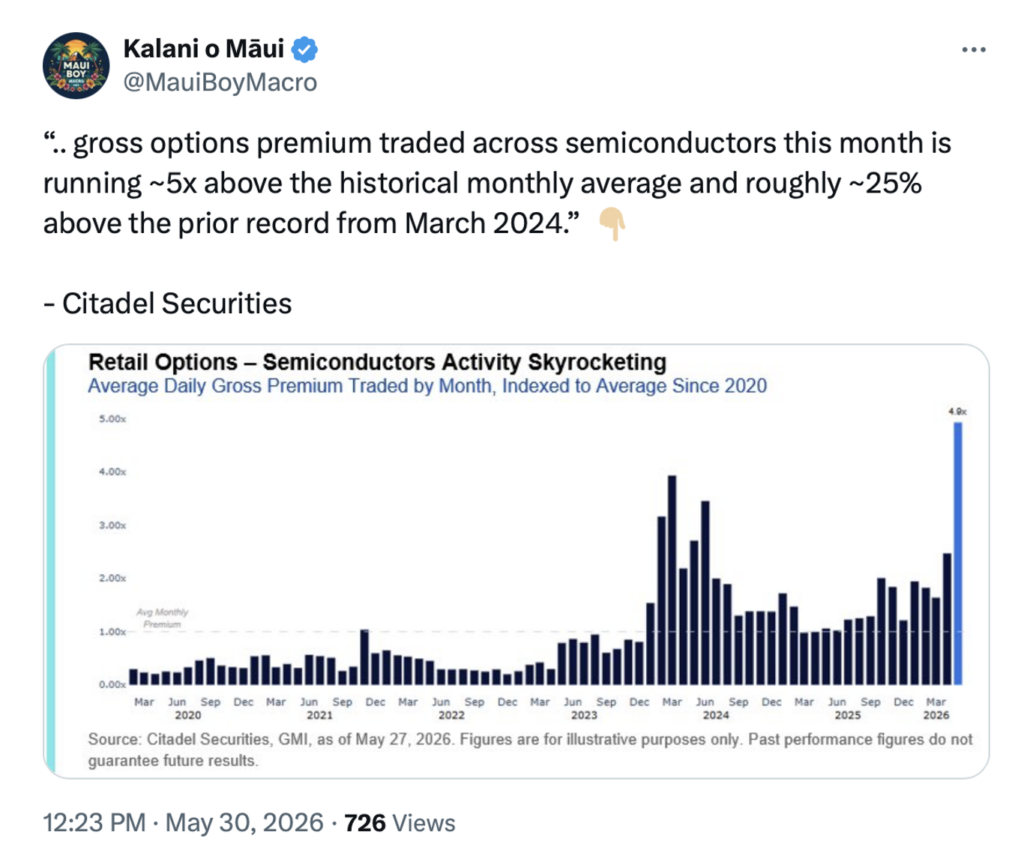

Speculation is running amok:

Moreover, the markets are growing increasingly synthetic:

One answer for the recent market momentum is the dominance of passive products and strategies that worship at the altar of price. They know everything about price and nothing about value.

Other explanations are the euphoria in AI and the fear of missing out (FOMO).

Nonetheless, excessive valuations, excesses and the idea of a “new era” are nothing new — we have seen these at the top of other cycles (for reasons of overenthusiasm/heated speculation).

Finally, it is my strong view that the components of the equity risk premium suggest, at the very least, a mean reversion back towards the historical premium as 2027 EPS estimates come down and interest rates likely rise.

Let’s not forget when Berkshire Hathaway’s shares were suffering in late 1999 and many were questioning Warren Buffett’s investing philosophy (as they are currently with his near $400 billion cash hoard) — right before a more than -80% drawdown in the Nasdaq.

To me, it’s not different this time.

I continue to choose the weighing machine over the voting machine.

This commentary was originally posted in Doug’s Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.