Commodity Rundown: Spikes in Oil Volatility Are Imminent

The energy markets have been low on "energy," but that might change in the weeks ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I don’t know much, but I do know to take note when markets become too quiet. Markets are living, breathing things that survive on human emotions for price discovery. As we are all reminded of daily by a crazy uncle, a parent or a child, humans are emotional creatures. We go through lulls, but eventually, something triggers us into misbehaving. This tendency bleeds into the financial and commodity markets, so when things are unusually calm, it is time to prepare for the unknown. In summary, humans and the markets are ticking time bombs; we should always position ourselves accordingly.

The oil market has been mostly hugging its 200-week trendline for roughly eight months. As a result, the implied volatility built into the oil options market, akin to the “oil VIX,” is at one of the lowest levels in history (see the included CVOL chart from the CME). To be fair, this was necessary to wipe out the frothy option market that came with the Russian invasion of Ukraine in 2022. For most of 2022, the oil options market was broken; speculators bought call options in bulk at impossible strike prices. For instance, at one point, the masses were paying four figures for the right to buy oil at $200 per barrel a few months later, or several hundred for the right to buy oil at $300!

Anyone who was long call options going into the war-triggered volatility event in 2022 was rewarded handsomely. Since then, buying oil options has been a mostly losing proposition due to the collapse in market volatility. On the other hand, option sellers have likely done very well over the last few years. Yet, as mentioned above, humans are emotional beings, and the calm won’t last forever. This is one of the best times in history to be an oil option buyer; likewise, it is one of the worst times to be an oil option seller.

Spikes in oil volatility are imminent, but the direction is uncertain. Prior to the 2022 volatility event, oil traders learned that, unlike stocks, which experience more downside volatility than upside, the oil market is an equal opportunity destroyer of wealth. Thus, perhaps being long (cheap) out-of-the-money strangles (both calls and puts) with plenty of time to expiration makes sense. Or, if you have a directional bias, as we do, you can pick one side and see what happens. We lean toward buying December calls with strikes in the high $80.00s. This offers traders a way to get into the oil market, with plenty of leverage and low and limited risk, at one of the most opportune times to be long volatility. If you are a bear, it is probably worth having long puts just in case the bottom falls out.

The weekly oil chart offers primary trendline support near $70.00 and secondary trendline support near $74.00. If you are a bull, there will be two areas to watch. As long as these levels continue to hold, we should take another crack and an upside breakout; look for resistance at $83.00 and again at $85.00. If so, $100.00 is in play once again. In our view, positive seasonality, global tensions and the declining U.S. rig count favor the upside in the coming months. If we are wrong, failure at $70.00 would likely see a repeat of the 2020 decline into the $30.00s (but probably not the temporary slip below zero). To clarify, the circumstances are right for low and limited-risk bullish plays, but swinging for the fence with long futures or short puts probably isn’t justified for most traders and account sizes.

