Doug Kass: Excuse Me While I Shoot Holes in the EPS Growth Argument

The consensus around the '26-'27 earnings per share growth argument is looking pretty suspect.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"A consensus means that everyone agrees to say collectively what no one believes individually."

- Margaret Thatcher

Nothing is more obstinate than a fashionable consensus.

Here is the conventional, consensus and linear bullish view from Ed Yardeni; it is repeated on Fin TV from 6 a.m. and throughout every trading day:

Ed Yardeni: "The stock market balloon is climbing higher, and the burners are firing. It isn't all hot air that is lifting stock prices. It's also earnings revisions, which are increasing for 2026 and 2027. Growth stocks and the Magnificent-7 have reasserted leadership over the…

— David Kass (@DrDavidKass)

Pointing to unprecedented growth in AI capital spending, most market observers that appear in the business media make several bullish points:

* The expected rate of growth in S&P 2026-2027 earnings per share has increased since year end.

* Price earnings ratios have resulted moderated and equities remain inexpensive.

One factor and simplistic market models and views like these are tempting for most to digest.

My more ursine argument is grounded in the notion that:

* The projected earnings per share gains over the next 12 months is dramatically skewed toward the contributions from large-cap technology. (It is not only the U.S. economy that is K-shaped, especially in a continued narrowing of leadership in profits and price appreciation)

* Indeed, taking out the forecast EPS contribution of Micron (MU) and Nvidia (NVDA) halves the 2026 S&P EPS from about +16% to under +10%.

* Consider the knock-on ramifications of the explosion in AI cap spend on American industry's non-hyperscaler companies -- the enormous construction outlays (think Caterpillar (CAT) et al), the added use and need for building materials (think infrastructure expense), massive energy usage, etc. and their contribution to S&P companies' top and bottom lines. Is the extraordinary AI spend sustainable or does it result in a slowdown producing an inevitable downturn in non tech sector revenues and operating profits? (I would consider this skeptical view as my baseline expectation).

* Speaking of energy companies' profitability, the Iran war has materially elevated the price of crude oil, and, along with tech companies, has contributed to the large gains in projected 2026 S&P profits. There is a universal view that the price of oil will fall meaningfully when the conflict in Iran is resolved. It follows that the large contribution of energy sector profits to 2026 S&P operating results will then be reversed in 2027. I am not aware of any investment strategist that is accounting for this reversal next year.

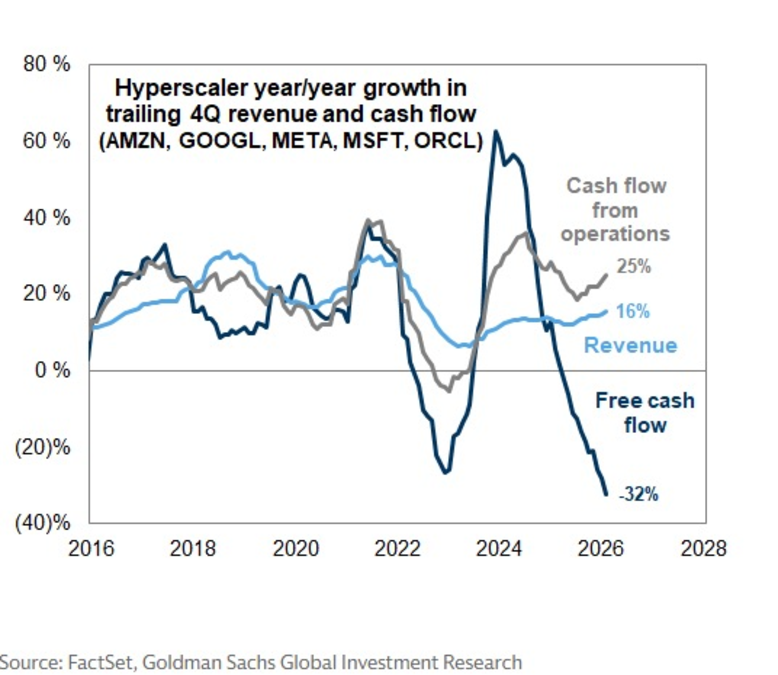

* AI capital spending is contributing to a rapid rise in debt at hyperscalers (and future interest costs) and plummeting free cash flow, it is not likely sustainable unless customer user sets/applications of AI improve rapidly and drive return on invested capital from that cap ex:

And then what? Are they really have products to sell with the large number of data centers not finished? Given the debt they put on, will interest expense soar. Will the accountants finally get after them for their circular finance deals

— nancy (@langwiser)

* Who and how demanding will be the buyers of hyperscaler debt?

As FCF rolls over

— Robert (infra 🏛️⌛️) (@infraa_)

Who’s going to buy the hyperscaler deb?

