Doug Kass: Icarus Is Flying Too Close to the Sun

The U.S. stock market is beginning to look as vulnerable as it was in 1974 (Nifty Fifty) and 2000 (Dot-com) — similar periods of narrowness in market leadership and participation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In Greek mythology, Icarus (and his waxen wings) perished when he flew too close to the sun.

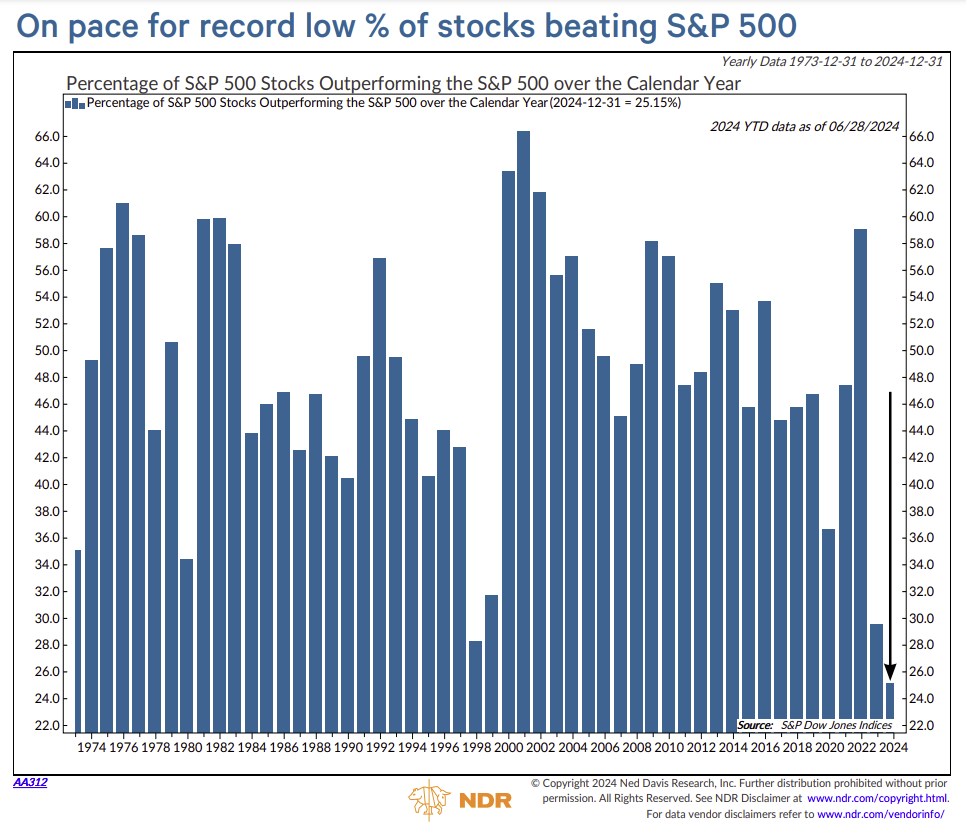

In 2024, the stock market's waxen wings are the unprecedented narrowness of breadth and leadership:

Throughout history there has always been an expiration date on markets like this.

Bad breadth and valuations are ignored until they aren't.

Feeding the market's bifurcation has been the dominance of passive investing which has delayed but hasn't extinguished the expiration date.

It is one thing for traders, investors and machines to worship at the altar of price. But it is another thing for asset allocators, driven by that market's momentum, to be forced to be longer (and more concentrated) than good sense would dictate.

When will the market's waxen wings melt? While that is not an easy question to answer, the rubber band has been stretched as demonstrated by so many charts/tables that quantify the narrowing leadership and participation.

Those wings melted at the top of The Nifty Fifty Market (in 1974), when portfolio insurance kicked in (October 1987) and in early 2000 at the end of the dot-com boom. The celebrated busts — accompanied by complacency, greed and chirping (see some the observations in our in the Comments Section of my Daily Diary) — were unexpected, swift and deep and had a debilitating impact on a lost generation of investors.

Adding importantly to the market's vulnerability (produced by a narrow momentum-based preoccupation) has been the divergence between stocks and bonds.

