The Déjà Vu Trade, Memory Stocks Lapse, Cybersecurity Surge

Markets move yet again on Trump’s words on Iran, my plan as storage stocks stumble, and what I’m eyeing on the S&P’s chart.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Feels like we’ve seen this movie a few times now. Is this time different? Guess we’ll know soon enough, won’t we? Monday was turning out to be a pretty rough day for U.S. financial markets. A word or two from Pres. Donald Trump late in the afternoon, turned the markets in a better direction. That’s the beauty of a keyword-driven, algorithmically run marketplace. To remove humans is to remove skepticism. Humans would question. Humans are gone. The AI behind the algos that now run our marketplace is not quite there. At least not yet.

Just a day after warning that the “clock was ticking,” Pres. Trump said that he would hold off on a planned Tuesday attack on Iran at the request of the leaders of Qatar, Saudi Arabia, and the United Arab Emirates. Supposedly, “serious negotiations are now taking place.” Front month crude oil futures came off of their highs for the session, stocks rallied off of their lows and Treasury yields relaxed just a bit. In addition, the Trump administration issued a new 30-day waiver permitting the sale of Russian crude already loaded on ocean-going vessels just days after the previous waiver had expired.

In a post to his Truth Social account, the president announced that he had directed Secretary of War / Defense Pete Hegseth and General Dan Caine not to proceed with what was apparently an attack on Iran planned for today. The president did warn that he had “further instructed them to be prepared to go forward with a full, large-scale assault of Iran, on a moment’s notice, in the event that an acceptable Deal is not reached.” In speaking to the media at an event on Monday, Pres. Trump added that the possibility for a diplomatic solution was a “very positive development, but we’ll see whether it amounts to anything.”

Memory Basket Stumbles

Memory and storage stocks appear to have apexed a week to 10 days ago, depending on the specific name. On Monday, Dave Mosley, the CEO of Seagate Technology (STX), mentioned that his company could have trouble keeping up with still rising demand for all things AI-related. STX dropped 6.9% on the day. SanDisk (SNDK) took a 5.3% hit, Micron Tech (MU) was stung for 6%, and Western Digital (WDC) tumbled 4.8%. As readers well know, I am long, but not overweight, this entire group. If one is indeed overweight, some profit-taking might be prudent just to reduce the risk. Myself, I would turn back into a buyer should this turn into a rout. Otherwise, I’m here for the ride.

Cybersecurity: To the Moon!

Just six weeks ago, sentiment for cybersecurity stocks was broadly negative. Palo Alto Networks (PANW) was up 1.9% on Monday to close at $247.55, which is an all-time high for that stock. PANW has run 34.8% since the closing bell on May 6. PANW is up 68.3% since the close of March 27. Incredible.

Long-time Sarge fave CrowdStrike (CRWD) popped for a gain of 4.2% on Monday, closing at $618.83. This, too, was an all-time high. CRWD is up 32.2% since the close of May 6 and up 63.3% since the close of April 10. Other cybersecurity stocks such as Fortinet (FTNT) and even Zscaler (ZS) have rallied as well, though one can make the case that ZS has lagged the group, but leadership appears to be focused upon Palo Alto and CrowdStrike.

Cybersecurity stocks had struggled mightily along with much of the software space though the early part of 2026 as fears that AI would disrupt entire industries. The fact is that Wall Street sees global cybersecurity spending exceeding $520 billion for the full-year 2026, up from $260 billion five years ago. The artificial intelligence-focused security subset alone is seen ramping from about $26.5 billion as recently as 2024 to more than $234 billion by calendar year 2032.

Now, with AI as a potential tailwind rather than an industry disruptor, Wall Street has had to rapidly catch cybersecurity up to the rest of the market and the street’s chosen couple of names, at least for now, seem obvious — memory/storage and cybersecurity. Is that the peripheral, inelastic-demand focused AI play? That’s the music I’m dancing to for now.

Marketplace

Markets rallied late Monday afternoon off of the president’s words to the point where the major equity indexes only suffered light losses. The S&P 500 gave up only 0.07%, while the Nasdaq Composite after stumbling through something of a rotation out of tech, gave up a more substantial 0.51%. The Dow Transports? Gained 0.41%. Small Caps? The Russell 2000 lost 0.65% but the S&P 600 gained 0.3%.