Euro/Asia driven into deficit (net debtor) from doubling of energy and GCC is driven rapidly into deficit due to SoH & have $50B of repairs

Maslow hierarchy of needs- GOOG debt, or food, energyhttps://t.co/hmkdSuREme

Leveraged speculators and investors have been the marginal buyers of AI related debt. That's why the US Treasury & the Fed are climbing all over the SIFI's books. Take a look at C&I lending - surging > inventory growth means backstops (revolvers) are kicking in.

— Robert Parenteau, CFA (@MacroEdge1)

Narrowing Continues

On Friday the S&P Index traded to a new high with less than 40% of the equities higher on the day:

The S&P 500 $SPY rallied at least 0.25% to a new high.

— Jason Goepfert (@jasongoepfert)

Not even 40% of its stocks rose on the day.

This has happened two other times since 1962. LOL, make of it what you will. pic.twitter.com/2WJkbcn7CA

As noted last week, the U.S. Stock Market's leadership is narrowing:

BY DOUG KASS · Apr 29, 2026, 7:10 AM EDT

The Market's Advance Is Narrowing

While investors/machines cheer the multi-week rally — and ignore higher inflation/interest rates/price of oil, plummeting confidence reads, the lack of fiscal discipline (manifested in a continued rise in the deficit and the aggregate U.S. debt load), still elevated valuations, improvisational policy in Washington D.C., bonafide questions regarding AI capital spending (and their anticipated returns etc.) — there are some signs of internal market weakness.