The equity risk premium recently fell back to the thinnest spread since 2006. And, with the S&P dividend yield at only 1.35% (compared to 1.47% last month, 1.66% a year ago and the long term average of 1.84%) vs. the six-month Treasury bill yield of 5.32% — it can be argued that equities are more overvalued relative to fixed income than at any point in several decades.

To date the relationship between stocks and bonds have been also ignored — even though interest rates (and the risk free rate of return) are fundamental to the market's intrinsic value.

As mentioned in a column recently, bulls have been mostly right for the wrong reasons.

As an example, back in the June, 2023 I debated Tom Lee at a Street conference at the NYSE:

At that time, the foundation of Tom's bullish argument was threefold:

* Interest rates will fall.

* The Federal Reserve will cut rates.

* The market would broaden. (Tom has been quoted that he expects the Russell Index to be +50% in 2024.)

Fast forward to today and none of these developments have occurred:

1. Interest rates have risen and the equity risk premium is at a multi-decade low. Meanwhile, the S&P dividend yield is at 1.35% compared to over 5.30% for six-month Treasuries. (It is a rare event for the S&P dividend yield to be nearly 4x the yield on Treasuries.)

2. Expectations for a Federal Reserve rate cut has declined from six events to 1-2 cuts over the balance of the year.

3. The market has broadened out to the downside (not to the upside). The equal-weighted S&P is weak, the Russell is lower on the year and we have the most narrow/concentrated leadership in history:

But Tom was right... however, the sizeable reset in valuations was caused by other factors than Tom anticipated (read: liquidity, animal spirits, fear of missing (FOMO) and market structure related).

That said I would rather be right for the wrong reasons than be wrong for the right reasons.

But there are no do-overs or crying on Wall Street.

More Doug Kass:

- Cannabis' Reward vs. Risk Has Never Been as Attractive as Now

- Warren Buffett, Berkshire Hathaway, and the XLF

- My Updated Market Outlook

Bottom Line

Equities have recently ignored the further narrowing in market leadership and participation — as well as the rise in bond yields.

Market participants are chirping more than ever as their portfolios, dominated by a handful of "compounders," lap the rest of the market.

Nonetheless, we should learn from history as these divergences have ended badly and unexpectedly.

From the legendary "Uncle" Bob Farrell's Ten Rules of Investing:

1. Markets tend to revert to the mean over time.

2. Excesses in one direction will lead to an opposite excess in the other direction.

3. There are no new eras – excesses are never permanent.

4. Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways.

5. The public buys the most at the top and the least at the bottom.

6. Fear and greed are stronger than long-term resolve.

7. Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

8. Bear markets have three stages – sharp down, reflexive rebound, and a drawn-out fundamental downtrend.

9. When all the experts and forecasts agree – something else is going to happen.

10. Bull markets are more fun than bear markets!

Many forecast with precision — which as I have written, is a "fool's errand." That applies both to Bulls (Fundstrat's Tom Lee is looking for much higher prices by year-end) and bears (JPMorgan's Marko Kolanovic is calling for a 23% drop).

As I wrote yesterday:

Warren Buffett once wrote that "the only value of stock forecasters is to make fortune tellers look good." He also commented that "short term market forecasts tell you more about the forecaster than the forecast."

In reality we never know the timing when the weight of the narrowing and higher yields finally are impactful.

But from my perch there is little question in my mind that the market's downside risks are accumulating relative to the upside reward and that a mean reversion in stock prices is moving ever closer.

I remain bearish — not only because of the aforementioned narrowness and interest rates — but because of a host of other fundamental reasons:

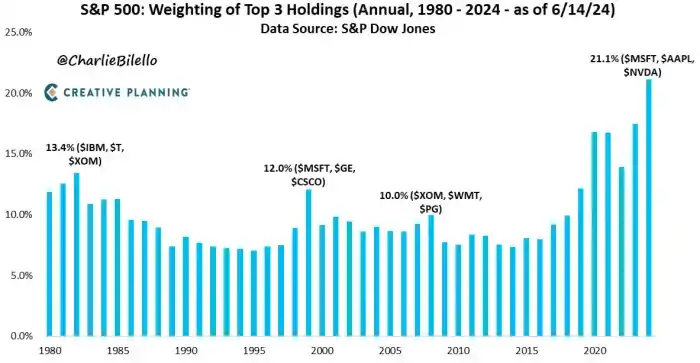

* Equity performance has been top heavy — with five large cap technology companies skewing returns. Nvidia (NVDA) undefined has accounted for 35% of the S&P Index's 2024 performance while four others (Google (GOOGL) , Meta (META) , Microsoft (MSFT) and Amazon (AMZN) ) are responsible for another 26% of the annual return. Not since the 1960s have five stocks accounted for so much (61%) of the total market return.

* Corporate profit performance is also reliant of mega-cap tech. In Q4 2023 corporate profits rose by +14% but without the seven largest tech stocks there was a -9% drop in profitability. In Q1 2024 corporate profits rose by +6%, but without the contribution of the Mag 7 there was a -2% decline in profits.

* Corporate profit expectations are unrealistic. According to my friend David Rosenberg’s (Rosenberg Research), arithmetically “backing out” from current valuations, the markets expect +17% per year growth in profits over the next five years. This compares to the actual long-run average for earnings growth in a five-year span over the past century of just +6%/year. A profits forecast of +17% is thus a near and highly unlikely two standard deviation event — particularly given the likelihood that the next Administration may be forced to increase both individual and corporate tax rates to fund the U.S. deficit.

From David:

Outside of the distortions around COVID-19 in 2020, this embedded EPS growth forecast was only exceeded by the prior Tech mania in the late 1990s. And we know how that ended — inevitably, that five-year forward earnings growth view reverted to the mean as the sector (typical with manias) became beset with excess capacity. And while it would have been impossible, at the peak in early 2000, to tell anyone that the S&P 500 Tech sector would then endure a two-year -80% bear market, that is exactly what ended up happening. There are clear differences between now and then, but the storyline is that all manias end up confronting the classic Bob Farrell rule #1 on mean reversion.

* The market is not broadening out. Breadth remains weak and the equal-weighted S&P Index is only +3% year-to-date (at last Friday's close).

* Traditional valuation metrics are generally in the 90% tile or higher.

* The breathtaking reset in valuations (since October) could mean reverse.

From Rosie:

Regarding the consensus earnings forecast for 2024, it is unchanged since mid-October at $244.80. For 2025, the consensus in mid-October was $270.18 and now is sitting at $277.07. That is the grand total of a 2.6% increase in profit views for next year. What has the S&P 500 done since that time? Try +26%! A 10x surge relative to earnings expectations. So, no — this has been and remains a multiple driven market. It definitely is not an earnings-driven market, despite what the talking heads on bubblevision tell you...

* Interest rates are likely to remain higher for longer. For the short- to intermediate- term, higher rates will provide more competition to historically high equity valuations as they will continue to provide equity-like returns with no risk nor volatility.

* Equities have rarely been as overvalued against interest rates as they are today. Consider that the S&P dividend yield stands at only 1.32% compared to a 5.37% yield on the six-month Treasury note — an uncommon wide of 4x! The equity risk premium is at the lowest level in nearly two decades.

* Global economic growth is expected to be weak (relative to consensus). Elevated mortgage rates will dull housing and continue to threaten commercial real estate, the impact of stacked or cumulative inflation (since 2020) will weigh on the overly indebted consumer and the cost of capital for most companies will be rising (in the face of a maturity cliff in 2025).

* Inflation (particularly of a service-kind) will remain sticky.

* Consensus S&P EPS may be too high. Among other issues, the current move away from globalization and towards reshoring will be corporate profit dampening. Moreover, the likelihood of higher corporate tax rates seems to be rising.

* Political risks are underappreciated. Extreme partisanship will likely translate into continued fiscal irresponsibility from both parties (and a general neglect towards addressing burgeoning U.S. deficits and lofty U.S. government debt loads).

* Geopolitical risks are unlikely to abate.

* Investor sentiment remains bullish and fear is absent.

* Market structure and investor positioning are potentially toxic market influences.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.