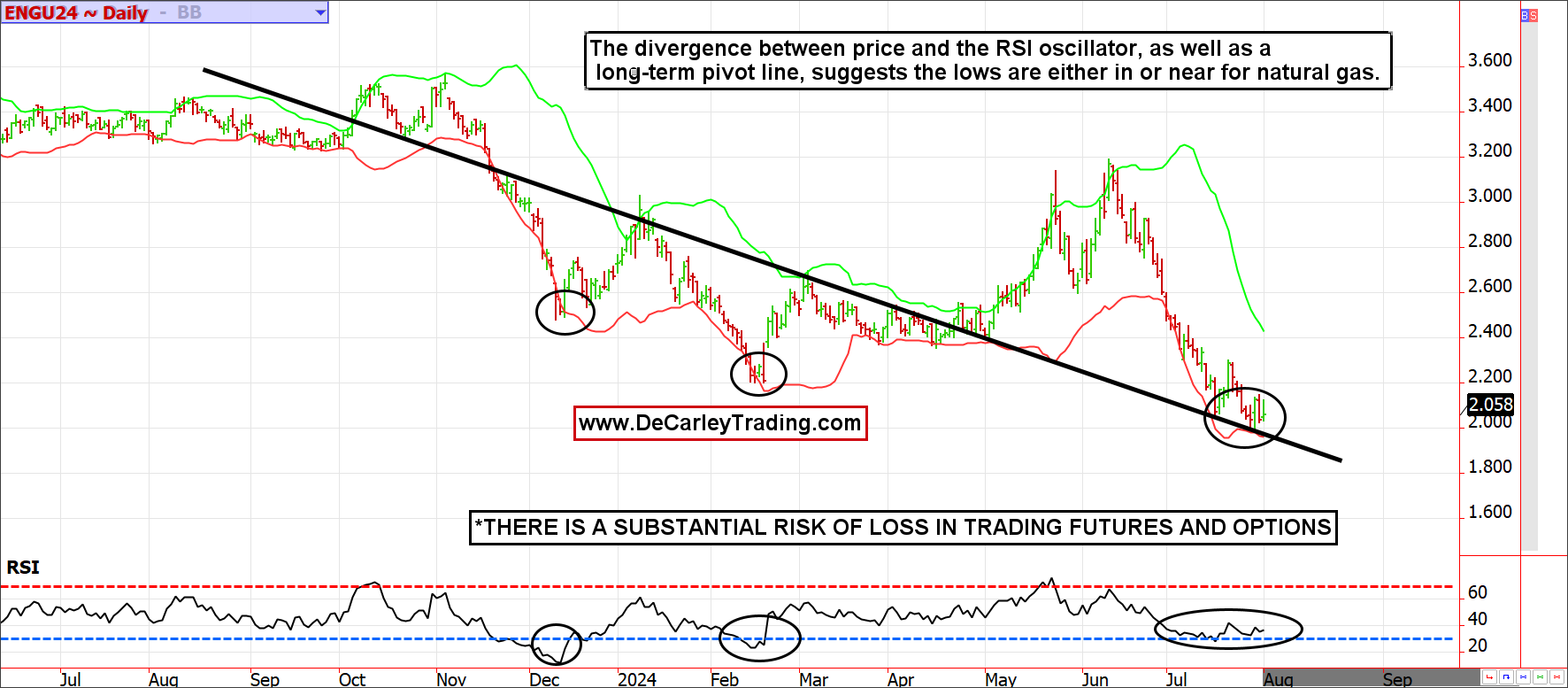

Like oil, the natural gas market has given back its wartime premium. Prior to the Russian invasion, natural gas was trading near $4.00 per 10,000 MMBtu. At the time, most market participants considered this a little rich for a market that started in the $1.50 area in mid-2020. As we now know, the gas market spent the next eight months more than doubling in price before returning to a more comfortable price level.

Before late 2021, the gas market spent a decade mostly trading between $2.00 and $4.00. We believe the gas market will return to a similar phase of lower volatility. Nevertheless, there are reasons to expect the gas market to find a bottom in the coming weeks. Even so, we should be looking for rallies to the high-$2.00s or $3.00s, not $10.00 (a price that might not be seen again in some of our lifetimes).

Also, like oil, the natural gas market has spent the last two years working off the froth in both speculation and price. Coincidentally, we are heading into a seasonally supportive time of year with prices at a significant psychological pivot area ($2.00) and a constructive chart. The downtrend has been dominated by a pivot line that dates back a year. Thus far, the most recent selloff has held as expected. Further, while the price of natural gas has been making lower lows, the relative strength index (RSI) has not; this is a sign of potential trend exhaustion. We are proceeding as though the gas market is in the process of bottoming, but we can’t rule out a messy decline of another 10 cents to 15 cents.

We hoped to get to the grains and ags in this piece, but we ran out of time, so look for a part three to our commodity rundown next.

At the time of publication, Garner had no position in any security mentioned.