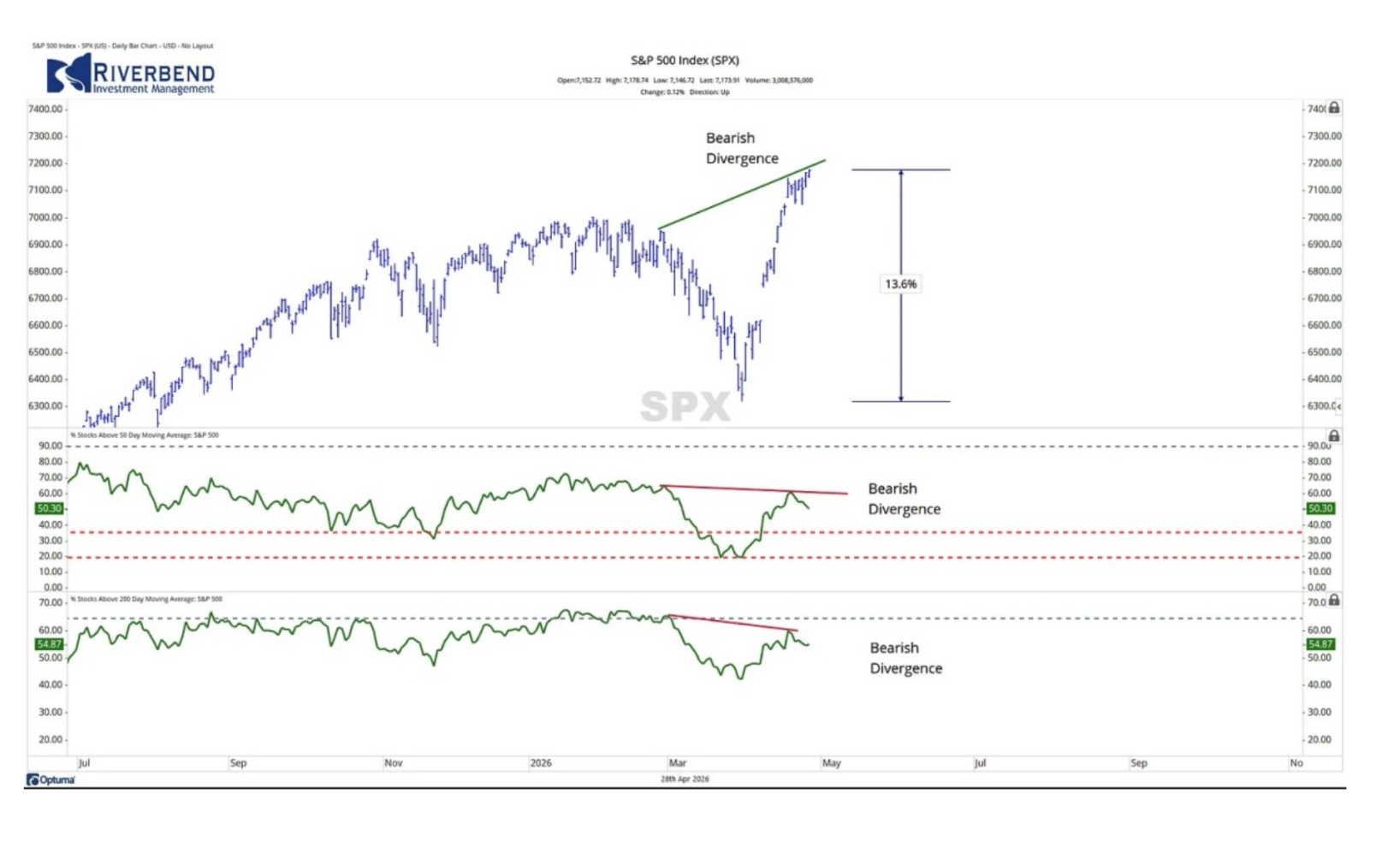

Specifically, fewer stocks are providing leadership. Here are three examples of the narrowing:* The number of stocks above their respective 50-day and 200-day moving averages is declining while the index continues to rise.

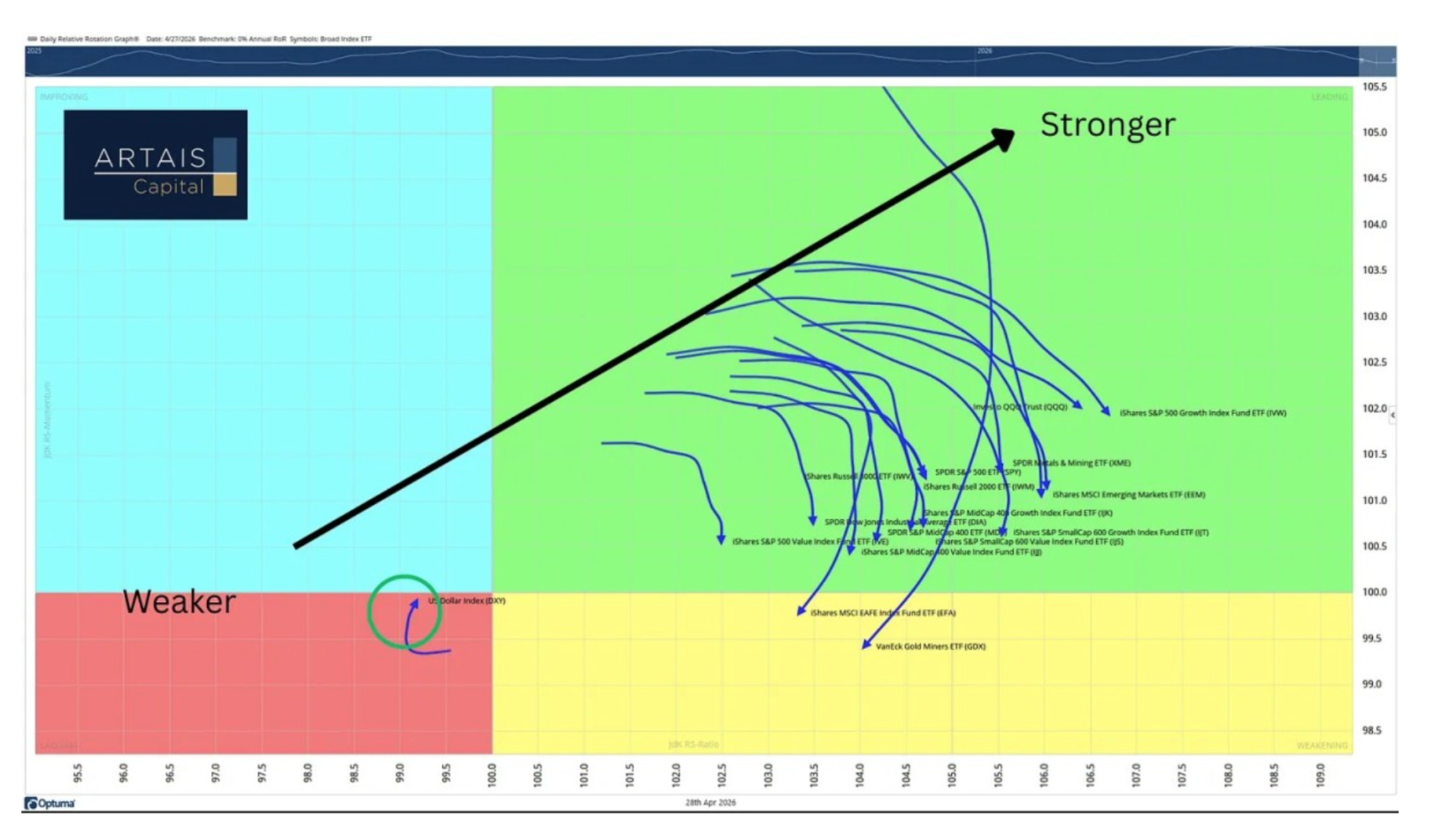

*Large-cap, mid-cap, and small-cap stocks are all rotating towards the “weakening” quadrant, indicating a loss of upside momentum:

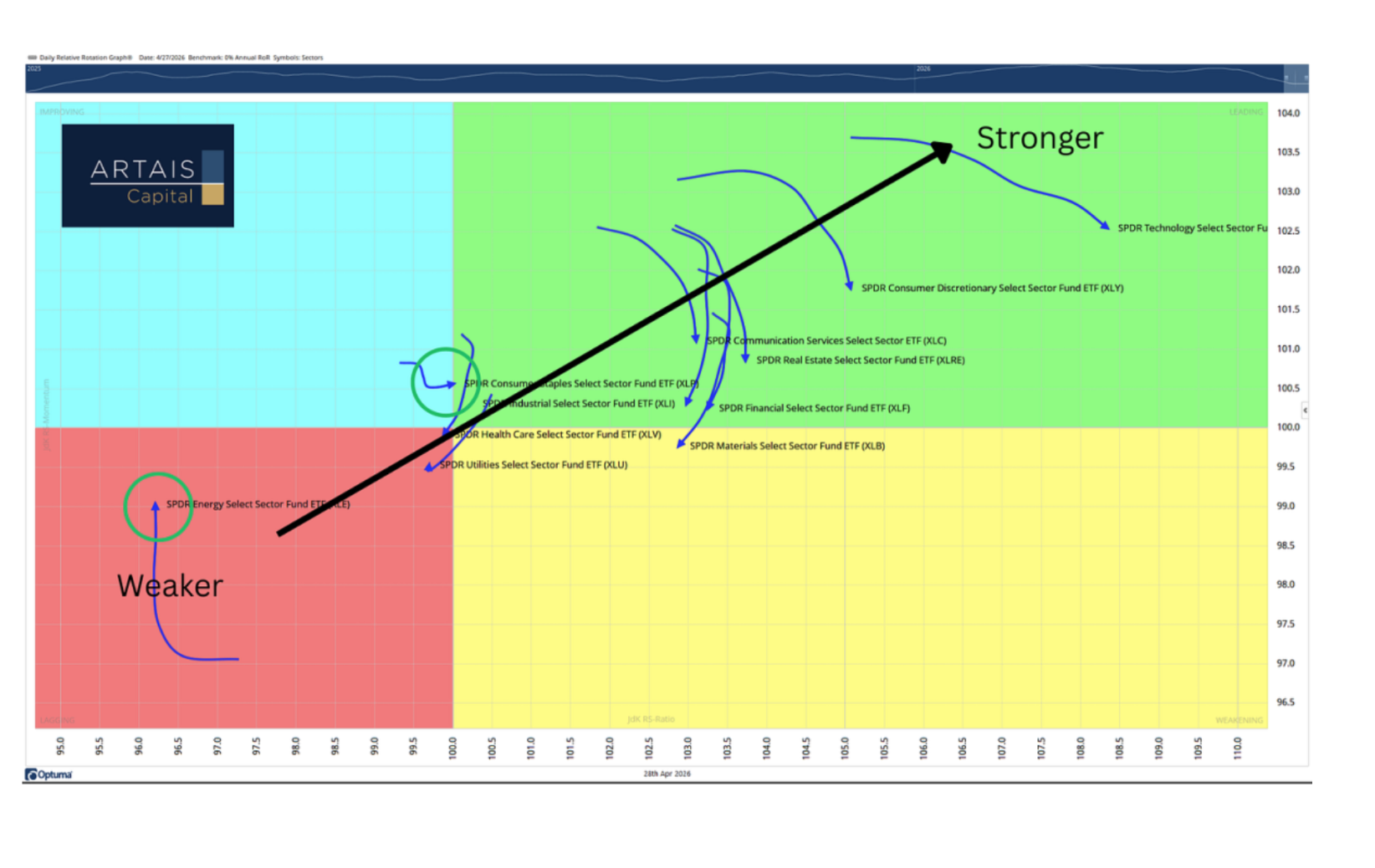

* Nine of the 11 sectors that make up the S&P 500 are also showing signs of weakness, with only the Energy and Consumer Staples sectors showing improvement:

Bottom Line

Interest rates, inflation and the price of crude oil have made multi-month highs, and appear likely to remain higher for longer.

Moreover, as pointed out, with such narrowing dispersion of investment performance and concentration of operating profits in a handle of stocks, what could possibly go wrong?

Related: 3 Key Charts I'm Watching as We Gauge the Health of the Market

At the time of publication, Kass was short SPY (VS).