CrowdStrike's Striking Day, Losing Streak Over? Powell on the Hill, Beige Book

Are portfolio managers unsure of themselves right now? I think a lot of them probably are.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Equity markets closed broadly higher on Wednesday. Huzzah! For joy, for joy.

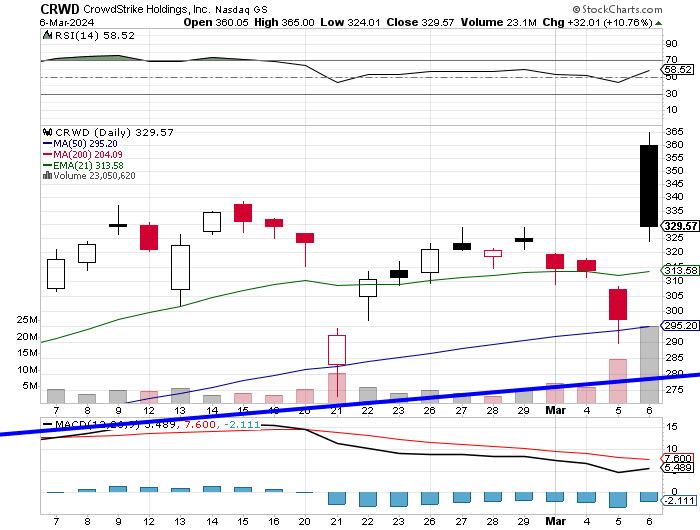

While it's true that domestic financial markets absorbed Fed Chair Jerome Powell's appearance before the House Financial Services Committee and the release of the Fed's latest Beige Book quite well on Wednesday, it's also true that the rally honestly came about just as much in response to CrowdStrike'sCRWD Tuesday evening earnings release and guidance, which were excellent.

CrowdStrike opened much higher on Wednesday morning as did U.S. markets and as the day wore on, enthusiasm for those higher prices appeared to wane...both for CrowdStrike and for U.S. equities at large. So, it is safe to say that while we broadly crossed the finish line in the green on Wednesday, it would not be accurate to say that the negativity of the day prior, and certainly not of the two days prior, had been completely unwound.

The S&P 500 gained back 0.51% for the Wednesday session, as the Nasdaq Composite took back 0.58%. Tech, of course, was hot, but not led by software, as one might have expected. Sure, CrowdStrike ran 10.76% on the session, after having been up more than 22% early. Sure, Palantir TechnologiesPLTR ran 9.87% after beating out RTX RTX , the old Raytheon, for a key U.S. Army contract. Sure, MicroStrategy MSTR took back 18.57% after selling off sharply on Tuesday as that firm found a way to finance future additions to its Bitcoin holdings, but the Dow Jones U.S. Software Index gained just 0.53% for the day.

The strongest slice of the market, below the sector-wide level, was again the semiconductors. The Philadelphia Semiconductor Index popped 2.42%. Taiwan Semiconductor TSM led the way, up 4.89%, followed by Skyworks Solutions SWKS and Qualcomm QCOM as those two gained roughly 4% each.

Powell on the Hill

The Fed Chair surprised no one on policy Wednesday morning, which is probably a good thing. Powell stuck to his 2024-to-date narrative that while there has clearly been progress made in the fight against consumer-level inflation, there are risks associated with acting too early or too late.

Powell told legislators that while the Fed Funds Rate has likely reached its peak for this cycle, the FOMC would still like to have a "greater confidence" that the central bank's 2% target was indeed reachable and in fact, probable before reducing short-term rates could be considered.

Where Powell may have surprised legislators and viewers a bit was not relative to any prospective changes made to monetary policy, but on the regulatory side. The Chair said that the Fed would likely make "broad and material changes" to proposals made to rewrite banks' (especially large banks) capital rules.

Powell, of course, was referring to the Fed's U.S. interpretation of the capital reserve standards put together by the Basel Committee on Banking Supervision. The proposals, referred to globally as Basel III, would require larger U.S. banks to hold greater reserves to protect against losses in an economic downturn. The U.S. interpretation has met with criticism by legislators as it is considered to be stricter than is the interpretation made by other developed countries and the Fed is apparently working on what changes it would consider to be fair to U.S. banks.

The Macro

The recent spate of weakening U.S. macroeconomic data continued on Wednesday. The ADP Employment Report for private payrolls showed job creation of 140K positions for February, up from just 111K positions in January, but below the 150K expected by economists. The ADP Report, which is far less volatile than the BLS survey results, especially since being reworked last year, is averaging just 127K new jobs per month over the past six months.

I hear quite a bit of criticism of this report as it has been a poor predictor of the BLS result every month. While both are seasonally adjusted, has anyone considered that the perspective could very well be seen more accurately the other way around? Perhaps, just perhaps, a data-based approach might be more accurate than surveying small samples and then extrapolating those results? Seems like common sense to me. Especially when the ADP numbers seem to be more in line with professional consensus on job creation every month than do the BLS numbers.

Later on, the BLS released January data on JOLTs job openings and quits. Job openings for January continued with the overall downward trend that had been in place, printing at a three-month low of 8.863M, which was below the 8.9M expected by economists.