Seven of the 11 S&P sector SPDR ETFs actually ended the Monday session on the green with energy (XLE) out in front. Defensives did outperform both cyclical sectors and growth. Technology (XLK) placed last of the 11, giving up 1.08% for the day. Within tech, the Dow Jones U.S. Software Index gained 0.8% (thanks cybersecurity) while the Philadelphia Semiconductor Index lost 2.47% (thanks, memory & storage).

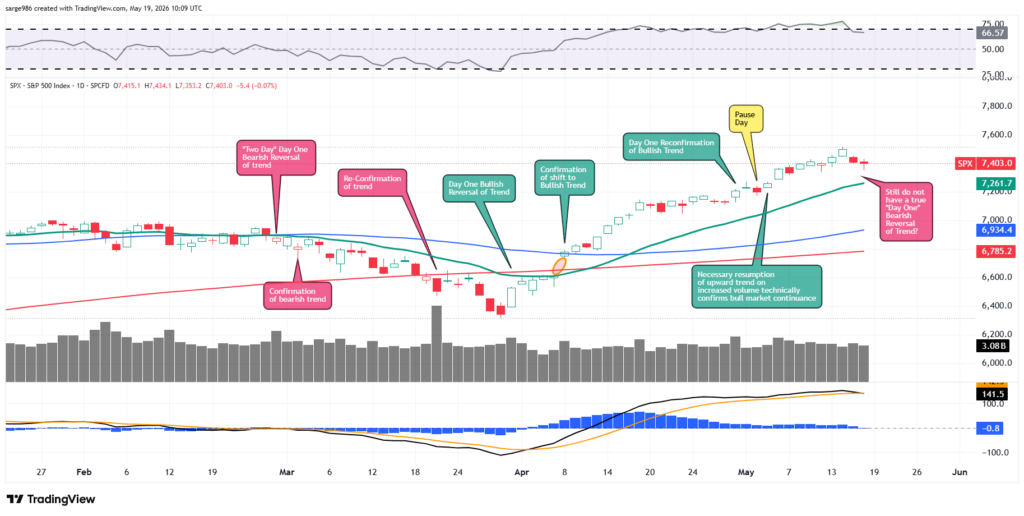

So, How Was The Breadth?

The truth is that market breadth was not really that bad at all. Remember, we doubted here what many saw as a “Day One” bearish reversal of trend on Friday. On Monday, winners beat losers at the NYSE by a seven-to-five margin and by a five-to-four margin across the Nasdaq. That’s right, winners beat losers on Monday at both exchanges. Advancing volume took a 60.2% share of composite NYSE-listed trade for the day as well as slightly more than a 50% split of composite Nasdaq-listed activity. Uh-huh. That’s right, advancing volume took a majority share of the action for names listed at both exchanges.

So… we still do not have what I would call a true “day one” bearish reversal of trend. Maybe today? That probably depends on what happens in western Asia. The problem that I see right now is a daily moving average convergence divergence for the S&P 500 that has just suffered a bearish cross-under of its 26-day exponential moving average by its 12-day EMA and a histogram of its 9-day EMA that has just crossed below the “zero bound.” These technicals are not yet decisively bearish, but do require some close watching, especially with Nvidia (NVDA) reporting tomorrow.

Economics

(All Times Eastern)

08:15 – ADP Employment Change (Weekly): Last 33K.

08:55 – Redbook (Weekly): Last 9.6% y/y.

10:00 – Pending Home Sales (Apr): Expecting 1.4% m/m, Last 1.5% m/m.

4:30 p.m. – API Oil Inventories (Weekly): Last -2.188M.

The Fed

(All Times Eastern)

09:00 – Speaker: Reserve Board Gov. Christopher Waller.

5:00 p.m. – Speaker: Philadelphia Fed Pres. Anna Paulson.

7:30 – Speaker: Interim Atlanta Fed Pres. Cheryl Venable.

Today’s Earnings Highlights

(Consensus EPS Expectations)

Before the Open: EXP (1.57), HD (3.41)

After the Close: TOL (2.58)

At the time of publication, Guilfoyle was long STX, SNDK, MU, WDC, CRWD, NVDA equity.