The real shocker was in job quits, though. At just 3.385M quits, the American workplace was the most stable on the supply side that it has been since August 2020. The quit rate is now below pre-pandemic levels. This is an indicator that employees with jobs are a lot less sure of being able to replace that job with one of equal value if lost. Put bluntly, this is a sign of a weakening labor market.

About the Beige Book (and About Myself)

Those looking for stability loved this Beige Book. The takeaway, nationally, from this anecdotal collection of economic information gathered since the last FOMC policy meeting on January 31, showed some quiet strength. Nothing to get excited about, but certainly not the kind of deterioration that I am prone to see in the data.

Admittedly, and if you read me often, you have probably recognized this, I do have a negative-leaning bias when looking at economic data. I can't help but notice even the not-so-pretty divots in otherwise good-looking numbers. I see them. I can, however, acknowledge this bias to readership so that new readers can fully understand my point of view, especially when compared to the Pollyannish view of the economy often offered up elsewhere in the financial media (without the admission of bias).

In the Beige Book's Own Words:

On...

Labor Markets... "Employment rose at a slight to moderate pace in most Districts. Overall, labor market tightness eased further, with nearly all Districts highlighting some improvement in labor availability and employee retention."

Inflation... "Price pressures persisted during the reporting period, but several Districts reported some degree of moderation in inflation."

From...

Boston... "Economic activity increased at a slow pace, and employment gains were modest."

New York... "Regional economic activity flattened after a period of sustained weakness."

Philadelphia... "Business activity resumed a slight decline during the current Beige Book period."

Cleveland... "District business activity increased slightly."

Richmond.... "The regional economy saw little growth, overall."

Atlanta... "Economic activity was little changed. Labor markets and wage pressures eased."

Chicago... "Economic activity increased modestly. Employment increased modestly."

St. Louis... "Economic activity has increased slightly since our previous report."

Minneapolis... "District economic activity was up slightly. Employment grew some, but labor demand softened."

Kansas City... "Economic activity in the Tenth District was stable. Job gains were moderate."

Dallas... "Economic activity expanded modestly. Wage growth was moderate."

San Francisco... "Economic activity grew slightly, employment levels rose slightly."

Good News!

I guess. For the short term.

The House of Representatives on Wednesday passed a $460B package full of spending bills that will keep key federal agencies funded throughout the remainder of this budget year (September 30). The vote went 339 to 85, which was crucial, because a two-thirds majority was needed to pass.

This package now heads to the Senate where a vote is expected by Friday as the House takes on a second package of six bills that includes defense spending, which if passed would keep all federal agencies fully funded ahead of a March 22 deadline. If all passes, we are still looking at total discretionary spending of $1.65T for the full year.

Like I said. Good news. Sort of. For now.

Caution?

I know. I know. Markets were broadly higher on Wednesday. Ten of the 11 S&P sector SPDR ETFs closed in the green but led by two defensive sectors, the Utilities XLU and the Staples XLP . FYI: Discretionaries XLY , were the only fund among the 11 to close in the red.

Winners beat losers by about 5 to 2 at the NYSE and by roughly 3 to 2 at the Nasdaq. Advancing volume was good, taking a 72.4% share of composite NYSE-listed trade and a 62.6% share of composite Nasdaq-listed trade.

This is where the kick in the pants comes from. Aggregate trading volume was only higher by a smidge across NYSE-listed securities and across the S&P 500. Now, and this could be important if this rally stalls, aggregate trade decreased close to 13% on a day-over-day basis across Nasdaq-listed securities as well as across the Nasdaq Composite. That means that on an "up" day, trading was lighter across the Nasdaq than on either of the two prior "down" days. Are portfolio managers unsure of themselves right now? I think a lot of them probably are.

Check this out as well. CrowdStrike was the catalyst for at least the early part of Wednesday's rally. I wrote this article in support of CRWD, it's been a darling name of mine for a while.

I increased my price target on Wednesday but look at Wednesday in isolation:

CRWD stock opened near the top of the day's range and closed near the bottom. For the short-term at least, this likely means that investors saw those early prices as overly inflated and took quick profits.

The stock stabilized at around 11:30 ET and hung tough over the final four and a half hours of the regular session. That's a positive, but the sharp rejection at the more elevated levels has to be noted and will be by those chartists who help write the algorithms used by the powers that be.

I'm still a CRWD bull, just food for thought.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly):Expecting 214K, Last 215K.

08:30 - Continuing Claims (Weekly):Last 1.905M.

08:30 - Balance of Trade (Jan):Last $-62.2B.

08:30 - Non-Farm Productivity (Q4-rev):Flashed 3.2% q/q.

08:30 - Unit Labor Costs (Q4-rev):Flashed 0.5% q/q.

10:30 - Natural Gas Inventories (Weekly):Last -96B cf.

15:00 - Consumer Credit (Jan): Last $1.56B.

The Fed (All Times Eastern)

10:00 - Speaker: Federal Reserve Chair Jerome Powell.

11:30 - Speaker:Cleveland Fed Pres. Loretta Mester.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: AEO (0.50), BJ (1.06), BURL (3.30), CIEN (0.47), KR (1.13), TTC (0.66)

After the Close: AVGO (10.42), COST (3.63), DOCU (0.65), GPS (0.24), MDB (.48)

At the time of publication, Guilfoyle was long CRWD and PLTR equity.